Executive summary:

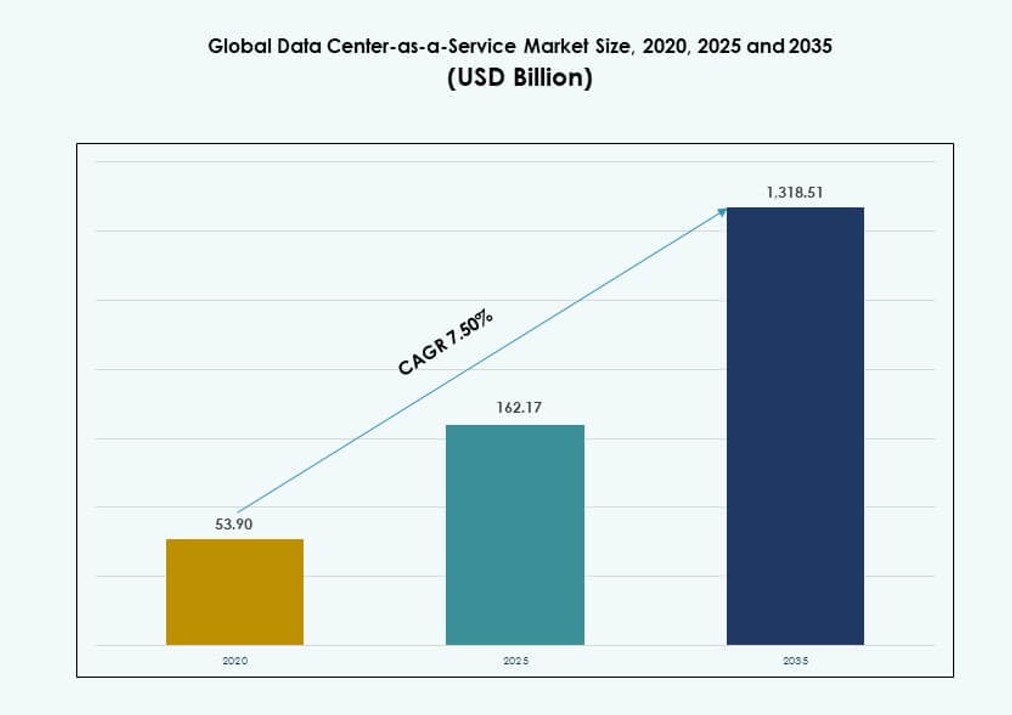

The Global Data Center-as-a-Service Market size was valued at USD 53.9 billion in 2020 to USD 162.17 billion in 2025 and is anticipated to reach USD 1,318.51 billion by 2035, at a CAGR of 7.50% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2035 |

| Data Center-as-a-Service Market Size 2025 |

USD 162.17 Billion |

| Data Center-as-a-Service Market, CAGR |

7.50% |

| Data Center-as-a-Service Market Size 2035 |

USD 1,318.51 Billion |

Cloud adoption and the demand for scalable, flexible infrastructure are driving strong momentum in this market. Businesses seek rapid deployment, cost efficiency, and hybrid cloud compatibility without investing in physical assets. Innovations in software-defined infrastructure and AI-led automation make service models more efficient and responsive. Enterprises prioritize resilience, uptime, and ease of orchestration, making DCaaS a strategic asset. For investors, recurring revenue streams and growing enterprise dependence on hosted services add financial attractiveness.

North America remains the dominant region due to mature hyperscaler activity and enterprise digital transformation. Europe follows with strong regulatory compliance demand and sovereign cloud expansion. Asia-Pacific is emerging rapidly, with China, India, and Southeast Asia seeing increased demand from startups and SMEs. These markets benefit from growing mobile usage, data localization policies, and rising cloud-first strategies in regional economies.

Market Dynamics:

Market Drivers

Cloud Infrastructure Modernization and IT Flexibility Fuel Enterprise Adoption

The Global Data Center-as-a-Service Market is gaining traction due to enterprises replacing legacy data centers with scalable cloud infrastructure. Businesses now require on-demand services that support workload agility and real-time resource scaling. The shift toward hybrid and multi-cloud environments enables IT departments to optimize performance across geographies. DCaaS solutions allow firms to reduce capital expenditure while improving operational efficiency. Innovations in software-defined infrastructure support seamless workload orchestration. Enterprises benefit from faster deployment timelines, minimal upfront investments, and outsourced maintenance. It enables CIOs to shift focus from hardware to service-level performance. For investors, it presents a stable recurring revenue model aligned with digital transformation budgets.

- For instance, Netflix migrated its core infrastructure to AWS, scaling to handle over 280 million global subscribers with auto-scaling groups that adjust compute resources in seconds during peak loads.

Edge Computing Acceleration Increases Strategic Value for DCaaS Providers

Rising demand for latency-sensitive applications has accelerated investment in edge computing, which complements centralized DCaaS models. Enterprises adopting IoT, autonomous systems, and AR/VR applications require data to be processed closer to the user. Data Center-as-a-Service vendors integrate edge nodes within hybrid cloud strategies to improve responsiveness and minimize bandwidth use. This distributed architecture strengthens market stickiness among clients seeking geographic redundancy and compliance with data sovereignty laws. The Global Data Center-as-a-Service Market gains strategic value by offering modular, scalable footprints across metro and Tier II regions. Providers able to meet regional demands without replicating full-scale infrastructure hold competitive advantage.

Enterprise Digitalization and Demand for Zero-Downtime Operations Expand DCaaS Utility

Digitalization strategies in banking, retail, and manufacturing sectors demand always-on infrastructure with real-time failover. Data Center-as-a-Service platforms offer high availability, SLA-backed uptime, and automated failover mechanisms without the capital complexity of building physical sites. Enterprises adopting SaaS, AI workloads, and ERP systems rely on DCaaS for guaranteed compute continuity. It also enables business continuity planning by decentralizing infrastructure risks. Data-intensive verticals now prioritize uptime over ownership, which boosts service contract volumes. The Global Data Center-as-a-Service Market supports mission-critical operations in environments where minutes of downtime translate into revenue losses. This operational assurance aligns with long-term digital growth roadmaps.

Sustainability Pressures and ESG Policies Reinforce DCaaS Investment Logic

Enterprise commitments to ESG goals push IT leaders to offload power-intensive infrastructure. Colocation and managed cloud services offer higher energy efficiency and carbon transparency than self-owned data centers. Modern DCaaS providers adopt green building certifications, renewable energy integration, and AI-led cooling systems. These capabilities allow enterprises to meet reporting standards while benefiting from technical upgrades. The Global Data Center-as-a-Service Market capitalizes on this by positioning itself as a cleaner alternative to legacy infrastructure. Investors tracking sustainable technology portfolios increasingly allocate capital to green data infrastructure plays. This momentum ensures long-term market relevance and institutional funding support.

- For example, Google data centers achieved an average annual PUE of 1.09 in 2024. This reflects AI-optimized cooling and 100% renewable energy matching for power consumption.

Market Trends

Service Consumption Models Are Shifting from Fixed CapEx to Scalable Opex Contracts

Organizations now favor flexible, pay-as-you-go consumption models over rigid capital expenditures for data center infrastructure. This change reflects evolving procurement priorities in IT operations. DCaaS solutions allow businesses to scale up or down with real-time demand without locking capital in depreciating assets. Subscription-based pricing offers budget predictability and aligns with software-driven operations. The Global Data Center-as-a-Service Market adapts to this trend by bundling compute, storage, and support in modular, SLA-bound packages. Enterprises prefer this structure to manage seasonal workloads and short-term projects efficiently. It also simplifies vendor management by consolidating infrastructure and service layers into one provider.

AI Integration into DCaaS Improves Infrastructure Efficiency and Predictive Maintenance

Leading providers embed AI and machine learning into infrastructure monitoring and resource allocation. These tools improve thermal efficiency, anticipate system failures, and reduce unplanned downtime. Real-time analytics optimize server performance and load balancing. Predictive maintenance reduces operational costs by preventing hardware faults. The Global Data Center-as-a-Service Market is adopting AI to improve customer satisfaction through proactive support. Intelligent automation enhances SLA performance and allows leaner management teams to control complex workloads. This capability differentiates high-performing vendors from commodity service providers. It also boosts profit margins in competitive service pricing environments.

Tier II and Emerging Markets Are Becoming Focal Points for Strategic Expansion

Demand for low-latency cloud services has prompted providers to expand footprints beyond major metro hubs. Enterprises in developing economies increasingly require local hosting options for compliance and performance needs. The Global Data Center-as-a-Service Market now sees regional buildouts in South Asia, Eastern Europe, and parts of Africa. Strategic deployments focus on underpenetrated areas where infrastructure investments remain low. Localized nodes enable faster application delivery, improved disaster recovery, and regulatory alignment. It enables providers to capture first-mover advantages and long-term contracts in untapped geographies. This trend aligns with global shifts in internet traffic flows and distributed computing.

Integrated Security Services Are Becoming Core Components of DCaaS Offerings

Enterprises now expect built-in data protection, firewall management, and compliance auditing in DCaaS contracts. Cybersecurity threats and evolving regulations require data centers to offer more than infrastructure. Providers embed secure access controls, threat monitoring, and compliance toolkits into their platforms. This shifts the perception of DCaaS from utility infrastructure to secure digital foundation. The Global Data Center-as-a-Service Market gains momentum by offering bundled protection that scales with usage. Enterprises trust providers that offer end-to-end accountability for uptime and security. This evolution supports market differentiation and higher-value service tiers.

Market Challenges

Legacy Infrastructure Integration and Data Migration Pose Transition Barriers for Enterprises

Enterprises with entrenched on-premises systems often struggle to migrate workloads seamlessly to DCaaS environments. Complex application stacks, licensing constraints, and data residency rules add friction during transition. Many organizations lack internal capabilities to manage hybrid integration at scale. DCaaS providers must build tools that ensure application portability and minimal downtime during migration. The Global Data Center-as-a-Service Market must also overcome stakeholder resistance to relinquishing physical control over data environments. It slows adoption in sectors where compliance and legacy systems dominate. Solutions that offer phased transition and workload mapping see better uptake in these cases.

High Competition and Low Differentiation Pressure Service Providers on Pricing and Profitability

The DCaaS landscape includes hyperscalers, regional providers, and telco-backed platforms offering similar services. Enterprises often compare vendors on cost rather than performance beyond SLAs. This commoditization pressures providers to lower margins and bundle more value-added features without proportional pricing power. It becomes difficult to sustain profitability while meeting uptime guarantees, security coverage, and customer support needs. Differentiating based on sustainability, security, and edge capabilities can help reposition offerings. However, vendors lacking scale or innovation pipelines may face consolidation pressures in the Global Data Center-as-a-Service Market.

Market Opportunities

Surge in AI and HPC Workloads Will Drive Demand for Specialized DCaaS Infrastructure

Enterprises deploying artificial intelligence, machine learning, and high-performance computing require infrastructure optimized for GPU clusters and parallel processing. Traditional cloud environments struggle to meet latency and bandwidth needs. The Global Data Center-as-a-Service Market has an opportunity to fill this gap by offering purpose-built, high-density environments with advanced cooling and connectivity. Providers that invest early in these capabilities can target fast-growing segments in life sciences, automotive, and finance.

Government Digitalization and Public Cloud Mandates Create New Procurement Channels

Several governments are mandating cloud adoption for citizen services and administrative systems. These policies create consistent demand pipelines for managed data center solutions with compliance certifications. DCaaS vendors offering sovereign cloud models can secure multi-year government contracts. It opens stable revenue streams and boosts provider credibility in the Global Data Center-as-a-Service Market. Providers must align offerings with national regulations and public sector digital frameworks to compete effectively.

Market Segmentation

By Service / Service Model

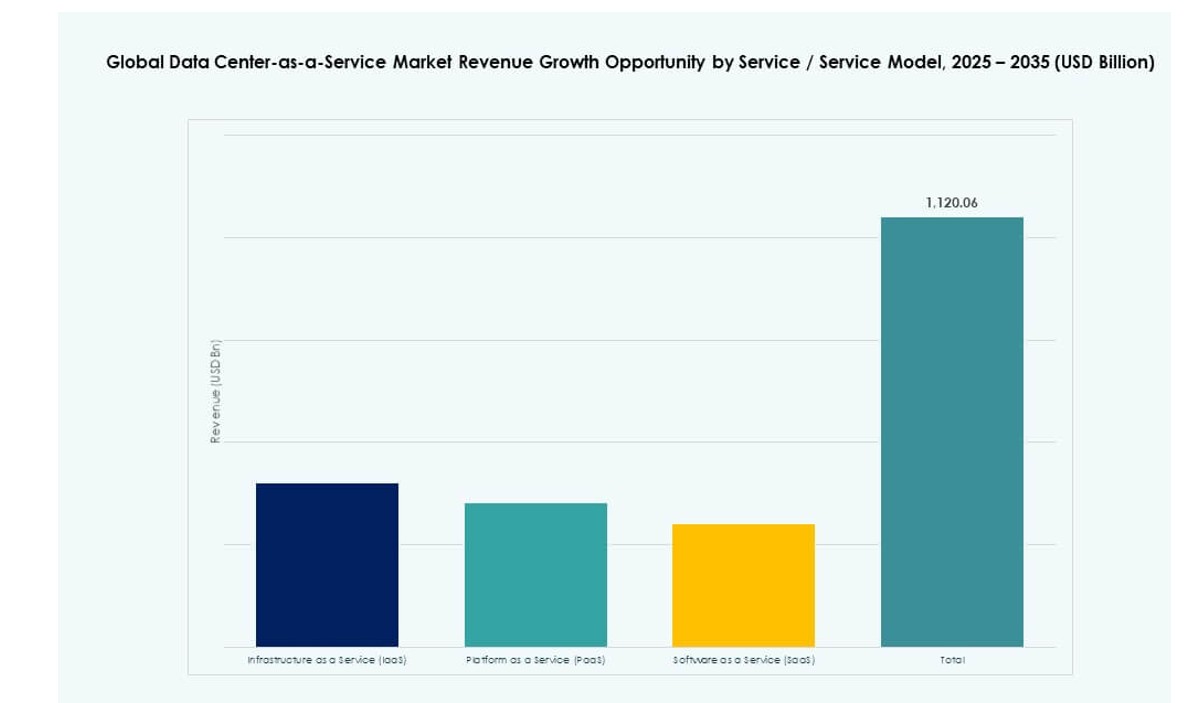

Infrastructure as a Service (IaaS) dominates the Global Data Center-as-a-Service Market, driven by its ability to deliver scalable compute, storage, and networking on-demand. Enterprises prefer IaaS for its flexibility, cost control, and ease of integration with existing IT systems. PaaS and SaaS are growing steadily, particularly in development and office productivity workloads, but IaaS remains the backbone for infrastructure outsourcing. Rapid cloud migration and digital transformation across verticals continue to push IaaS revenue upward.

By IaaS Sub-Segments

Among IaaS sub-segments, storage leads due to the explosion of enterprise data from cloud apps, video, AI, and IoT systems. Reliable and scalable storage is essential to cloud operations, making it a top priority in contract renewals. Networking and security services follow closely, driven by the need for secure, high-speed data transmission and compliance. Server provisioning continues to support workload agility and testing environments, but data storage remains the stickiest element in the service mix.

By Enterprise Size

Large enterprises account for the highest revenue share in the Global Data Center-as-a-Service Market, driven by high-volume IT workloads and demand for global uptime. These firms often seek hybrid deployments, leveraging both private and public infrastructure. SMEs are a fast-growing segment due to their need for flexible, affordable cloud-based infrastructure. Many SMEs adopt DCaaS to eliminate upfront costs, access managed services, and stay competitive against larger players. Vendor bundling strategies are helping improve SME adoption.

By Deployment Model

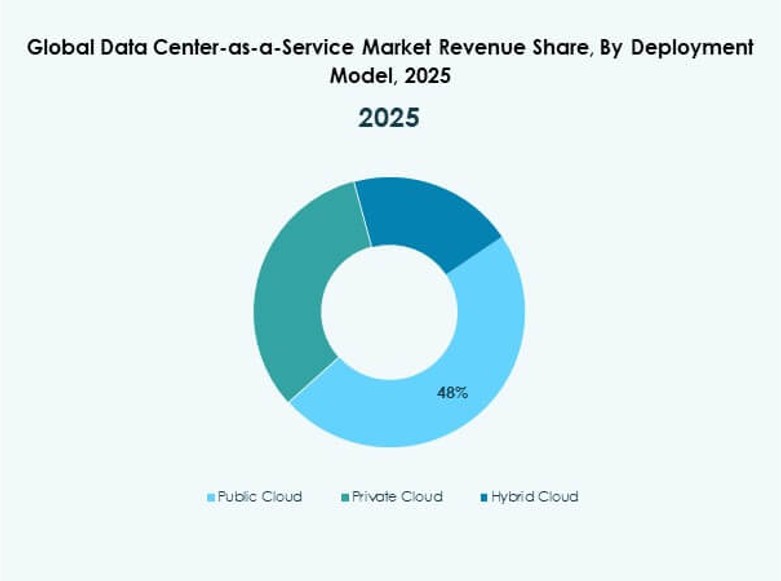

Hybrid cloud leads deployment preferences, combining the control of private clouds with the flexibility of public clouds. This model supports disaster recovery, regulatory compliance, and multi-region scalability. Public cloud remains strong in digital-native startups and tech platforms, while private cloud still finds demand in healthcare, finance, and sensitive data environments. The Global Data Center-as-a-Service Market is evolving toward hybrid models that offer best-of-both-worlds performance for mission-critical applications.

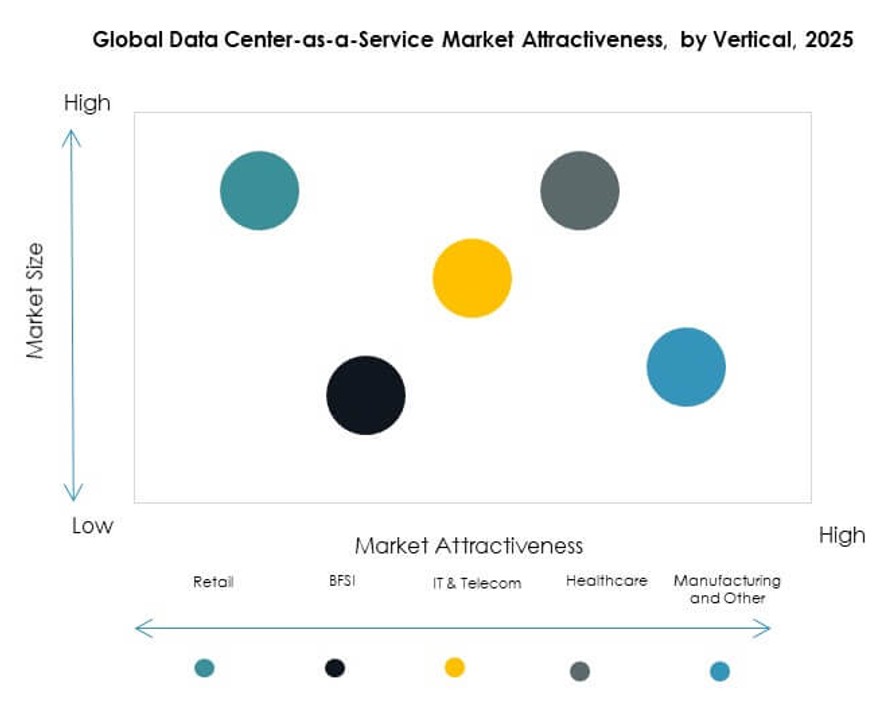

By Vertical (End-Use Industry)

IT & Telecom holds the dominant share due to continuous demand for low-latency infrastructure and API-integrated services. BFSI follows with its strong need for data security, compliance, and 24/7 operations. Healthcare and retail sectors are adopting DCaaS for EMR hosting and omnichannel operations respectively. Manufacturing shows steady demand tied to IoT and edge applications. The Global Data Center-as-a-Service Market also sees traction in education, government, and logistics within the ‘others’ segment.

Regional Insights

North America Leads Due to Cloud Maturity, Hyperscale Investments, and Strategic Vendor Presence

North America holds the largest share of the Global Data Center-as-a-Service Market at approximately 38%. The United States remains the anchor due to widespread enterprise cloud adoption and hyperscaler activity. It benefits from advanced IT infrastructure, aggressive digital transformation policies, and strong cloud vendor competition. Canada and Mexico contribute to regional strength with cross-border enterprise contracts and growing startup ecosystems. The region offers ideal conditions for hybrid and multi-cloud deployments.

- For instance, AWS US East (N. Virginia) supports 6 Availability Zones (us-east-1a to us-east-1f) with 99.999999999% (11 9’s) durability for Amazon S3 object storage across multi-petabyte workloads.

Europe Shows Strong Growth Backed by Regulatory Compliance and Sovereign Cloud Initiatives

Europe captures around 27% of the market, driven by GDPR-aligned infrastructure and increasing digital investments across the EU. Countries like Germany, France, and the UK lead demand, particularly in healthcare, finance, and public services. Local compliance and data sovereignty continue to influence DCaaS design. Western Europe dominates the region’s revenue share, but Eastern Europe is emerging with cross-border services and enterprise IT upgrades. The region promotes sustainable data centers, attracting ESG-conscious buyers.

Asia-Pacific Emerges as a High-Growth Region Supported by Digitalization, SMEs, and Startup Ecosystems

Asia-Pacific accounts for roughly 23% of the market and is the fastest-growing regional segment. China, India, and Southeast Asia are investing heavily in cloud infrastructure to support mobile-first economies and rapid digital inclusion. SMEs and startups drive large-scale adoption of managed infrastructure in cities beyond capital hubs. Japan and South Korea add enterprise-grade demand from technology and automotive sectors. The region favors flexible, modular DCaaS offerings with localized support.

- For instance, Alibaba Cloud’s Indonesia (Jakarta) region (ap-southeast-5) features 3 Availability Zones: ap-southeast-5a, ap-southeast-5b, and ap-southeast-5c. SMEs and startups drive large-scale adoption of managed infrastructure in cities beyond capital hubs.

Competitive Insights:

- IBM Corporation

- Microsoft

- Amazon Web Services (AWS)

- Hewlett Packard Enterprise (HPE)

- Dell Technologies

- Alibaba Cloud

- Oracle Cloud

- Tencent Cloud

- Equinix

- Digital Realty

The competitive landscape of the Global Data Center-as-a-Service Market is shaped by a mix of hyperscale cloud providers, regional players, and specialized colocation vendors. IBM, Microsoft, and AWS dominate enterprise cloud transformation projects with end-to-end service models. Alibaba, Tencent, and Oracle focus on platform scalability and regional compliance. Equinix and Digital Realty provide infrastructure and interconnectivity services for hybrid deployments. It remains highly competitive due to pricing pressure, rapid innovation, and rising demand for integrated services. Companies invest in AI optimization, green infrastructure, and edge capabilities to differentiate. Strategic partnerships, mergers, and expansion into Tier II cities define growth moves across providers. Large-scale players aim to lock clients with bundled offerings, while smaller firms focus on customization and service quality.

Recent Developments

- In January 2026, Digital Realty announced the acquisition of CSF Group, a Malaysian data center owner, including the TelcoHub 1 facility and adjacent land for up to 14 MW expansion. The deal integrates into PlatformDIGITAL, enhancing Southeast Asia presence with ServiceFabric for interconnection and orchestration.

- In September 2025, Equinix launched its first AI-ready International Business Exchange (IBX) data center, CN1, in Chennai, India, with a $69 million investment. This facility supports high-density AI workloads through liquid cooling and provides low-latency access to cloud ecosystems like AWS, Google Cloud, Microsoft Azure, and Oracle Cloud.

- In July 2025, Alibaba Cloud announced new partnerships and over $60 million in investments including with PingCAP for TiDB database on its marketplace and Atos for reselling cloud infrastructure.