Executive summary:

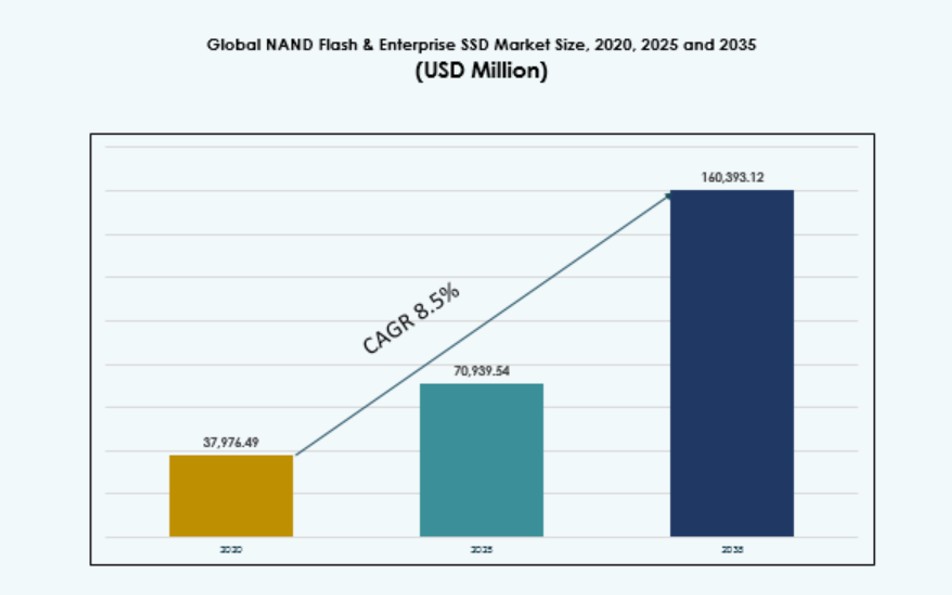

The NAND Flash & Enterprise SSD Market size was valued at USD 37,976.49 million in 2020 to USD 70939.54 million in 2025 and is anticipated to reach USD 169393.12 million by 2035, at a CAGR of 8.5% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2035 |

| NAND Flash & Enterprise SSD Market Size 2025 |

USD 70939.54 Million |

| NAND Flash & Enterprise SSD Market, CAGR |

8.5% |

| NAND Flash & Enterprise SSD Market Size 2035 |

USD 169393.12 Million |

The market is gaining momentum as enterprises accelerate adoption of high-performance storage to support cloud computing, AI workloads, data analytics and edge infrastructure. Innovation in NAND architecture, controller design and power-efficient SSD platforms improves speed, endurance and scalability. Businesses value enterprise SSDs for faster data access, reduced latency and stronger workload reliability, while investors view the market as a strategic growth area tied to digital infrastructure expansion.

North America leads the market due to strong hyperscale data center presence, advanced cloud infrastructure and early enterprise adoption of AI-ready storage systems. Asia Pacific is emerging rapidly, supported by semiconductor manufacturing strength in China, South Korea, Japan and Taiwan, along with expanding cloud and electronics ecosystems. Europe shows steady demand from enterprise modernization, automotive electronics, industrial automation and data sovereignty-driven storage investments.

Market Dynamics:

Market Drivers:

Rising enterprise data workloads create sustained demand for high-performance flash storage infrastructure

The NAND Flash and Enterprise SSD market is being strongly supported by rapid growth in enterprise data volumes across cloud platforms, AI infrastructure, analytics workloads, and digital business applications, all of which require faster storage architectures that can deliver lower latency, higher endurance, and better reliability than legacy hard disk systems. As enterprises modernize data centers, SSD adoption is becoming strategically important because flash-based platforms help reduce performance bottlenecks in real-time transactions, automation environments, and high-volume application traffic while also improving energy efficiency and rack-space utilization.

This transition is particularly valuable in hybrid cloud and edge settings, where businesses need scalable, resilient storage that can maintain service continuity and support rising data access requirements without compromising operational productivity. Investors also view this shift as structurally important because enterprise storage now sits at the core of digital transformation spending, especially as AI workloads drive greater use of high-capacity QLC enterprise SSDs in server environments. For Instance, TrendForce reported that the combined revenue of the top five global NAND Flash suppliers surged 83.7 percent quarter on quarter to more than US$38.9 billion in 1Q26, driven by an exponential rise in enterprise SSD demand from cloud service providers building AI server infrastructure.

Innovation in NAND architecture and controller technology strengthens enterprise SSD performance

The NAND Flash and Enterprise SSD market continues to advance through innovation in NAND layer counts, controller design, PCIe and NVMe interface standards, and firmware optimization, all of which are improving storage density, endurance, read-write performance, and power efficiency for enterprise workloads. These advances allow enterprises to deploy faster, more compact, and more reliable storage platforms without proportionate growth in physical infrastructure, which is especially valuable in hyperscale data centers, AI training clusters, high-frequency trading systems, database acceleration, and large-scale virtualization environments.

The shift toward advanced NAND architectures is also strengthening premium demand because higher-layer products and high-capacity QLC enterprise SSDs support better error correction, stronger data protection, and lower cost per bit across data-intensive use cases. Technology providers gain competitive advantage by aligning these innovations with the needs of cloud, telecom, industrial, and AI customers, while investors increasingly favor vendors that can scale production and maintain higher-margin enterprise offerings. For Instance, TrendForce reported that by the end of 2026, NAND Flash products featuring 200 layers or more are expected to firmly establish themselves as the market mainstream, while Samsung alone generated US$13.51 billion in NAND Flash revenue in 1Q26, up 104.7 percent quarter on quarter.

Expansion of cloud, AI and edge computing reshapes storage procurement strategies

The NAND Flash and Enterprise SSD market continues to advance through innovation in NAND layer counts, controller design, PCIe and NVMe interface standards, and firmware optimization, all of which are improving storage density, endurance, read-write performance, and power efficiency for enterprise workloads. These advances allow enterprises to deploy faster, more compact, and more reliable storage platforms without proportionate growth in physical infrastructure, which is especially valuable in hyperscale data centers, AI training clusters, high-frequency trading systems, database acceleration, and large-scale virtualization environments.

The shift toward advanced NAND architectures is also strengthening premium demand because higher-layer products and high-capacity QLC enterprise SSDs support better error correction, stronger data protection, and lower cost per bit across data-intensive use cases. Technology providers gain competitive advantage by aligning these innovations with the needs of cloud, telecom, industrial, and AI customers, while investors increasingly favor vendors that can scale production and maintain higher-margin enterprise offerings. For Instance, TrendForce reported that by the end of 2026, NAND Flash products featuring 200 layers or more are expected to firmly establish themselves as the market mainstream, while Samsung alone generated US$13.51 billion in NAND Flash revenue in 1Q26, up 104.7 percent quarter on quarter.

Data center modernization and energy efficiency priorities accelerate SSD replacement cycles

The NAND Flash & Enterprise SSD Market receives strong support from enterprise data center modernization and the need for more efficient storage infrastructure. Organizations replace older storage systems to reduce latency, improve uptime and support dense computing environments. It helps data center operators lower space requirements, reduce power use and improve workload performance across critical applications. Enterprise SSDs support higher storage density, which allows operators to manage expanding data volumes without excessive facility expansion.

Energy efficiency has become a major procurement factor because data centers face rising operating costs and sustainability targets. Flash-based storage helps companies improve infrastructure efficiency while maintaining high-speed access to business-critical data. Industry shifts toward disaggregated infrastructure, software-defined storage and hybrid cloud platforms further increase the need for flexible SSD deployment. Businesses and investors view this transition as important because it links storage technology directly to cost control, competitiveness and long-term digital infrastructure growth.

Market Trends:

Shift toward higher-density 3D NAND designs and enterprise-grade storage tier optimization

The NAND Flash & Enterprise SSD Market shows a clear trend toward higher-density 3D NAND designs that help vendors improve capacity per device. Manufacturers use advanced stacking methods to raise storage output within compact form factors. It supports enterprise storage tier optimization across hot, warm and archival workloads. Buyers now assess SSDs based on endurance class, workload fit and lifecycle cost rather than capacity alone. This trend supports more precise storage deployment across cloud, finance, healthcare and telecom environments. Vendors also refine product lines for read-intensive, mixed-use and write-intensive applications. Enterprise customers prefer platforms that balance performance, cost and durability across diverse workloads. This shift creates better portfolio segmentation and stronger value positioning for storage suppliers.

Growing preference for NVMe-based platforms across mission-critical enterprise applications

The NAND Flash & Enterprise SSD Market reflects a strong shift toward NVMe-based SSD platforms across performance-sensitive enterprise environments. NVMe improves data access by using faster interfaces and more efficient command structures than older protocols. It supports mission-critical applications that need rapid response, consistent throughput and high queue depth. Enterprises use NVMe SSDs for databases, virtualization, AI model support and real-time analytics workloads. The trend also pushes server vendors to redesign storage architectures around faster flash connectivity. Cloud operators prefer NVMe-based systems because they improve resource use and service-level performance. Storage buyers now treat protocol support as a key purchase factor. This transition strengthens demand for premium SSD products with advanced enterprise features.

Rising focus on security, endurance and data integrity in enterprise storage procurement

The NAND Flash & Enterprise SSD Market is seeing stronger demand for SSDs with built-in security, endurance and data integrity features. Enterprises now place greater value on encryption, secure erase functions and firmware-level protection. It supports compliance needs across banking, health care, public sector and regulated industrial environments. Vendors focus on improving error correction, power-loss protection and thermal control to protect critical workloads. Buyers also assess write endurance more carefully because enterprise data cycles continue to intensify. Storage procurement teams prefer SSDs that reduce failure risk and support predictable long-term performance. This trend increases demand for enterprise-grade devices over consumer-class storage alternatives. It also helps premium suppliers defend margins through reliability-focused product differentiation.

Increased customization of SSD solutions for hyperscale, telecom and industrial use cases

The NAND Flash & Enterprise SSD Market is moving toward more customized SSD solutions for specific enterprise and infrastructure use cases. Hyperscale cloud providers seek tailored drives that match their server designs, workload patterns and cost targets. Telecom operators need durable SSDs for distributed infrastructure, network edge systems and low-latency service platforms. Industrial users prefer rugged storage that can handle heat, vibration and continuous operation. It creates demand for specialized firmware, endurance profiles and form factors. Vendors collaborate more closely with large customers to align storage design with operational needs. This trend changes the market from standard product supply to solution-led engagement. It strengthens long-term customer relationships and supports differentiated growth for technology providers.

Market Challenges:

Price volatility and supply-demand imbalance continue to pressure enterprise storage margins

The NAND Flash & Enterprise SSD Market faces recurring pressure from NAND price cycles, inventory corrections and uneven demand across consumer, enterprise and data center channels. Suppliers must balance capacity expansion with disciplined production control to protect profitability. It becomes difficult for vendors to maintain stable margins when oversupply drives price erosion across high-capacity SSD categories. Enterprise buyers also delay procurement during price declines, which affects near-term revenue visibility. Memory manufacturers face high capital intensity because advanced NAND production requires costly fabrication upgrades and process improvements. Smaller suppliers struggle to compete when large players use scale, technology depth and customer contracts to defend their position. Businesses must manage procurement risk carefully to avoid exposure to sudden pricing shifts. Investors need to assess company resilience across downcycles, especially firms with weak cost structures or narrow product portfolios.

Endurance limits, integration complexity and qualification delays restrict faster enterprise adoption

The NAND Flash & Enterprise SSD Market must address technical challenges tied to endurance, workload compatibility, thermal control and long enterprise qualification cycles. Customers test SSDs rigorously before deployment because storage failure can disrupt critical business operations. It creates a long sales cycle for vendors that target hyperscale, financial services, telecom and health care environments. Enterprise workloads vary widely, so one SSD design may not meet every performance, endurance and reliability requirement. Thermal management remains important because high-speed SSDs can lose performance under sustained workloads. System integration also becomes complex when enterprises combine flash storage with legacy infrastructure, hybrid cloud systems and software-defined platforms. Data security, firmware stability and power-loss protection require constant validation. These challenges can slow adoption despite clear performance benefits and may increase development costs for suppliers.

Market Opportunities:

AI infrastructure and hyperscale cloud expansion create premium enterprise SSD opportunities

The NAND Flash & Enterprise SSD Market can capture strong opportunities from AI infrastructure, hyperscale cloud and high-performance computing demand. Enterprises need faster storage to support model training, analytics and real-time workloads. It helps cloud providers improve latency, server efficiency and service reliability. Vendors can target premium SSD tiers with higher endurance and stronger security features. Businesses gain value through faster data access and better workload continuity. Investors can track suppliers with strong enterprise portfolios and hyperscale customer exposure. Edge AI systems also create demand for compact, durable flash storage. This opportunity supports long-term growth across digital infrastructure.

Specialized SSD designs for regulated, industrial and edge environments expand addressable demand

The NAND Flash & Enterprise SSD Market can benefit from demand for customized SSD platforms across health care, finance, telecom, defense and industrial automation. These sectors need secure, reliable and workload-specific storage systems. It gives vendors room to develop rugged drives, encrypted SSDs and firmware-optimized solutions. Enterprises value products that meet strict uptime, compliance and durability needs. Telecom and edge networks require storage with low latency and stable operation. Industrial users need devices that perform in harsh environments. Businesses can reduce operational risk through purpose-built flash storage. Investors may find value in suppliers that serve specialized, high-margin enterprise segments.

Segment Analysis

Product

In the NAND Flash & Enterprise SSD Market, TLC NAND remains the dominant product category, with an estimated 45% market share, driven by its strong balance between storage density, cost efficiency and endurance. It supports broad enterprise and consumer use cases, including data centers, laptops, smartphones and storage arrays. QLC NAND continues to gain traction because it offers higher capacity at lower cost for read-intensive workloads. MLC retains relevance in performance-sensitive applications, while SLC serves specialized industrial and mission-critical systems that require high durability and reliability.

Enterprise SSD

In the NAND Flash & Enterprise SSD Market, NVMe SSDs dominate the enterprise SSD segment with an estimated 58% share, supported by high-speed data transfer, low latency and strong compatibility with modern server architectures. Enterprises prefer NVMe SSDs for cloud computing, AI workloads, databases and high-performance analytics. SATA SSDs continue to serve cost-sensitive upgrades and legacy infrastructure due to broad compatibility. SAS SSDs remain important in mission-critical enterprise systems where reliability, dual-port access and stable performance support demanding storage environments.

End user

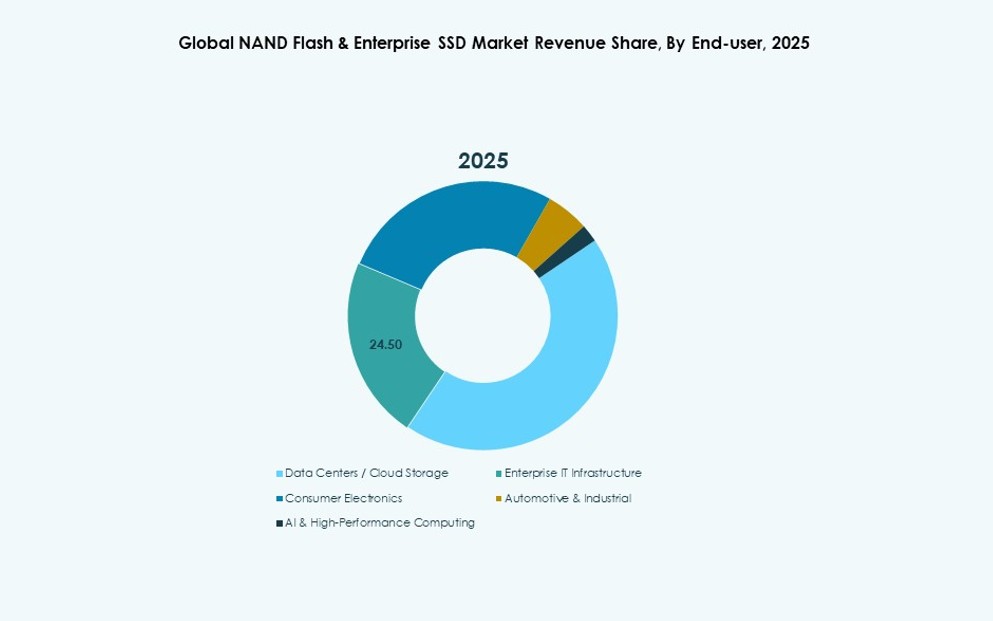

In the NAND Flash & Enterprise SSD Market, data centers and cloud storage represent the leading end-user segment, with an estimated 42% market share. Hyperscale operators, colocation providers and cloud platforms require high-capacity SSDs to support digital services, AI applications and enterprise workloads. Enterprise IT infrastructure follows with strong demand from modernization projects and hybrid cloud adoption. Consumer electronics generate volume demand, while automotive, industrial, AI and high-performance computing applications expand rapidly due to rising data processing needs at the edge and in specialized systems.

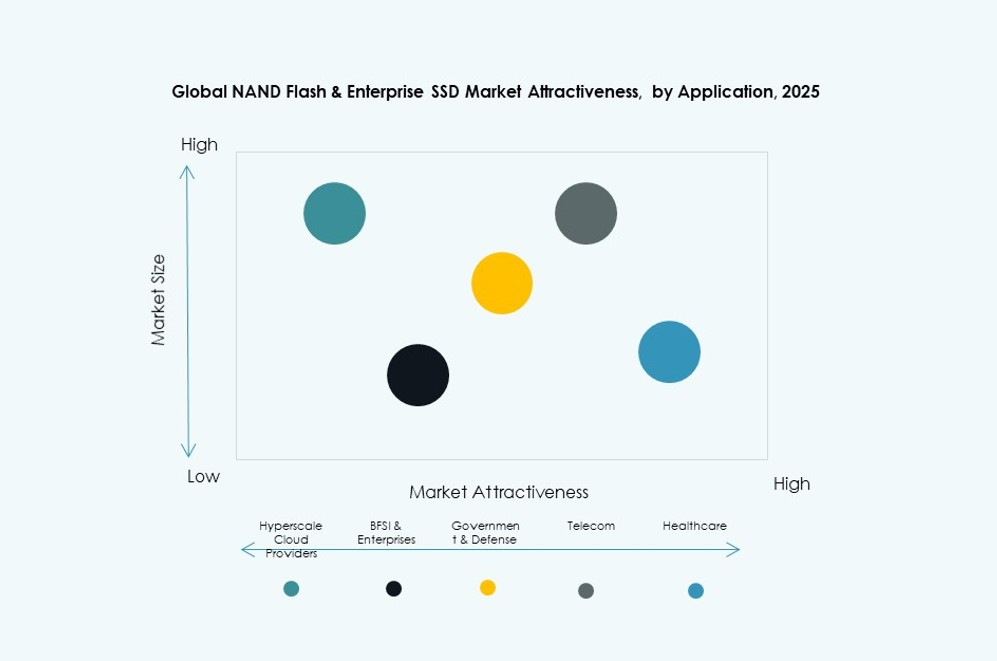

Application

In the NAND Flash & Enterprise SSD Market, hyperscale cloud providers dominate the application segment with an estimated 38% share, driven by large-scale storage demand across cloud services, AI platforms and content delivery infrastructure. These providers need high-density, low-latency and energy-efficient SSDs to improve server utilization and service performance. BFSI and enterprises also contribute strong demand because secure and reliable storage supports transactions, compliance and analytics. Government, defense, telecom and health care applications continue to expand through digital modernization and mission-critical data requirements.

Deployment

In the NAND Flash & Enterprise SSD Market, cloud and hyperscale data centers lead the deployment segment with an estimated 60% share, supported by rapid growth in cloud infrastructure, AI workloads and enterprise digital platforms. These facilities require scalable SSD systems that deliver high throughput, lower latency and better energy efficiency. On-premise data centers retain demand among large enterprises, regulated sectors and organizations with strict control over data security. Hybrid strategies also support steady SSD adoption across private infrastructure and cloud-connected environments.

Market Segmentation:

By Product NAND Flash Memory

- SLC (Single-Level Cell)

- MLC (Multi-Level Cell)

- TLC (Triple-Level Cell)

- QLC (Quad-Level Cell)

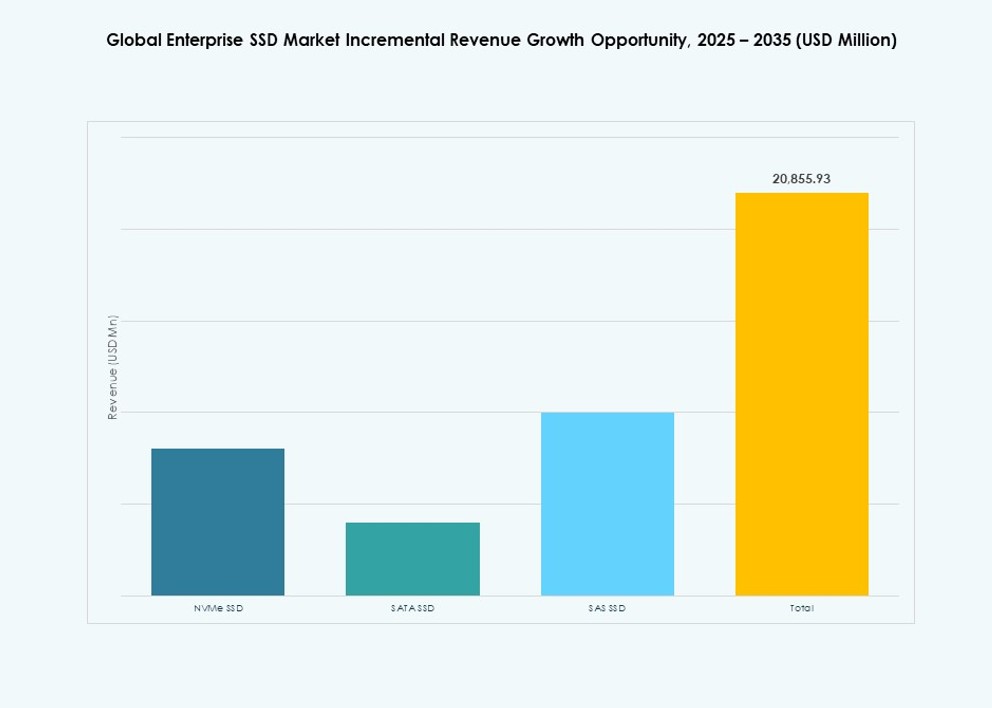

By Enterprise SSD

- NVMe SSD

- SATA SSD

- SAS SSD

By End-user

- Data Centers / Cloud Storage

- Enterprise IT Infrastructure

- Consumer Electronics

- Automotive & Industrial

- AI & High-Performance Computing

By Application

- Hyperscale Cloud Providers

- BFSI & Enterprises

- Government & Defense

- Telecom

- Healthcare

By Deployment

- On-Premise Data Centers

- Cloud / Hyperscale Data Centers

Regional Insights:

North America and Europe

North America leads the NAND Flash & Enterprise SSD Market with an estimated 38% share, supported by strong hyperscale cloud infrastructure, AI data center expansion and advanced enterprise IT spending. The U.S. drives most regional demand due to large cloud service providers, semiconductor design strength and rapid adoption of NVMe-based enterprise SSDs. Canada contributes through data center investments and enterprise cloud migration. Europe holds an estimated 24% share, led by Germany, the U.K., France and the Netherlands. It benefits from digital transformation, industrial automation, data sovereignty rules and enterprise modernization. Regional demand remains steady across BFSI, telecom, health care and public sector storage applications.

Asia Pacific

Asia Pacific accounts for an estimated 30% share and stands as the fastest-growing regional market. China, South Korea, Japan and Taiwan play a major role due to their strong semiconductor manufacturing base, electronics supply chains and expanding cloud ecosystems. South Korea and Japan support the market through advanced NAND production and technology innovation. China drives demand through cloud platforms, AI infrastructure, consumer electronics and industrial digitization. India is emerging rapidly due to data center growth, enterprise cloud adoption and digital service expansion. It benefits from rising investment in edge infrastructure, telecom networks and high-performance computing systems across major economies.

Latin America, Middle East and Africa

Latin America holds an estimated 4% share, with Brazil, Mexico and Chile leading demand through cloud adoption, fintech growth and enterprise IT upgrades. The Middle East accounts for an estimated 3% share, supported by data center investments in the UAE, Saudi Arabia and Qatar. Africa represents an estimated 1% share, with South Africa, Egypt, Nigeria and Kenya showing early-stage demand. These regions remain smaller but offer long-term potential through digital government programs, telecom expansion and cloud service localization. It gains relevance as enterprises replace legacy storage with faster flash-based systems. Growth depends on infrastructure maturity, cloud penetration and enterprise technology budgets.

Competitive Insights:

The NAND Flash & Enterprise SSD Market remains highly competitive, with Samsung, SK hynix, Micron, Kioxia and Western Digital holding strong positions through NAND production scale, process technology and enterprise SSD portfolios. Samsung leads through vertical integration, advanced NAND design and broad data center SSD offerings, while SK hynix strengthens its position through Solidigm and high-density NAND innovation. Micron competes through advanced memory technology, enterprise SSD performance and exposure to AI infrastructure demand. Kioxia and Western Digital benefit from long-term flash technology collaboration and strong storage channel access. Solidigm remains important in high-capacity enterprise SSDs for hyperscale customers. Competition centers on density, endurance, power efficiency, NVMe performance, controller optimization and customer-specific platforms. It also favors vendors that can manage price cycles, secure supply and meet strict enterprise qualification needs.

Key Players:

- Samsung Electronics

- SK hynix

- Micron Application

- Kioxia Holdings

- Western Digital

- Solidigm

- Intel

- Kingston Application

- Seagate Application

- NetApp

- Yangtze Memory Technologies

- Winbond Electronics

- Silicon Motion

- Macronix International

- Powerchip Application

- Others

Recent Developments:

- In May 2025, Kioxia announced the development and prototype demonstration of its CM9 Series enterprise NVMe SSDs, described as the company’s first enterprise drives built with BiCS FLASH generation 8 TLC 3D flash memory using CBA, or CMOS directly bonded to array, technology. Kioxia said the PCIe 5.0 SSDs were designed to deliver roughly 65% higher random write performance, 55% better random read performance, and up to 95% better power efficiency in sequential write versus its prior generation, making the launch a notable architectural leap rather than a routine refresh. This was a breakthrough innovation in enterprise NAND storage because it demonstrated how advanced bonding and next-generation TLC NAND can simultaneously improve speed, efficiency, and scalability for AI and data-center workloads.

- In August 2025, Sandisk showcased its new UltraQLC technology platform at FMS 2025 and demonstrated a 256TB NVMe enterprise SSD, which it described as a milestone in storage capacity, performance, and power efficiency. The platform combines BiCS8 2Tb QLC CBA NAND, custom controllers, and system-level optimizations such as Direct Write QLC, dynamic frequency scaling, and a new data-retention profile designed to reduce recycle events by up to 33%, while the company said its 128TB SN670 and 256TB UltraQLC SSDs would begin shipping in 2026. This was one of the clearest breakthrough innovations in the segment because it pushed QLC enterprise SSDs to a new hyperscale-capacity tier aimed directly at AI data lakes and dense cloud storage.

- In August 2025, SK hynix announced it had developed and started mass production of a 321-layer 2Tb QLC NAND device, which TrendForce described as the world’s first QLC NAND product to exceed 300 layers. The company said the product was targeted for release in the first half of 2026 after global customer validation and that it would first be used in PC SSDs before expanding into enterprise SSDs for data centers and ultra-high-capacity AI server storage. This was a major NAND breakthrough because surpassing the 300-layer threshold materially raises density and strengthens the roadmap for larger-capacity enterprise SSDs built around QLC economics.

- In April 2025, StorONE announced an expansion of its strategic partnership with Phison Electronics to deliver AI-native, on-premises storage platforms that combine Phison’s aiDAPTIV+ memory extension technology with StorONE’s high-performance storage software. The companies said the joint solution, scheduled for availability in Q2 2025, was intended to help enterprises and research teams train and deploy large language models on secure, high-throughput infrastructure with simplified conversational management. This qualified as a significant collaboration in the NAND flash and enterprise SSD ecosystem because it linked a leading NAND-controller innovator with enterprise storage software to create a more AI-optimized storage stack rather than just a standalone hardware launch.