Executive summary:

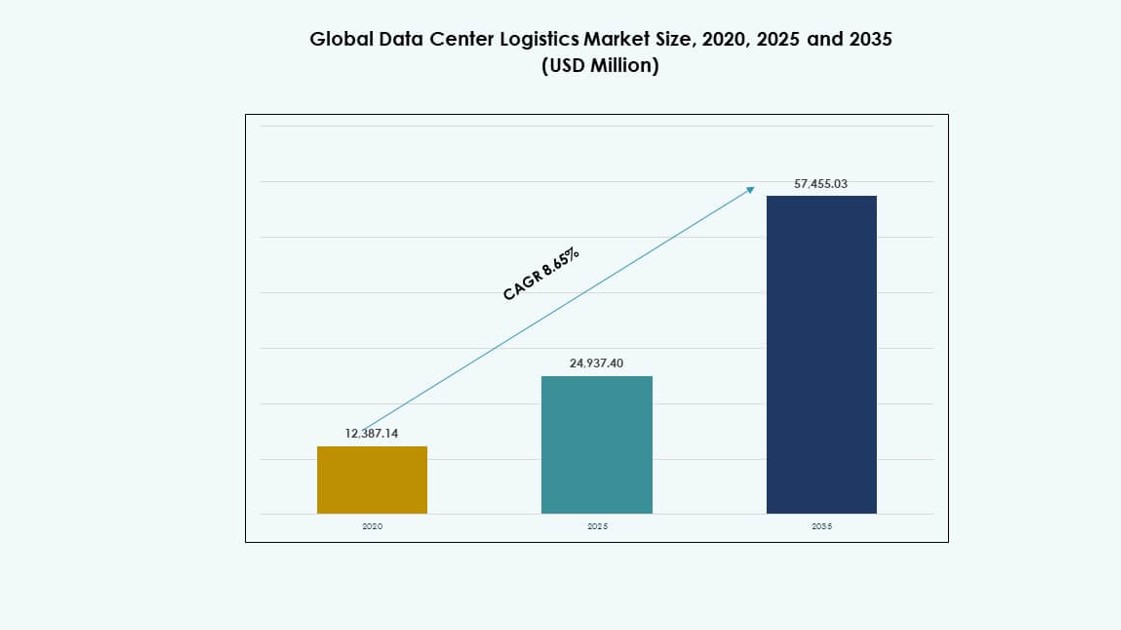

The Global Data Center Logistics Market size was valued at USD 12,387.14 million in 2020 to USD 24,937.40 million in 2025 and is anticipated to reach USD 57,455.03 million by 2035, at a CAGR of 8.65% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2035 |

| Data Center Logistics Market Size 2025 |

USD 24,937.40 Million |

| Data Center Logistics Market, CAGR |

8.65% |

| Data Center Logistics Market Size 2035 |

USD 57,455.03 Million |

Global Data Center Logistics Market expands as hyperscale and colocation buildouts push time-critical delivery of high-value IT and power infrastructure. Operators demand tighter chain-of-custody, lower damage rates, and predictable site appointments, which raises the need for specialized handling and secure staging. Control-tower platforms, real-time tracking, and exception workflows improve schedule reliability and reduce project risk. These shifts increase service depth, strengthen contract visibility, and support premium offerings that matter for business resilience and investor confidence.

Global Data Center Logistics Market remains led by North America and Western Europe due to dense data center clusters, mature carrier networks, and frequent refresh cycles. Asia Pacific emerges fast, led by India, Singapore, Japan, and Australia as new capacity ramps and cross-border supply chains expand. Gulf markets also rise with large digital infrastructure programs that require secure logistics and compliance discipline. Regional growth follows power availability, connectivity hubs, and permitting pace, which shapes where new campuses and edge sites scale first.

Market Dynamics:

Market Drivers

Hyper-Scale Data Center Buildouts And Multi-Site Expansion Demand

Global Data Center Logistics Market grows when hyperscalers and colocation operators scale footprints across multiple metros and edge zones. It raises shipment volume for racks, servers, power gear, and cabling across tight deployment windows. Buyers prioritize providers that control lead times and protect schedule certainty for go-live dates. Standardized deployment playbooks push consistent service quality across countries and sites. This driver strengthens demand for time-critical transport, bonded handling, and secure staging capacity. Investors track it because it signals durable project pipelines and repeatable logistics revenue.

- For instance, Equinix states that its xScale portfolio spans 36 facilities with expected capacity above 720 MW when fully built, and each xScale Data Hall can support more than 250 cabinets while scaling in multi-megawatt increments, highlighting why repeatable, multi-site hyperscale programs intensify demand for synchronized logistics execution.

Higher Equipment Complexity And Mission-Critical Handling Requirements

Global Data Center Logistics Market benefits from higher equipment density and tighter tolerances in modern data halls. It drives demand for specialized packaging, shock control, humidity control, and chain-of-custody compliance. Operators require loss prevention because damaged components can delay commissioning and breach SLAs. Providers win contracts when they show audited handling processes and low damage rates. It supports premium pricing for high-value cargo with monitored stops and security controls. Businesses value it for uptime protection, while investors value it for stronger margins.

- For instance, Vertiv said AI-driven rack densities are making 30 kW racks a standard baseline, with some deployments reaching 120 kW or higher, which directly increases handling sensitivity and raises the need for specialized cooling-aware transport, packaging, and installation controls.

Digital Supply Chain Control Towers And Predictive Planning Adoption

Global Data Center Logistics Market advances when operators demand end-to-end visibility from supplier dock to cage or suite. It shifts procurement toward partners that provide real-time tracking, alerts, and exception workflows. Predictive ETA logic helps teams plan labor, receiving slots, and site access windows. Buyers require integrations with ERP, WMS, and DCIM tools to align assets and deployment tickets. It strengthens demand for data-driven route choices and rapid re-routing for critical items. Investors view it as a signal of scalable, software-enabled service models.

Lifecycle Services Growth From Commissioning To Decommissioning And Circular Flows

Global Data Center Logistics Market expands when refresh cycles accelerate across compute and storage fleets. It increases movement for spares, replacements, and phased upgrades that avoid downtime. It also lifts demand for secure reverse logistics, certified disposal, and auditable destruction certificates. Integrated lifecycle programs reduce vendor count and simplify governance for operators. It increases the value of inventory control, serial tracking, and compliance reporting. Businesses and investors view it as strategic because it converts projects into recurring lifecycle revenue.

Market Trends

Standardized Modular Deployment Kits And Pre-Configuration At Origin

Global Data Center Logistics Market shows a trend toward pre-configured shipments that arrive site-ready. It shifts work upstream into kitting, labeling, configuration, and packaging validation. It reduces on-site dwell time and supports predictable installation labor plans. Repeatable module BOMs simplify receiving checks and customs classification. Sealed units reduce touchpoints and damage exposure across long lanes. Investors track it because it supports differentiation and higher service attachment.

Secure Staging Near Data Center Clusters And Just-In-Time Release

Global Data Center Logistics Market trends toward secure staging hubs near large colocation corridors. It enables JIT release that matches rack readiness, power turn-up, and labor availability. Providers expand cage-secured storage, bonded options, and appointment-based dispatch. It reduces last-mile risk and prevents early delivery congestion at sites. Multi-site allocation from a single buffer stock pool improves utilization. Investors value it because premium warehousing stays sticky once embedded.

Greater Use Of Rail-Sea Combinations For Cost Control On Non-Critical Lanes

Global Data Center Logistics Market trends toward multimodal routing to cut cost on non-critical equipment. Operators separate critical-path components from bulk infrastructure freight. Sea and rail options reduce exposure to air price swings and capacity limits. Providers offer mode-optimization playbooks that balance lead time, risk, and insurance needs. Longer lanes raise demand for moisture control and stronger packaging discipline. Investors track it because it supports cost governance and margin protection.

Contract Structure Shift Toward KPI-Linked Performance And Outcome Delivery

Global Data Center Logistics Market shows a trend toward outcome-based contracts tied to on-time, damage rate, and site readiness. Scorecards and shared dashboards tighten accountability across subcontractors and last-mile partners. Operators push SLAs for appointment adherence, staged inventory accuracy, and secure proof of handoff. Providers formalize escalation paths and recovery playbooks for exceptions. Audit packs for compliance, security, and incident reporting become standard. Investors value it because KPI-led models often support longer tenures and predictable renewals.

Market Challenges

Cross-Border Compliance, Security Mandates, And Documentation Burden

Global Data Center Logistics Market faces friction from complex customs rules, export controls, and security checks across multiple jurisdictions. It raises risk of holds when documentation lacks precision on serials, HS codes, and declared values. It also raises exposure to compliance audits for controlled components and encryption-related items. Providers must enforce chain-of-custody rigor, secure storage, and vetted carrier networks to meet operator security standards. Many sites restrict access windows, which amplifies impact from late arrivals and missed appointments. Insurance and liability disputes can rise when multiple parties handle high-value cargo. It forces investment in compliance staff, trade expertise, and standardized document workflows.

Capacity Constraints, Labor Gaps, And Schedule Volatility Around Peak Build Cycles

Global Data Center Logistics Market must manage tight capacity for specialized trucks, rigging crews, and secure warehousing near key clusters. It creates bottlenecks during simultaneous build phases across adjacent metros. It also raises wage pressure for skilled handlers who follow strict facility protocols. Port congestion, carrier disruptions, and route restrictions can break project calendars that require precise sequencing. Operators often change delivery windows based on construction readiness, which forces rapid rescheduling and increases empty miles. Provider networks can suffer when subcontractor quality varies across regions. This challenge pressures service consistency and raises risk of damage or delay events.

Market Opportunities

Integrated Control-Tower Programs With End-To-End Asset Governance

Global Data Center Logistics Market can expand through control-tower offerings that unify transport, staging, and site delivery under one governance layer. It allows KPI-based program management, exception control, and unified reporting for buyers. Providers can attach higher-value services such as serial tracking, spares positioning, and compliance documentation. It reduces vendor fragmentation for operators and improves schedule reliability. This opportunity supports long-term contracts and multi-site expansion scopes.

Lifecycle Circularity Services With Certified Data Destruction And Redeploy Paths

Global Data Center Logistics Market can grow via secure reverse flows for refresh cycles and decommission programs. It supports certified destruction for storage media and auditable chain-of-custody logs. Providers can build refurbish, redeploy, and resale channels that reduce waste and recover value. It aligns with ESG reporting needs and internal governance for large operators. This opportunity also increases recurring revenue tied to refresh cadence rather than one-time builds.

Market Segmentation

By Service Type

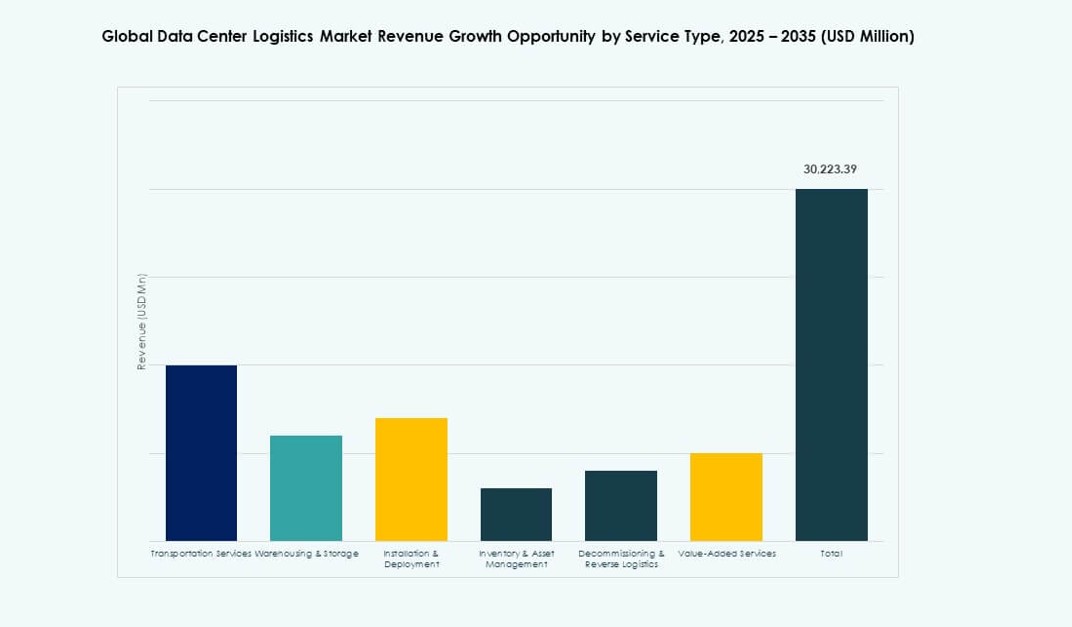

Global Data Center Logistics Market skews toward Transportation Services as the dominant segment with an estimated 34% share in 2025 due to tight deployment windows and high-value lane control. Warehousing & Storage follows at 20% as operators adopt secure staging near cluster markets. Installation & Deployment reaches 16% as white-glove delivery and rack placement gain priority. Inventory & Asset Management holds 12% as serial tracking and spares governance mature. Decommissioning & Reverse Logistics reaches 10% due to refresh cycles and compliance needs. Value-Added Services account for 8% but show faster growth where pre-configuration and testing reduce site time.

By Servers

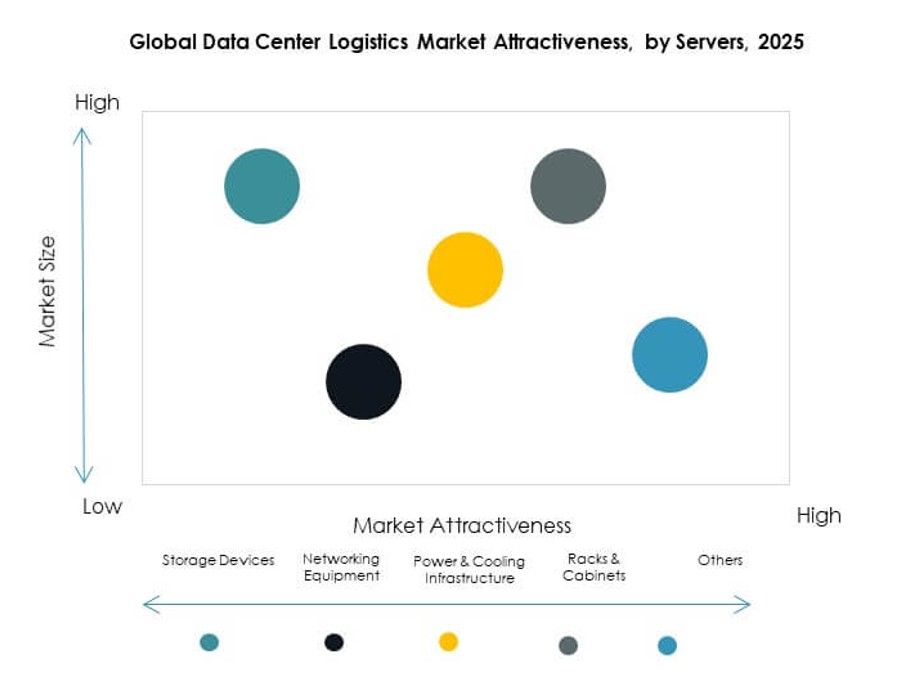

Global Data Center Logistics Market sees Networking Equipment as a leading category at 28% share in 2025 because deployments require fast integration and strict handling controls for high-value units. Storage Devices follow at 24% due to refresh cadence and capacity expansion. Power & Cooling Infrastructure holds 26% as operators expand electrical and thermal systems for higher rack density. Racks & Cabinets reach 22% with steady demand tied to new halls and fit-out phases.

By End-User

Global Data Center Logistics Market remains led by Cloud Service Providers with an estimated 36% share in 2025 due to hyperscale buildouts and frequent refresh programs. Colocation Providers hold 29% as multi-tenant campuses expand in major metros. Enterprises represent 18% with selective modernization and hybrid deployments. Telecommunications Companies reach 9% as edge and network upgrades continue. Government & BFSI holds 5% with higher security requirements and controlled procurement. Healthcare & Others account for ~3% but grow where compliance-driven infrastructure upgrades occur.

By Mode Of Transportation

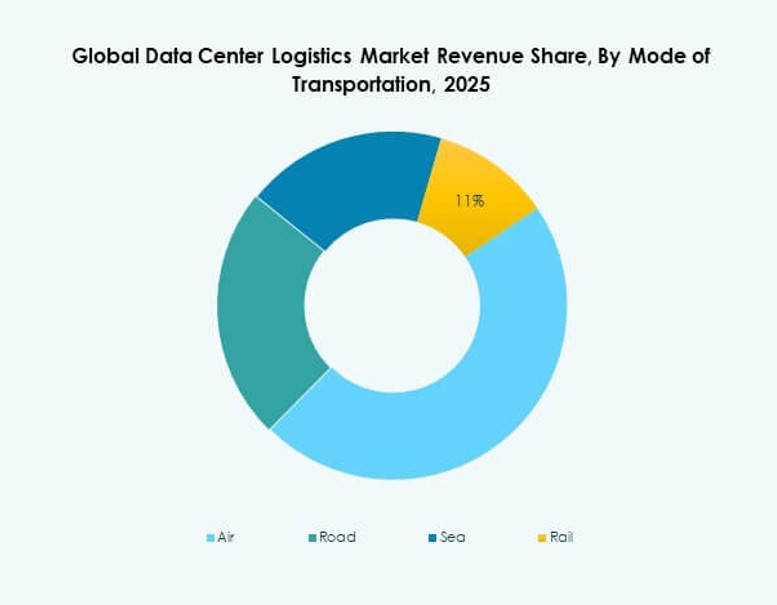

Global Data Center Logistics Market relies on Road as the dominant mode at 46% share in 2025 due to last-mile control, appointment delivery, and regional hub-to-site moves. Air holds 28% for critical-path equipment and urgent replacements. Sea accounts for 20% for bulky infrastructure and cost-managed lanes. Rail remains 6% but gains interest where intermodal corridors reduce cost and improve predictability.

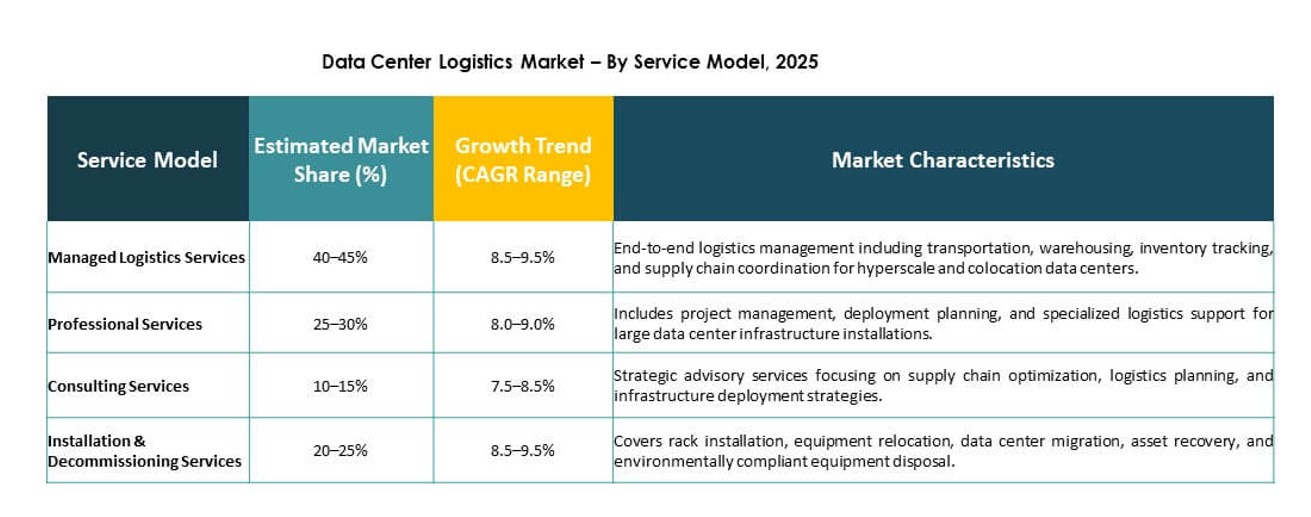

By Service Model

Global Data Center Logistics Market favors Managed Logistics Services at 41% share in 2025 because operators seek single-point accountability, KPI governance, and multi-site scalability. Professional Services hold 24% where project-based deployments require specialist execution. Consulting Services account for 13% as buyers formalize network design, trade compliance, and risk programs. Installation & Decommissioning Services reach 22% due to lifecycle activity and security-led reverse flows.

Regional Insights

North America And Latin America

Global Data Center Logistics Market remains led by North America with an estimated 38% share in 2025 due to hyperscale clusters, dense colocation ecosystems, and high refresh cadence. The U.S. drives most regional volume through multi-campus expansions and frequent equipment turnover. Canada adds steady growth tied to cloud region buildouts and cross-border hardware flows. Latin America holds ~8% share, led by Brazil and Mexico where new capacity ramps in major metros. It faces higher trade friction and variable infrastructure quality, which increases reliance on secure staging and vetted carriers.

- For instance, ODATA launched the first building of its QR03 campus in Querétaro with 72 MW of IT power, said the five-building site will scale to 300 MW, and reported energizing 200 MW in the first phase in February 2025 while deploying its Delta³ cooling system designed for power densities of up to 50 kW per rack.

Europe, Middle East, And Africa

Global Data Center Logistics Market captures 27% share in Europe, supported by strong colocation demand and cross-border supply chains across the EU. Key hubs in Western and Northern Europe drive complex multi-country lanes that favor providers with trade expertise. The Middle East reaches ~9% share as large-scale digital infrastructure projects expand and new campuses emerge in Gulf markets. Africa holds ~4% share, with growth concentrated in South Africa, Kenya, and Nigeria where connectivity upgrades support new facilities. It faces capacity gaps in specialized handling and secure warehousing in several corridors.

- For instance, NTT states that its greater London platform interconnects seven data centers and is being developed to support over 100 MW of IT load, while its Paris roadmap includes three data centers totaling up to 84 MW, with Paris 1 alone planned at 36 MW.

Asia Pacific

Global Data Center Logistics Market holds 22% share in Asia Pacific, with strong momentum from buildouts across India, Southeast Asia, Japan, Australia, and selective China corridors. Singapore, India, and Japan act as major demand centers due to dense capacity additions and high equipment throughput. Southeast Asia shows rapid expansion that raises demand for cross-border coordination and secure last-mile execution. Australia supports stable growth through multi-city cloud region expansion and modernization projects. It benefits from diversified manufacturing and supplier networks that shorten lead times for certain components.

Competitive Insights

- DHL Supply Chain

- Kuehne + Nagel

- DB Schenker

- CEVA Logistics

- UPS Supply Chain Solutions

- Nippon Express

- Schneider Electric

- Iron Mountain Incorporated

- Logistics Plus Inc.

- NTT Ltd.

Global Data Center Logistics Market shows competition between global 3PLs with secure freight networks and specialists that focus on white-glove data center moves. Large players win on geographic coverage, standardized SOPs, and the ability to scale staging near major clusters. Specialists win where operators need high-touch handling, site access compliance, and complex inside-the-fence execution. Differentiation relies on damage-rate control, appointment adherence, and audit-ready chain-of-custody. Control-tower platforms and KPI scorecards shape vendor selection and renewals. Partner ecosystems matter because last-mile quality drives customer satisfaction. Pricing pressure rises on basic lanes, while premium work holds margins through compliance and security scope. Consolidation risk stays present where buyers reduce vendor count and award multi-year MSAs.

Recent Developments

- In March 2025, Iron Mountain Incorporated took ownership of Indian data center firm WebWerks, giving it a portfolio of six data centers across Mumbai, Bangalore, Hyderabad, Pune, and Noida, while also adding a larger expansion pipeline in India.

- In March 2025, UPS announced a 10-year strategic collaboration with NTT DATA under which NTT DATA will purchase and operate one of UPS’s mission-critical data centers, supporting UPS’s IT modernization and future digital service development.

- In May 2025, DHL Supply Chain acquired IDS Fulfillment, adding more than 1.3 million square feet of multi-customer warehouse and distribution space across the United States and strengthening its contract logistics network.

- In November 2025, Equinix, Inc. completed the acquisition of BT’s data center business in Ireland, increasing its Irish colocation footprint from four to five facilities and expanding capacity in Dublin.