Executive summary:

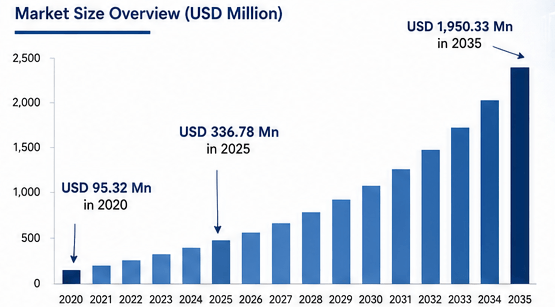

The Global Data Center Cooling CDU Pumps Market size was estimated at USD 95.32 million in 2020 to USD 336.78 million in 2025 and is anticipated to reach USD 1,950.33 million by 2035, at a CAGR of 19.20% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2035 |

| Data Center Cooling CDU Pumps Market Size 2025 |

USD 336.78 Million |

| Data Center Cooling CDU Pumps Market, CAGR |

19.20% |

| Data Center Cooling CDU Pumps Market Size 2035 |

USD 1,950.33 Million |

The market is driven by the rapid shift from air cooling to liquid cooling across AI, high-performance computing, hyperscale and colocation data centers. CDU pumps play a critical role in coolant circulation, pressure control, flow stability and thermal reliability across direct-to-chip and immersion cooling systems. Growth is further supported by rising rack densities, increased GPU deployment and the need to reduce energy losses in high-density server environments. Industry benchmarks support this outlook, with public estimates placing the broader data center CDU market at USD 2.40 billion in 2025 and projecting it to reach USD 14.61 billion by 2035 at a CAGR of 19.80%.

North America leads the market due to hyperscale AI investment, advanced colocation capacity and early deployment of direct-to-chip cooling systems. Europe follows with strong demand from energy-conscious operators, regulated industries and high-performance computing facilities. Asia Pacific is emerging as a high-growth region because of cloud expansion, AI infrastructure investment and data center construction across China, Japan, India, South Korea and Southeast Asia. Latin America, the Middle East and Africa remain smaller markets, but rising cloud adoption and sovereign data center projects create long-term expansion potential.

Market Dynamics:

Market Drivers

Rising Adoption Of Direct-To-Chip Liquid Cooling In AI Data Centers

Direct-to-chip liquid cooling is the strongest growth driver for the Global Data Center Cooling CDU Pumps Market because AI servers generate higher thermal loads than conventional enterprise systems. CDU pumps help maintain controlled coolant flow across cold plates, manifolds and heat exchangers, which supports stable operation of GPU-rich racks. Hyperscale and colocation operators increasingly require pumps that can manage higher pressure, redundancy and variable-speed performance. This shift supports demand for centrifugal, inline and magnetic drive pumps integrated into liquid-to-liquid CDU systems. For instance, Vertiv states that the CDU is a key component in the liquid cooling loop because it provides temperature and flow-rate control and maintains liquid hygiene through filtration.

Expansion Of High-Density AI, HPC And GPU Cluster Infrastructure

AI and HPC workloads are pushing cooling infrastructure toward higher flow rates, stronger pressure control and more reliable pump redundancy. The Global Data Center Cooling CDU Pumps Market benefits because operators need CDU pump systems that can support dense GPU clusters without thermal throttling. Pump design is becoming more important as rack density rises from traditional server levels to hundreds of kilowatts in advanced AI deployments. This creates demand for high-flow CDU pumps, redundant pump circuits and low-maintenance wetted materials. For instance, Uptime Institute noted that AI training cluster roadmaps now point to 200 kW per rack and above within a few years, making liquid cooling more important for high-density deployments.

Need For Energy Efficiency, Thermal Stability And Lower Operating Cost

Data center operators face rising power costs, grid pressure and tighter efficiency expectations. CDU pumps support energy optimization by matching coolant flow with thermal load rather than running at fixed speeds. Variable-speed pumps, efficient motor designs and better controls can reduce unnecessary pumping energy while improving cooling stability. This matters because liquid cooling infrastructure must deliver both thermal performance and cost discipline. The market benefits as operators retrofit existing facilities and design new AI-ready sites with more efficient cooling loops. For instance, the International Energy Agency projects global data center electricity consumption to double to about 945 TWh by 2030, increasing the need for efficient cooling systems.

Growth Of Liquid-To-Liquid CDU Architectures Across Hyperscale And Colocation Facilities

Liquid-to-liquid CDU systems dominate large-scale deployments because they connect IT cooling loops to facility water systems with strong heat transfer efficiency. The Global Data Center Cooling CDU Pumps Market benefits from this architecture because these systems require reliable pumps to circulate coolant across technology cooling systems and facility-side heat exchangers. Hyperscale operators and colocation providers prefer liquid-to-liquid CDU pumps for high-capacity deployments where uptime, compact footprint and scalable flow control are essential. For instance, Vertiv’s CoolChip CDU 2300 is a liquid-to-liquid unit that delivers 2.3 MW of cooling capacity and supports direct-to-chip cooling and rear-door heat exchangers.

Market Trends

Shift Toward High-Capacity CDU Pump Systems For Megawatt-Scale Cooling

The market is moving toward CDU pump systems that support megawatt-scale cooling capacity in compact footprints. This trend reflects the rapid increase in AI rack power and the need to cool multiple high-density racks from fewer CDU units. Pump suppliers are responding with stronger flow rates, redundant pump circuits, higher-pressure designs and more compact hydraulic layouts. This trend benefits vendors that can balance performance, reliability and ease of maintenance. For instance, CoolIT Systems introduced the CHx2000 CDU with 2 MW liquid cooling capacity, hot-swappable pumps and support for up to twelve 120 kW NVIDIA GB200 NVL72 racks.

Integration Of Smart Controls, Monitoring And Predictive Maintenance

CDU pump systems are becoming more intelligent as operators demand real-time visibility into flow, pressure, temperature and coolant condition. The Global Data Center Cooling CDU Pumps Market reflects this trend through pumps integrated with sensors, controls and remote monitoring. Smart pump control allows operators to adjust flow based on workload demand, reduce energy waste and detect faults before service disruption. This is especially important in AI and HPC facilities where downtime can be costly. For instance, Vertiv states that its CoolChip CDU controller adapts temperature and flow to workload demand and supports redundancy, unit-to-unit communication and remote monitoring.

Rising Demand For Retrofit-Friendly Liquid-To-Air CDU Pumps

Many existing data centers were not designed with facility water systems near IT racks. This creates rising demand for liquid-to-air CDU pumps that enable localized direct-to-chip cooling without full facility-water conversion. The Global Data Center Cooling CDU Pumps Market benefits because retrofits require compact units, safe coolant circulation and easy integration with existing air-cooled infrastructure. This trend is important for enterprise and colocation facilities that want to support AI workloads without building new sites. Boyd notes that liquid-to-air CDUs provide the benefits of liquid cooling without full-scale facility water implementation, using data center air conditioning to dissipate heat from server racks or rows.

Broader Use Of CDU Pumps In Immersion And Hybrid Liquid Cooling

The market is expanding beyond direct-to-chip cooling into immersion and hybrid cooling designs. CDU pumps are required to circulate coolant or transfer heat between immersion tanks, secondary loops and facility cooling infrastructure. Single-phase immersion remains easier to deploy, while two-phase immersion is gaining attention for specialized high-density applications. Hybrid liquid cooling also creates demand for pumps that can handle multiple flow paths and mixed thermal loads. This trend supports product diversification across pump type, flow rate and CDU configuration. Public market data shows the broader data center liquid cooling market is expected to grow from USD 4.8 billion in 2025 to USD 27.1 billion by 2035.

Market Challenges

Integration Complexity Across Existing Data Center Cooling Infrastructure

Integration remains a major challenge because many facilities were built around air cooling, chilled water systems and legacy mechanical layouts. CDU pump deployment often requires changes to piping, manifolds, leak detection, controls, maintenance routines and facility-water interfaces. Operators must also manage risk when introducing liquid loops near high-value IT assets. This can slow adoption in enterprise data centers and older colocation sites. The challenge is stronger in retrofit environments where floor space, water access and service windows are limited. Vendors must address these barriers through modular designs, installation support, training and strong reliability validation.

High Reliability Requirements And Concerns Around Leaks, Maintenance And Downtime

CDU pumps operate in mission-critical environments where failure can create immediate thermal risk. Buyers require redundant pumps, clean coolant chemistry, filtration, leak detection and high serviceability. Any concerns around leaks, pump wear, maintenance access or control failure can delay purchasing decisions. This challenge is especially important for BFSI, government, defense and healthcare users that prioritize uptime and operational risk control. Suppliers must prove long-life performance, compatibility with coolant formulations and stable operation under variable loads. This raises engineering requirements and increases the importance of qualification testing, service networks and system-level warranties.

Market Opportunities

Expansion Of AI-Ready Hyperscale And Colocation Data Centers

AI-ready hyperscale and colocation facilities create the strongest opportunity for the Global Data Center Cooling CDU Pumps Market. These operators need high-flow, high-pressure and redundant pump systems that can support direct-to-chip and hybrid liquid cooling at scale. New greenfield projects offer easier integration because facility water systems, manifolds and liquid cooling corridors can be designed from the start. Colocation providers also create recurring demand as they build liquid-cooled halls for cloud and AI customers. Vendors that offer scalable CDU pump systems, commissioning support and global service coverage can capture long-term growth from this shift.

Growth In Emerging Regions And Sovereign Digital Infrastructure Projects

Emerging markets create a strong opportunity as governments and enterprises invest in domestic cloud, AI, telecom and data infrastructure. Asia Pacific, the Middle East and Latin America are especially attractive because new data centers can adopt liquid cooling earlier in the design cycle. CDU pump suppliers can benefit from partnerships with engineering firms, data center operators and liquid cooling integrators. Demand will rise as regional operators deploy high-density workloads and seek better energy efficiency. Vendors that provide localized support, flexible product ranges and reliable maintenance models can strengthen their position in these developing markets.

Market Segmentation

By Pump Type

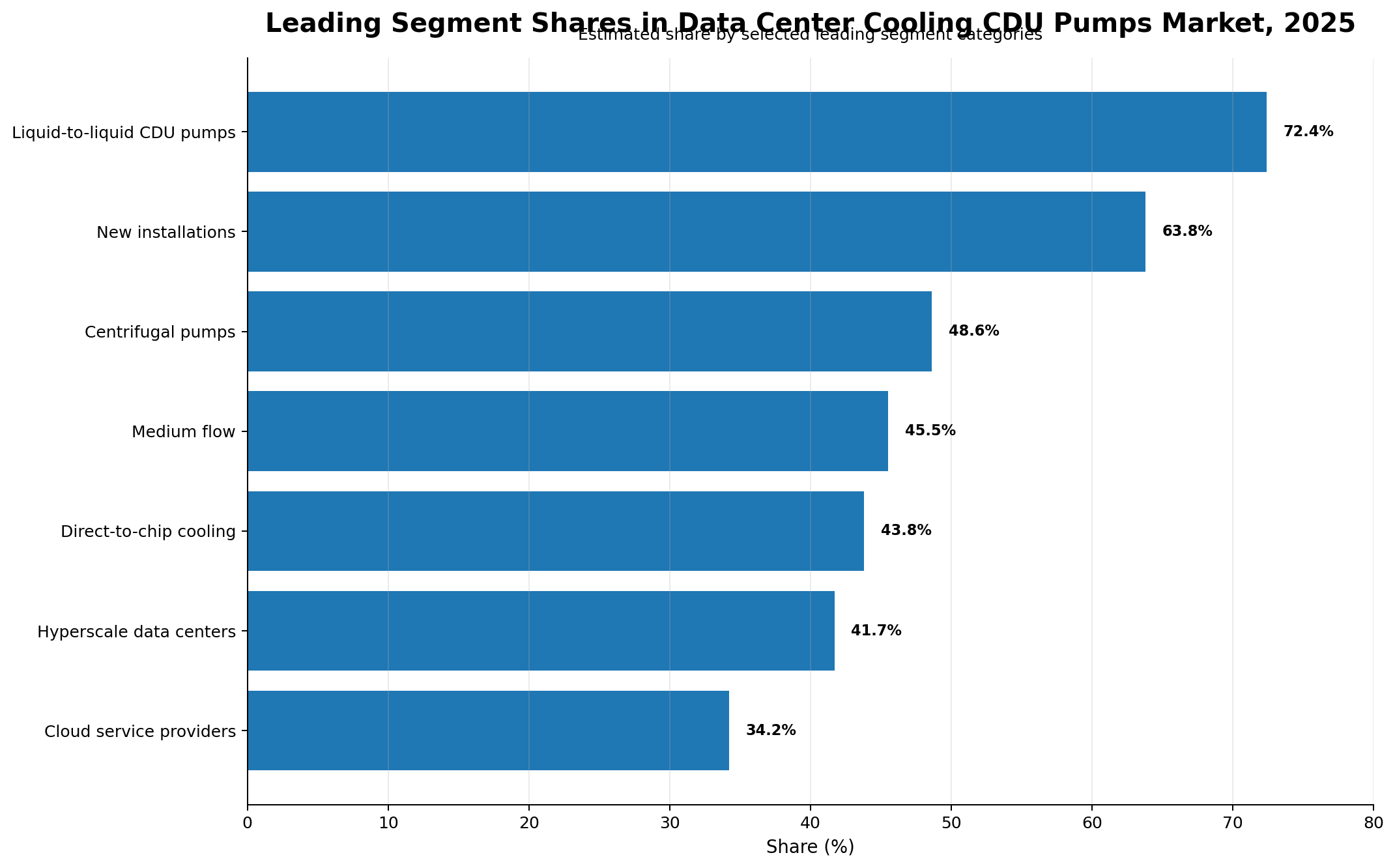

The Global Data Center Cooling CDU Pumps Market by pump type includes centrifugal pumps, positive displacement pumps, magnetic drive pumps and inline pumps. Centrifugal pumps led the segment with an estimated 48.6% share in 2025 because they offer strong flow capacity, proven reliability and effective performance across liquid-to-liquid CDU systems. Positive displacement pumps hold demand where controlled dosing, precise flow and pressure management are required. Magnetic drive pumps are gaining traction due to leak-reduction advantages and sealed-drive designs. Inline pumps remain important in compact CDU architectures because they support space efficiency and easier integration into rack, row and facility-level cooling loops.

By Cooling Technology

The market by cooling technology includes direct-to-chip liquid cooling, immersion cooling, single-phase immersion, two-phase immersion and hybrid liquid cooling. Direct-to-chip liquid cooling held the largest share at about 43.8% in 2025 because it provides efficient heat removal at CPUs, GPUs and accelerators while fitting well into hyperscale and colocation designs. Immersion cooling is expanding in specialized high-density and HPC deployments. Single-phase immersion remains more practical for near-term adoption due to lower complexity, while two-phase immersion is used in advanced workloads. Hybrid liquid cooling is growing because many facilities combine air, liquid and rear-door approaches during phased transitions.

By End-User / Vertical

The market by end-user includes cloud service providers, AI and machine learning data centers, telecommunications, BFSI, government and defense, healthcare, manufacturing, research and academia and others. Cloud service providers dominated with an estimated 34.2% share in 2025 due to large-scale AI infrastructure deployment, rapid capacity expansion and higher willingness to adopt advanced cooling technologies. AI and machine learning data centers represent the fastest-growing vertical due to GPU cluster growth. Telecommunications demand is rising through edge and network workloads. BFSI, government and healthcare rely on CDU pumps where uptime, security and thermal reliability are critical for digital operations.

By Data Center Type

The market by data center type includes hyperscale data centers, colocation data centers, enterprise data centers, edge/micro data centers and high-performance computing data centers. Hyperscale data centers led with an estimated 41.7% share in 2025 because large cloud and AI operators deploy liquid cooling at significant scale. Colocation data centers follow closely as providers build high-density halls for enterprise AI and cloud customers. Enterprise data centers adopt CDU pumps more gradually, often through retrofits and selective high-density zones. Edge and micro data centers use smaller systems, while HPC data centers require advanced flow control, high reliability and strong cooling capacity.

By Flow Rate

The market by flow rate includes low flow below 100 L/min, medium flow from 100 to 300 L/min and high flow above 300 L/min. Medium flow systems held the largest share at about 45.5% in 2025 because they serve a wide range of rack-level and row-level CDU applications. High-flow systems are expected to grow faster due to AI clusters, megawatt-scale CDU deployment and higher coolant circulation requirements. Low-flow systems remain relevant in smaller enterprise, edge and laboratory environments where cooling demand is more limited. Flow-rate selection depends on rack density, coolant type, heat exchanger design and redundancy requirements.

By CDU Type

The market by CDU type includes liquid-to-liquid CDU pumps and liquid-to-air CDU pumps. Liquid-to-liquid CDU pumps led with an estimated 72.4% share in 2025 because hyperscale and high-density deployments prefer facility-water integration for efficient heat rejection. These systems are better suited for large AI halls, HPC clusters and colocation facilities with advanced mechanical infrastructure. Liquid-to-air CDU pumps hold a smaller share but are important in retrofit projects where facility water is unavailable or expensive to introduce. This segment will grow as operators seek practical ways to add direct-to-chip cooling to existing air-cooled data centers.

By Installation

The market by installation includes new installations and retrofit installations. New installations, or greenfield projects, accounted for about 63.8% of the market in 2025 because operators can design liquid cooling systems, CDU placement, piping and monitoring into the facility from the beginning. This lowers integration risk and supports higher-density deployment. Retrofit installations remain important as existing enterprise and colocation facilities upgrade to support AI workloads. Retrofit demand is likely to rise over the forecast period because many operators must extend useful facility life while supporting higher rack densities. Vendors that simplify installation and minimize downtime will gain advantage.

Regional Insights

North America And Europe Maintain Leadership Through AI Infrastructure Expansion And Early Liquid Cooling Adoption

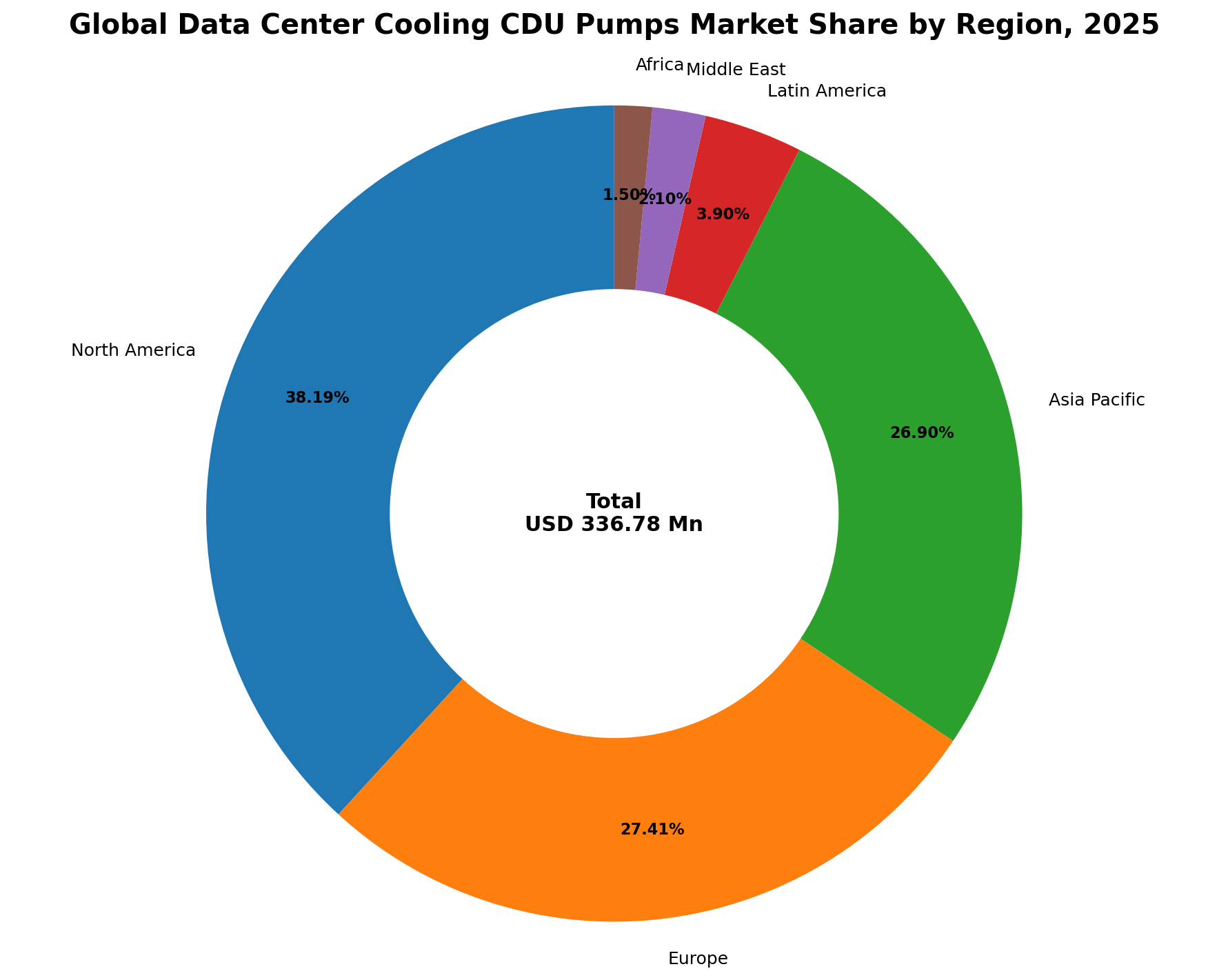

North America led the Global Data Center Cooling CDU Pumps Market with USD 128.62 million in 2025, accounting for 38.19% share. The United States remains the main contributor due to hyperscale AI investment, advanced cloud infrastructure and early adoption of liquid cooling technologies. Canada adds demand through colocation development and research computing, while Mexico shows gradual progress through enterprise and telecom modernization. Europe held USD 92.31 million in 2025, representing 27.41% share. Demand across Germany, the UK, France, Italy, Spain and the Nordics is supported by energy-efficiency goals, high-performance computing and regulated digital infrastructure. Uptime Institute’s 2025 survey highlights rising costs, worsening power constraints and challenges in meeting AI demand, which strengthens the case for advanced cooling systems in mature data center regions.

Asia Pacific Emerges As A High-Growth Region With Strong Cloud, AI And Manufacturing Support

Asia Pacific accounted for USD 90.60 million in 2025, equal to 26.90% share of the Global Data Center Cooling CDU Pumps Market. China, Japan, South Korea and India remain major demand centers due to cloud growth, AI investments, semiconductor ecosystems and strong digital infrastructure expansion. Southeast Asia is also gaining momentum as Singapore, Malaysia, Indonesia and Thailand attract new data center projects. The region benefits from greenfield development, which allows liquid cooling and CDU pump systems to be designed into new facilities. Delta Electronics showcased liquid cooling solutions in 2025, including in-rack liquid-to-liquid CDUs with cooling capacity of up to 200 kW per rack for high-density GPU and AI deployments.

Latin America, Middle East And Africa Gain Ground Through Cloud Expansion And Sovereign Data Center Projects

Latin America generated USD 13.13 million in 2025, accounting for 3.90% share, with Brazil and Mexico representing the strongest demand pockets. The Middle East reached USD 7.07 million in 2025, representing 2.10% share, supported by sovereign cloud projects, smart city programs and AI infrastructure investment across GCC countries. Africa held USD 5.05 million in 2025, equal to 1.50% share, with South Africa leading adoption through colocation and financial sector digitization. These regions remain smaller in revenue terms but offer solid long-term growth potential as new data centers adopt high-density cooling systems earlier in the design cycle. The opportunity is strongest where operators combine cloud expansion with energy-efficient thermal infrastructure.

Competitive Insights:

- Grundfos

- Xylem Inc.

- Wilo Group

- KSB SE & Co. KGaA

- Ebara Corporation

- Flowserve Corporation

- SPX FLOW

- Armstrong Fluid Technology

- Vertiv

- Schneider Electric

- CoolIT Systems

- Boyd

- Delta Electronics

- Parker Hannifin

- Alfa Laval

The Global Data Center Cooling CDU Pumps Market features competition between pump manufacturers, thermal management specialists, data center infrastructure vendors and liquid cooling system providers. Grundfos, Xylem, Wilo, KSB, Ebara, Flowserve, SPX FLOW, Armstrong Fluid Technology and Parker Hannifin compete through pump engineering, hydraulic efficiency, reliability and service depth. Vertiv, Schneider Electric, CoolIT Systems, Boyd and Delta Electronics hold stronger positions in integrated CDU systems, direct-to-chip cooling infrastructure and AI-ready data center platforms. Alfa Laval contributes through heat exchange and thermal system expertise. Competition is intensifying as operators demand higher cooling capacity, lower energy use, redundant pump designs, smart controls and compact footprints. Vendors that can combine pump reliability with CDU-level integration, monitoring, coolant compatibility and global service support will hold a stronger competitive edge.

Recent Developments:

- In November 2024, Vertiv announced two high-capacity coolant distribution units, including the Vertiv CoolChip CDU 2300kW liquid-to-liquid system and the CoolChip CDU 350kW liquid-to-air system. The 2.3 MW model targets large-scale liquid cooling deployments for hyperscale and colocation providers.

- In April 2025, CoolIT Systems introduced the CHx2000 row-based CDU with 2 MW cooling capacity, compact 750 mm by 1,200 mm footprint, hot-swappable pumps and support for high-density AI deployments.

- In October 2025, Delta Electronics showcased cooling and infrastructure solutions for data centers at Data Centre World Asia, including in-rack liquid-to-liquid CDUs with up to 200 kW cooling capacity per rack for GPU and AI workloads.

- In January 2026, Motivair by Schneider Electric introduced new CDU models designed for HPC, AI factory and data center environments, with global availability and production ramp-up planned in early 2026.

- In March 2026, Ecolab announced it would acquire CoolIT Systems for about USD 4.75 billion in cash to expand into liquid cooling for AI data centers, with the transaction expected to close in the third quarter of 2026.