Executive summary:

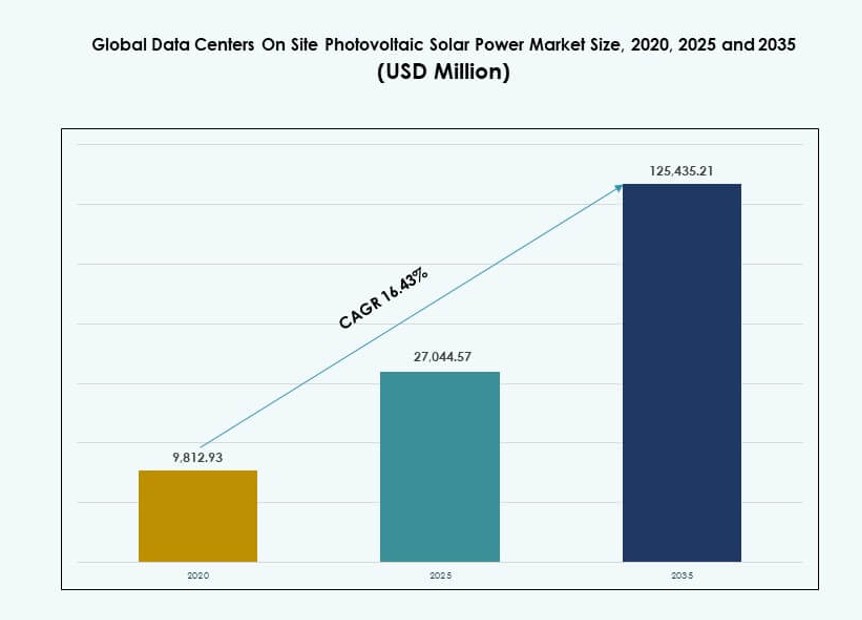

The Global Data Centers On Site Photovoltaic Solar Power Market size was valued at USD 9,812.93 million in 2020 to USD 27,044.57 million in 2025 and is anticipated to reach USD 125,435.21 million by 2035, at a CAGR of 16.43% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2035 |

| Data Centers On Site Photovoltaic Solar Power Market Size 2025 |

USD 27,044.57 Million |

| Data Centers On Site Photovoltaic Solar Power Market, CAGR |

16.43% |

| Data Centers On Site Photovoltaic Solar Power Market Size 2035 |

USD 125,435.21 Million |

Rising energy demands, grid instability, and carbon neutrality goals are driving investments in on-site photovoltaic systems. Data center operators are rapidly adopting solar power to gain energy independence, improve uptime, and align with ESG commitments. Innovations in high-efficiency panels, digital monitoring systems, and hybrid solar-plus-storage models make integration more attractive. Businesses view solar-powered infrastructure as a long-term hedge against rising energy costs, while investors favor assets that improve sustainability, reliability, and lifetime returns.

North America leads deployment due to early adoption by hyperscale operators and supportive renewable policies. Europe follows, driven by high power costs and climate legislation. Asia Pacific is emerging fast, led by rising digital infrastructure needs in China, India, and Southeast Asia. The Middle East is gaining momentum with landmark solar-data center projects, while Latin America and Africa show long-term potential due to improving solar economics and digital growth.

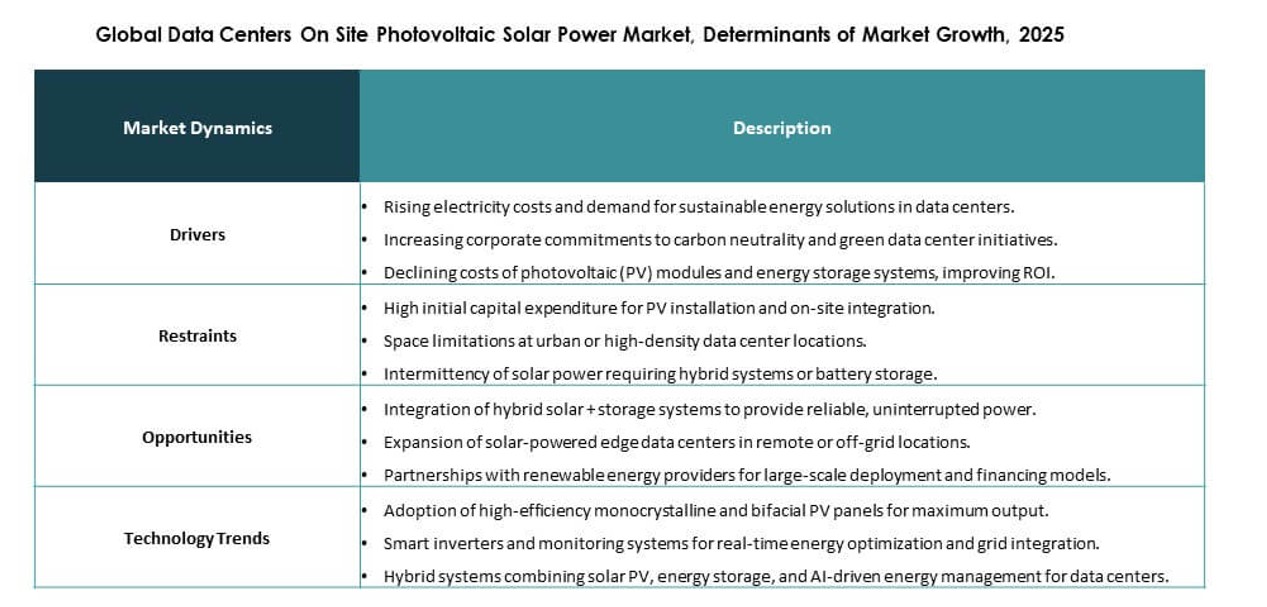

Market Dynamics:

Market Drivers

Rising Pressure to Reduce Energy Costs and Carbon Footprint Across Data Centers

Data center operators face sustained pressure to lower operating costs and meet climate targets. Energy expenses form a large share of total ownership cost. On‑site solar power supports predictable energy pricing over long periods. The Global Data Centers On Site Photovoltaic Solar Power Market gains importance due to this cost stability. Enterprises use solar to hedge against grid price swings. Sustainability reporting standards also shape procurement decisions. Corporate net‑zero goals push renewable integration at facility level. Investors value assets with lower long‑term energy risk. This driver strengthens long‑term deployment confidence.

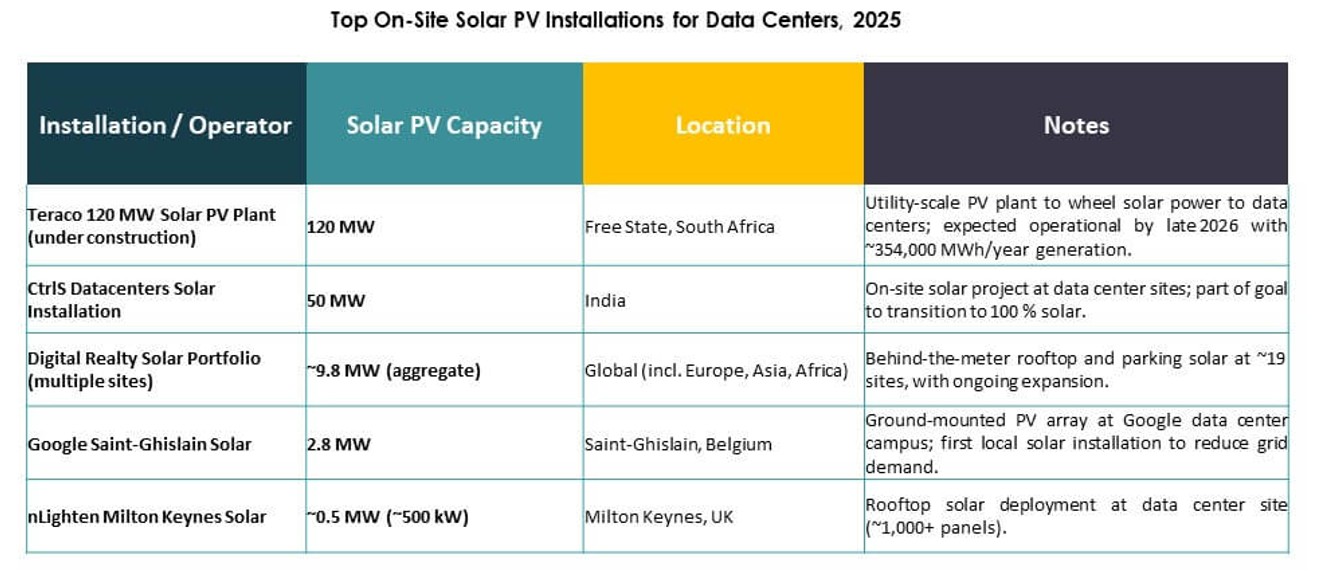

- For instance, CtrlS Datacenters commissioned its 125 MW GreenVolt solar plant in Nagpur to supply its Mumbai campus, covering over 60% of total load using N-type modules.

Growing Adoption of Hybrid Energy Architectures for Power Resilience

Data centers require uninterrupted power under all conditions. Hybrid systems that combine solar, storage, and grid supply improve resilience. Solar power supports daytime load coverage and grid relief. Battery integration strengthens backup capability during outages. The Global Data Centers On Site Photovoltaic Solar Power Market benefits from this architectural shift. Operators prioritize uptime and power quality over single‑source dependence. Energy autonomy becomes a strategic operational metric. This shift supports capital allocation toward integrated energy systems. Long‑term reliability attracts institutional investment.

Advancements in Solar Technology and Digital Energy Management Platforms

Panel efficiency improvements enhance output within limited site space. Smart inverters support stable power conversion under variable loads. Digital energy platforms allow real‑time optimization of solar output. The Global Data Centers On Site Photovoltaic Solar Power Market aligns with this digital control trend. Predictive analytics improve asset utilization and maintenance planning. Automation reduces manual intervention and energy loss. Technology maturity lowers perceived execution risk. Vendors align offerings with data center performance standards. Innovation strengthens commercial scalability.

- For instance, JinkoSolar upgraded 40% of its lines in 2025 to produce 40–50 GW of TOPCon modules reaching up to 24.8% efficiency, ideal for dense PV installations in hyperscale campuses.

Strategic Role of Renewable Assets in Data Center Valuation and Financing

Renewable integration influences asset valuation in capital markets. Financial institutions favor infrastructure with sustainable power profiles. Solar assets support green financing and lower borrowing costs. The Global Data Centers On Site Photovoltaic Solar Power Market supports long‑term asset attractiveness. Power independence improves risk assessment models. Investors view renewable‑powered sites as future‑ready assets. Long asset lifecycles align with solar payback periods. This driver reshapes infrastructure investment strategies. Market confidence continues to rise.

Market Trends

Expansion of On‑Site Solar in Hyperscale and Colocation Facility Design

Hyperscale operators embed solar at design stage. Colocation providers use solar to attract sustainability‑focused clients. Site planning integrates rooftop and ground‑mounted arrays. The Global Data Centers On Site Photovoltaic Solar Power Market reflects this design‑first approach. Power planning shifts from retrofit to native integration. Operators seek modular solar capacity growth. Long‑term power planning improves cost predictability. Client demand influences provider investment decisions. This trend reshapes facility development models.

Shift Toward Energy‑Aware Workload and Power Load Management

Energy‑aware scheduling gains attention across large data centers. Operators align workloads with solar output windows. Power management software supports this coordination. The Global Data Centers On Site Photovoltaic Solar Power Market supports flexible energy use strategies. Solar availability influences operational planning. This approach improves renewable utilization rates. It reduces reliance on grid peak pricing. Digital coordination strengthens system efficiency. Operational intelligence becomes a key differentiator.

Increased Focus on Space‑Efficient and High‑Output Solar Installations

Data center land constraints influence solar selection. High‑efficiency panels gain preference. Compact mounting systems support dense layouts. The Global Data Centers On Site Photovoltaic Solar Power Market reflects this efficiency focus. Operators maximize output per square meter. Engineering innovation supports structural integration. Space optimization improves project feasibility. Urban and edge sites benefit strongly. This trend supports premium technology adoption.

Growing Collaboration Between Data Center Operators and Solar OEMs

Strategic partnerships increase across the value chain. OEMs customize systems for data center loads. Operators seek long‑term performance guarantees. The Global Data Centers On Site Photovoltaic Solar Power Market benefits from joint solution development. Collaboration improves deployment speed. Standardization reduces integration complexity. Shared roadmaps support scale expansion. Vendor relationships influence procurement strategy. Partnership‑driven execution gains momentum.

Market Challenges

High Initial Capital Requirement and Long Payback Expectations

On‑site solar projects require notable upfront investment. Capital approval remains complex for cost‑sensitive operators. Payback timelines depend on energy pricing assumptions. The Global Data Centers On Site Photovoltaic Solar Power Market faces financing scrutiny. Smaller operators face budget limitations. Project economics vary by geography. Financial uncertainty delays adoption decisions. Risk perception affects investment pacing. Capital intensity remains a key barrier.

Operational Complexity and Grid Integration Constraints

Solar integration adds technical complexity to data center operations. Grid interconnection rules vary by region. Power quality management requires advanced controls. The Global Data Centers On Site Photovoltaic Solar Power Market must address these constraints. Skilled workforce availability limits execution speed. Regulatory approval cycles extend timelines. Maintenance coordination adds operational burden. Integration risk concerns conservative operators. Complexity slows uniform adoption.

Market Opportunities

Rising Demand for Renewable‑Powered Digital Infrastructure from Enterprise Clients

Enterprise customers prefer sustainable data hosting partners. Renewable power improves brand alignment. Solar adoption strengthens service differentiation. The Global Data Centers On Site Photovoltaic Solar Power Market benefits from client‑driven demand. Green credentials influence contract decisions. Long‑term service agreements support investment recovery. Sustainability audits shape vendor selection. This opportunity supports premium pricing models.

Untapped Potential Across Emerging Markets and Edge Data Centers

Emerging economies expand digital infrastructure rapidly. Grid reliability challenges support on‑site solar use. Edge data centers require local power autonomy. The Global Data Centers On Site Photovoltaic Solar Power Market aligns with this need. Modular solar fits distributed deployments. Government renewable targets support adoption. Infrastructure gaps create deployment space. This opportunity expands addressable demand.

Market Segmentation

By Component

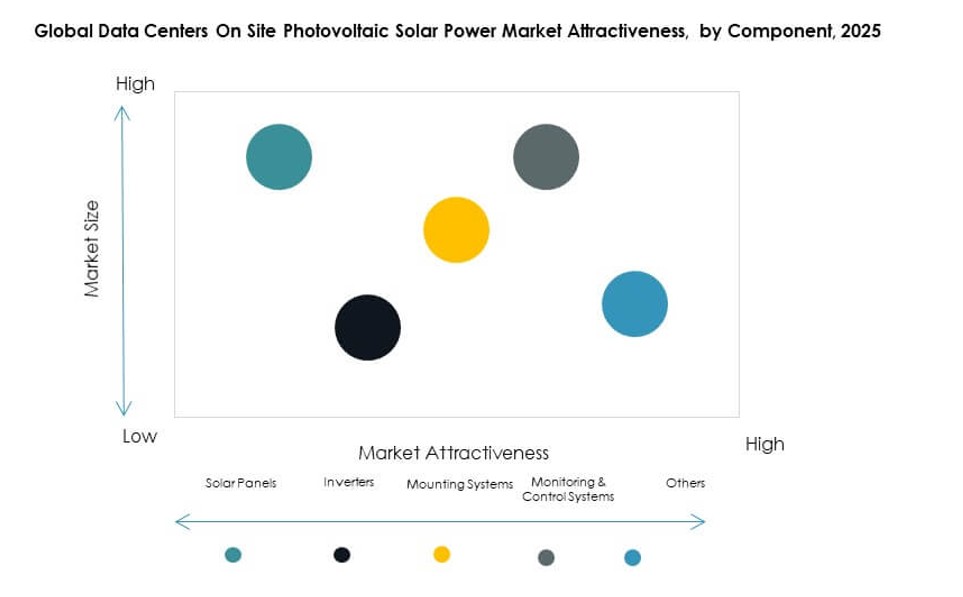

Solar panels dominate due to direct energy generation role and falling unit costs. High‑efficiency modules gain strong preference in data center environments. Inverters support stable power conversion under variable loads. Mounting systems enable space‑efficient deployment. Monitoring and control systems improve performance visibility and uptime. The Global Data Centers On Site Photovoltaic Solar Power Market benefits from integrated component solutions. Panels account for the largest share due to scale requirements. Innovation across balance‑of‑system components supports long‑term reliability.

By Application

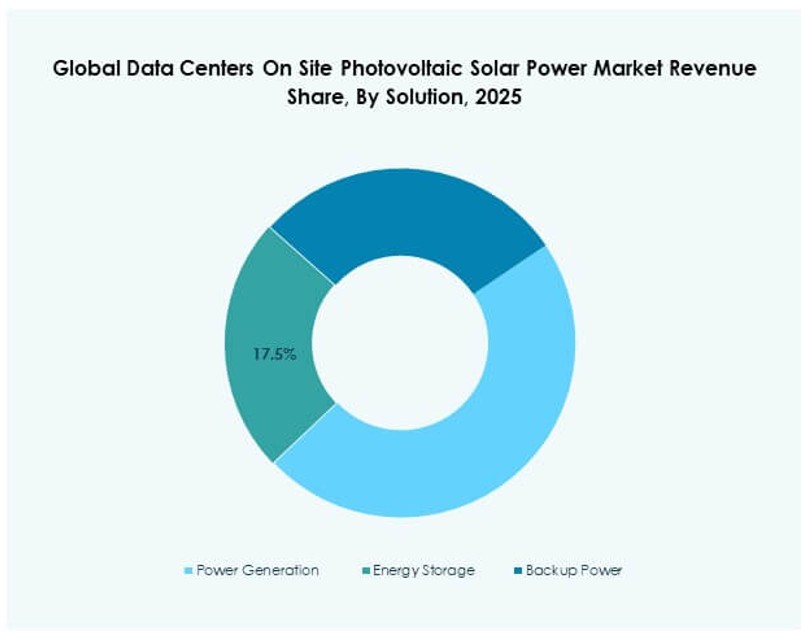

Power generation remains the leading application since operators aim to offset primary grid consumption. Energy storage gains traction where reliability and load balancing matter. Backup power applications support resilience strategies. The Global Data Centers On Site Photovoltaic Solar Power Market sees strongest adoption in primary power support. Storage integration improves solar utilization. Backup use remains secondary but strategic. Application choice depends on site size and grid quality. Power generation continues to dominate overall demand.

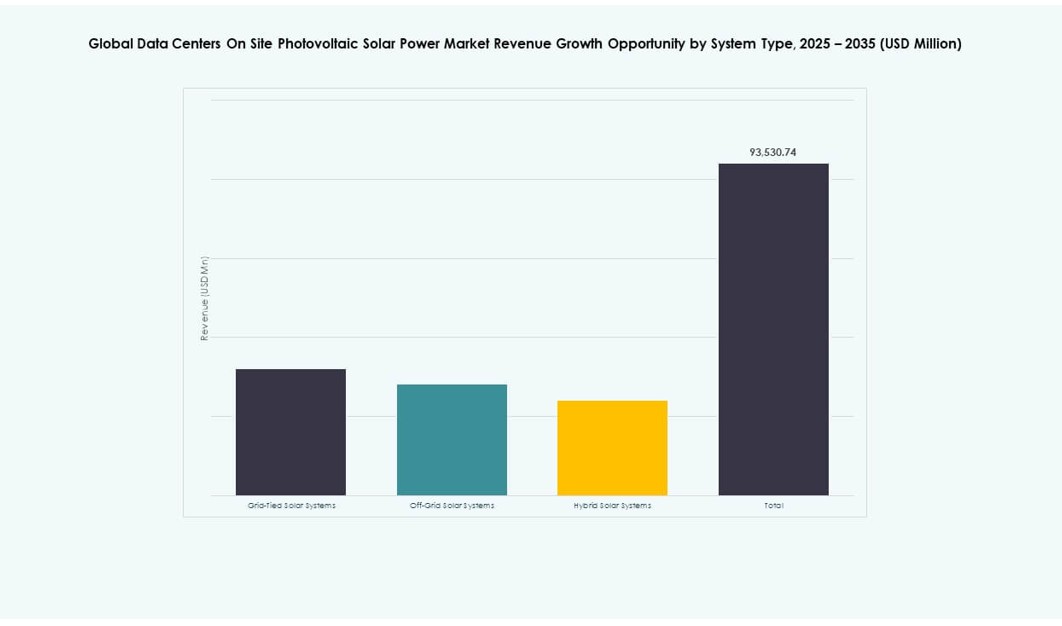

By System Type

Grid‑tied systems hold the largest share due to cost efficiency and grid support. Hybrid systems show faster growth due to resilience benefits. Off‑grid systems remain niche for remote locations. The Global Data Centers On Site Photovoltaic Solar Power Market favors hybrid architectures in new builds. Grid‑tied systems reduce upfront costs. Hybrid models improve uptime assurance. System choice reflects reliability goals. Hybrid adoption accelerates steadily.

By Data Center Type

Hyperscale data centers dominate due to large energy demand and scale economics. Colocation facilities follow with strong client‑driven sustainability needs. Enterprise sites adopt selectively based on budget. Edge data centers show rising interest due to power autonomy needs. The Global Data Centers On Site Photovoltaic Solar Power Market aligns closely with hyperscale expansion. Scale supports solar feasibility. Colocation adoption grows steadily. Edge deployment creates new demand pockets.

By Technology

Monocrystalline panels lead due to high efficiency and space optimization. Polycrystalline panels serve cost‑sensitive installations. Thin‑film PV finds use in specific structural applications. The Global Data Centers On Site Photovoltaic Solar Power Market favors monocrystalline technology for performance reasons. Efficiency supports higher output density. Technology choice reflects land constraints. Durability influences lifecycle cost. Monocrystalline panels remain dominant.

Regional Insights

North America and Europe

North America leads with about 38% market share due to hyperscale concentration and renewable policies. The United States drives early adoption through corporate sustainability goals. Canada supports growth with clean energy incentives. Europe holds nearly 27% share due to strict climate regulations. Germany, France, and the UK lead regional deployment. Power price volatility supports solar adoption. The Global Data Centers On Site Photovoltaic Solar Power Market remains strong across these regions.

- For instance, Microsoft achieved 96% global renewable energy coverage in 2023, supported by large-scale solar PPAs in Virginia and Texas, where it operates high-density data center regions aligned with its 100/100/0 zero-carbon energy commitment.

Asia Pacific

Asia Pacific accounts for around 25% share with rapid data center expansion. China leads due to large‑scale digital infrastructure investment. India shows strong growth due to renewable targets. Japan and South Korea focus on energy security. The Global Data Centers On Site Photovoltaic Solar Power Market benefits from new build activity. Power demand growth supports solar integration. Government support accelerates adoption.

Middle East, Latin America, and Africa

These regions together hold about 10% share but show rising potential. The Middle East adopts solar to manage energy intensity. Latin America benefits from high solar irradiance. Africa explores solar for grid stability. The Global Data Centers On Site Photovoltaic Solar Power Market sees gradual uptake. Policy frameworks improve project feasibility. Early investments signal long‑term growth. Emerging regions expand future opportunities.

- For instance, DEWA launched the second phase of its green data center in Dubai in January 2026, powered by solar from the Mohammed bin Rashid Al Maktoum Solar Park, enhancing digital and grid services through on-site renewable energy.

Competitive Insights:

- Trina Solar

- JA Solar Co., Ltd.

- SunPower Corporation

- First Solar, Inc.

- JinkoSolar

- Canadian Solar

- Yingli Solar

- Hanwha Q CELLS

- Vikram Solar Pvt. Ltd.

- SCHOTT North America, Inc.

The Global Data Centers On Site Photovoltaic Solar Power Market features a competitive landscape shaped by a mix of established solar manufacturers and regionally focused suppliers. It includes global players who dominate through high-efficiency panels, turnkey EPC services, and strong partnerships with data center operators. Companies like Trina Solar, JinkoSolar, and SunPower compete on technology performance, bankability, and large-scale deployment capabilities. Players also differentiate through integrated solutions, offering not just modules but also inverters, storage, and energy monitoring platforms. Market activity includes mergers, R&D investment, and regional expansion into high-growth areas. Competitive intensity is rising as operators demand customized systems that align with digital infrastructure standards. Strategic alignment with hyperscale and colocation clients remains central to maintaining leadership in this market.

Recent Developments:

- In January 2026, Dubai Electricity and Water Authority (DEWA) approved the second phase of its solar-powered green data center at Warsan, primarily powered by on-site renewable energy from the Mohammed bin Rashid Al Maktoum Solar Park. This expansion boosts capacity, resilience, and efficiency for digital services and smart grid operations.

- In February 2025, CtrlS Datacenters completed its 125MW GreenVolt 1 on-site solar farm in Nagpur, Maharashtra, to power its Mumbai data center campus. The project, built in two phases with the first 65.2MW live in June 2024, uses efficient N-type solar panels and covers 60% of the campus’s energy needs.