Executive summary:

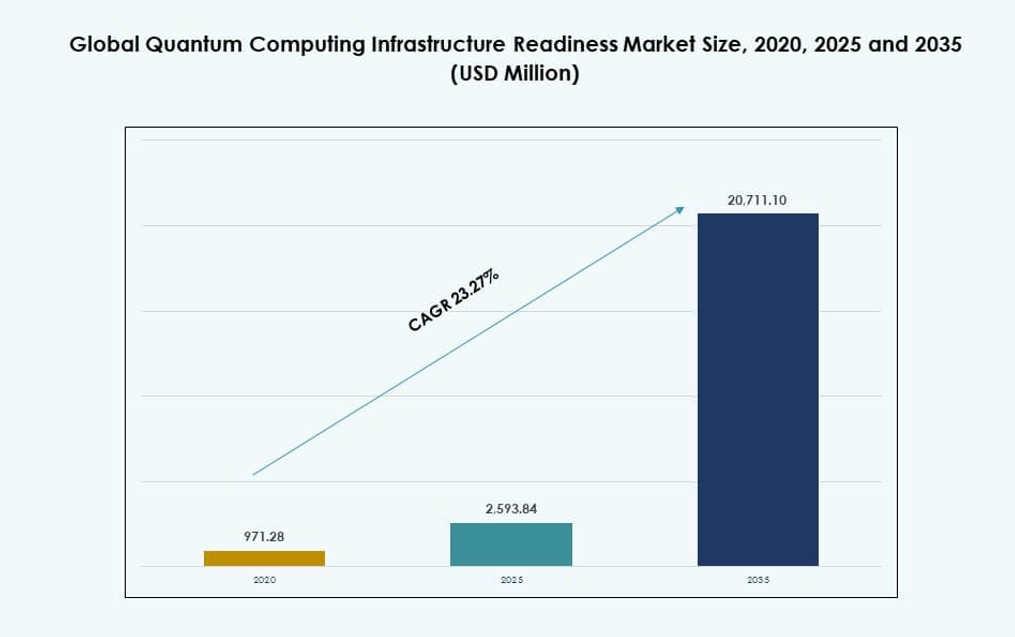

The Global Quantum Computing Infrastructure Readiness Market size was valued at USD 971.28 million in 2020 to USD 2,593.84 million in 2025 and is anticipated to reach USD 20,711.10 million by 2035, at a CAGR of 23.27% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2035 |

| Quantum Computing Infrastructure Readiness Market Size 2025 |

USD 2,593.84 Million |

| Quantum Computing Infrastructure Readiness Market, CAGR |

23.27% |

| Quantum Computing Infrastructure Readiness Market Size 2035 |

USD 20,711.10 Million |

The Global Quantum Computing Infrastructure Readiness Market advances through faster enterprise adoption of hybrid quantum-classical architecture, stronger cloud access models, and steady progress in control software, orchestration, and error-correction research. Technology firms now align quantum roadmaps with AI, HPC, and cybersecurity strategies, which raises the need for integrated infrastructure. It holds strategic importance for businesses because it supports future computational advantage, while investors value it for early positioning in a high-growth, deep-technology ecosystem.

The Global Quantum Computing Infrastructure Readiness Market remains led by North America due to strong vendor presence, cloud ecosystem depth, and institutional research support. Europe follows with solid momentum from public funding, cross-border research programs, and industrial collaboration. Asia Pacific stands out as the key emerging region, led by Japan and China, while India and Australia build capacity through partnerships and digital infrastructure expansion. Latin America, the Middle East, and Africa show earlier-stage adoption, with selective growth in national and academic initiatives.

Market Dynamics:

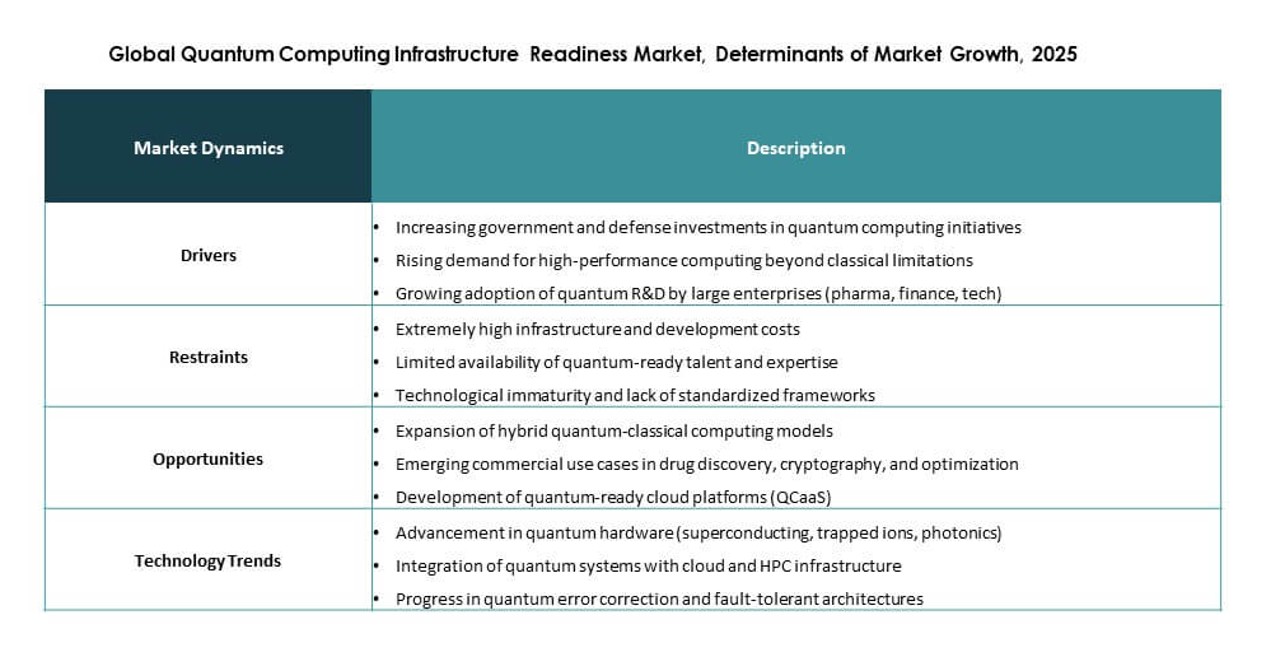

Market Drivers

Enterprise Demand For Quantum-Ready Hybrid Compute Environments And Secure Architecture Roadmaps

The Global Quantum Computing Infrastructure Readiness Market gains traction because enterprises want compute environments that support future quantum workloads alongside existing HPC and AI systems. Large organizations seek architectures that connect quantum processors with secure cloud platforms, classical servers, and data center controls. This shift moves quantum from lab experiments to enterprise planning. It raises demand for readiness assessments, orchestration tools, and integration services. Boards favor investments that fit current infrastructure strategies. Investors also value suppliers that can capture early spending. This driver strengthens long-term commercial confidence across hardware, software, and services ecosystems.

Growing Integration Of Quantum Systems With Classical Compute, Cloud Platforms, And AI Infrastructure

The Global Quantum Computing Infrastructure Readiness Market expands because quantum value depends on strong integration with CPUs, GPUs, cloud systems, and enterprise data environments. Companies no longer assess quantum hardware in isolation. They want hybrid workflows that connect simulation, optimization, and analytics tools with existing compute assets. This trend raises demand for middleware, control electronics, workload orchestration, and low-latency network design. Cloud access also reduces entry barriers for commercial users. Vendors that support seamless hybrid execution gain a strategic edge. This driver supports broader adoption and improves the market’s relevance for business planners and investors.

- For instance, NVIDIA and Quantum Machines said DGX Quantum enables under-4-microsecond round-trip latency between GPU and QPU control, and Diraq later reported a 3.3-microsecond round-trip in real-time GPU-QPU integration, highlighting how tightly coupled classical-quantum execution is becoming a measurable infrastructure requirement.

Improving Hardware Reliability And Error Correction Progress That Strengthens Commercial Buyer Confidence

The Global Quantum Computing Infrastructure Readiness Market benefits from technical progress that improves buyer confidence in long-term deployment value. Advances in error correction, system fidelity, and hardware stability reduce concern around performance limits. Enterprises and public institutions now see clearer roadmaps toward useful and scalable quantum systems. This makes infrastructure planning more credible and less speculative. Confidence in technical durability supports spending on cryogenic systems, control electronics, and software platforms. It also helps vendors secure longer contracts and strategic partnerships. Investors view this progress as a signal that infrastructure demand can expand with stronger market discipline.

Public Funding, National Quantum Strategies, And Technology Sovereignty Priorities That Expand Market Support

The Global Quantum Computing Infrastructure Readiness Market receives strong support from public funding, national quantum strategies, and sovereignty-driven technology programs. Governments view quantum capability as a strategic asset tied to research leadership, cybersecurity, and defense modernization. This creates demand for local infrastructure, secure deployment models, and institutional partnerships. National labs and research centers often serve as early anchors for adoption. Their projects help vendors prove deployment capability and expand regional ecosystems. Public investment also lowers early market risk. For businesses and investors, this support improves visibility, strengthens ecosystem development, and creates more stable long-term commercial pathways.

- For instance, Israel Aerospace Industries, together with the Israel Innovation Authority, Hebrew University, and Yissum, brought Israel’s first domestically built 20-qubit superconducting quantum computer into operation in December 2024, directly tying a measurable technical milestone to a sovereignty-driven national infrastructure effort.

Market Trends

Platform-Centric Procurement Models Are Replacing Standalone Hardware Purchases Across Enterprise Accounts

The Global Quantum Computing Infrastructure Readiness Market shows a clear move toward platform-centric procurement rather than isolated hardware purchases. Enterprises now prefer solutions that combine access, orchestration, software tools, and technical support within one commercial framework. This model simplifies evaluation and reduces integration burden. Buyers can test workloads without large initial capital commitments. Vendors gain stronger customer retention through recurring platform relationships. Competition now depends less on hardware claims alone and more on ecosystem depth and execution quality. This trend supports software and services growth. It also broadens access for enterprises with limited internal quantum expertise.

Flexible Multi-Modality Strategies And Vendor-Neutral Architectures Are Becoming A Core Buyer Preference

The Global Quantum Computing Infrastructure Readiness Market reflects growing buyer preference for flexible architectures that avoid early dependence on one qubit modality. Enterprises want the option to evaluate superconducting, trapped-ion, photonic, and annealing systems through adaptable software and infrastructure frameworks. This supports vendor-neutral procurement and reduces long-term risk. It also favors orchestration platforms that manage multiple back-end environments. Buyers increasingly value optionality because the technology landscape still evolves. Vendors that support this flexibility gain wider commercial appeal. This trend shapes roadmap decisions across cloud access, hybrid deployment, and future on-premises readiness strategies for large organizations.

Structured Quantum Readiness Programs, Governance Models, And Workforce Development Are Gaining Importance

The Global Quantum Computing Infrastructure Readiness Market now includes a stronger focus on readiness programs, governance frameworks, and workforce development. Enterprises no longer treat quantum preparation as an isolated research issue. They want practical plans that address use-case mapping, infrastructure priorities, risk oversight, and staff capability. This expands demand beyond hardware and software into consulting and managed support. Governance-led adoption helps firms move from experimentation to planned deployment. Workforce preparation also matters because quantum adoption requires cross-functional coordination. This trend supports service revenue growth and improves commercial maturity across the market for long-term institutional and enterprise adoption.

Quantum Infrastructure Planning Is Converging With Cybersecurity And Post-Quantum Risk Management Priorities

The Global Quantum Computing Infrastructure Readiness Market shows strong convergence with cybersecurity and post-quantum risk planning. Enterprises increasingly link quantum infrastructure preparation with cryptographic transition strategies and future data protection goals. This expands the market’s relevance beyond research and advanced simulation. Financial institutions, governments, and telecom operators now view readiness as part of a wider security agenda. Security-focused infrastructure planning influences vendor selection, deployment models, and budget timing. It also supports demand for secure access layers, key management capabilities, and governance tools. This trend raises board-level attention and strengthens the market’s strategic enterprise value.

Market Challenges

High Technical Complexity, Limited Standards, And Cross-Functional Procurement Gaps Slow Adoption Pace

The Global Quantum Computing Infrastructure Readiness Market faces a major challenge from high technical complexity across hardware, software, control electronics, and site requirements. Many enterprises still lack clear internal ownership for quantum decisions. Procurement teams often struggle to compare vendor offerings across different architectures and service models. Industry standards remain limited, which weakens confidence during evaluation. Talent shortages add further pressure in areas such as quantum engineering, cryogenics, and hybrid systems design. Buyers must align research, infrastructure, security, and finance teams before action. This slows sales cycles and increases execution risk for both vendors and investors.

Heavy Infrastructure Costs And Uncertain Near-Term Returns Continue To Restrain Commercial Expansion

The Global Quantum Computing Infrastructure Readiness Market also faces pressure from high infrastructure costs and uncertain short-term commercial returns. Quantum deployment can require expensive cooling systems, precision electronics, site preparation, and specialized support. Many end users still operate at pilot scale, which limits immediate revenue realization. Boards often demand measurable business value before approving broader investments. This delays full deployment and keeps many projects in exploratory phases. Vendors must balance long research cycles with commercial expectations. That strain can affect margins and expansion plans. It remains a key barrier to faster mainstream enterprise adoption worldwide.

Market Opportunities

Managed Readiness Services And Integration Advisory Offer Strong Early Revenue Potential Across Buyer Groups

The Global Quantum Computing Infrastructure Readiness Market offers strong opportunity in managed readiness services and integration advisory work. Many enterprises, research centers, and public agencies lack internal expertise to assess infrastructure needs, security gaps, and deployment models. This creates demand for architecture reviews, site planning, governance support, and workforce training. Service-led engagement helps vendors enter accounts before full hardware procurement begins. It also supports recurring contracts and long-term relationships. Buyers value expert guidance because it lowers project risk. This opportunity can generate early revenue while broader quantum hardware adoption still develops across commercial sectors.

Hybrid Access Models And Expanding Industry Use Cases Create Wider Long-Term Commercial Potential

The Global Quantum Computing Infrastructure Readiness Market also gains opportunity from hybrid access models and a widening set of industry use cases. Cloud-based entry allows enterprises to test workloads without full capital exposure, while hybrid models support later expansion into secure dedicated environments. This phased approach lowers adoption barriers and improves budget flexibility. Demand can emerge across finance, healthcare, telecom, materials, and defense sectors. Vendors that support flexible deployment and modality choice can serve more customer profiles. Software and orchestration providers also benefit. This opportunity strengthens the value chain and broadens long-term investor interest.

Market Segmentation

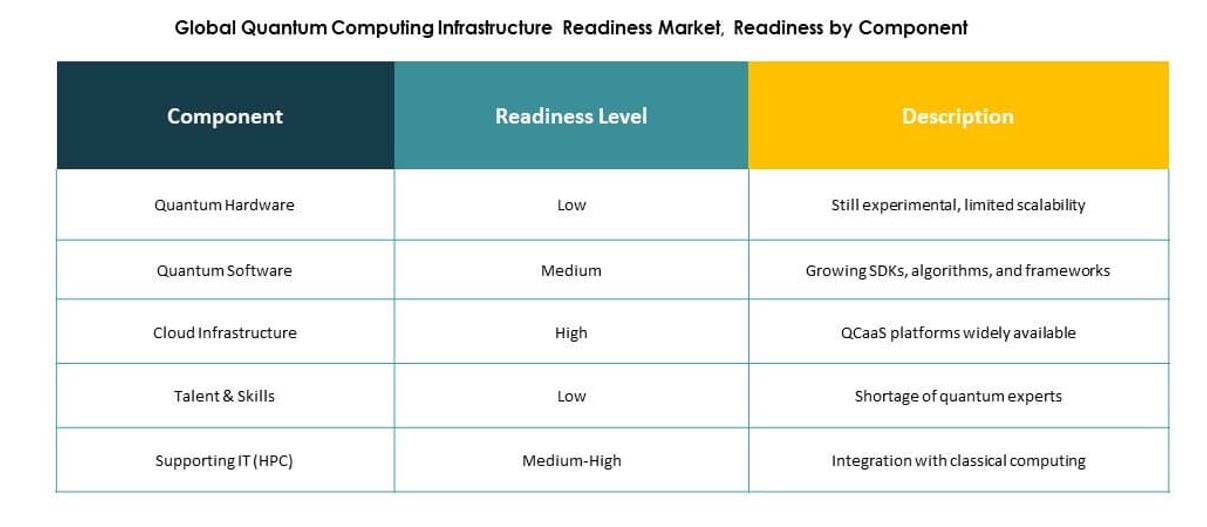

By Component

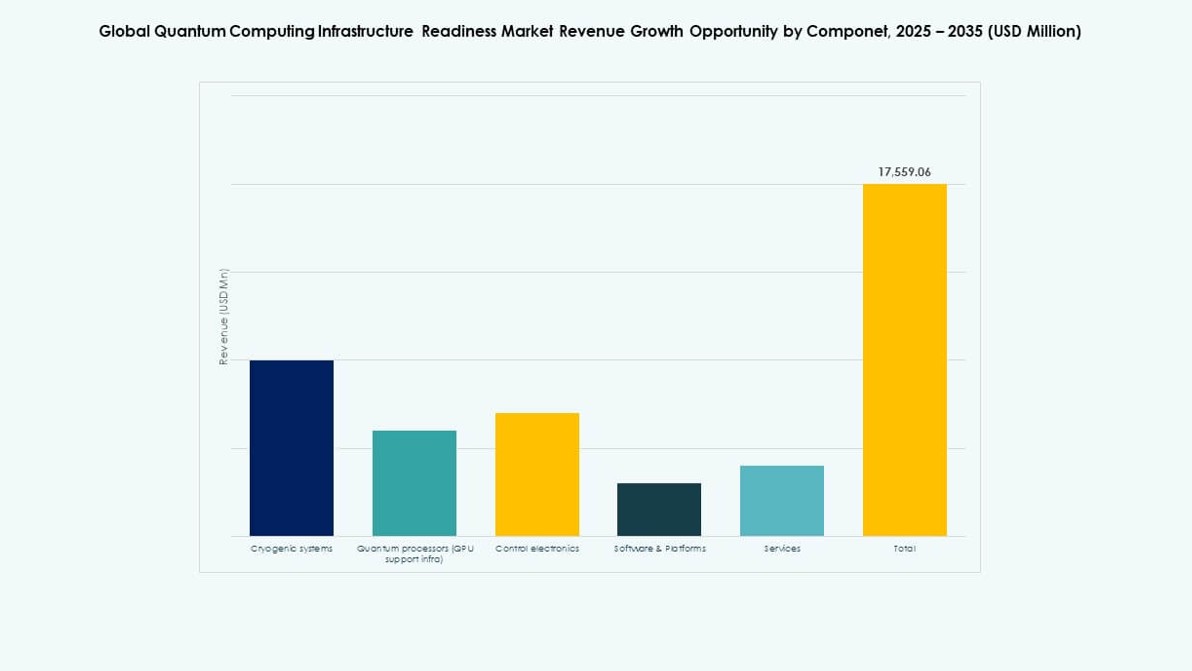

The Global Quantum Computing Infrastructure Readiness Market shows software and platforms as the dominant component segment, with an estimated 29% share, because enterprises often start with orchestration, development tools, and access frameworks before hardware commitments. Services follow closely due to demand for readiness assessments, deployment support, and integration consulting. Control electronics and cryogenic systems remain essential because stable system performance depends on precise thermal and signal management. Quantum processor support infrastructure also holds a meaningful position in full-stack projects. Software leads because it supports governance, hybrid workflows, scalability, and multi-vendor interoperability across early and advanced deployment strategies.

By Application

The Global Quantum Computing Infrastructure Readiness Market sees optimization problems lead the application segment with an estimated 24% share, driven by demand from logistics, energy, mobility, and industrial planning users. Cryptography and cybersecurity also represent a major share because institutions link quantum readiness with future security strategy. Drug discovery and healthcare attract steady interest through simulation-led research potential. Financial modeling remains important for portfolio analysis and scenario testing. Material science supports research-based investment, while AI and machine learning gains pace through hybrid compute experimentation. Optimization leads because it offers broad cross-industry relevance and near-term commercial evaluation potential.

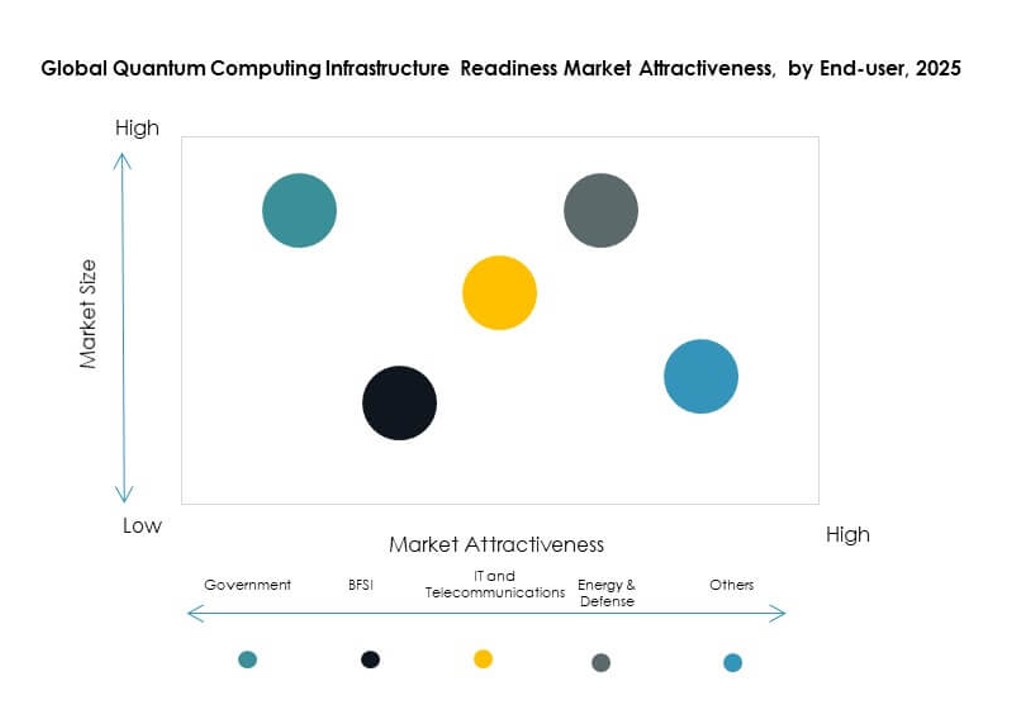

By End User

The Global Quantum Computing Infrastructure Readiness Market remains led by research institutes and academia, which hold an estimated 31% share due to grant-backed projects, pilot deployments, and foundational research programs. Government and defense follow with strong influence because national security and sovereignty goals support long-term funding. BFSI represents a major commercial segment through interest in optimization, risk analysis, and post-quantum security. IT and telecom firms invest to prepare hybrid infrastructure and secure digital networks. Healthcare and pharma continue to build demand through discovery use cases. Research institutions lead because they anchor ecosystem development and early system adoption.

By Infrastructure Readiness

The Global Quantum Computing Infrastructure Readiness Market shows data center readiness as the dominant infrastructure readiness segment, with an estimated 27% share. Buyers focus first on power, cooling, floor planning, and secure facility design because these elements determine system viability. Compute integration follows closely since quantum value depends on close coordination with classical HPC and AI resources. Security readiness also holds a major position because enterprises want protected access, policy control, and future-proof cryptographic frameworks. Network readiness remains important for remote access and distributed collaboration. Data center readiness leads because it forms the physical foundation for scalable deployment and sustained performance.

By Deployment Mode

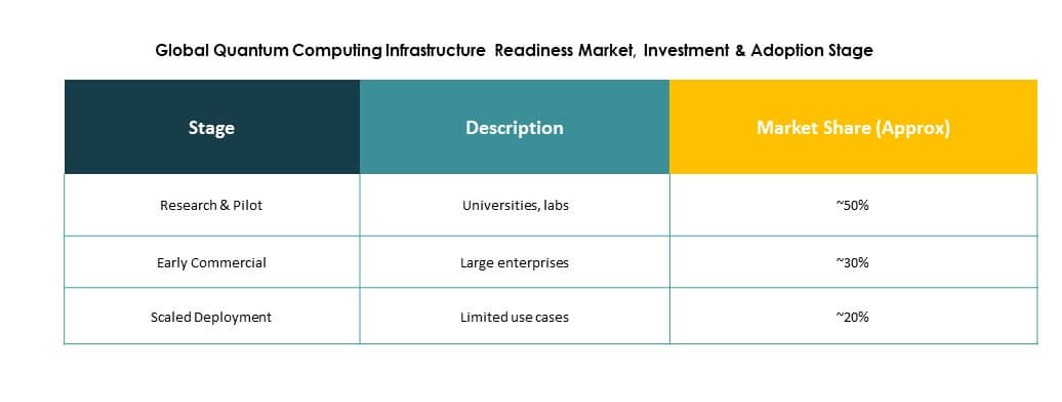

The Global Quantum Computing Infrastructure Readiness Market is led by cloud-based quantum access, which holds an estimated 46% share because it lowers entry barriers, reduces capital burden, and supports rapid workload testing. Hybrid deployment follows at about 33%, driven by organizations that want flexible paths combining cloud experimentation with secure local integration. On-premises quantum infrastructure remains the smallest segment, though it retains importance in defense, national labs, and highly regulated environments. Cloud access leads because it supports pilot programs, developer adoption, and broad user training. Hybrid models show strong growth where compliance and long-term scaling shape procurement decisions.

By Offering Type

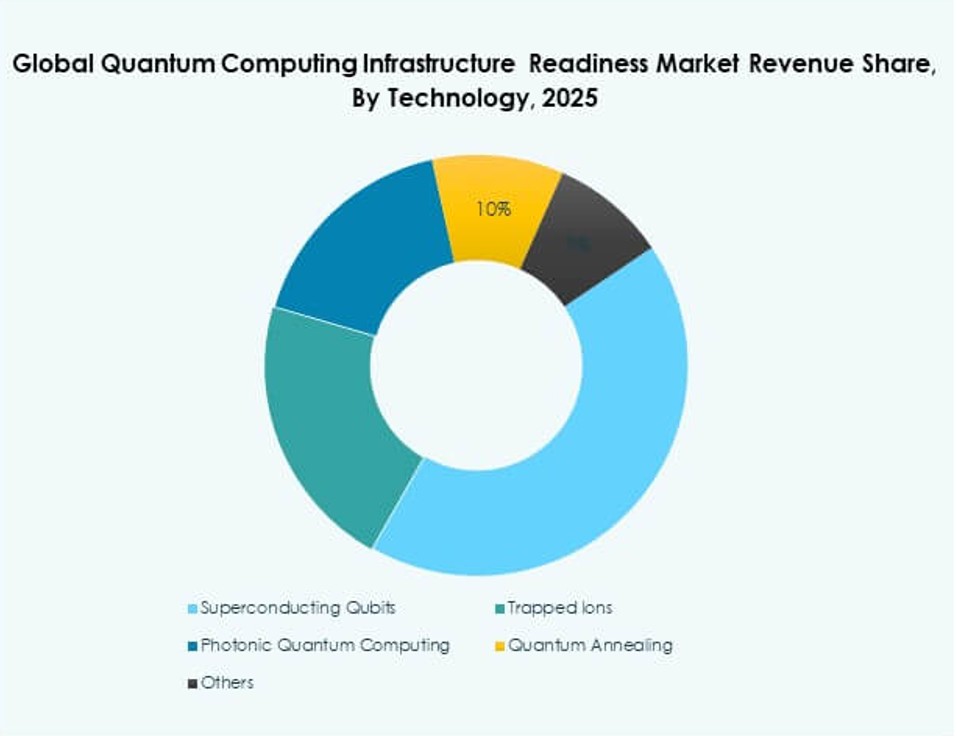

The Global Quantum Computing Infrastructure Readiness Market is dominated by superconducting qubits, which account for an estimated 34% share due to strong ecosystem support, major vendor investment, and broad visibility in commercial roadmaps. Trapped ions hold the next notable position because they offer high fidelity and flexible deployment potential. Photonic quantum computing gains attention through possible advantages in networking and scalability. Quantum annealing maintains relevance for optimization-focused use cases and specialized commercial tasks. The others category includes emerging modalities with selective uptake. Superconducting systems lead because infrastructure, software support, and enterprise familiarity are stronger at this stage.

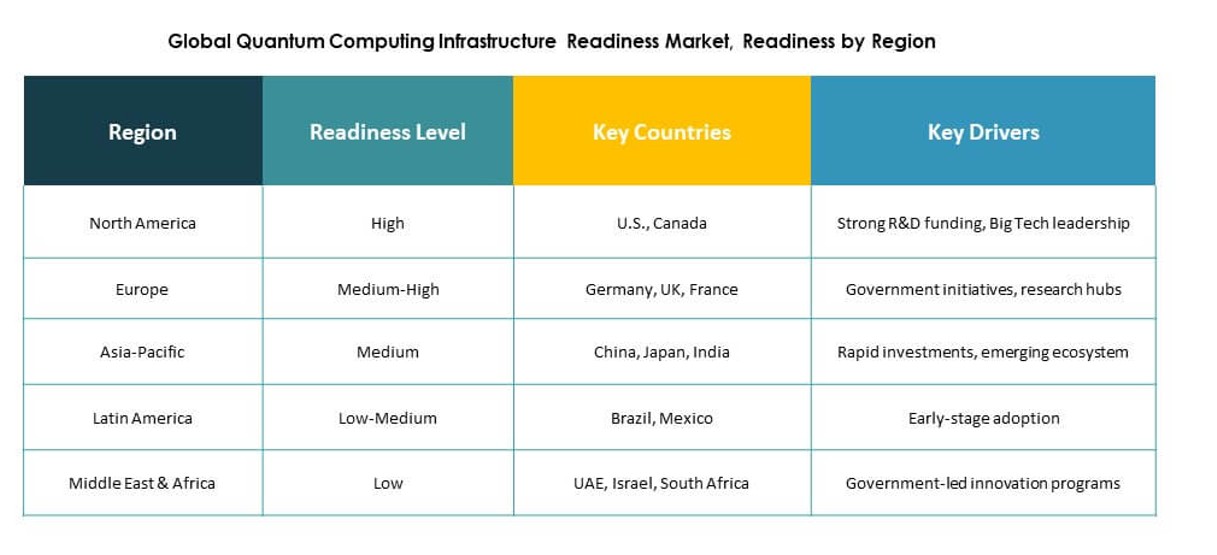

Regional Insights

North America Holds The Lead While Europe Builds Strong Institutional And Commercial Depth

The Global Quantum Computing Infrastructure Readiness Market is led by North America with an estimated 38% share. The U.S. drives this position through major vendor presence, cloud ecosystem strength, enterprise pilots, and national lab support. Canada adds depth through academic research and startup development. Europe follows with about 27% share, supported by coordinated public programs and strong institutional collaboration. The UK, Germany, and France anchor regional momentum. Buyers across both regions prioritize secure hybrid architecture, software platforms, and quantum-classical integration. These strengths keep North America and Europe at the center of current market development.

- For instance, IBM launched the Aachen system in Germany in April 2025 with its 156-qubit Heron R2 processor, and IBM stated that it had 13 utility-scale quantum computers with more than 100 qubits in operation as of early 2025, underlining the technical and deployment depth shaping readiness across North America and Europe.

Asia Pacific Emerges As The Fastest-Developing Region With Strong Research And Infrastructure Momentum

The Global Quantum Computing Infrastructure Readiness Market assigns Asia Pacific an estimated 24% share, making it the fastest-developing regional bloc. Japan, China, South Korea, India, and Australia continue to expand research programs, ecosystem partnerships, and digital infrastructure support. Japan and China hold the strongest institutional depth, while India and Australia build momentum through research alliances and technology investment. Enterprises across the region increasingly favor cloud access and phased readiness models. This supports demand for software platforms, integration services, and data center preparation. Asia Pacific stands out for its speed of strategic commitment and long-term infrastructure ambition.

- For instance, Fujitsu and RIKEN unveiled a 256-qubit superconducting quantum computer in April 2025, building on their earlier 64-qubit system launched in October 2023, and they also stated a roadmap toward a 1,000-qubit computer in 2026, demonstrating the scale and pace of infrastructure advancement in the region.

Latin America, The Middle East, And Africa Show Early-Stage Growth With Targeted Strategic Investment

The Global Quantum Computing Infrastructure Readiness Market gives Latin America about 5% share, the Middle East 4%, and Africa 2%. These regions remain at an earlier adoption stage but show clear strategic interest. Brazil leads Latin America through academic capacity and innovation policy support. Israel and GCC states anchor Middle East activity through research capability and digital sovereignty priorities. South Africa serves as the main African entry point through institutional research strength. Most buyers prefer cloud-based access, partnerships with global vendors, and targeted pilot programs. This measured approach helps manage cost while local ecosystems continue to mature.

Competitive Insights:

- IBM

- Google

- Microsoft

- Amazon Web Services

- Quantinuum

- IonQ

- Rigetti Computing

- D-Wave Quantum

- Intel Corporation

- NVIDIA Corporation

The Global Quantum Computing Infrastructure Readiness Market features competition between full-stack quantum providers, hyperscale cloud firms, and specialized hardware developers. IBM holds a strong position through its integrated hardware, platform, and quantum-safe portfolio, while Quantinuum and IonQ compete on full-stack access and enterprise-grade system performance. Google and Rigetti maintain relevance through superconducting hardware development, and D-Wave stands apart with cloud-first quantum and hybrid optimization services. Microsoft, AWS, and NVIDIA shape competition from the software, orchestration, and hybrid compute side, which gives them influence over enterprise adoption paths. Intel remains important through control, packaging, and semiconductor expertise. It remains a technology-led market where ecosystem depth, cloud reach, integration capability, and roadmap credibility define vendor strength more than hardware claims alone.

Recent Developments:

- In November 2025, HPE and seven partner organizations launched the Quantum Scaling Alliance, a global initiative designed to make quantum computing more scalable and practical for mainstream use. HPE said the alliance would focus on hybrid solutions that combine quantum systems with classical high-performance computing and advanced networking, which directly supports broader quantum infrastructure development.

- In May 2025, IBM and Tata Consultancy Services (TCS), together with the Government of Andhra Pradesh, unveiled plans tied to Quantum Valley Tech Park in Amaravati to help expand India’s quantum computing ecosystem. The initiative includes deployment of IBM Quantum System Two at the site, positioning the partnership as a major infrastructure-building step for quantum readiness in India.

- In April 2025, Terra Quantum announced a strategic partnership with Siemens Cre8Ventures to bring a Quantum-as-a-Service platform into the Siemens Cre8Ventures Digital Twin Marketplace. The partnership gives users access to Terra Quantum’s hybrid quantum tools and quantum-secure infrastructure, supporting infrastructure readiness for automotive, aerospace, and drone-related applications.