Executive summary:

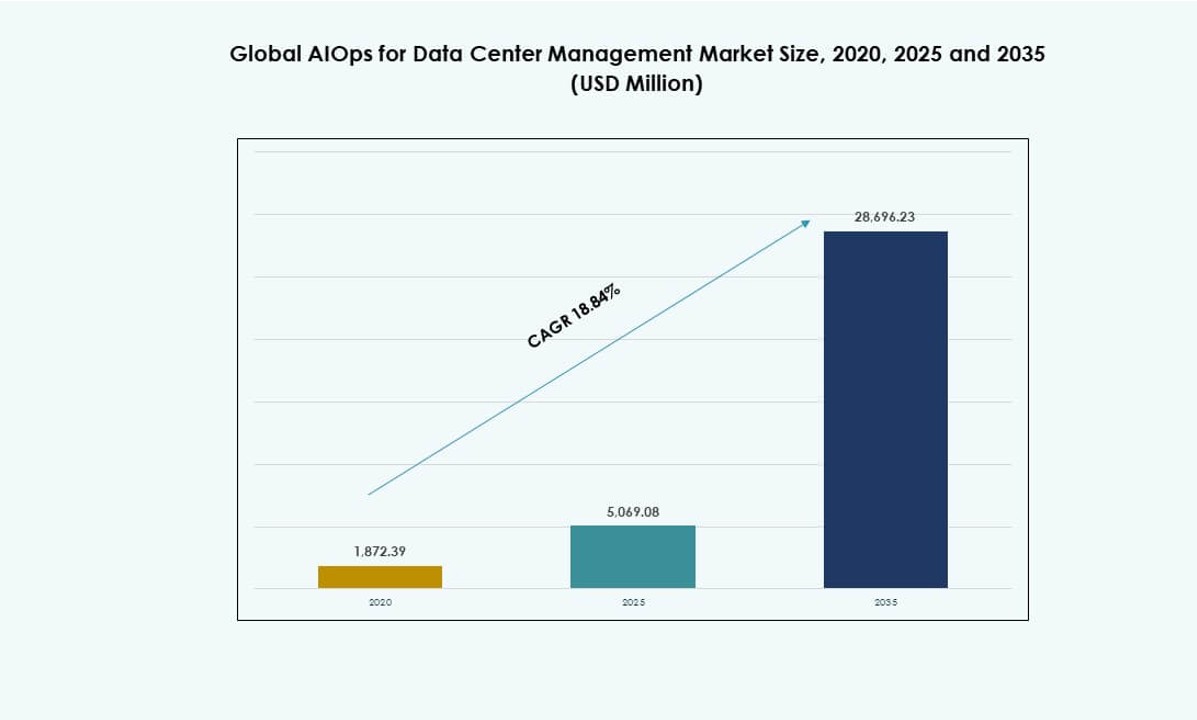

The Global AIOps for Data Center Management Market size was valued at USD 1,872.39 million in 2020 to USD 5,069.08 million in 2025 and is anticipated to reach USD 28,696.23 million by 2035, at a CAGR of 18.84% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2035 |

| AIOps for Data Center Management Market Size 2025 |

USD 5,069.08 Million |

| AIOps for Data Center Management Market, CAGR |

18.84% |

| AIOps for Data Center Management Market Size 2035 |

USD 28,696.23 Million |

Enterprises adopt AIOps to manage complex hybrid data centers and reduce alert noise that strains operations teams. Vendors advance correlation, topology mapping, and explainable automation to improve incident response and prevent outages. Cloud and AI infrastructure builds increase telemetry volumes and speed change cycles, which raises demand for policy-driven control. It supports uptime discipline, better capacity planning, and lower operational risk. Investors value recurring subscriptions, platform consolidation, and strong expansion potential across adjacent ops use cases.

North America leads due to hyperscale capacity, mature SRE practices, and broad enterprise adoption across regulated industries. Europe follows with strong governance needs and compliance-led operational standards that favor auditable automation. Asia Pacific emerges fast as cloud expansion and new data center builds raise complexity across distributed sites. Latin America, the Middle East, and Africa show steady uptake through colocation growth and managed service models where talent gaps persist. Partner ecosystems and cloud adoption pace shape regional momentum.

Market Dynamics:

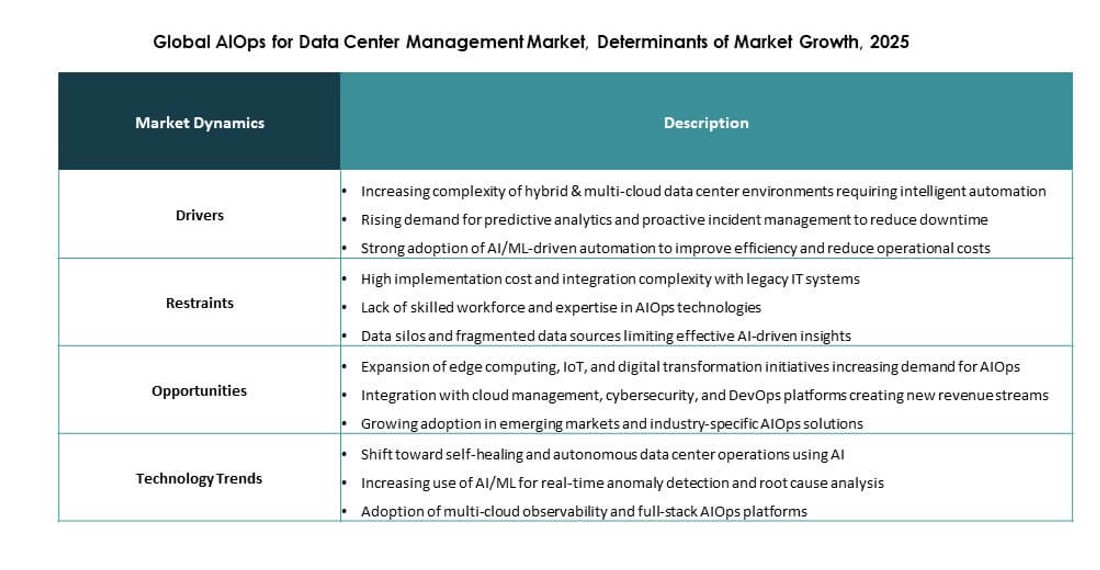

Market Drivers

Escalating Data Center Complexity And Uptime Accountability

Enterprises expand hybrid estates, edge nodes, and multi-tenant footprints across critical workloads. This scale raises alert volumes and weakens manual triage. The Global AIOps for Data Center Management Market benefits from demand for faster root-cause isolation. Operators push for higher availability targets with clear audit trails. Boards treat downtime as a revenue and reputation risk, not only an IT issue. AIOps platforms cut mean time to detect and mean time to resolve through correlated signals. Teams also seek predictable operations that protect SLA commitments. Vendors position it as a core control layer for resilient services. Investors favor providers that prove measurable reliability outcomes and strong renewal rates.

Rapid AI Adoption For Predictive Operations And Capacity Discipline

CIOs prioritize predictive operations to prevent incidents before they affect customers. This driver strengthens budgets for telemetry, models, and closed-loop remediation. The Global AIOps for Data Center Management Market gains from enterprise AI road maps that demand trusted monitoring. Data center leaders require better capacity forecasts to avoid overbuild and waste. AIOps supports proactive patch planning, performance baselines, and anomaly detection. It also helps engineers tune policies with fewer false positives. Procurement teams prefer tools that reduce tool sprawl and consolidate dashboards. This shift raises strategic value for platform vendors and system integrators. Private equity and corporates pursue assets with recurring software revenue and clear expansion paths.

- For instance, DriveNets reported that its AIOps root-cause analysis demo reduced the total time spent identifying, diagnosing, and mitigating incidents by 87%, and it also cited Telia’s TM Forum Catalyst work showing automated incident correlation and root-cause analysis can accelerate problem detection and diagnosis by up to 90% and improve MTTR by 37% on average.

Shift Toward Software-Defined Infrastructure And Automated Control Planes

Data centers adopt software-defined compute, storage, and network to improve agility. This change increases configuration churn and policy complexity across domains. The Global AIOps for Data Center Management Market grows when enterprises need cross-domain correlation. AIOps tools map dependencies across virtual layers and physical assets. They enable safer automation through guardrails, approvals, and rollback logic. This reduces human error during change windows and incident response. Leaders treat standardized runbooks as a competitive operating advantage. Cloud operators and colocation providers also require consistent service quality. That requirement supports investment in mature orchestration features and partner ecosystems.

Security, Compliance, And Risk Governance Demand Faster Insight

Regulators and customers demand stronger controls over data, access, and continuity. Security teams need faster detection of anomalous behavior in infrastructure signals. The Global AIOps for Data Center Management Market advances when firms unify observability with compliance reporting. AIOps supports policy enforcement and evidence capture for audits. It can flag drift in configurations that create exposure. Enterprises also require separation of duties and traceable remediation actions. This pushes buyers toward platforms with robust governance and role controls. Insurers and risk committees favor tools that document operational discipline. It strengthens vendor differentiation in regulated verticals and supports higher contract values.

- For instance, AWS reported that its automated remediation program for Volkswagen operated across 1,200 AWS accounts, deployed more than 15 remediation modules, completed over 100,000 remediations in its first year, improved fixed critical vulnerability rates from 95% to 99.9%, and raised high-severity remediation rates from 85% to 98%, demonstrating strong numerical progress in governance and risk control.

Market Trends

Rise Of Model-Driven Incident Prioritization With Business Context

Enterprises shift from alert counts to impact-ranked incidents tied to services. They map telemetry to customer journeys, revenue flows, and contractual SLAs. The Global AIOps for Data Center Management Market reflects demand for smarter prioritization over raw detection. Platforms embed service topology and dependency graphs to score blast radius. Teams route tickets based on skills, ownership, and confidence scores. This approach reduces noise and improves on-call experience. Buyers ask for explainable outputs that help prove decision quality. Vendors respond with transparent reason codes and audit-friendly logs. This trend favors products that integrate with ITSM and CMDB stacks without heavy customization.

Convergence Of Observability, ITSM, And FinOps Into Unified Operations

Enterprises reduce overlapping tools across monitoring, tickets, and cost controls. They expect a single operational view that spans performance, incidents, and spend. The Global AIOps for Data Center Management Market tracks this convergence through broader platform bundles. Vendors align metrics with cost signals such as power, cooling, and utilization. Ops teams use common dashboards to coordinate SRE, network, and facilities. This improves accountability and shortens handoffs across functions. Procurement favors suites that simplify contracts and vendor management. Partners build packaged integrations to speed deployment. The trend increases cross-sell potential for vendors and lifts customer lifetime value.

Expansion Of Edge And Distributed Data Centers With Lightweight AIOps

Edge growth creates many small sites with limited local staff and strict latency targets. Operators need centralized control without heavy on-site tooling. The Global AIOps for Data Center Management Market adapts through lighter agents and remote policy control. Vendors deliver modular deployments with selective data collection. Teams emphasize bandwidth discipline and local autonomy for critical actions. This drives demand for robust automation with safe constraints. Channel partners package edge operations for retail, telecom, and industrial users. Buyers also seek rapid rollouts with standardized templates. This trend opens new midmarket and vertical-specific deals and expands addressable site counts.

Greater Focus On Data Quality, Telemetry Governance, And Benchmarking

Enterprises treat telemetry as an asset that needs standards and stewardship. They define common naming, tagging, and retention policies across teams. The Global AIOps for Data Center Management Market benefits from buyers who demand clean inputs for reliable outputs. Organizations adopt benchmarks for MTTR, change failure rate, and incident recurrence. They compare sites and vendors with consistent KPIs. This pushes platforms to offer strong data pipelines and validation. Buyers request automated health checks for collectors and integrations. Vendors add scorecards and maturity assessments to guide adoption. The trend increases services pull-through for consulting and supports premium enterprise tiers.

Market Challenges

Fragmented Tooling, Siloed Data, And Integration Friction

Enterprises run many monitoring tools across apps, networks, storage, and facilities. This fragmentation blocks a unified view of dependencies and incident chains. The Global AIOps for Data Center Management Market faces long integration cycles in complex estates. Teams struggle with inconsistent tags, duplicate events, and missing context. Legacy systems also limit API access and slow connector development. Change control processes delay rollout of new collectors and agents. Buyers demand quick value, yet foundational work consumes early timelines. Vendors must prove interoperability across diverse stacks and versions. This challenge raises implementation risk for customers and can slow purchase decisions.

Trust, Governance, And Talent Gaps That Limit Automation Scale

Leaders hesitate to allow automated actions that can affect critical services. They require explainable outputs and clear accountability for model decisions. The Global AIOps for Data Center Management Market must address concerns over false positives and unsafe remediation. Security teams insist on strict access controls and audit trails for every action. Data privacy rules restrict telemetry sharing across regions and tenants. Skills gaps in SRE, data engineering, and model oversight limit adoption depth. Organizations also face cultural resistance from teams that prefer manual control. Vendors and integrators must offer strong guardrails and training. These factors can delay expansion from monitoring to remediation and can cap realized ROI.

Market Opportunities

Industry-Specific Packages For Regulated And High-Availability Workloads

Vendors can build preconfigured playbooks for BFSI, healthcare, and telecom operations. These packages shorten deployment time and reduce integration effort. The Global AIOps for Data Center Management Market can expand via compliance-ready reporting and controls. Buyers pay for proven templates that map to audits and SLA needs. Partners can deliver vertical accelerators with clear KPIs and runbooks. This supports higher margins through differentiated offerings. Enterprises also value predictable outcomes and standardized governance. It creates repeatable deployments across many sites. This opportunity supports faster sales cycles and stronger renewals.

Managed AIOps Services And Outcome-Based Contracts For Midmarket Buyers

Many firms lack staff to operate advanced platforms at scale. Service providers can run it as a managed layer with clear SLAs. The Global AIOps for Data Center Management Market can grow through outcome-based pricing tied to MTTR and uptime. This model aligns vendor incentives with customer value. MSPs can bundle observability, ITSM integration, and automation governance. Midmarket customers gain enterprise-grade operations without large teams. Vendors gain recurring revenue and broader reach through channels. Investors favor stable cash flows and expansion potential. This opportunity increases adoption beyond large enterprises and improves market penetration.

Market Segmentation

By Component

In the Global AIOps for Data Center Management Market, platforms hold the dominant share at about 62% due to demand for unified correlation, topology, and automation control. Enterprises favor a core platform that connects monitoring tools, ITSM, and asset records. Buyers select platforms to reduce tool sprawl and create a single operational view across hybrid estates. Providers differentiate through explainable insights and policy control that support controlled remediation. Platform road maps now stress guardrails, auditability, and workflow alignment with service ownership. This supports premium enterprise subscriptions and multi-year contracts. It also strengthens vendor stickiness through expansion into adjacent operational use cases.

By Application

In the Global AIOps for Data Center Management Market, performance monitoring leads at roughly 24% because uptime and latency directly affect revenue and user trust. Organizations rely on it to maintain service quality across cloud, network, and infrastructure layers. Teams prioritize early anomaly detection, baseline management, and KPI alignment to business services. Vendors invest in workflow automation that ties alerts to tickets and enforces ownership. Enterprises also demand explainable prioritization so teams act with confidence during incidents. Strong performance monitoring outcomes support expansion into incident, infrastructure, and security use cases. This strengthens adoption across large estates with complex dependency chains.

By End-user

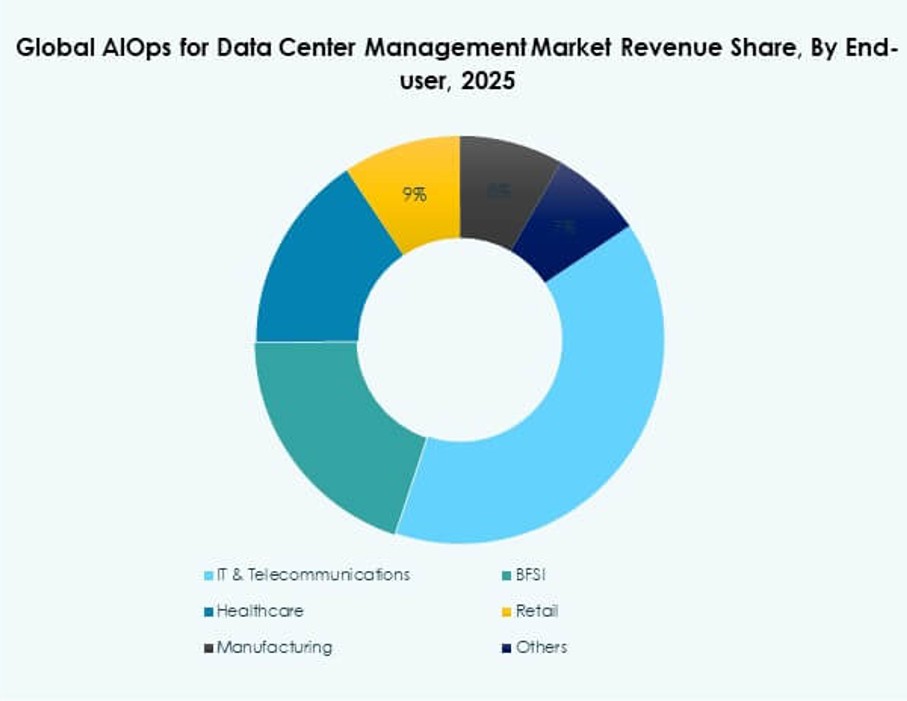

In the Global AIOps for Data Center Management Market, IT and telecommunications leads at about 32% since operators manage large distributed networks and strict SLAs. These buyers require rapid fault isolation across network fabrics, compute, and application layers. They also manage high event volumes that overwhelm manual triage and on-call teams. AIOps helps enforce consistent incident workflows across NOCs and SRE functions. Buyers also demand role controls, audit logs, and clear escalation paths. Service providers often prioritize multi-tenant capabilities and standardized runbooks to reduce operational variance. This segment supports high contract values due to scale and criticality of uptime. It also drives product road maps toward stronger correlation and topology capabilities.

By Enterprise Size

In the Global AIOps for Data Center Management Market, large enterprises dominate near 68% because they run complex hybrid footprints and can fund platform consolidation. They face higher downtime exposure and stricter governance requirements across many teams and sites. Buyers often run pilots in high-impact services, then expand across domains and geographies. Vendors win scale deals through integration depth, enterprise-grade security, and strong professional services. This dynamic supports tiered packaging and platform expansion across adjacent IT operations. It also increases renewal strength when deployments become operationally embedded.

By Deployment Mode

In the Global AIOps for Data Center Management Market, cloud-based deployment leads at about 57% due to scalability, faster updates, and easier integration with SaaS ITSM tools. Buyers prefer quicker time to value and lower infrastructure overhead for the management layer. Cloud deployment also supports centralized visibility across distributed sites and hybrid environments. On-premises remains important for regulated and latency-sensitive environments, but buyers still seek modern user experiences and rapid feature access. Vendors respond with flexible architectures, data routing controls, and deployment templates. This keeps both modes relevant while cloud adoption continues to expand. It also supports recurring subscription growth through continuous feature delivery.

By Offering Type

In the Global AIOps for Data Center Management Market, platform-based AIOps leads at about 40% as buyers seek broad coverage across domains and vendors. Enterprises favor a unified layer that correlates signals across tools rather than isolated point solutions. Buyers also value policy control and consistent runbooks that enable controlled automation. Vendors compete on integration depth, topology intelligence, explainable insights, and ITSM alignment. Strong partner ecosystems accelerate deployment through packaged connectors and industry playbooks. Competitive pressure drives consolidation among vendors that can prove measurable MTTR and availability gains. This segment benefits from enterprise preference for suite buying and long-term platform road maps.

Regional Insights

North America And Europe Set The Pace Through Scale And Governance

North America held 38.55% share in 2025, supported by hyperscale capacity, mature SRE practices, and strong enterprise spend on automation. Enterprises prioritize uptime discipline, policy control, and faster incident closure to protect revenue and SLAs. Buyers also expect deep integration with ITSM, observability, and security stacks to reduce tool sprawl. Organizations favor explainable alerts, audit-ready workflows, and controlled remediation to meet governance standards. The Global AIOps for Data Center Management Market benefits in these regions from platform consolidation, multi-year contracts, and expansion into cross-domain operations.

- For instance, Volkswagen’s Digital Production Platform on AWS deployed more than 15 remediation modules across 1,200 AWS accounts, executed over 100,000 remediations in its first year, and improved fixed critical vulnerability rates from 95% to 99.9% while lifting high-severity remediation rates from 85% to 98%, demonstrating the kind of audit-ready automation and governance discipline buyers in Europe increasingly value.

Asia Pacific Gains Momentum With New Capacity And Distributed Operations

Asia Pacific accounted for 23.86% share in 2025 as operators expand cloud capacity and deploy more distributed data center footprints. Regional buyers invest in automation to manage high alert volumes with lean operations teams. They prioritize rapid onboarding, standardized runbooks, and policy-based controls that work across many sites. Telecom, digital commerce, and financial services push demand for low-latency performance and consistent service reliability. Vendors compete on integration breadth, multilingual support, and partner-led deployment models. The Global AIOps for Data Center Management Market grows here through new builds, hybrid estates, and rising requirements for predictive operations and capacity discipline.

- For instance, Taiwan-based Gogolook migrated a database containing 2.6 billion entries in 4 months on AWS, reduced database TCO by 40%, and achieved 16% time savings through generative AI-powered multilingual call labeling, highlighting how Asia Pacific operators are pairing scale-out infrastructure with automation-led operational discipline.

Latin America, Middle East, And Africa Expand Through Modernization And Managed Delivery

Latin America represented 4.96% share in 2025, with growth tied to cloud adoption, colocation expansion, and stronger service reliability targets. The Middle East held 2.61% share in 2025 as governments and enterprises invest in digital infrastructure, resilient data centers, and secure operations frameworks. Africa reached 2.00% share in 2025, where buyers focus on cost control, stable uptime, and simplified operations across fewer skilled resources. Many organizations prefer managed services and packaged deployments that reduce integration effort and speed time to value. Vendors that offer strong governance, clear ROI metrics, and lightweight deployment options win more deals. The Global AIOps for Data Center Management Market advances in these regions through partner ecosystems, outcome-based offers, and gradual migration from manual monitoring to automated remediation.

Competitive Insights:

- IBM Corporation

- Cisco Systems, Inc.

- Splunk Inc.

- Broadcom Inc.

- BMC Software

- Dynatrace

- Datadog, Inc.

- New Relic, Inc.

- ScienceLogic

- LogicMonitor

Competition centers on platform depth, domain coverage, and proven ROI in incident reduction and service uptime. The Global AIOps for Data Center Management Market features large incumbents that bundle AIOps with broader infrastructure, security, and IT service management portfolios, which supports enterprise-wide deals. Pure-play observability vendors compete through faster deployment, stronger telemetry analytics, and product-led adoption that scales from teams to large accounts. Buyers favor vendors with rich integrations across cloud, network, and facility tools, plus mature ITSM connectors and governance controls. Partnerships with hyperscalers, MSPs, and system integrators influence deal velocity and expansion. Vendors also compete on explainable insights, automation guardrails, and pricing models that align with usage and outcomes.

Recent Developments:

- In June 2025, Cisco announced that it was launching new AI-ready data center innovations and expanding partnerships with NVIDIA and new neocloud providers. The company said these updates were designed to simplify, secure, and future-proof data centers so enterprises and service providers could scale AI infrastructure more effectively.

- In June 2025, Schneider Electric announced a strategic collaboration with NVIDIA to develop scalable, sustainable AI-ready power, cooling, and control systems for data center infrastructure across Europe. Schneider also said the partnership included new NVIDIA-enabled EcoStruxure rack and pod solutions intended to speed deployment and improve energy-efficient data center operations.

- In December 2025, HPE announced an expanded partnership with NVIDIA that added new secure and scalable AI factory solutions, a new AI datacenter interconnect, and the first AI Factory Lab in the EU in Grenoble, France. HPE also stated that new Datacenter Ops Agents from World Wide Technology, NVIDIA, and HPE were introduced to simplify AI data center management across agentic AI and hybrid cloud environments.