Executive summary:

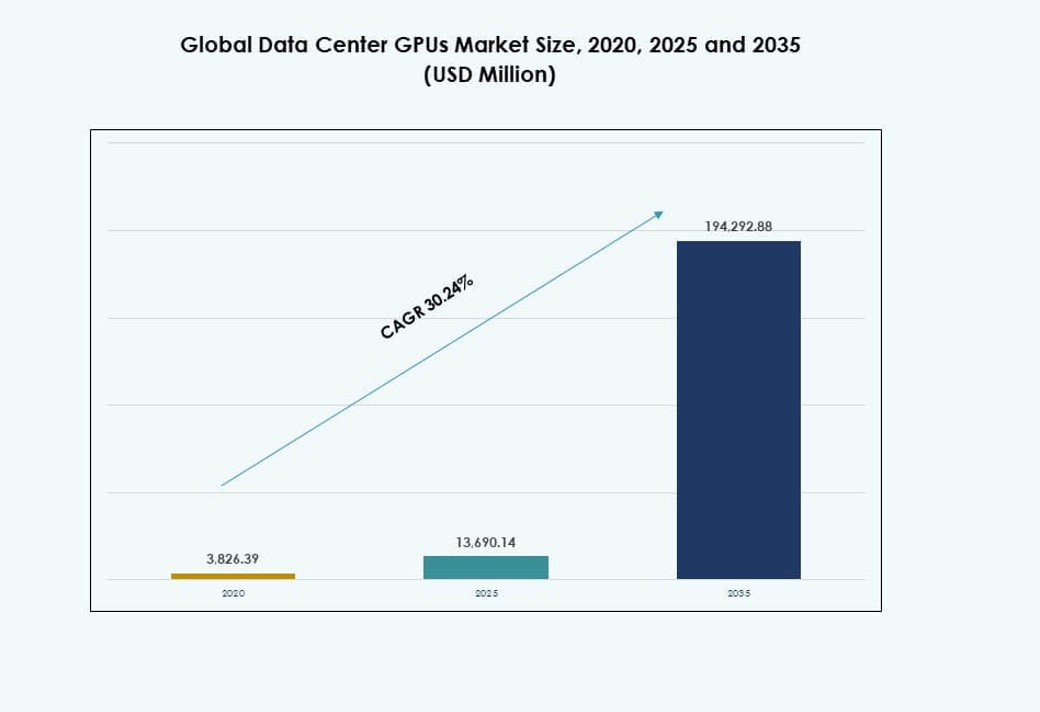

The Global Data Center GPUs Market size was valued at USD 3,826.39 million in 2020 to USD 13,690.14 million in 2025 and is anticipated to reach USD 194,292.88 million by 2035, at a CAGR of 30.24% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2035 |

| Data Center GPUs Market Size 2025 |

USD 13,690.14 Million |

| Data Center GPUs Market, CAGR |

30.24% |

| Data Center GPUs Market Size 2035 |

USD 194,292.88 Million |

Data center operators expand GPU capacity to meet sustained demand for AI training and large-scale inference across cloud and enterprise workloads. Vendors advance architecture efficiency, memory bandwidth, and interconnect performance to improve throughput per rack and reduce deployment friction. Buyers prioritize validated platforms, mature software stacks, and fleet management tools that shorten time-to-production. It supports faster product cycles for digital services, strengthens competitiveness for enterprises, and attracts investor interest through high utilization potential and durable infrastructure spending.

North America leads due to hyperscaler concentration, deep AI software ecosystems, and strong enterprise adoption across the U.S. Europe follows with growth in sovereign cloud initiatives and industrial AI use, led by the UK, Germany, and France. Asia Pacific emerges rapidly, driven by China, Japan, South Korea, and India through new data center builds and expanding cloud regions. Middle East hubs gain momentum through national AI programs, while Latin America grows steadily as colocation capacity and cloud availability improve.

Market Dynamics:

Market Drivers:

Explosive AI Workload Growth And GPU-Centric Compute Planning

Global Data Center GPUs Market demand rises because AI workloads now shape capacity plans across hyperscalers and enterprises. Hyperscalers expand GPU clusters to support large-model training and high-volume inference at scale. Enterprises move critical analytics and automation programs to GPU-ready platforms to improve time-to-insight. Procurement teams treat accelerator supply as a strategic asset that affects product road maps and revenue timing. Boards approve larger capital budgets when GPU capacity links to customer retention and premium services. Investors track utilization and backlog trends because they signal durability of AI-led spend. Cloud providers compete on GPU availability, price-performance, and service-level commitments for AI users.

- For instance, Meta deployed two 24,576-GPU data center-scale clusters specifically to train its Llama 3 model family, with a roadmap to accumulate 350,000 NVIDIA H100 GPUs representing compute power equivalent to nearly 600,000 H100s by the end of 2024, directly linking GPU procurement volume to its generative AI product road map.

High-Performance Interconnect And Cluster Architecture Upgrades Raise GPU Pull-Through

Global Data Center GPUs Market expands with each generation of faster interconnect and denser node designs that improve scaling and cluster efficiency. Data centers upgrade networking and fabrics to reduce latency and keep accelerators fed with data. Vendors improve memory bandwidth, chip-to-chip links, and multi-GPU scaling features for larger jobs. Operators adopt composable and disaggregated designs to allocate GPUs across teams with tighter control. Standardized reference architectures shorten deployment time and reduce risk for large cluster rollouts. System integrators package validated stacks that lower integration effort for enterprises and public sector labs. Capital flows to platforms that show predictable performance under production conditions.

Energy Efficiency And Space Constraints Accelerate Transition To New GPU Platforms

Global Data Center GPUs Market gains momentum because energy limits force efficiency-first purchasing decisions across new builds and retrofits. Operators prioritize performance per watt to expand compute within fixed utility and cooling envelopes. New GPU designs reduce total cost of ownership through higher throughput per rack and per megawatt. Thermal management upgrades support higher-density deployments and protect uptime for mission-critical AI services. Colocation providers add liquid-capable suites to capture tenants that need dense accelerator pods. Sustainability targets influence procurement, with efficiency metrics tied to corporate commitments and audits. Investors favor operators that turn energy constraints into competitive advantage through smarter architectures.

- For instance, Supermicro’s validated comparison of liquid-cooled versus air-cooled NVIDIA GPU systems found that liquid cooling maintains GPU junction temperatures at 46–54°C versus 55–71°C for air-cooled configurations, delivers up to 17% higher computational throughput under stress, and reduces node-level power draw by an average of 1 kW (16%) per node translating to approximately $2.25 million in annual energy cost savings across a 2,000-node deployment.

Software Ecosystems And Developer Productivity Reinforce GPU Platform Stickiness

Global Data Center GPUs Market benefits from software stacks that reduce friction for model development and deployment at scale. Developer teams rely on mature libraries, compilers, and runtime tools that shorten experiment cycles. Platform vendors invest in security, orchestration, and observability features that meet enterprise controls. MLOps pipelines standardize training, evaluation, and deployment steps across hybrid environments. A strong ecosystem lowers switching costs and supports multi-year platform road maps for buyers. Channel partners and OEMs expand validated offerings that simplify adoption for midMarket enterprises. Investors view ecosystem depth as a moat that supports pricing power and recurring platform revenue. It increases demand for GPUs that pair hardware capability with robust tooling and long-term support.

Market Trends:

GPU Supply Contracts Shift Toward Capacity Reservation And Service Guarantees

Global Data Center GPUs Market shows a shift toward structured procurement and multi-quarter planning as buyers seek certainty on delivery and uptime. Buyers negotiate capacity reservations to secure delivery windows and stabilize expansion schedules. Cloud providers publish clearer availability tiers that link pricing to queue priority. Enterprises adopt managed GPU services to reduce operational burden and speed internal adoption. Vendors bundle support, firmware updates, and fleet tools into subscription-like programs. Financing structures gain traction for large deployments that need predictable cash flow. Partners offer turnkey cluster delivery with performance benchmarks and acceptance criteria. It improves planning discipline and reduces delays tied to uncertain lead times.

Inference Optimization Becomes A Primary Design Goal Across Data Centers

Global Data Center GPUs Market evolves as inference volume rises across search, copilots, customer service, and internal productivity tools. Operators tune stacks to cut latency and reduce cost per request through quantization and model compression. Scheduling policies prioritize steady throughput and predictable response time for user-facing workloads. Mixed-precision execution expands, with operators balancing accuracy targets and compute cost. Multi-tenant inference grows inside shared clusters that use stronger isolation and governance controls. Edge inference expands for latency-sensitive use cases, with selective deployment near users and devices. Vendors emphasize platform features that support efficient batching and tighter memory management at scale. It shifts purchasing decisions toward GPUs that excel in real-time and high-volume inference.

Cluster Operations Mature With Telemetry-Driven Fleet Management

Global Data Center GPUs Market reflects a stronger focus on operational control as fleets grow and failure impact rises. Operators standardize telemetry to track utilization, errors, thermals, and job efficiency across clusters. Automated remediation policies reduce downtime and protect high-value GPU assets from cascading failures. SRE teams adopt workload-aware monitoring that ties performance to service objectives. Predictive maintenance becomes common, with failure signals used to schedule service and reduce outages. Policy-based governance controls job priority, quota, and cost allocation across business units. Security hardening expands, with tighter isolation and firmware integrity checks across the stack. It raises demand for GPUs that integrate cleanly with fleet tools and enterprise controls.

Liquid-Capable Facilities Expand Beyond Hyperscalers Into Colocation Portfolios

Global Data Center GPUs Market tracks new facility builds that support higher rack densities and stable thermal performance. Colocation providers add liquid-ready halls to win AI tenants that need dense accelerator pods. Design standards shift toward direct-to-chip and rear-door options for predictable heat removal. Operators revisit power distribution to support higher draw per rack without stability issues. Construction plans favor modular pods that shorten delivery time and scale in repeatable increments. Site selection ties more closely to power access, permitting, and heat rejection options. Service providers develop operating playbooks for coolant management and maintenance. It expands addressable deployments outside captive hyperscale campuses.

Market Challenges:

Supply Concentration And Qualification Cycles Create Procurement Risk

Global Data Center GPUs Market faces procurement risk because supply concentration and long qualification cycles limit flexibility for many buyers. A small set of vendors and foundry routes increases exposure to allocation constraints and disruptions. Large buyers secure priority through volume, which tightens availability for smaller enterprises. Qualification requirements slow substitution because software stacks and drivers require validation at scale. Export controls and compliance rules add friction for cross-border deployments and reseller channels. Lead-time uncertainty complicates capex timing and delays service launches tied to GPU capacity. Warranty, firmware, and security requirements raise due diligence effort for operators. It forces buyers to diversify suppliers, negotiate stronger terms, and maintain buffer capacity.

Power, Cooling, And Cost Pressures Challenge Deployment Economics

Global Data Center GPUs Market confronts hard limits from power delivery, cooling capability, and rising capital intensity that can weaken deployment economics. Older sites struggle to host dense GPU racks without major retrofits and operational risk. Energy price volatility affects total cost of ownership and can shift location decisions quickly. Grid constraints delay new builds, which slows cluster expansion even when demand stays strong. Cooling complexity raises maintenance needs and increases the impact of operational errors. Capital intensity grows, which elevates the need for clear utilization targets and chargeback models. Skilled talent shortages limit the pace of reliable deployment and day-two operations. It pushes buyers to optimize utilization and prioritize workloads with the strongest returns.

Market Opportunities:

Enterprise Adoption Expands Through Managed Platforms And Vertical AI Use Cases

Global Data Center GPUs Market can accelerate as enterprises scale AI programs beyond pilots and adopt managed GPU platforms that reduce setup time. Managed services support governance, security, and cost control, which helps regulated industries expand faster. Industry-specific models in finance, health care, and manufacturing drive predictable demand patterns tied to measurable outcomes. Private and hybrid deployments help buyers keep data controls while using modern AI stacks. It creates room for integrators, OEMs, and software partners that package validated solutions and support repeatable rollouts.

Emerging Regions Add New Capacity Through Colocation And Sovereign AI Programs

Global Data Center GPUs Market has upside where new data center builds align with national AI priorities and local compute programs. Sovereign cloud and public-sector procurement support long-term capacity plans and stable demand signals. Colocation providers expand GPU-ready footprints to serve startups and enterprises without captive campuses. Edge deployments unlock latency-sensitive inference for retail, telecom, and smart infrastructure. It opens opportunities for vendors that deliver efficient platforms, strong service ecosystems, and deployment support across new regions.

Market Segmentation:

By Deployment Type

Global Data Center GPUs Market skews toward cloud-based deployments, which hold about 68% share due to hyperscaler scale, pooled utilization, and broad developer access. CSPs attract model developers with elastic capacity, managed services, and faster provisioning across regions. On-premises growth persists in regulated industries that require tighter data control and predictable cost structures. Enterprises adopt hybrid patterns that burst to cloud for peak training cycles while keeping sensitive workloads local. Security requirements and latency targets support local clusters for specific use cases. It benefits vendors that deliver consistent software stacks and management tools across cloud and enterprise environments.

By Function

Global Data Center GPUs Market remains training-led, with training GPUs near 58% share because frontier models require large-scale compute and long run times. Inference expands quickly as AI features move into everyday products and internal workflows across sectors. Operators focus on inference efficiency to improve latency and reduce cost per request at scale. Training demand stays strong in foundation model development, advanced research, and large enterprise pipelines. Mixed workloads push buyers toward flexible platforms that support both functions with stable performance. It favors vendors that pair high throughput with strong scheduling, isolation, and reliability features.

By Application

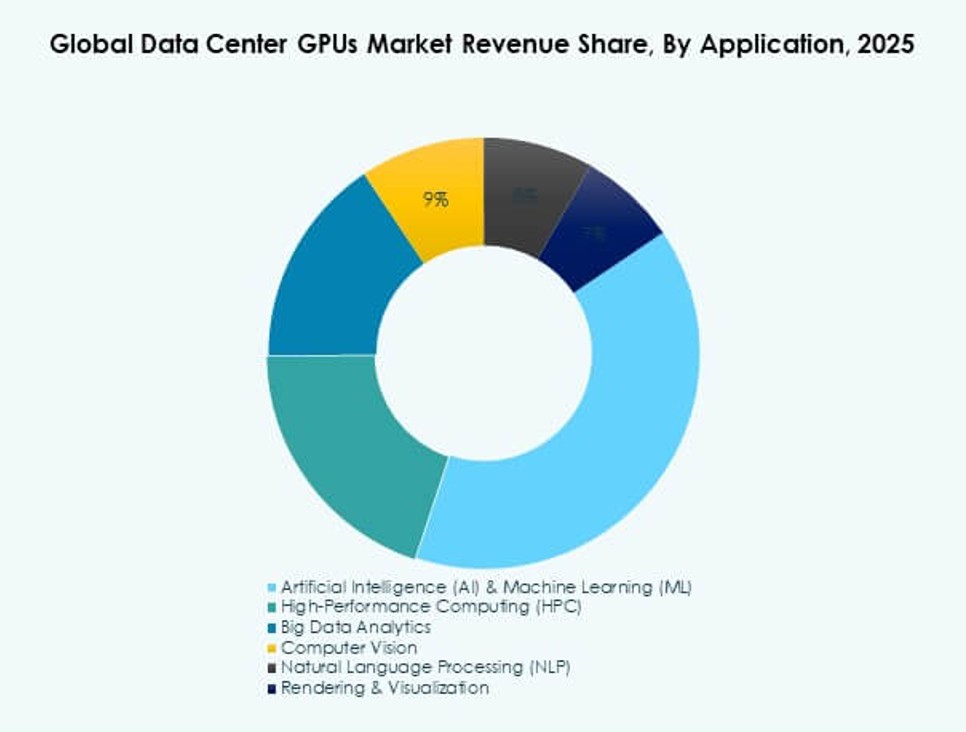

Global Data Center GPUs Market is dominated by AI and ML at roughly 46% share due to rapid deployment of copilots, automation, and predictive analytics across industries. HPC keeps a strong position in science, engineering simulation, and national lab workloads that demand high precision. Big data analytics uses GPUs to speed feature extraction and complex query processing for faster decision cycles. Computer vision and NLP grow with enterprise search, content moderation, surveillance, and customer engagement tools. Rendering and visualization remain important for media production, design workflows, and digital twins. It expands as more applications require low-latency inference and scaled model training.

By End User

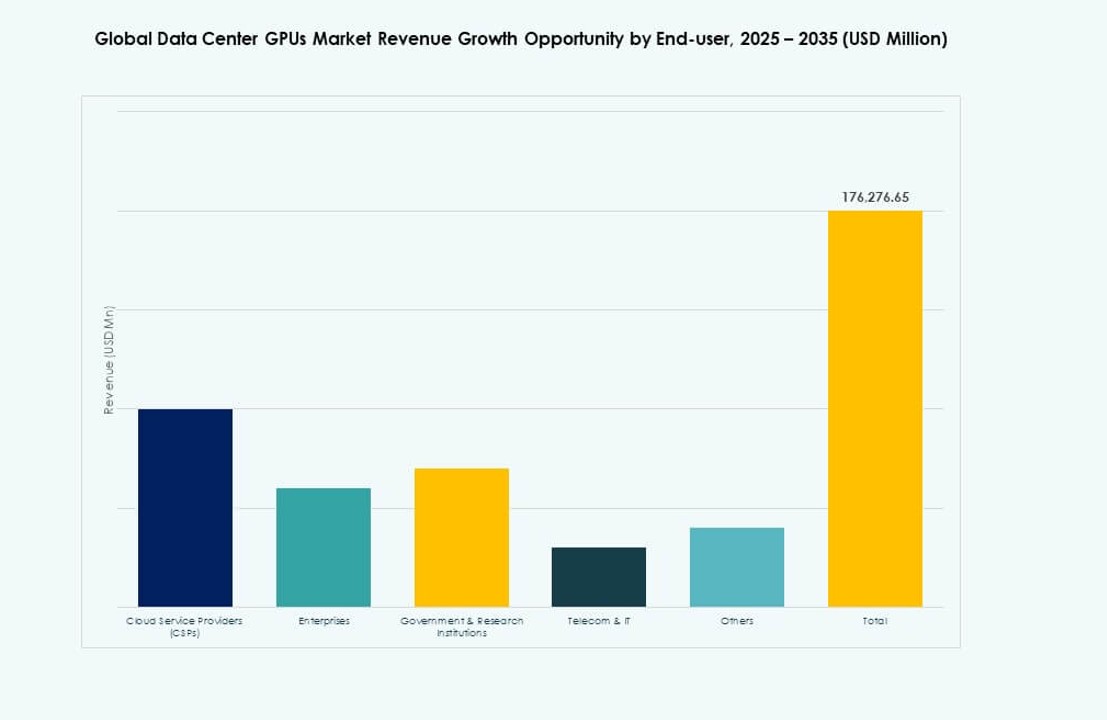

Global Data Center GPUs Market is led by cloud service providers with about 64% share because they aggregate demand and operate high-utilization fleets. Enterprises follow with steady growth tied to internal AI platforms, analytics modernization, and industry-focused solutions. Government and research institutions invest in sovereign compute, advanced research, and simulation priorities. Telecom and IT players adopt GPUs for network analytics, edge inference, and service delivery platforms. Other end users include startups and digital-native firms that rent capacity through cloud and colocation ecosystems. It rewards providers that deliver availability, predictable performance, and strong support programs.

By GPU Type / Architecture

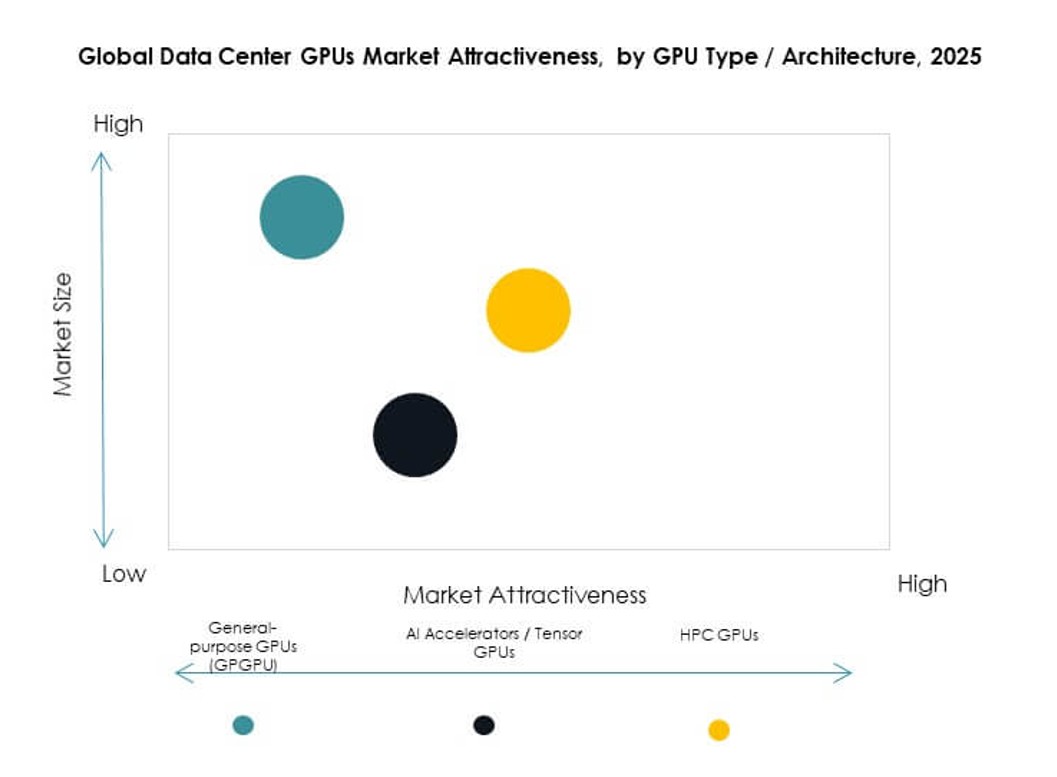

Global Data Center GPUs Market tilts toward AI accelerators or tensor GPUs at around 52% share due to specialization for matrix-heavy workloads and strong performance on modern AI models. General-purpose GPUs keep a broad role where flexibility and mature tooling support diverse workloads. HPC GPUs remain critical for double-precision and large-scale simulation needs in research and engineering. Architecture choices depend on memory bandwidth, interconnect scaling, and software compatibility across toolchains. Buyers also weigh security features and lifecycle support for long-life deployments. It grows where platforms combine strong performance with dependable software and service commitments.

By Data Center Type

Global Data Center GPUs Market is anchored in hyperscale data centers with about 62% share because they deploy the largest GPU clusters and set performance benchmarks. Colocation expands as providers build liquid-capable suites to host dense accelerator pods for enterprises and cloud partners. Edge data centers grow for latency-sensitive inference and distributed AI services that need proximity to users and devices. Hyperscale sites drive standards for efficiency and operational maturity that influence procurement across the Market. Colocation supports faster Market entry for buyers that avoid heavy capex and want flexible scaling. It broadens as GPU-ready capacity spreads across more facility types and geographies.

Regional Insights:

North America And Europe Lead Through Hyperscaler Scale And Enterprise Spend

Global Data Center GPUs Market is strongest in North America at 38% share due to hyperscaler concentration, deep software ecosystems, and strong enterprise AI spend. U.S. demand remains high as cloud providers expand GPU regions and AI services for commercial customers. Canada benefits from research networks and new data center capacity in key metros. Europe holds about 23% share, supported by industrial AI adoption and rising sovereign cloud priorities. UK, Germany, and France drive deployments through enterprise modernization and public-sector digitization initiatives. It gains from a strong colocation base that offers GPU-ready capacity for regional customers.

- For instance, Microsoft said its European footprint will extend to more than 200 datacenters across the continent, and at Ignite 2024 it introduced Azure ND GB200 V6 virtual machines powered by NVIDIA GB200 Superchips to scale advanced AI training and inference workloads in the cloud.

Asia-Pacific Expands Rapidly With New Capacity And National AI Priorities

Global Data Center GPUs Market shows fast expansion in Asia-Pacific with 32% share due to new builds, broad enterprise digitization, and major cloud investment. China, Japan, South Korea, and India drive demand through cloud expansion and large-scale AI deployment across industries. Regional platforms invest in domestic AI stacks and high-volume inference for consumer and enterprise services. Data center construction accelerates in key hubs, with more sites designed for high-density compute and liquid readiness. Local procurement policies and supply strategies shape platform choices and deployment pace. It benefits from rising colocation capacity that supports startups and multinational enterprises across the region.

Latin America And Middle East And Africa Build A Smaller But Rising Base

Global Data Center GPUs Market remains smaller in Latin America at 4% share, yet demand rises in Brazil and selected regional hubs where cloud regions expand. Colocation growth improves access to accelerator capacity for local enterprises and digital services. Middle East and Africa account for about 3% share, supported by GCC investment programs and digital sovereignty agendas. New hyperscale-linked projects and public-sector compute programs lift early adoption. Power access, permitting, and facility readiness remain key constraints that slow large cluster rollout. It advances where operators pair GPU capacity with strong connectivity, reliable power, and enterprise-grade services.

- For instance, AWS states that its cloud now spans 123 Availability Zones across 39 geographic Regions, with seven more Availability Zones and two additional Regions planned in Saudi Arabia and Chile, while current regional service coverage already includes São Paulo, Bahrain, and the UAE, underscoring the steady build-out of cloud infrastructure across Latin America and the Middle East.

Competitive Insights:

- NVIDIA Corporation

- Advanced Micro Devices (AMD)

- Intel Corporation

- Google LLC (Google Cloud TPU)

- Amazon Web Services (AWS)

- Microsoft Corporation (Azure)

- Huawei Technologies Co., Ltd.

- Qualcomm Incorporated

- Samsung Electronics

- Cambricon Technologies

The competitive landscape in the Global Data Center GPUs Market centers on performance leadership, ecosystem depth, and supply assurance. NVIDIA sets the pace in high-end accelerators and software tooling, while AMD pressures pricing and expands platform options across AI and HPC workloads. Intel competes through CPU-GPU platform integration and enterprise procurement reach, even as it rebuilds credibility in accelerated computing. Hyperscalers shape demand with custom silicon strategies, proprietary stacks, and preferred supplier programs that influence Market access. Chinese vendors such as Huawei and Cambricon target domestic capacity needs and sovereign compute programs. Memory and packaging partners such as Samsung reinforce scale and roadmap execution. It rewards vendors that secure advanced process access, deliver stable drivers, and support fleet-grade management.

Recent Developments:

- In March 2026, Supermicrolaunched seven new AI Data Platform Solutions powered by NVIDIA RTX Pro 6000 GPUs and Spectrum-X networking, in collaboration with partners including DDN, as showcased at the NVIDIA GTC 2026 conference. These platforms are designed to support enterprise AI and HPC workloads with flexible deployment options.

- In October 2025, Qualcommannounced its entry into the data center GPU Market with the launch of two new AI accelerator chips the AI200 (available in 2026) and the AI250 (planned for 2027) both designed to fit into liquid-cooled server racks.

- In March 2026, NVIDIAunveiled its next-generation Vera Rubin GPU platform at its annual GTC conference in San Jose, California, combining Vera CPUs and Rubin GPUs alongside NVLink 6 Switch, ConnectX-9 SuperNIC, and Spectrum-6 Ethernet Switch.

- In January 2026, AMDunveiled its next-generation Instinct MI400X accelerator at CES in Las Vegas, designed to handle on-premises AI workloads, along with the Helios rack-scale system promising 3 AI exaflops of performance in a single rack.