Executive summary:

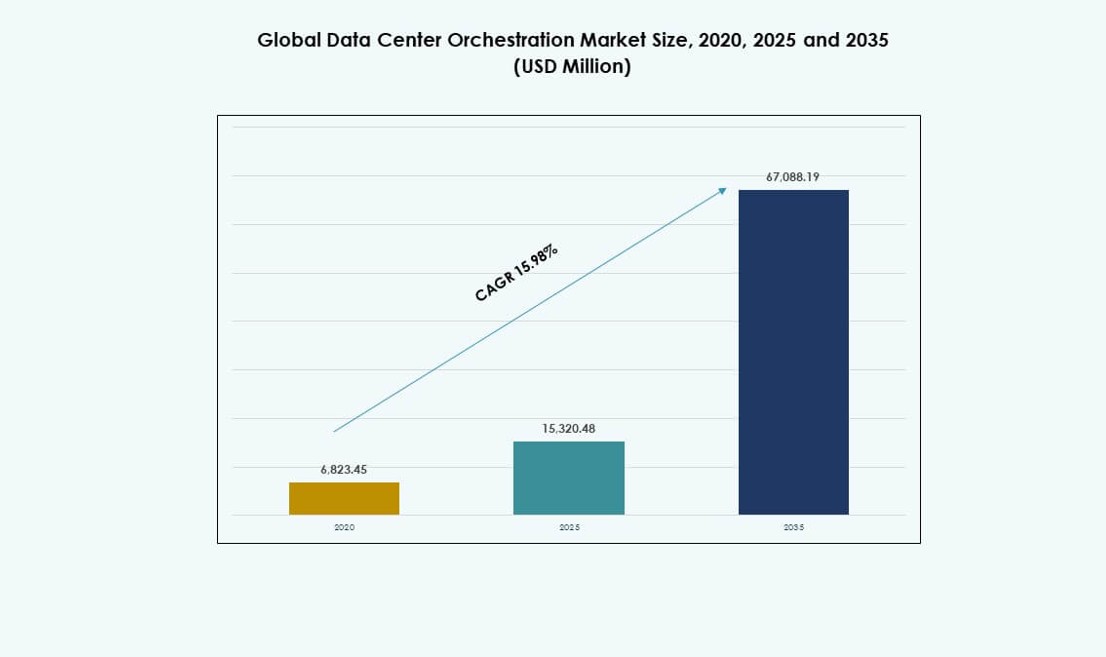

The Global Data Center Orchestration Market size was valued at USD 6,823.45 million in 2020 to USD 15,320.48 million in 2025 and is anticipated to reach USD 67,088.19 million by 2035, at a CAGR of 15.98% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2035 |

| Data Center Orchestration Market Size 2025 |

USD 15,320.48 Million |

| Data Center Orchestration Market, CAGR |

15.98% |

| Data Center Orchestration Market Size 2035 |

USD 67,088.19 Million |

The market is driven by rising adoption of hybrid cloud environments, software-defined infrastructure, and automated workload management across enterprise data centers. Organizations now seek orchestration platforms that can improve resource efficiency, reduce manual intervention, and strengthen service reliability. Innovation in AI-led operations, observability tools, and policy-based automation also supports wider deployment. For businesses and investors, this market holds strategic importance because it sits at the center of digital infrastructure modernization and long-term operational scalability.

North America leads the market due to strong hyperscale investment, mature enterprise IT ecosystems, and early adoption of automation platforms. Europe follows with solid demand from regulated industries that require governance, resilience, and standardized infrastructure control. Asia Pacific is the fastest-emerging region, supported by cloud expansion, telecom network upgrades, and rapid digital transformation across China, India, Japan, and Southeast Asia. Latin America, the Middle East, and Africa also show rising potential with growing colocation activity and enterprise modernization.

Market Dynamics:

Market Drivers

Rising Need For Unified Control Across Hybrid And Multi-Cloud Data Center Environments

Enterprises now run workloads across private clouds, colocation sites, edge nodes, and hyperscale platforms, which increases the need for unified control. The Global Data Center Orchestration Market benefits because businesses want a single framework for compute, storage, network, and security tasks. It helps reduce manual effort, service delays, and configuration errors. Large operators prefer platforms that standardize provisioning, patching, policy enforcement, and workload placement across mixed environments. This shift reflects broader automation goals. Businesses also value faster service delivery because digital products depend on stable, flexible infrastructure with strong governance and predictable performance.

- For instance, HPE states that HPE Morpheus Enterprise Software integrates hypervisors, public clouds, and Kubernetes clusters behind a single control plane, while HPE Morpheus VM Essentials can reduce VM license costs by up to 90% through multi-hypervisor support and self-service cloud consumption.

Expansion Of AI Workloads And High-Density Infrastructure Management Requirements

AI clusters, GPU-rich racks, and high-performance servers have changed how operators manage data center resources. The Global Data Center Orchestration Market benefits because AI workloads require dynamic scheduling, thermal awareness, power coordination, and policy-based allocation. Traditional tools often lack the range to manage that complexity. Enterprises now seek orchestration platforms that align compute capacity with storage access, network paths, and energy limits. It also supports smarter capacity planning because AI demand can shift quickly. This driver carries strategic value for businesses and investors since AI-ready infrastructure requires intelligent, automated, and scalable control layers.

- For instance, Schneider Electric noted that the NVIDIA GB300 NVL72 runs 72 GPUs in parallel at 142 kW per rack, while conventional 400V AC and 48V DC approaches become difficult at 200 kW per rack and impossible at 400 kW per rack, leading Schneider to advance an 800 VDC architecture for single IT racks from 400 kW up to 1 MW.

Greater Focus On Operational Efficiency, Service Reliability, And Cost Discipline

CIOs and infrastructure leaders face pressure to improve uptime while keeping operating costs under control. The Global Data Center Orchestration Market gains from this need because orchestration software automates repetitive tasks, reduces service tickets, and supports faster incident response. It also improves resource use by matching workloads to the right infrastructure pool. Many firms now view automation as a financial tool, not only a technical upgrade. Service providers use orchestration to protect service-level agreements across complex customer environments. This driver matters because businesses want stable digital operations, lower disruption risk, and stronger returns on infrastructure investment.

Shift Toward Software-Defined Infrastructure And Policy-Based Data Center Operations

Software-defined compute, storage, and networking have created a strong base for wider orchestration adoption. The Global Data Center Orchestration Market expands because organizations want policy-driven control that converts business intent into automated infrastructure actions. This shift moves operators away from device-level management toward service-level automation. It also supports modernization programs where firms seek repeatable deployment models and centralized governance. Vendors now embed APIs, analytics, and workload intelligence into orchestration platforms. Businesses view these capabilities as essential for digital resilience, faster service rollout, and stronger control. Investors also see durable potential in this long-term architecture transition.

Market Trends

Convergence Of Orchestration Platforms With AIOps, Observability, And Predictive Analytics

Vendors now combine orchestration with AIOps and observability to create more intelligent infrastructure control. The Global Data Center Orchestration Market reflects this trend through platforms that link telemetry, anomaly detection, and automated remediation in one workflow. It allows operators to respond before service quality declines. This trend differs from basic automation because it adds context, prediction, and policy refinement. Providers now position orchestration as a decision layer rather than only an execution engine. Buyers favor tools that connect logs, metrics, and infrastructure actions in near real time. This trend raises platform value and strengthens vendor differentiation.

Adoption Of Open APIs And Interoperable Control Frameworks Across Diverse Infrastructure Stacks

Enterprises no longer want orchestration tools tied to narrow vendor ecosystems. The Global Data Center Orchestration Market now shows a strong trend toward open APIs, modular design, and interoperability across servers, containers, virtualization layers, and cloud platforms. It reflects customer demand for integration with existing IT service management and security tools. Many operators prefer this model because infrastructure estates often combine legacy assets with modern cloud-native systems. Vendors that support broad compatibility gain an advantage in large modernization projects. This trend also reduces migration friction and increases the appeal of flexible orchestration platforms across mixed environments.

Growth Of Industry-Specific Orchestration Use Cases With Compliance And Service Policy Controls

Sector-specific orchestration use cases now shape product design and buyer demand. The Global Data Center Orchestration Market reflects this trend in platforms tailored for finance, healthcare, government, and telecom environments. It shows the need for automation linked to compliance, security policy, and audit readiness. Vendors now package orchestration rules around data residency, workload isolation, backup policy, and access control. This approach helps customers align infrastructure automation with sector risk profiles and service obligations. Buyers value solutions that reduce custom work and speed deployment. The trend also supports recurring revenue through vertical modules and specialized service packages.

Rise Of Edge-Aware Orchestration For Distributed Facilities And Latency-Sensitive Workloads

Edge infrastructure growth has pushed orchestration beyond core and cloud data centers. The Global Data Center Orchestration Market now includes stronger support for distributed sites that host telecom functions, industrial workloads, and latency-sensitive applications. It reflects demand for centralized control of remote assets with limited on-site staff. Vendors now offer lighter orchestration frameworks that enforce policy, deploy workloads, and monitor service health across many locations. This trend differs from earlier central data center models because it requires location-aware execution. Buyers in telecom, retail, and manufacturing show strong interest. It expands orchestration’s role in distributed digital infrastructure.

Market Challenges

Integration Complexity Across Legacy Systems, Proprietary Tools, And Multi-Vendor Architectures

Many enterprises still depend on legacy systems, older virtualization layers, and proprietary management tools that complicate orchestration projects. The Global Data Center Orchestration Market faces a major challenge because customers often need deep integration before they can realize full automation value. It can raise deployment time, project risk, and service costs. Buyers also worry about disruption to live environments during migration. Vendor lock-in remains a concern when orchestration tools rely on narrow ecosystems. Internal skill gaps can also slow adoption. Security teams may resist broad automation rights without strong governance, which further delays large-scale implementation.

Shortage Of Automation Expertise And Difficulty In Proving Near-Term Return On Investment

A second challenge comes from talent shortages and uneven executive confidence in short-term payback. The Global Data Center Orchestration Market must address the fact that many firms lack staff with expertise in automation, workflow design, and cross-domain policy control. It makes adoption harder, especially for mid-size enterprises with smaller IT teams. Budget owners often seek clear proof that orchestration will cut costs, improve uptime, or delay capital spending. Those benefits are real but may depend on process maturity and deployment scale. Vendors must support adoption with training, consulting, and strong business value evidence.

Market Opportunities

Expansion Of Colocation, Managed Services, And AI-Ready Data Center Platforms

Colocation firms, managed service providers, and AI infrastructure operators create strong growth potential for the Global Data Center Orchestration Market. These providers need policy-based automation to manage multi-tenant environments, service quality, and rapid capacity shifts. It supports margin control and helps launch new services faster. Demand will rise where operators offer GPU clusters, private AI clouds, and high-availability enterprise platforms. Vendors that combine orchestration with tenant governance and service assurance can capture this demand. The opportunity holds long-term value because provider environments often scale faster than internal enterprise estates and require recurring automation support.

Rising Demand From Emerging Economies And Mid-Market Infrastructure Modernization Programs

Emerging markets and mid-size enterprises offer another strong growth path for the Global Data Center Orchestration Market. Many of these buyers now modernize infrastructure to support digital services, cloud adoption, and stricter uptime targets. It creates demand for modular solutions that deliver automation without heavy customization. Vendors can gain ground with scalable pricing, cloud-delivered control planes, and faster deployment models. Regional data center growth in Asia Pacific, the Middle East, and parts of Latin America supports this opportunity. Firms that build local partnerships and flexible support models can strengthen adoption and capture market share.

Market Segmentation

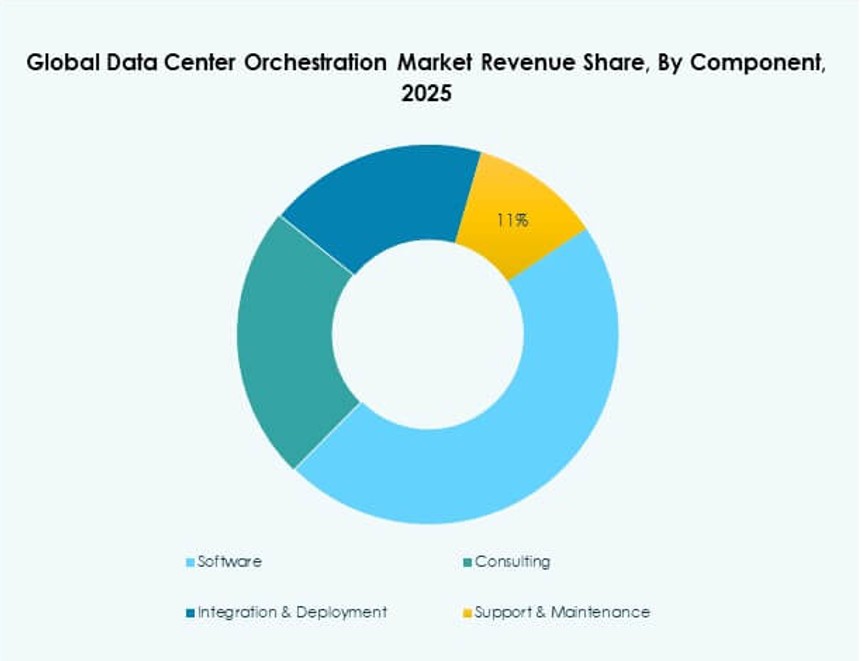

By Component

The Global Data Center Orchestration Market by component includes software, consulting, integration and deployment, and support and maintenance. Software led the segment with an estimated 46.8% share in 2025 because enterprises prioritize centralized automation, policy engines, workload coordination, and analytics dashboards. Consulting remains important in early-stage modernization projects where firms need architecture review and roadmap planning. Integration and deployment also show strong demand due to API mapping, workflow design, and hybrid environment alignment. Support and maintenance ensure platform continuity, performance tuning, and update management. Software will likely remain dominant because it delivers scalable control and recurring enterprise value.

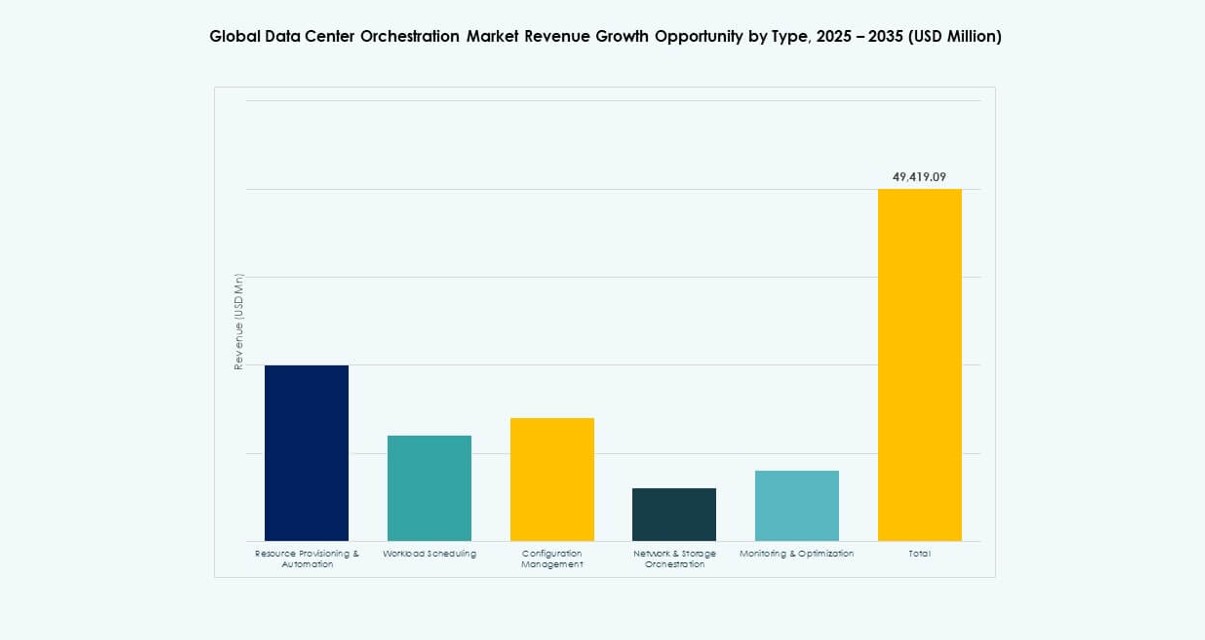

By Application

The Global Data Center Orchestration Market by application includes resource provisioning and automation, workload scheduling, configuration management, network and storage orchestration, and monitoring and optimization. Resource provisioning and automation held the largest share at about 29.4% in 2025 because enterprises seek faster service rollout, lower manual effort, and consistent policy execution. Workload scheduling has gained importance with AI, containers, and mixed cloud environments that need dynamic resource placement. Configuration management stays central in policy-sensitive environments. Network and storage orchestration expands with software-defined infrastructure, while monitoring and optimization gain traction through automated performance control and telemetry-driven decisions.

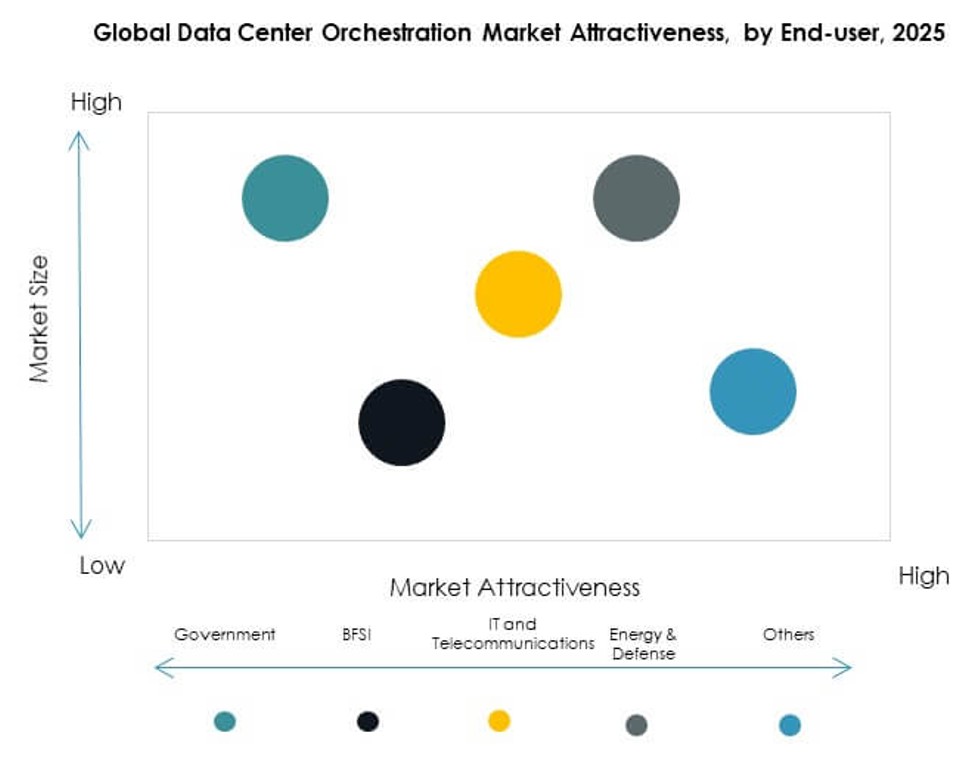

By End-user

The Global Data Center Orchestration Market by end-user includes IT and telecom, BFSI, healthcare, retail, government, and others. IT and telecom dominated with an estimated 31.6% market share in 2025 due to large infrastructure estates, strong cloud integration, and constant pressure to deliver reliable digital services. BFSI follows with demand tied to uptime, compliance, and secure workload control. Healthcare adoption rises as providers expand digital care and analytics systems. Retail firms deploy orchestration to support omnichannel operations and distributed infrastructure. Government demand remains notable where agencies modernize services and seek stronger infrastructure efficiency and policy control.

By Enterprise Size

The Global Data Center Orchestration Market by enterprise size is segmented into large enterprises and SMEs. Large enterprises accounted for about 67.9% of the market in 2025 because they operate complex hybrid estates, broad application portfolios, and high infrastructure density. These organizations also have stronger budgets for automation, consulting, and integration. SMEs hold a smaller revenue base, yet growth potential remains solid due to cloud-led adoption and the need for lean infrastructure operations. Many smaller firms now prefer packaged orchestration tools with lower deployment burden. Large enterprises continue to lead because orchestration value rises sharply with operational scale and complexity.

By Deployment Mode

The Global Data Center Orchestration Market by deployment mode includes on-premises, cloud-based, and hybrid models. Hybrid deployment led with an estimated 41.7% share in 2025 because most enterprises now manage workloads across internal infrastructure and external cloud platforms. This model supports flexibility, business continuity, and selective workload placement based on cost, latency, and compliance needs. On-premises deployments remain important in regulated sectors and mission-critical environments that require direct control. Cloud-based orchestration shows strong momentum due to faster deployment and easier scalability. Hybrid models will likely remain dominant because they match the operating reality of most large organizations.

Regional Insights

North America And Europe Maintain Leadership Through Early Automation Adoption And Mature Enterprise IT Estates

North America led the Global Data Center Orchestration Market with an estimated 37.8% share in 2025. The United States held the largest portion due to hyperscale growth, enterprise cloud maturity, and broad use of software-defined infrastructure. Canada added stable demand through colocation growth and financial sector digitization, while Mexico showed gradual progress through telecom and enterprise modernization. Europe held about 27.4% share, supported by investment across the UK, Germany, France, Italy, and Spain. The region also benefits from compliance-driven infrastructure control needs. Demand in both regions remains strong because enterprises seek reliable orchestration across hybrid, complex environments.

- For instance, Europe-based Schneider Electric expanded its EcoStruxure Data Center portfolio with solutions engineered for AI cluster environments where rack power densities are projected to reach 1 MW and beyond, underscoring the kind of high-performance automated infrastructure that supports regional leadership.

Asia Pacific Emerges As The Fastest-Growing Regional Block With Broad Digital Infrastructure Expansion

Asia Pacific captured an estimated 24.6% share of the Global Data Center Orchestration Market in 2025 and posted the fastest growth trajectory. China and Japan remain major demand centers due to large enterprise IT estates, cloud expansion, and data center investment. India and South Korea show rapid adoption driven by digital transformation, telecom capacity growth, and higher demand for automated workload control. Australia supports the region through mature enterprise cloud use and active managed service deployment. Rest of Asia Pacific adds momentum through new colocation and edge projects. This regional profile creates strong long-term opportunity for global vendors and local integration partners.

- For instance, NTT DATA announced six new AI-powered Cyber Defense Centers, including four already operational in India, and said its automation framework can deliver up to 60% faster investigations and 90% fewer alerts, highlighting the scale and measurable efficiency gains now being deployed across Asia Pacific’s digital infrastructure landscape.

Latin America, The Middle East, And Africa Gain Ground Through Colocation Growth And Public-Private Digitalization Programs

Latin America represented about 5.2% of the Global Data Center Orchestration Market in 2025, with Brazil as the main revenue contributor due to rising cloud demand and enterprise infrastructure upgrades. The Middle East held around 3.1% share, supported by GCC investment in digital infrastructure, sovereign cloud projects, and smart city programs. Israel and Turkey add demand through enterprise modernization and stronger service provider activity. Africa accounted for nearly 1.9%, with South Africa leading adoption due to colocation presence and financial sector digitization. These regions remain smaller in revenue terms, yet they present strong expansion potential over the forecast period.

Competitive Insights:

- Cisco Systems, Inc.

- Microsoft Corporation

- IBM Corporation

- Hewlett Packard Enterprise (HPE)

- VMware, Inc.

- Amazon Web Services (AWS)

- Oracle Corporation

- Google LLC

- Dell Technologies Inc.

- Red Hat, Inc.

The Global Data Center Orchestration Market features strong competition among cloud providers, enterprise infrastructure vendors, and software-led automation specialists. Cisco, HPE, Dell Technologies, and IBM compete through integrated infrastructure portfolios that combine orchestration with network, compute, storage, and hybrid IT management capabilities. Microsoft, AWS, Google, and Oracle use cloud ecosystem depth, automation tools, and platform reach to strengthen enterprise adoption across hybrid and multi-cloud environments. VMware and Red Hat maintain a strong position through virtualization, container orchestration, and policy-based infrastructure control. It remains moderately consolidated, with leading firms focusing on platform interoperability, AI-driven automation, observability, and security-led orchestration. Strategic partnerships, product enhancements, and hybrid cloud integration shape market positioning. Vendors that deliver unified control, open APIs, and scalable automation frameworks hold a stronger competitive edge.

Recent Developments:

- In February 2025, IBM said it completed its acquisition of HashiCorp to create a more comprehensive end-to-end hybrid cloud platform. IBM added that HashiCorp’s infrastructure automation and security products would help clients automate cloud infrastructure at scale and extend HashiCorp technology into data center environments.

- In May 2025, Nutanix and Pure Storage unveiled a partnership to deliver a deeply integrated solution for deploying and managing virtual workloads on modern infrastructure. The companies said the offering combines Nutanix Cloud Infrastructure with Pure Storage all-flash systems and includes disaster recovery orchestration and cyber-resilience capabilities.

- In June 2025, Cisco announced new data center tools and partnerships aimed at speeding adoption of AI-ready infrastructure across enterprise and hyperscale environments. Cisco said the release includes Unified Nexus Dashboard, which consolidates management across LAN, SAN, IP fabric, and AI/ML IT environments into a single interface, alongside technical integrations with NVIDIA.

- In August 2025, VMware Explore 2025, Broadcom said VMware Private AI Services would become a standard component of VMware Cloud Foundation 9.0. Broadcom stated that this change makes VCF 9.0 an AI-native platform for secure, modern private cloud infrastructure at scale.