Executive Summary:

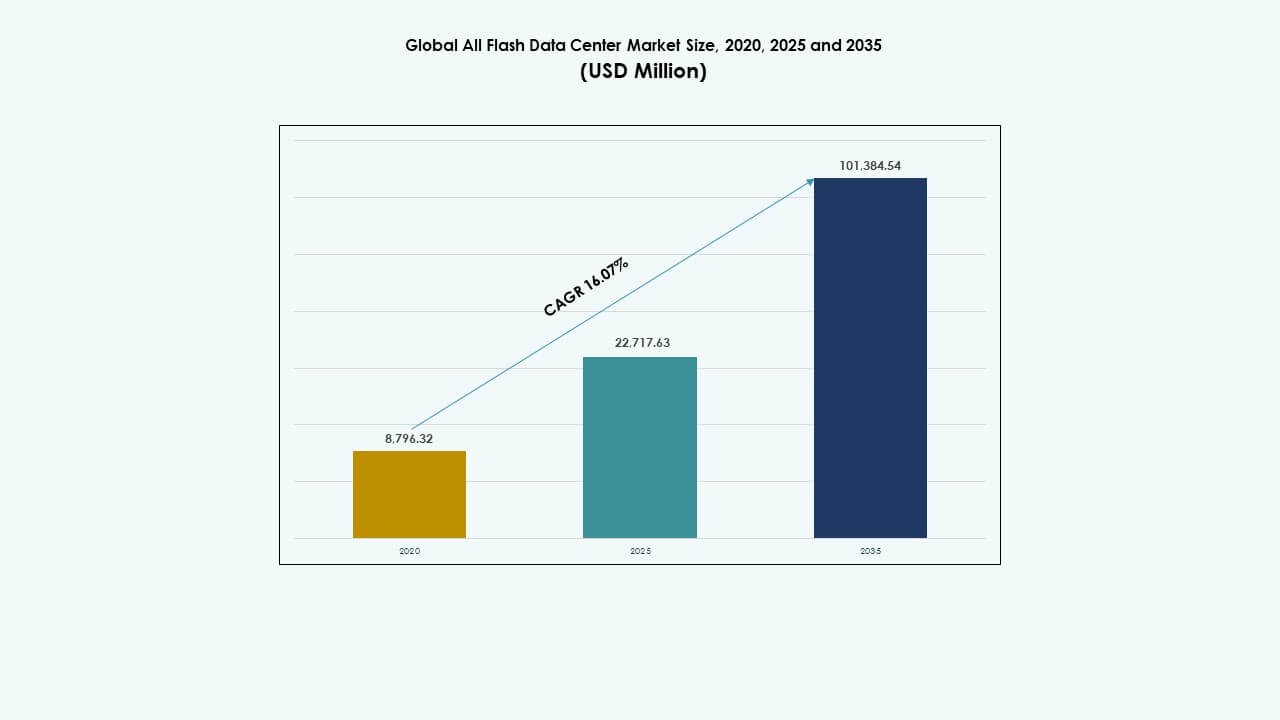

The Global All Flash Data Center Market size was valued at USD 8,796.32 million in 2020, grew to USD 22,717.63 million in 2025, and is anticipated to reach USD 101,384.54 million by 2035, at a CAGR of 16.07% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2035 |

| All Flash Data Center Market Size 2025 |

USD 22,717.63 Million |

| All Flash Data Center Market, CAGR |

16.07% |

| All Flash Data Center Market Size 2035 |

USD 101,384.54 Million |

Enterprises are embracing all-flash infrastructure to handle high-performance workloads with reduced latency, improved energy efficiency, and scalable storage capacity. Rapid growth in AI, analytics, and cloud-native applications demands storage solutions that deliver consistent throughput and speed. Innovation in NVMe, software-defined storage, and HCI platforms is reshaping data center strategies. The Global All Flash Data Center Market supports digital transformation across industries by enabling faster data processing, real-time decision-making, and reduced operational complexity, making it a key focus area for investors and CIOs.

North America leads the Global All Flash Data Center Market, driven by hyperscale data center growth, strong cloud adoption, and early flash integration across sectors. Asia-Pacific is emerging quickly, with countries like China, India, and Japan investing in smart infrastructure, fintech, and public digital services. Europe remains a steady contributor, supported by green data center initiatives and data compliance needs. Latin America, Middle East, and Africa show rising demand, propelled by connectivity expansion and enterprise IT modernization.

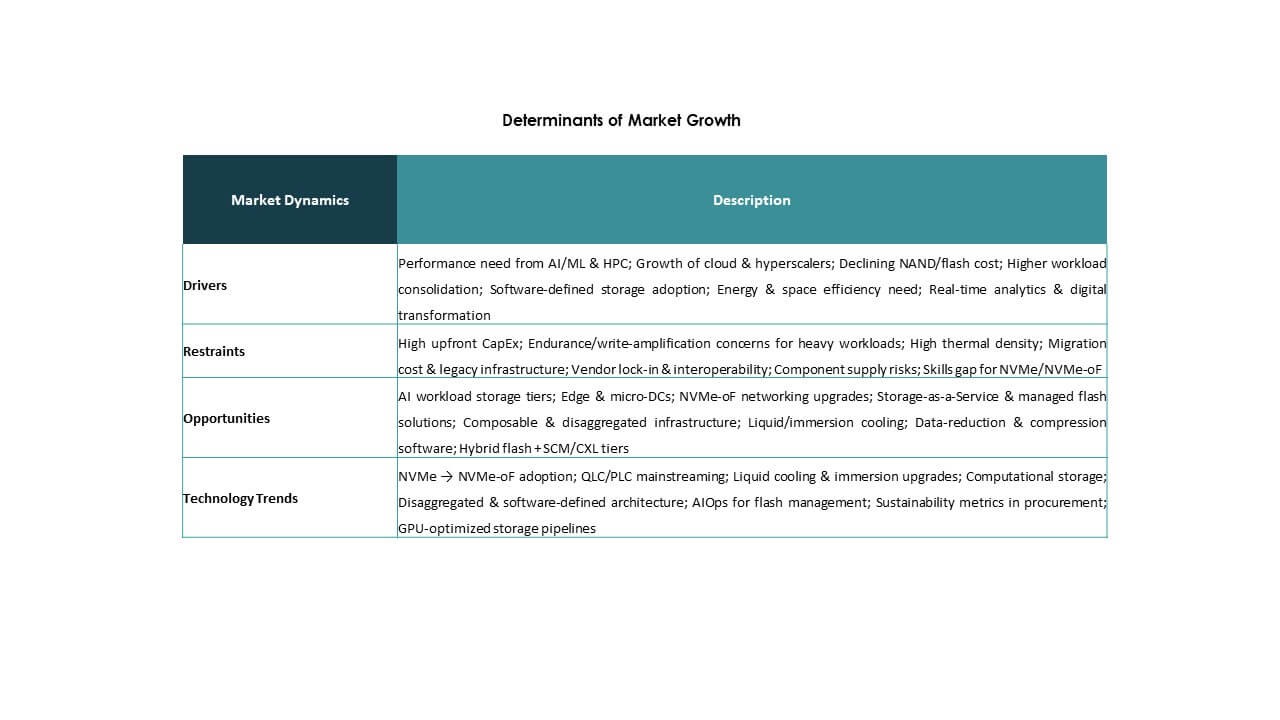

Market Drivers

Rising Adoption Of High‑Performance Flash Storage For Data‑Intensive Workloads

Enterprises adopt flash storage to handle fast data growth and low latency needs. AI, analytics, and real‑time processing drive this shift. Flash systems deliver consistent performance under heavy workloads. Businesses require predictable response times for digital services. NVMe architectures improve throughput across enterprise applications. IT teams favor flash for mission‑critical systems. The Global All Flash Data Center Market gains importance for competitive operations. Investors view flash adoption as a long‑term infrastructure upgrade. The market supports scalable and resilient digital platforms.

Shift Toward Cloud‑Native And Software‑Defined Data Center Architectures

Cloud models influence storage design across modern data centers. Enterprises deploy flash to support containerized workloads. Software‑defined storage improves resource flexibility. Flash arrays integrate well with virtualization platforms. Hybrid environments require fast and reliable storage layers. Businesses seek unified management across cloud and on‑premise systems. The Global All Flash Data Center Market supports cloud agility goals. Strategic value rises for firms modernizing legacy infrastructure. This shift strengthens enterprise digital readiness.

- For instance, Dell PowerStore all-flash systems deliver up to 25% faster performance for mixed workloads in virtualized and containerized environments, supported by modular architecture optimized for hybrid cloud deployments.

Growing Focus On Energy Efficiency And Data Center Optimization

Data centers face pressure to reduce power use. Flash storage consumes less energy than disk systems. Higher density reduces floor space needs. Cooling efficiency improves with fewer moving components. Operators target better sustainability performance. Flash supports green data center strategies. The Global All Flash Data Center Market aligns with ESG priorities. Businesses improve operational efficiency through modern storage. Investors favor assets with lower energy risk.

Expansion Of AI, Machine Learning, And High‑Performance Computing Use Cases

AI workloads demand high input and output speed. Flash storage meets these performance needs. Machine learning models process large datasets rapidly. HPC environments require consistent latency control. Flash arrays support parallel data access. Enterprises deploy flash for research and automation. The Global All Flash Data Center Market supports advanced computing adoption. Strategic value increases for innovation‑driven industries. This driver strengthens long‑term infrastructure demand.

- For example, BDO Unibank adopted Huawei OceanStor Dorado all‑flash storage, lifting storage utilization from under 40% to around 70% and delivering 1.3 GB/s throughput, dramatically improving data handling for analytics and shared workloads.

Market Trends

Market Trends

Rising Adoption Of NVMe‑Over‑Fabrics In Enterprise Data Centers

NVMe‑over‑Fabrics gains traction across large facilities. This design reduces storage latency further. Enterprises upgrade networks to support NVMe protocols. Flash arrays benefit from faster data paths. Performance gains improve application responsiveness. Vendors expand NVMe‑ready product portfolios. The Global All Flash Data Center Market reflects this shift. IT buyers prioritize end‑to‑end flash optimization. This trend reshapes storage network design.

Growth Of Consumption‑Based And As‑A‑Service Storage Models

Enterprises prefer flexible spending models. Vendors offer flash storage through subscription plans. Usage‑based pricing improves cost visibility. Businesses avoid large upfront investments. Financial planning becomes more predictable. Flash adoption expands across mid‑size firms. The Global All Flash Data Center Market supports service‑led delivery. Providers align offerings with cloud economics. This trend changes vendor revenue strategies.

Integration Of All Flash Systems With Edge And Distributed Data Centers

Edge computing expands across industries. Flash storage supports compact edge deployments. Low latency improves local data processing. Telecom and retail drive edge demand. Flash arrays fit space‑constrained sites. Data moves faster closer to users. The Global All Flash Data Center Market adapts to edge growth. Vendors design rugged and scalable flash systems. This trend supports distributed architectures.

Increased Use Of AI‑Driven Storage Management And Automation Tools

Automation improves storage efficiency and uptime. AI tools optimize flash performance. Predictive analytics reduce system downtime. IT teams gain better workload visibility. Automated tiering improves data placement. Vendors embed intelligence into flash platforms. The Global All Flash Data Center Market benefits from smart management. Enterprises reduce manual operations. This trend improves operational control.

Market Challenges

Market Challenges

High Initial Capital Requirements And Migration Complexity For Enterprises

Flash infrastructure requires significant upfront investment. Budget limits slow adoption in cost‑sensitive sectors. Legacy system migration adds technical risk. Data transfer planning requires skilled teams. Downtime concerns delay replacement decisions. Smaller firms face financial pressure. The Global All Flash Data Center Market faces slower uptake in such cases. Vendors must address cost barriers. Adoption speed varies across regions.

Supply Chain Constraints And Flash Memory Price Volatility

Flash memory depends on global semiconductor supply chains. Disruptions affect component availability. Price swings impact procurement planning. Long lead times delay deployments. Enterprises face uncertainty in storage budgets. Vendors manage inventory risk carefully. The Global All Flash Data Center Market reacts to supply shifts. Strategic sourcing becomes critical. Market stability depends on chip production capacity.

Market Opportunities

Rising Demand From Emerging Economies And Digital Transformation Programs

Emerging markets expand digital infrastructure rapidly. Governments invest in cloud and data centers. Enterprises modernize IT systems. Flash storage supports scalable growth. Financial services and telecom drive demand. Local data regulations favor domestic facilities. The Global All Flash Data Center Market sees expansion potential. Vendors target regional partnerships. This opportunity supports long‑term growth.

Expansion Of Industry‑Specific Flash Solutions And Vertical Use Cases

Industries require tailored storage performance. Healthcare demands fast data access. BFSI relies on low latency systems. Manufacturing uses flash for automation data. Retail adopts flash for analytics platforms. Vendors design vertical‑focused solutions. The Global All Flash Data Center Market benefits from specialization. Businesses gain better workload alignment. This opportunity enhances value creation.

Market Segmentation:

Market Segmentation:

By Deployment

The Hybrid Cloud segment dominates the Global All Flash Data Center Market, accounting for over 40% of the total share in 2025. Enterprises favor hybrid models to balance data control and scalability. Hybrid deployments offer flexibility to run critical workloads on-premise while leveraging cloud agility. Flash systems enhance workload responsiveness across distributed environments. On-premises solutions follow, supported by demand from highly regulated sectors like banking and government. Private cloud usage also expands in security-sensitive industries. The market continues to shift toward hybrid-first infrastructure strategies, making it a central focus for vendors and IT buyers.

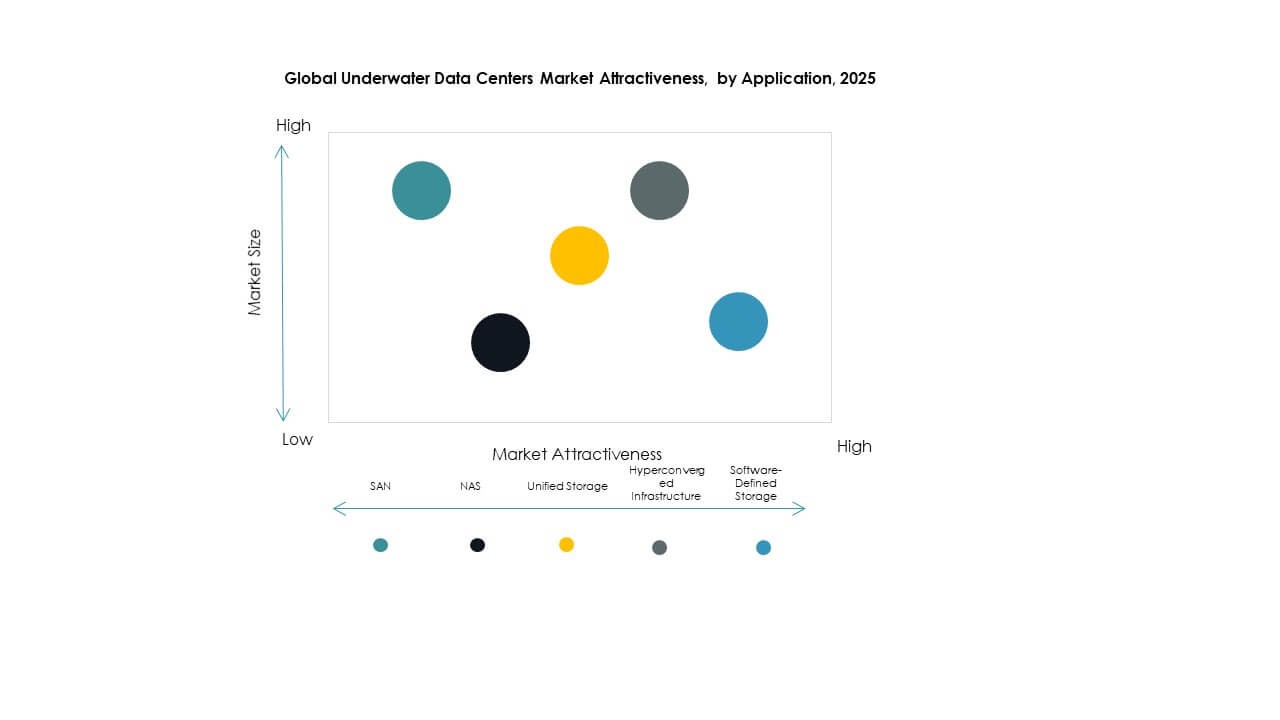

By Storage Architecture

The SAN (Storage Area Network) segment leads the Global All Flash Data Center Market with approximately 35% share due to its performance in latency-sensitive environments. Enterprises deploy SAN flash arrays for structured databases, financial workloads, and ERP systems. Hyperconverged Infrastructure (HCI) is the fastest-growing subsegment, driven by its ability to combine compute, storage, and networking in a scalable unit. Software-Defined Storage (SDS) gains momentum by enabling flexible, hardware-agnostic flash management. Unified and NAS systems support mid-scale operations with ease of deployment. Architecture preference depends on workload intensity, scalability goals, and total cost of ownership.

By Application

Big Data Analytics holds the largest share in the Global All Flash Data Center Market, accounting for about 30% of deployment cases in 2025. Flash arrays handle massive, real-time data streams in AI, IoT, and machine learning environments. Backup and Recovery follows as a major application area due to flash’s ability to reduce restore times significantly. Database Management, particularly in NoSQL and distributed systems, also sees strong growth. High-Performance Computing (HPC) and Virtualization segments are expanding across research and corporate IT environments. Content Delivery Networks leverage flash for rapid data retrieval across distributed locations.

By End User

The IT & Telecom sector leads the Global All Flash Data Center Market with nearly 32% share, driven by rising demand for low-latency infrastructure, 5G readiness, and high throughput. Cloud Service Providers follow closely, using flash to deliver consistent, high-speed services to enterprise clients. BFSI is a critical segment due to flash’s ability to support high-frequency transactions and secure data handling. Healthcare & Life Sciences benefit from flash adoption in genomics and digital imaging. Manufacturing & Retail embrace flash for supply chain analytics, while Government & Public Sector deployments focus on secure, high-performance data handling.

Regional Insights:

Regional Insights:

North America Dominates Due to Cloud Spending and Flash Technology Integration

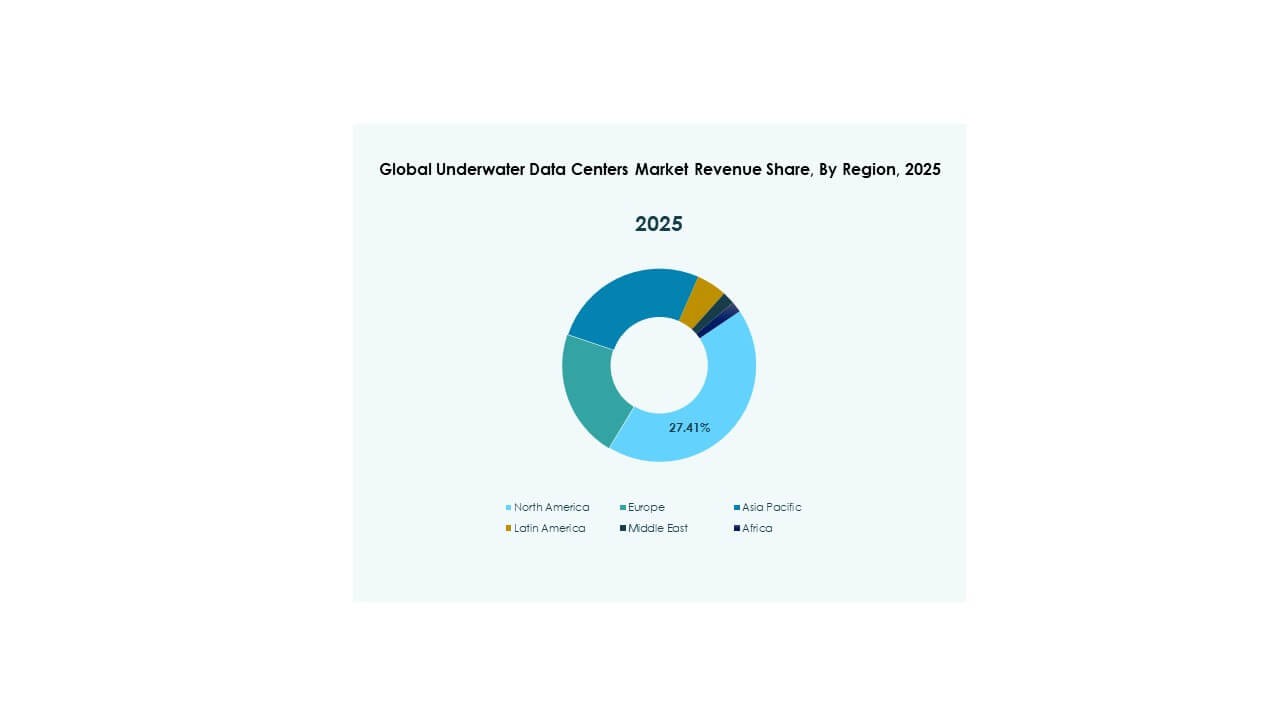

North America holds the largest share in the Global All Flash Data Center Market, accounting for approximately 38% of the global revenue. The United States leads in hyperscale investments, driven by Amazon, Google, and Microsoft. Cloud service providers deploy flash infrastructure to ensure speed, scale, and reliability. Enterprises across sectors integrate AI and analytics, further fueling flash demand. The region also benefits from mature digital ecosystems and skilled IT labor. Strong government focus on secure, energy-efficient facilities supports growth. Canada contributes through AI innovation zones and colocation expansions. Mexico sees increasing adoption across telecom and finance sectors. The region remains at the forefront of flash‑based transformation.

- For instance, Amazon and Google together accounted for half of the 52 new hyperscale data centers that opened globally in 2020, with Microsoft also being particularly active in these deployments.

Asia-Pacific Emerges Rapidly with Government Support and Digital Acceleration

Asia-Pacific follows with around 29% share, led by China, Japan, and India. China drives large-scale deployments due to data localization laws and digital economy goals. Japan’s advanced industrial base and robotics investments require reliable flash systems. India experiences growth from fintech, public digital infrastructure, and smart city programs. South Korea and Taiwan support demand through semiconductor innovation and regional cloud services. Southeast Asian countries such as Singapore, Indonesia, and Malaysia build next-gen facilities for regional data traffic. The Global All Flash Data Center Market in this region benefits from both hyperscale and edge deployments. Government incentives, rising tech startups, and increased mobile usage fuel expansion.

- For instance, Huawei introduced the OceanStor Dorado all‑flash storage systems at MWC Barcelona 2025, featuring a design that enhances performance and resilience for AI and cloud workloads.

Europe Focuses on Sustainability and Energy Efficiency in Storage Deployments

Europe holds nearly 21% of the Global All Flash Data Center Market, driven by strict energy regulations and green data strategies. Countries like Germany, France, and the UK invest in flash systems to meet performance and carbon goals. The market favors low-latency systems for financial trading, healthcare, and manufacturing. Adoption grows in Nordic countries due to cold climate benefits and renewable integration. Enterprises migrate from legacy storage to comply with GDPR and improve operational control. Flash infrastructure supports cloud adoption in public sector initiatives across the EU. Southern and Eastern Europe show slower growth but offer long-term opportunity through digital transformation roadmaps. Europe remains stable, with policy-driven technology upgrades shaping storage trends.

Competitive Insights:

Competitive Insights:

- Dell Technologies

- NetApp

- Pure Storage

- Hewlett Packard Enterprise (HPE)

- IBM

- Hitachi Vantara

- Huawei Technologies

- Fujitsu

- Western Digital

- Seagate Technology

- Oracle Corporation

- Super Micro Computer

- Solidigm

- Quantum Corporation

- VAST Data

The competitive landscape of the Global All Flash Data Center Market features established IT infrastructure giants and specialized flash storage innovators. Dell Technologies, HPE, and IBM lead through broad portfolios and deep integration with enterprise systems. Pure Storage and VAST Data focus on high‑performance flash arrays and next‑gen architectures. NetApp and Hitachi Vantara emphasize unified storage and scalable deployment models. Western Digital and Seagate Technology support flash adoption through component expertise. Huawei, Fujitsu, and Oracle leverage regional strengths and complete ICT solutions. Solidigm and Quantum introduce niche offerings for performance‑intensive workloads. Super Micro Computer enhances custom flash‑optimized servers. Competition centers on innovation, performance, and total cost of ownership improvements. Vendors pursue partnerships, product upgrades, and geographic expansion to gain market share.

Recent Developments:

Recent Developments:

- In April 2025, Dell Technologies launched the PowerProtect All-Flash Ready Node, marking the first step in its all-flash data protection journey for data centers, offering over 61% faster restore speeds, 30% less power usage, and a 5X smaller footprint compared to traditional systems.

- In March 2025, Huawei launched its New-Gen All-Flash Data Center products, including the OceanStor Dorado Converged All-Flash Storage for mission-critical applications, at MWC Barcelona. These innovations feature a data and control plane separation architecture that triples performance and ensures zero data loss even with multiple controller failures, targeting AI-driven data challenges in sectors like finance