Executive summary:

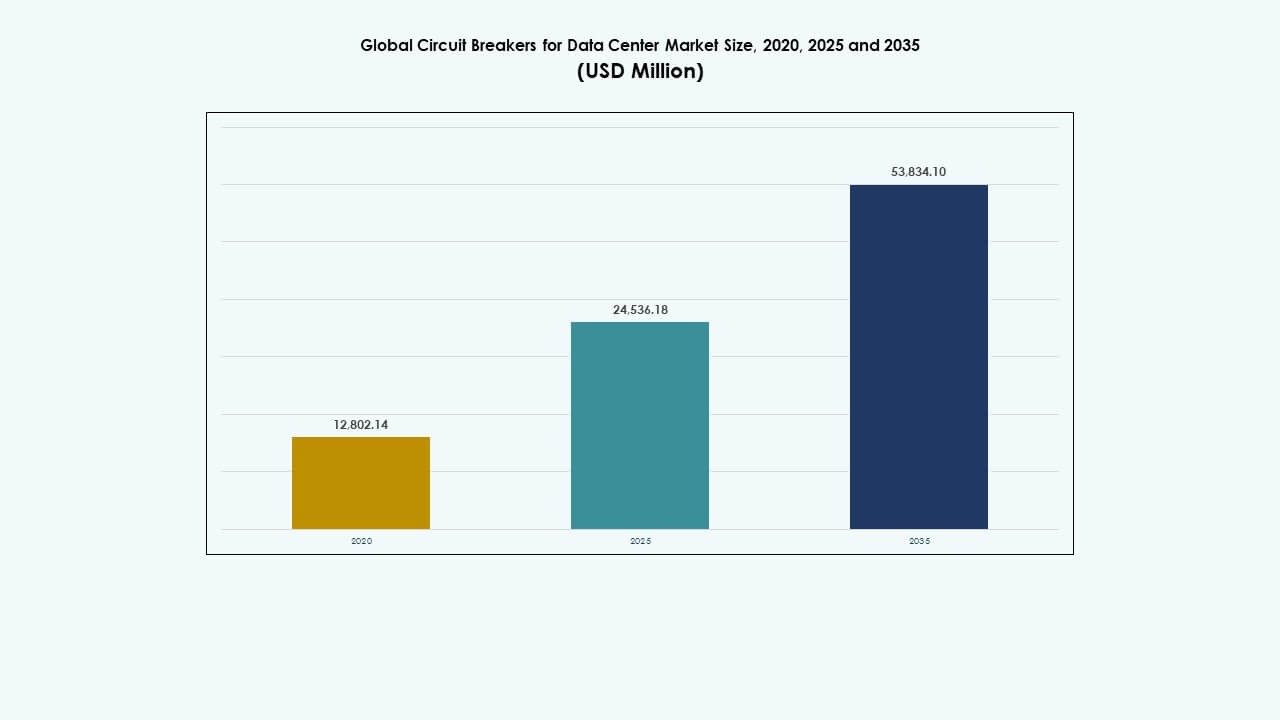

The Global Circuit Breakers for Data Center Market size was valued at USD 12,802.14 million in 2020, grew to USD 24,536.18 million in 2025, and is anticipated to reach USD 53,834.10 million by 2035, at a CAGR of 8.11% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2035 |

| Circuit Breakers for Data Center Market Size 2025 |

USD 24,536.18 Million |

| Circuit Breakers for Data Center Market, CAGR |

8.11% |

| Circuit Breakers for Data Center Market Size 2035 |

USD 53,834.10 Million |

Strong demand for intelligent power protection is driving this market forward. Operators are adopting smart circuit breakers with remote monitoring, diagnostics, and modular form factors. Innovation in solid-state and arc flash protection is reshaping product designs. The shift toward AI workloads, edge computing, and high-density power architectures raises the importance of reliable circuit protection. Businesses view advanced breakers as critical assets to maintain uptime and power quality. Investors prioritize vendors offering scalable and digitally integrated solutions for growing data environments.

North America leads the market, supported by a mature hyperscale ecosystem and strong digital infrastructure. Europe shows consistent growth due to green data center standards and modernization needs. Asia-Pacific is rapidly expanding, with China, India, and Southeast Asia emerging as major hubs. These regions benefit from cloud adoption, urbanization, and policy support. Latin America, the Middle East, and Africa show early-stage activity, driven by telecom growth and enterprise digitization.

Market Drivers

Growing Demand for High-Performance Power Distribution in Hyperscale and Colocation Data Centers

Hyperscale and colocation operators continue to expand globally, raising demand for advanced power protection. Circuit breakers play a critical role in minimizing downtime and protecting mission-critical loads. The need for high power density, rapid fault response, and low latency in energy delivery strengthens the case for intelligent circuit breakers. Smart breakers offer real-time monitoring, remote operation, and trip diagnostics. These features are essential in facilities handling AI, machine learning, and edge computing tasks. Global Circuit Breakers for Data Center Market growth aligns with these evolving operational needs. It supports facility uptime, power quality, and fault containment. Companies seek modular and scalable solutions to match changing load profiles. Smart power protection infrastructure is becoming an investment priority across Tier III and Tier IV data centers.

- For example, ABB’s SACE Emax 2 breakers were installed in a financial services data center by ILS Electro Mechanical Supplies, with 50 E1.2 units up to 1600A, 60 E2.2 up to 2500A, and 20 E4.2 up to 4000A, achieving 20% footprint savings and 15 sqm more space for IT equipment via compact design and Ekip Touch trip units with 1% current accuracy per IEC 61557-12.

Increased Deployment of Intelligent Circuit Breakers with IoT and Embedded Control Capabilities

The industry shift toward software-defined infrastructure is pushing demand for circuit breakers that support data visibility and control. Digital circuit breakers now come with onboard sensors, IoT communication, and self-testing capabilities. These systems integrate with DCIM platforms and energy management tools. Operators gain actionable insights into load patterns, fault occurrences, and breaker health. It reduces manual intervention and simplifies predictive maintenance schedules. Businesses value the transparency and data granularity these breakers provide. Global Circuit Breakers for Data Center Market reflects the move toward digital-native operations in energy management. Integrating intelligent breakers ensures greater automation in fault detection and system recovery. This technology adoption supports cost optimization and higher availability.

Shift Toward Energy Efficiency and Regulatory Compliance in Power Infrastructure

Energy regulations are becoming stricter, especially in Europe and North America. Facilities must comply with efficiency mandates, renewable integration, and grid-interactive operations. Circuit breakers support these goals by enabling sectional control, load shedding, and energy usage tracking. Their design evolution improves energy efficiency with reduced contact resistance and arc losses. Global data center operators invest in circuit protection systems aligned with green building standards. Global Circuit Breakers for Data Center Market is influenced by sustainability targets and carbon reduction strategies. It supports adoption of eco-efficient breakers with recyclable materials and minimal heat loss. This regulatory pressure encourages procurement of next-gen protection gear.

- For example, ABB’s SACE Emax 2 Ekip Touch trip units in data center switchgear provide continuous measurements and historical logs (events, trips) via integrated Modbus RTU to DCIM systems, supporting efficiency through precise 1% accuracy monitoring without added modules.

Need for High Availability and Fault-Tolerant Electrical Designs in Modern Facilities

Downtime in data centers leads to financial and reputational losses. Operators focus on achieving N+1 or 2N redundancy through reliable electrical layouts. Circuit breakers serve as core components in fault-tolerant designs, ensuring isolation without affecting adjacent circuits. They enable safe switching, selective coordination, and real-time status updates. Adoption of zone-selective interlocking and energy-limiting designs has grown. These features reduce damage to sensitive IT equipment. Global Circuit Breakers for Data Center Market benefits from the push toward operational excellence and risk mitigation. It enables secure, fast restoration following short circuits, ground faults, or overloads. System-wide fault analysis and trip time optimization are critical design considerations today.

Market Trends

Market Trends

Adoption of Solid-State Circuit Breakers for Faster Switching and Space-Saving Designs

Solid-state circuit breakers are gaining traction in edge and modular data centers. These devices offer ultra-fast switching without mechanical parts, improving reliability. They consume less space and operate silently, suiting high-density racks. Their programmable logic enables adjustable trip thresholds and arc flash mitigation. Unlike traditional models, they integrate into smart bus systems and allow seamless firmware updates. Global Circuit Breakers for Data Center Market sees growing preference for solid-state types in next-generation deployments. Their design supports automation, reduced latency, and improved energy efficiency. Solid-state adoption is reshaping expectations in speed and responsiveness.

Integration of Circuit Breakers into Busbar and Rack Power Distribution Architectures

Data center designs are becoming compact and modular. Traditional wiring is being replaced by busbar systems and intelligent rack PDUs. Circuit breakers are now embedded in these architectures for localized protection. Operators benefit from simplified cable management, faster deployment, and reduced installation costs. Breakers with remote reset and modular slots support future scalability. Global Circuit Breakers for Data Center Market reflects this trend of integrated power management. Facilities now demand rack-level circuit control with remote firmware access. This architectural shift improves thermal performance and power distribution density.

Deployment of Breakers Supporting Remote Operation, Diagnostics, and Firmware Updates

The move toward lights-out data centers increases demand for remote operability. Modern circuit breakers allow wireless diagnostics, status alerts, and fault trip capture. Technicians receive real-time notifications via integrated apps and dashboards. Breakers supporting over-the-air firmware updates enhance serviceability. This reduces on-site maintenance time and improves operational continuity. Global Circuit Breakers for Data Center Market benefits from this remote-centric control model. It aligns with unmanned site strategies and centralized monitoring platforms. Operators expect higher functionality with minimal manual input.

Growth of Arc-Flash Mitigation and Zone-Selective Interlocking Features in Breaker Systems

Safety remains a major concern in high-capacity electrical rooms. New circuit breakers offer built-in arc flash protection, reducing injury risk. Zone-selective interlocking enables coordinated tripping to isolate faults precisely. These features protect staff and minimize equipment damage. Demand is rising in hyperscale and colocation sites where fault energy is high. Global Circuit Breakers for Data Center Market sees increased investment in safety-enhancing designs. Businesses prioritize safety ratings and fault-clearing speed in procurement. These features support compliance with workplace safety standards.

Market Challenges

Market Challenges

Complexity in Upgrading Legacy Systems with Intelligent Breaker Technologies and Digital Control

Many existing data centers operate on traditional electrical infrastructure. Upgrading these environments with smart breakers involves cost, compatibility checks, and layout redesigns. Integration with existing switchgear and DCIM platforms requires skilled engineering. Not all legacy systems support plug-and-play retrofits or open protocols. Global Circuit Breakers for Data Center Market growth may slow where retrofitting is not feasible or financially viable. Smaller operators may delay upgrades due to limited ROI clarity. Mismatched voltage ratings and outdated panel configurations add to the challenge. Training needs for service staff also increase during tech transitions.

High Cost of Premium Circuit Breaker Solutions and Limited Supplier Consolidation Globally

Advanced circuit breakers with IoT, arc flash control, and modularity come at a high cost. Procurement teams must balance capital investment with long-term reliability goals. In emerging regions, pricing remains a barrier to adoption of intelligent systems. Global Circuit Breakers for Data Center Market faces constraints in regions with fewer local suppliers and slower regulatory adoption. OEM options are limited in some countries, increasing lead times and maintenance complexity. Cost-conscious operators often defer adoption or limit it to high-load sections only. This creates uneven deployment and fragmented maintenance strategies across markets.

Market Opportunities

Expansion of Edge Data Centers and Regional Colocation Facilities in Emerging Economies

The shift toward edge computing creates demand for compact, intelligent circuit protection in remote sites. These deployments need flexible breakers that operate in constrained environments. It opens new growth opportunities in Southeast Asia, Latin America, and Eastern Europe. Global Circuit Breakers for Data Center Market can tap into rising digitization and cloud expansion in these regions. Vendors focusing on local support, training, and modular designs are well positioned.

Focus on Sustainability and Integration of Eco-Efficient, Low-Loss Breaker Designs

Green data centers prefer circuit breakers with minimal energy loss and recyclable parts. OEMs offering low-resistance designs and compliance with green standards stand to gain. It enables operators to meet ESG goals while improving operational efficiency. Global Circuit Breakers for Data Center Market benefits from increasing preference for energy-saving and sustainable technologies.

Market Segmentation:

By Voltage

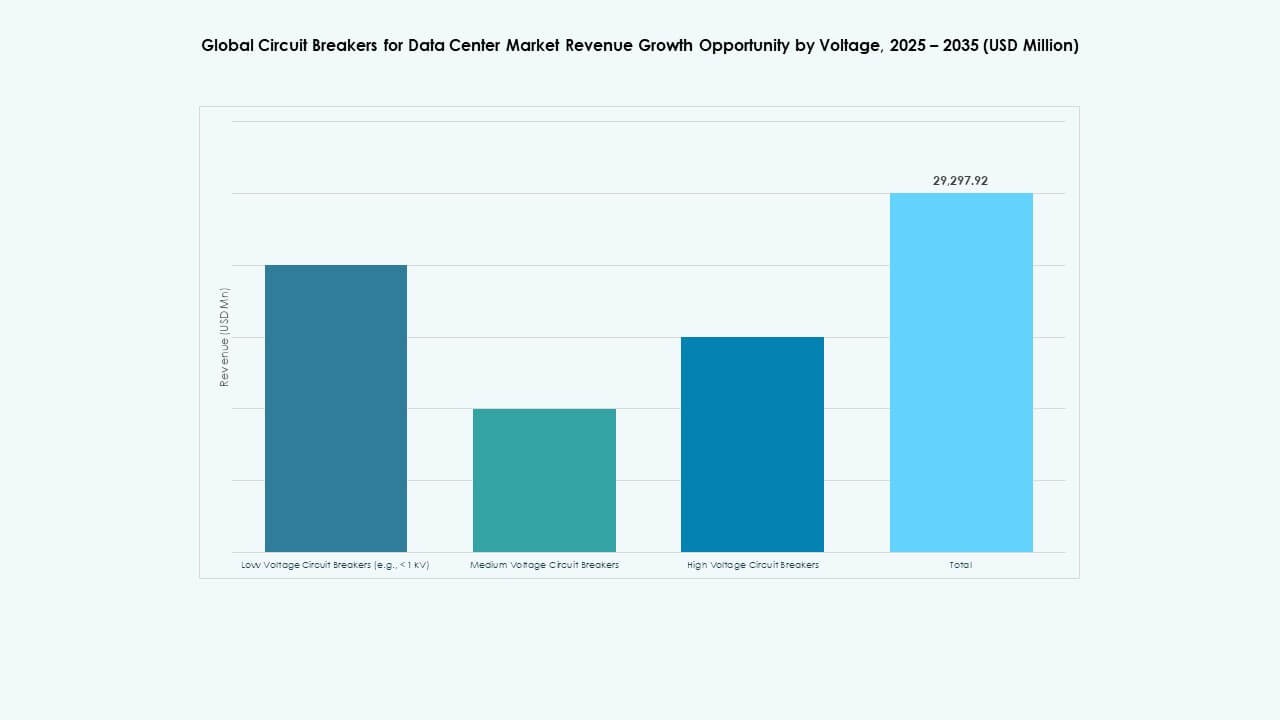

In the Global Circuit Breakers for Data Center Market, low voltage circuit breakers (< 1 kV) dominate due to their widespread use in IT racks, PDUs, and UPS systems. These are critical for downstream protection in hyperscale and enterprise facilities. Medium voltage breakers are gaining traction in main distribution boards and backup systems. High voltage breakers remain niche, used primarily in large-scale utility-linked campuses. The low voltage segment holds the largest share, driven by demand for compact, intelligent, and easily replaceable units with advanced monitoring and remote control features.

By Type

Among circuit breaker types, air circuit breakers lead the Global Circuit Breakers for Data Center Market due to their use in low and medium voltage panels and easy maintenance features. Vacuum circuit breakers are preferred for medium voltage switchgear, offering arc extinguishing in compact form. Gas-insulated (SF₆) breakers find use in space-constrained and high-reliability environments but face sustainability concerns. Oil circuit breakers are in decline, used rarely due to higher maintenance and environmental risks. Air and vacuum types dominate due to wide compatibility, fast operation, and integration into smart control systems.

By Application

Power distribution is the leading application segment in the Global Circuit Breakers for Data Center Market, accounting for the majority of installed units. Circuit breakers are essential in protecting distribution panels, rack PDUs, and backup systems across hyperscale and edge facilities. Power transmission applications, though smaller in share, involve medium and high voltage protection across incoming utility lines and substation interfaces. Growth in distribution-focused applications is driven by increasing rack power densities and segmented circuit layouts supporting fail-safe operations and rapid restoration.

By Rated Current

Circuit breakers rated 500 A to 1,500 A dominate the Global Circuit Breakers for Data Center Market due to their fit for typical distribution boards and backup connections in modern data centers. Units below 500 A are commonly used in rack-level protection and modular setups. Ratings above 2,500 A are deployed in hyperscale switchgear, especially where large IT load clusters demand fault tolerance. The 500 A–1,500 A range sees highest adoption, offering optimal balance between protection range, flexibility, and compact design for high-density layouts.

By Data Center Type

Hyperscale data centers represent the largest segment in the Global Circuit Breakers for Data Center Market, driven by growing AI workloads, cloud expansion, and need for robust power protection. These facilities require hundreds of circuit breakers integrated into smart panels and zone-based distribution systems. Colocation providers also contribute significantly, adopting scalable breakers for diverse client setups. Edge and modular data centers are emerging as high-growth areas, requiring compact and intelligent circuit breakers. Hyperscale dominance stems from massive power infrastructure, high uptime targets, and continuous facility expansion globally.

Regional Insights:

Regional Insights:

North America and Europe

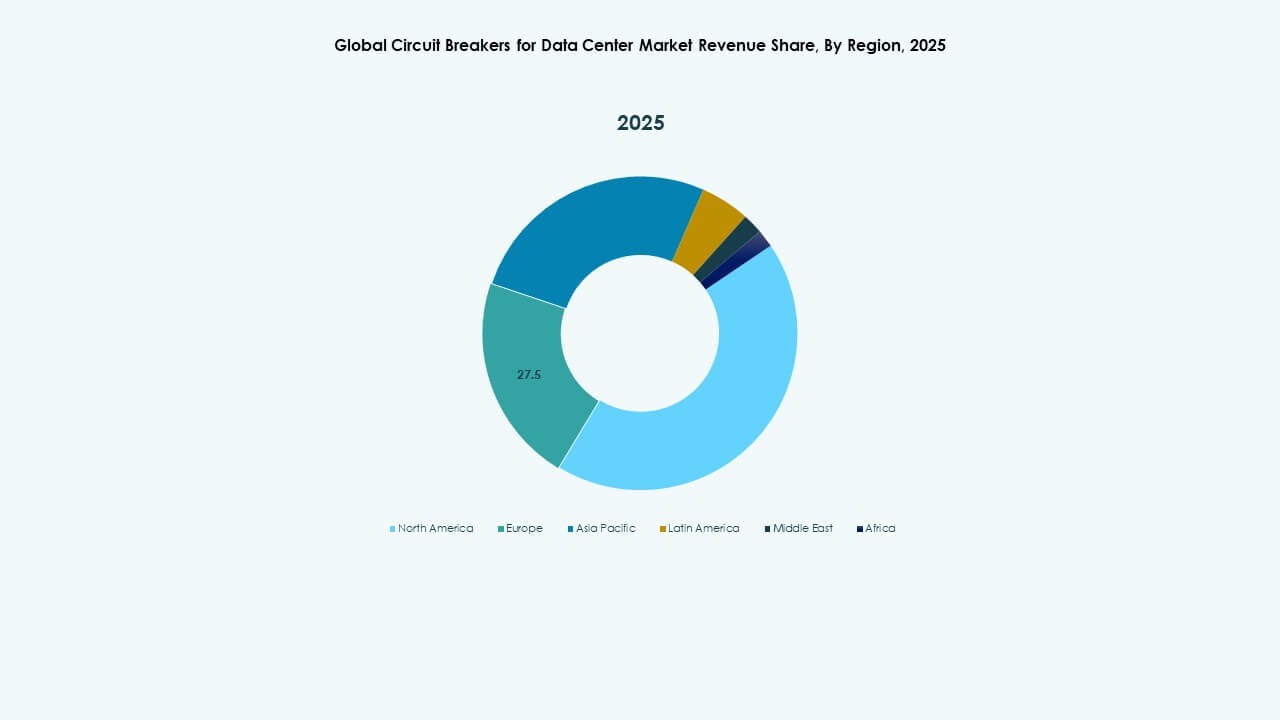

North America leads the Global Circuit Breakers for Data Center Market with over 35% market share. Strong hyperscale presence, rising AI workloads, and advanced power infrastructure drive demand. The U.S. remains dominant due to continued expansions by Amazon, Microsoft, and Google. Canada and Mexico also show growth through colocation and enterprise facility upgrades. Europe holds about 25% share, with Germany, the UK, and the Netherlands investing in energy-efficient data centers. Regulatory mandates on energy performance and safety influence breaker adoption across both low and medium voltage systems. It benefits from modernization projects and rising edge deployments.

- For instance, in October 2025, Amazon activated Project Rainier, an AI compute cluster powered by nearly 500,000 Trainium2 chips to support large-scale AI workloads across multiple data center facilities in Indiana. This marks one of AWS’s largest AI infrastructure deployments to date.

Asia-Pacific

Asia-Pacific accounts for roughly 28% of the Global Circuit Breakers for Data Center Market. China dominates regional demand, backed by large-scale government initiatives and hyperscale growth. India shows strong momentum in cloud services, fintech, and telecom-backed data centers. Japan and South Korea prioritize smart grid integration and high-reliability electrical designs, boosting demand for intelligent circuit breakers. Southeast Asian countries including Indonesia, Malaysia, and Vietnam continue to attract investments in modular and colocation sites. It supports high growth in volume, with power reliability and scalable design as key purchasing criteria. Vendors are localizing support and enhancing supply chains to meet rising demand.

- For instance, in November 2025, NTT, Chunghwa Telecom, and Accton/Edgecore began collaboration to enhance distributed data centers, integrating advanced network technologies to support AI infrastructure development.

Latin America, Middle East, and Africa

Latin America holds around 6% of global share, led by Brazil and Mexico through regional cloud expansions and financial sector digitalization. The Middle East contributes about 4%, driven by the UAE and Saudi Arabia, where smart city and AI infrastructure projects increase circuit protection needs. Africa remains nascent with approximately 2% share, focused on South Africa, Egypt, and Nigeria where telecom and cloud activity is growing. The Global Circuit Breakers for Data Center Market in these regions gains traction through increased power stability, cross-border connectivity, and digital government efforts. It presents long-term growth opportunities through public-private partnerships and infrastructure modernization.

Competitive Insights:

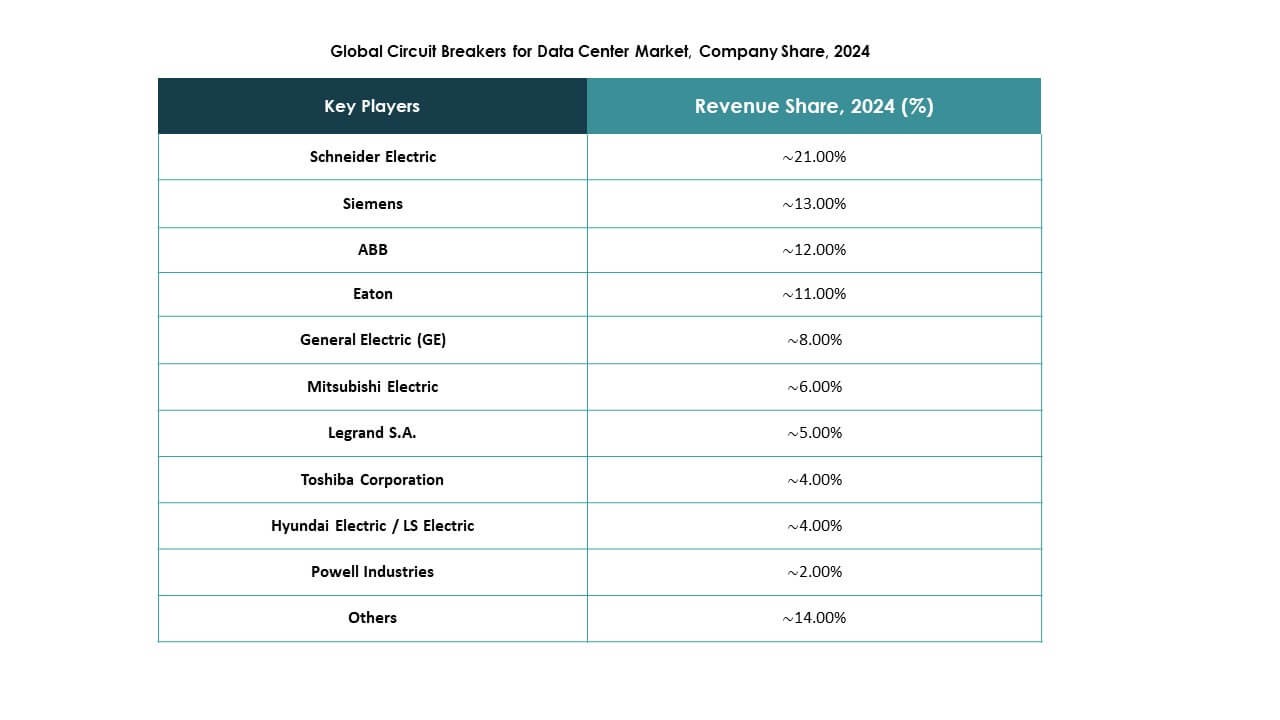

- Schneider Electric

- ABB

- Eaton

- Siemens

- Mitsubishi Electric Corporation

- General Electric (GE)

- Legrand S.A.

- Toshiba Corporation

- Hyundai Electric / LS Electric

- Powell Industries

The Global Circuit Breakers for Data Center Market features a consolidated competitive landscape led by multinational power equipment manufacturers. Schneider Electric, ABB, Eaton, and Siemens hold strong positions through broad product portfolios, global distribution, and advanced digital circuit breaker technologies. These players focus on intelligent, modular systems with real-time diagnostics and integration capabilities for data center applications. Mitsubishi Electric, GE, and Toshiba cater to medium and high voltage segments with reliable and compact breaker solutions. Regional players such as Hyundai Electric and Powell Industries serve niche needs with tailored offerings for specific voltage classes. It remains innovation-driven, with competition centered around safety features, IoT readiness, arc flash protection, and low maintenance. Strategic partnerships with data center operators, system integrators, and EPC contractors are key to expanding market reach and securing multi-year contracts.

Recent Developments:

Recent Developments:

- In October 2025, ABB introduced its next‑generation MNS® low‑voltage power distribution solution that integrates the new SACE Emax 3 air circuit breaker for AI‑ready data centers.

- In June 2025, Eaton and Siemens Energy formed a collaboration to accelerate deployment of new data center capacity by delivering integrated on‑site power systems.