Executive summary:

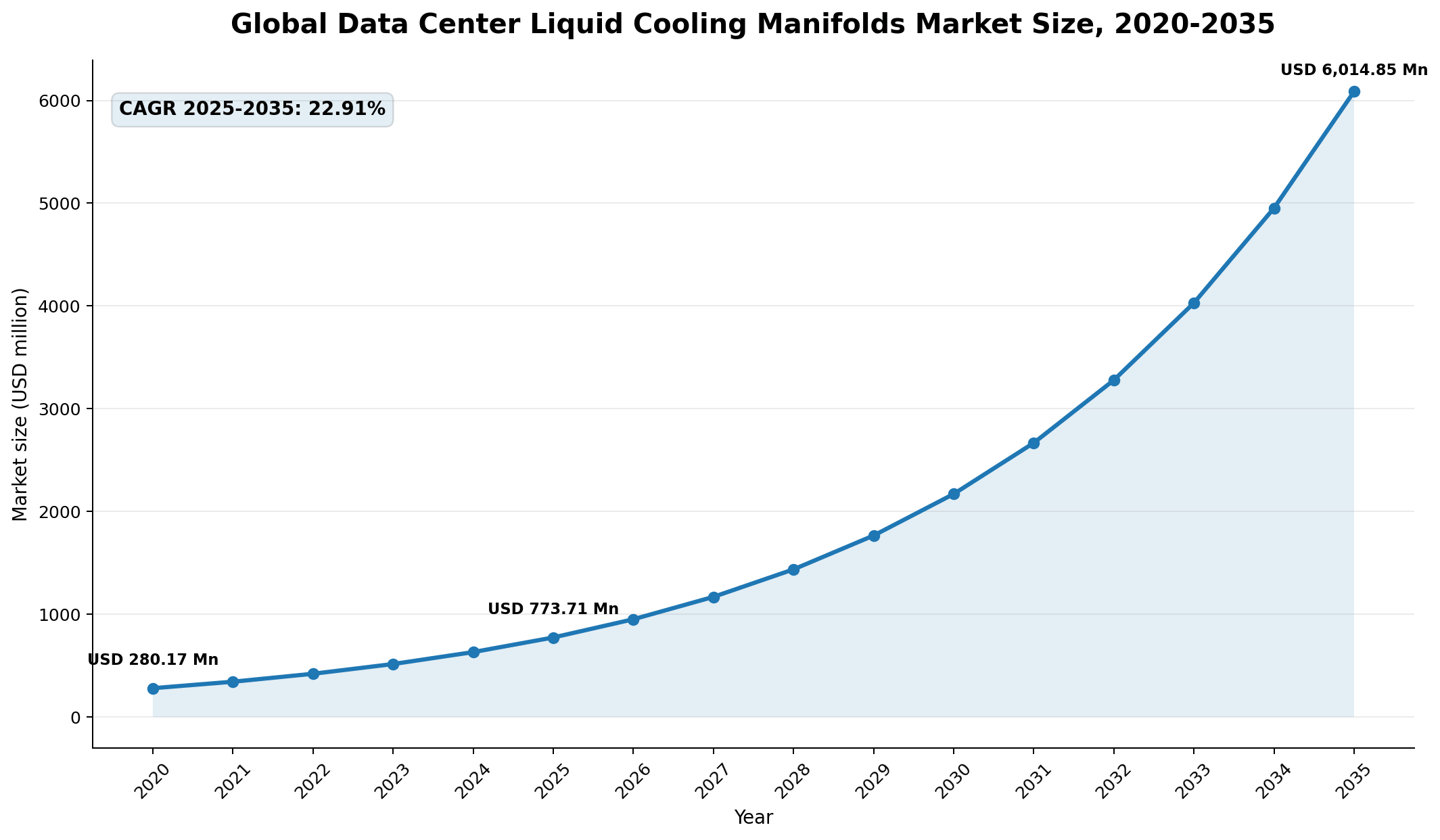

The Global Data Center Liquid Cooling Manifolds Market size was valued at USD 280.17 million in 2020 to USD 773.71 million in 2025 and is anticipated to reach USD 6,014.85 million by 2035, at a CAGR of 22.91% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2035 |

| Data Center Liquid Cooling Manifolds Market Size 2025 |

USD 773.71 Million |

| Data Center Liquid Cooling Manifolds Market, CAGR |

22.91% |

| Data Center Liquid Cooling Manifolds Market Size 2035 |

USD 6,014.85 Million |

The market is driven by rapid deployment of liquid cooling infrastructure across AI, high-performance computing, hyperscale and colocation data centers. Liquid cooling manifolds play a critical role in distributing coolant evenly across racks, rows, cold plates, immersion loops and facility-side systems. They help operators manage flow balance, pressure control, leakage risk and thermal reliability as rack power density rises. The market also benefits from stronger adoption of direct-to-chip cooling, modular liquid cooling architectures and high-performance manifold materials that support long-term uptime.

North America leads the market due to strong hyperscale investment, early AI infrastructure deployment and wider adoption of direct-to-chip liquid cooling. Europe follows with solid demand from energy-conscious data center operators, regulated industries and high-performance computing facilities. Asia Pacific is emerging as a high-growth region due to rapid cloud growth, AI cluster deployment and new data center construction across China, Japan, India, South Korea and Southeast Asia. Latin America, the Middle East and Africa remain smaller markets, but new colocation facilities, sovereign cloud projects and digital infrastructure investments support long-term growth.

Market Dynamics:

Market Drivers

Rising Adoption Of Direct-To-Chip Cooling In AI And HPC Data Centers

Direct-to-chip liquid cooling represents a major driver for the Global Data Center Liquid Cooling Manifolds Market because AI servers require precise coolant distribution near CPUs, GPUs and accelerators. Manifolds support this transition by routing coolant through rack-level or row-level loops while maintaining balanced flow across multiple cold plates. Hyperscale and HPC operators need highly reliable manifold systems that can support high-density racks, quick-connect fittings and modular expansion. This demand is rising as operators shift from traditional air cooling to liquid-based architectures. For instance, Vertiv states that direct-to-chip cooling can effectively cool about 75% of the IT load, which supports the need for advanced coolant distribution systems in high-density deployments.

Growth Of High-Density AI Rack Architectures And GPU Cluster Deployments

AI rack architectures require stronger fluid routing, better pressure stability and more reliable connection systems than conventional data center racks. The Global Data Center Liquid Cooling Manifolds Market benefits because manifolds serve as the coolant distribution backbone between CDUs, cold plates, immersion tanks and rack-level loops. Their importance increases as GPU clusters move toward higher thermal design power and denser server configurations. Operators need manifolds that can scale across multiple circuits, reduce pressure drops and simplify maintenance. This driver supports demand for in-rack manifolds, row-based manifolds and custom engineered manifold systems designed for AI and HPC environments.

Need For Energy Efficiency And Lower Thermal Management Cost

Data center operators are under pressure to reduce power consumption, improve cooling efficiency and manage rising operating costs. The Global Data Center Liquid Cooling Manifolds Market benefits because better manifold design improves coolant flow control, reduces imbalance and supports more efficient liquid cooling loops. Efficient distribution also helps facilities reduce overcooling and improve thermal predictability. This is especially important in hyperscale and colocation sites where small efficiency gains can have large financial impact. For instance, Vertiv reported that introducing liquid cooling in a fully optimized study created a 10.2% reduction in total data center power and more than 15% improvement in total usage effectiveness.

Expansion Of Greenfield Liquid-Cooled Data Center Construction

New AI-ready data centers are increasingly being designed with liquid cooling infrastructure from the beginning. The Global Data Center Liquid Cooling Manifolds Market benefits because greenfield facilities can integrate manifolds, piping, CDUs, leak detection and monitoring systems into the mechanical design. This reduces retrofit complexity and improves long-term scalability. New installations also create demand for modular manifolds that support phased rack deployment and future capacity expansion. Hyperscale and colocation operators prefer these systems because they reduce installation time and improve standardization across data halls. This driver supports strong growth across North America, Europe and Asia Pacific.

Market Trends

Shift Toward Modular And Multi-Circuit Manifold Designs

Modular and multi-circuit manifolds are becoming more important as operators deploy liquid cooling across different rack densities and workload zones. The Global Data Center Liquid Cooling Manifolds Market reflects this trend through systems that support flexible expansion, easier maintenance and better control over multiple coolant branches. Multi-circuit designs allow operators to isolate loops, support redundancy and balance flow across racks with different thermal loads. Modular manifolds also help colocation providers serve different customer requirements within the same facility. This trend favors suppliers that can provide standardized platforms with custom configuration options for direct-to-chip, immersion and hybrid liquid cooling systems.

Rising Use Of Stainless Steel, Polymer And Composite Flow Solutions

Material selection is becoming a key buying factor as liquid cooling systems require durability, corrosion resistance and fluid compatibility. The Global Data Center Liquid Cooling Manifolds Market is seeing stronger demand for stainless steel, copper, brass, aluminum and engineered plastic or composite materials. Stainless steel remains important in high-reliability environments, while advanced polymer solutions are gaining traction because they reduce corrosion risk and support lighter cooling infrastructure. For instance, Valex states that it provides high-purity stainless steel solutions for data center thermal management, including manifolds, tubing, fittings and valves for cold plate, dielectric and immersion cooling.

Adoption Of Open Standards, Quick Disconnects And Service-Friendly Architectures

Liquid cooling infrastructure is moving toward standardized, service-friendly architectures that reduce installation risk and simplify maintenance. The Global Data Center Liquid Cooling Manifolds Market reflects this trend through growing use of quick disconnects, dripless fittings, rack-level distribution points and open specification designs. These components help operators reduce leak risk during servicing and improve deployment speed. They also support broader supplier interoperability across cold plates, CDUs and rack systems. For instance, Parker Hannifin notes that its CDT Series dry-break, thread-to-connect quick disconnects are designed for liquid cooling inlets and manifolds and are based on Open Compute Project specifications.

Integration Of Manifolds With Smart Monitoring And Liquid Cooling Controls

Manifolds are increasingly being integrated with sensors, valves, flow meters and monitoring systems. The Global Data Center Liquid Cooling Manifolds Market benefits from this trend because operators want real-time insight into coolant flow, pressure, temperature and leak status. Smart monitoring helps reduce downtime risk and supports predictive maintenance across AI and HPC infrastructure. It also allows facility teams to optimize coolant flow based on workload demand. As liquid cooling adoption scales, operators will likely favor integrated manifold systems that connect with CDU controls, building management systems and data center infrastructure management platforms.

Market Challenges

Leakage Risk, Reliability Concerns And Qualification Complexity

Leak prevention remains one of the most important challenges for the Global Data Center Liquid Cooling Manifolds Market. Manifolds operate near high-value IT hardware, which makes reliability, sealing performance and maintenance procedures critical. Operators require strong validation across fittings, materials, pressure ratings and coolant compatibility before large-scale deployment. Even small leaks can create downtime risk, raise insurance concerns and slow enterprise adoption. Qualification can also take time because each data center may use different coolant chemistries, rack designs and service requirements. Vendors must support adoption with testing, certification, installation guidance and robust after-sales service.

Retrofit Difficulty Across Legacy Air-Cooled Facilities

Many existing data centers were built around air cooling and do not have the piping, facility water access or floor layouts needed for large-scale liquid cooling. This creates a challenge for manifold deployment because retrofits can require changes to racks, CDUs, piping routes, leak detection, maintenance workflows and safety procedures. The Global Data Center Liquid Cooling Manifolds Market faces slower adoption in older enterprise facilities where downtime windows are limited and capital budgets are constrained. Vendors that offer compact, modular and retrofit-friendly manifold systems can reduce this barrier and capture demand from existing data center modernization programs.

Market Opportunities

Expansion Of AI-Ready Hyperscale And Colocation Facilities

AI-ready hyperscale and colocation data centers create the strongest opportunity for the Global Data Center Liquid Cooling Manifolds Market. These facilities require scalable coolant distribution systems that can support high-density server racks and future GPU upgrades. Colocation providers also need flexible manifold designs to serve different customer power densities in the same building. This creates demand for in-rack manifolds, row-based manifolds and facility-level manifolds with strong serviceability. Vendors that can deliver validated, modular and high-capacity manifold systems will gain an advantage as AI infrastructure spending continues to shift cooling design from optional upgrade to core infrastructure requirement.

Rising Demand From Emerging Markets And Sovereign Data Infrastructure Projects

Emerging markets offer a strong long-term opportunity as governments, telecom operators, cloud providers and enterprises invest in local data centers. New facilities in Asia Pacific, the Middle East, Latin America and Africa can adopt liquid cooling infrastructure earlier in the design phase, which supports manifold demand. Sovereign cloud, AI computing and digital public infrastructure programs also require reliable and energy-efficient cooling systems. Vendors can gain share by building local partnerships, offering standardized product platforms and supporting regional installation teams. This opportunity is strongest where new data centers are built for high-density workloads from the start.

Market Segmentation

By Manifold Type

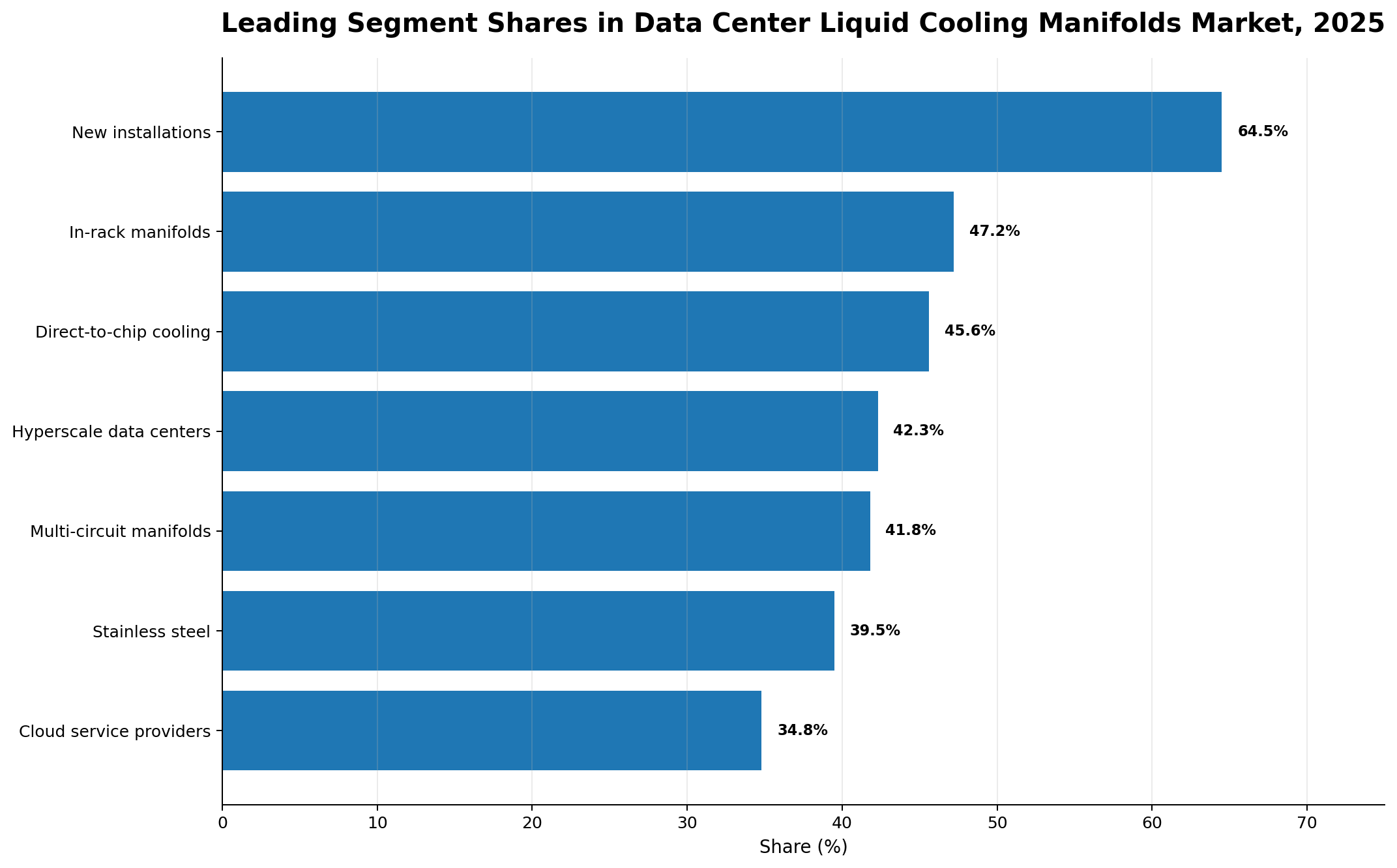

The Global Data Center Liquid Cooling Manifolds Market by manifold type includes in-rack manifolds, row-based manifolds and facility-level manifolds. In-rack manifolds led the segment with an estimated 47.2% share in 2025 because they directly support rack-level coolant distribution for direct-to-chip cooling and high-density server systems. Row-based manifolds are gaining demand in colocation and hyperscale facilities where coolant distribution needs to support multiple racks in a controlled zone. Facility-level manifolds remain important for large-scale coolant routing between CDUs, heat exchangers and data hall distribution systems. In-rack manifolds will likely remain dominant as AI servers require more precise rack-level fluid management.

By Cooling Technology

The market by cooling technology includes direct-to-chip liquid cooling, immersion cooling, single-phase immersion, two-phase immersion and hybrid liquid cooling. Direct-to-chip liquid cooling held the largest share at about 45.6% in 2025 because it offers effective heat removal near chips while allowing operators to retain rack-based infrastructure. Immersion cooling is expanding in specialized high-density and HPC environments. Single-phase immersion remains more practical for near-term deployments because it has lower operating complexity than two-phase systems. Hybrid liquid cooling is gaining traction because many facilities combine air cooling, direct-to-chip cooling and rear-door heat exchangers during phased transitions.

By End-User / Vertical

The market by end-user includes cloud service providers, AI and machine learning data centers, telecommunications, BFSI, government and defense, healthcare, manufacturing, research and academia and others. Cloud service providers dominated with an estimated 34.8% share in 2025 because they operate the largest hyperscale infrastructure estates and deploy high-density AI clusters at scale. AI and machine learning data centers represent the fastest-growing vertical because they require advanced thermal management from the design stage. Telecommunications demand is rising through edge, 5G and network workloads. BFSI, government, healthcare and research users adopt liquid cooling manifolds where uptime and system reliability are critical.

By Data Center Type

The market by data center type includes hyperscale data centers, colocation data centers, enterprise data centers, edge/micro data centers and high-performance computing data centers. Hyperscale data centers led with an estimated 42.3% share in 2025 because large cloud and AI operators deploy liquid cooling infrastructure at scale. Colocation data centers follow as providers build high-density suites for enterprise AI, cloud and HPC users. Enterprise data centers adopt liquid cooling manifolds more selectively, mainly for AI pilot zones and high-performance workloads. Edge and micro data centers use smaller systems, while HPC data centers require high-flow, high-reliability manifold designs.

By Material

The market by material includes stainless steel, copper, brass, aluminum and engineering plastics or composite materials. Stainless steel held the largest share at about 39.5% in 2025 due to its corrosion resistance, strength, cleanliness and suitability for mission-critical cooling infrastructure. Copper remains important where thermal conductivity and established cooling-system familiarity are key considerations. Brass is used in selected fittings and connector applications. Aluminum supports lightweight designs, while engineering plastics and composite materials are gaining traction due to corrosion resistance and lower weight. GF Piping Systems states that polymer piping systems for direct liquid cooling are corrosion-free, compatible with glycol-based fluids and made from recyclable materials.

By Design

The market by design includes single-circuit manifolds, multi-circuit manifolds, modular manifolds and custom engineered manifolds. Multi-circuit manifolds led with an estimated 41.8% share in 2025 because high-density racks and rows require controlled distribution across multiple coolant branches. Modular manifolds are expected to grow strongly because operators need scalable designs that support phased deployment and easier maintenance. Single-circuit manifolds remain relevant in smaller or simpler liquid cooling loops. Custom engineered manifolds hold demand in advanced AI, HPC and research environments where rack layouts, pressure requirements and coolant chemistry require tailored engineering.

By Installation

The market by installation includes new installations and retrofit installations. New installations, or greenfield projects, accounted for an estimated 64.5% share in 2025 because new AI-ready facilities can integrate manifolds, piping, CDUs and monitoring systems into the original design. This lowers installation complexity and supports higher rack densities. Retrofit installations remain important because many existing colocation and enterprise facilities must upgrade to support AI workloads. Retrofit demand will rise over the forecast period as operators seek to extend facility life while adding liquid-cooled zones. Suppliers with compact, pre-tested and service-friendly manifold systems can capture stronger retrofit demand.

Regional Insights

North America And Europe Maintain Leadership Through Hyperscale AI Investment And Early Liquid Cooling Adoption

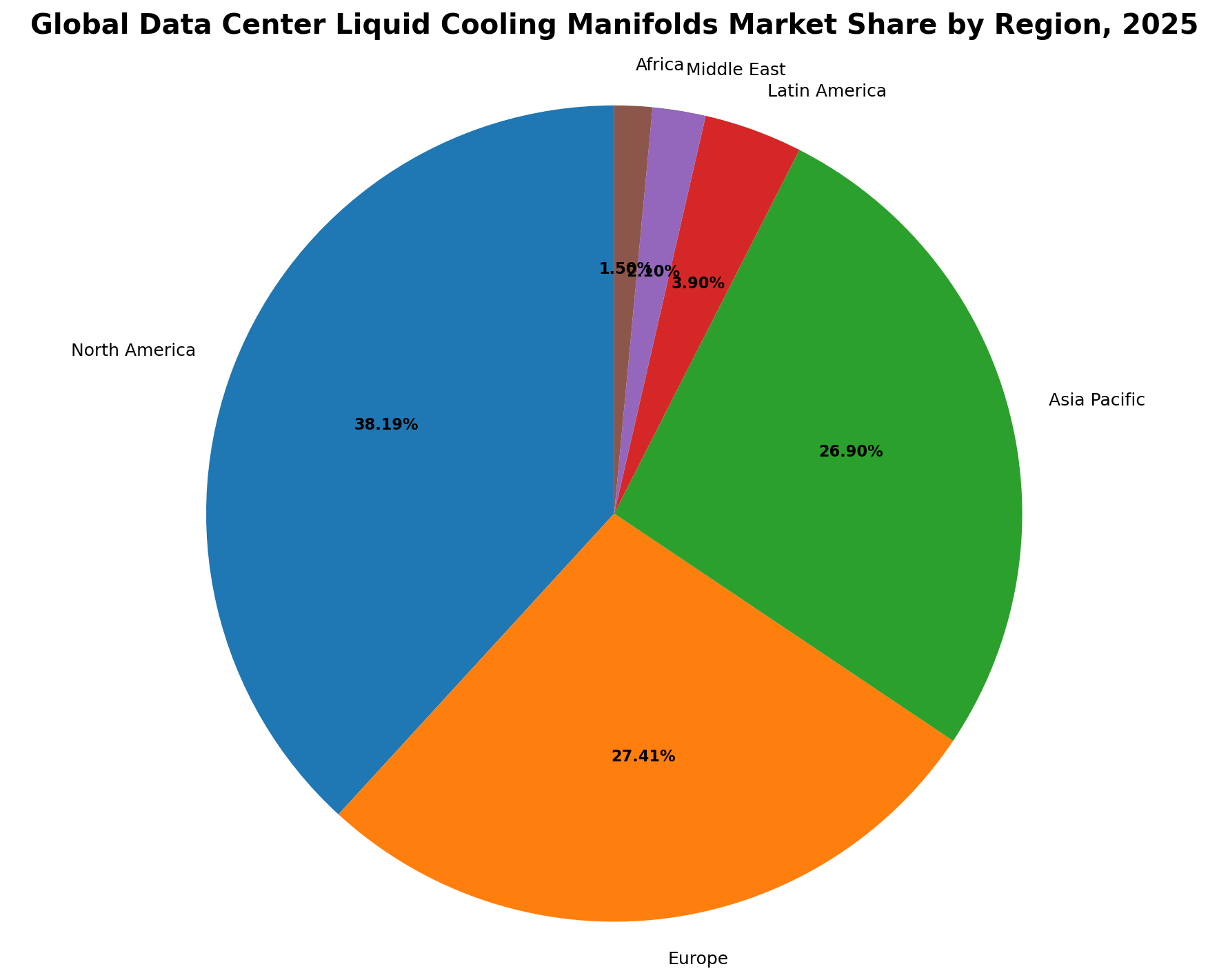

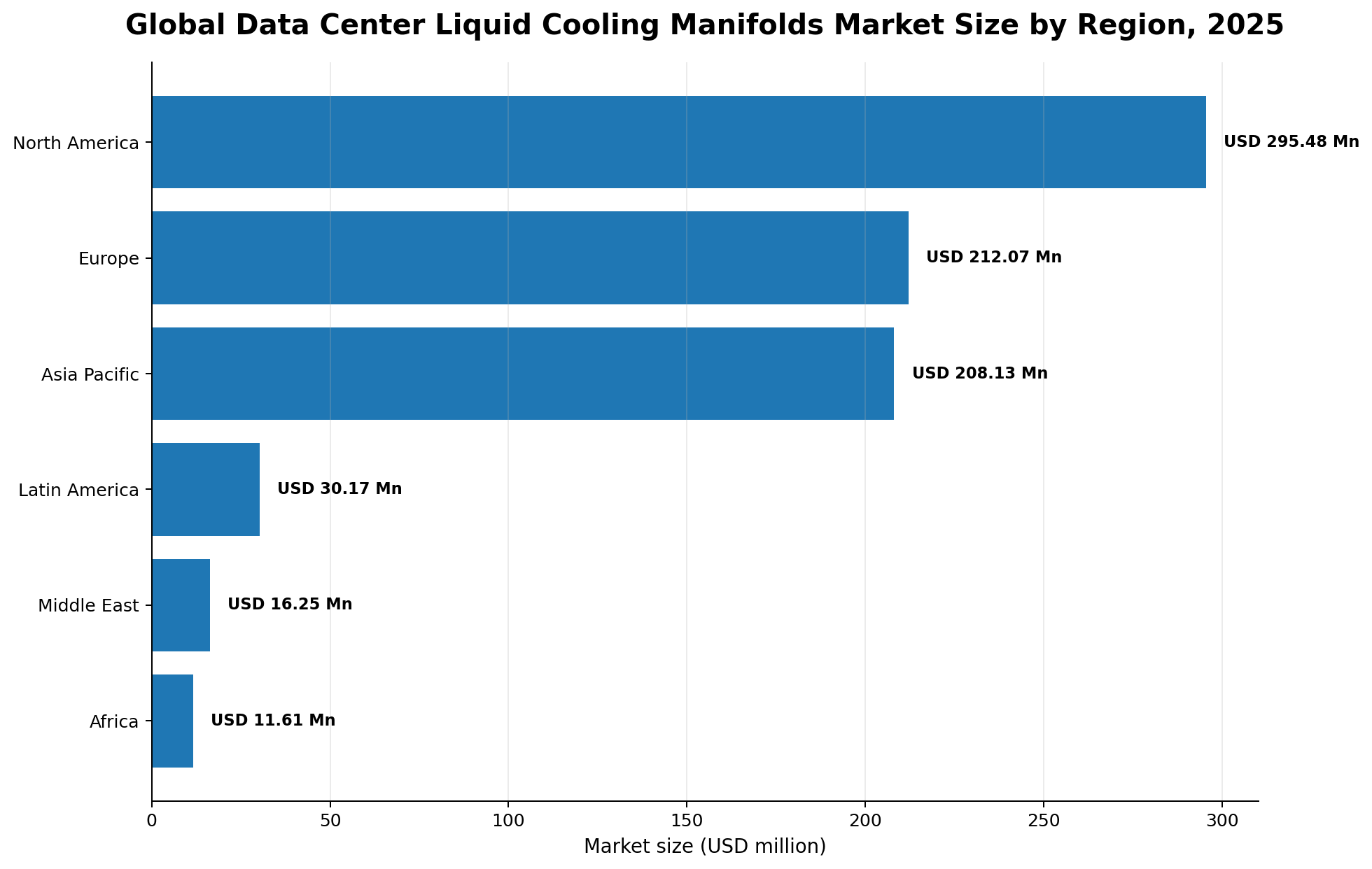

North America led the Global Data Center Liquid Cooling Manifolds Market with USD 295.48 million in 2025, accounting for 38.19% share. The United States remains the largest revenue contributor due to major cloud service providers, rapid AI infrastructure deployment and strong adoption of direct-to-chip liquid cooling. Canada adds demand through colocation, research computing and enterprise modernization, while Mexico shows gradual progress through telecom and cloud expansion. Europe held USD 212.07 million in 2025, representing 27.41% share. The region benefits from strong demand across Germany, the UK, France, the Nordics, Italy and Spain. Energy efficiency rules, high electricity costs and strong sustainability expectations support wider liquid cooling adoption in mature European data center markets.

For instance, Schneider Electric said its Motivair CDU technology enables thermal performance for six of the world’s top 10 supercomputers and is certified for NVIDIA’s latest hardware, underscoring the scale of liquid cooling infrastructure now used in advanced computing environments.

Asia Pacific Emerges As A High-Growth Region With Strong Cloud, AI And Manufacturing Demand

Asia Pacific accounted for USD 208.13 million in 2025, equal to 26.90% share of the Global Data Center Liquid Cooling Manifolds Market. China, Japan, South Korea and India remain major demand centers due to cloud growth, AI investment, semiconductor manufacturing and expanding digital infrastructure. Southeast Asia is also gaining momentum as Singapore, Malaysia, Indonesia and Thailand attract hyperscale and colocation projects. The region benefits from greenfield data center construction, which allows operators to integrate liquid cooling manifolds, CDUs and facility distribution systems from the start. Delta Electronics, GF Piping Systems and other regional suppliers also strengthen the supply ecosystem for high-density data center cooling.

For instance, GF Piping Systems said it presented direct liquid cooling solutions for AI next-generation data centers at Data Centre World London in 2025, reflecting stronger supplier focus on liquid cooling infrastructure for high-density AI data centers.

Latin America, The Middle East And Africa Gain Ground Through Cloud Expansion And Sovereign Digital Infrastructure

Latin America generated USD 30.17 million in 2025, accounting for 3.90% share, with Brazil and Mexico representing the main demand centers. The Middle East reached USD 16.25 million in 2025, or 2.10% share, supported by sovereign cloud investments, AI initiatives, smart city programs and hyperscale partnerships across GCC countries. Africa held USD 11.61 million in 2025, equal to 1.50% share, with South Africa leading adoption through colocation and financial sector digitization. These regions remain smaller in market value, but they offer long-term opportunities as new data centers adopt liquid cooling infrastructure to manage higher-density workloads and improve energy efficiency.

Competitive Insights:

- CoolIT Systems

- Vertiv

- Parker Hannifin

- nVent

- GF Industry & Infrastructure Flow Solutions

- Schneider Electric

- Boyd

- Accelsius

- Chilldyne

- JetCool Technologies

- Delta Electronics

- DCX Liquid Cooling Systems

- Hanley Controls

- Valex

- Steel & O’Brien Manufacturing

The Global Data Center Liquid Cooling Manifolds Market features strong competition among liquid cooling system providers, flow-control specialists, thermal management vendors and precision component manufacturers. CoolIT Systems, Vertiv, Schneider Electric, Boyd, Accelsius, Chilldyne and JetCool Technologies compete through direct-to-chip cooling platforms, CDUs, cold plates, rack manifolds and integrated thermal systems. Parker Hannifin, GF Industry & Infrastructure Flow Solutions, Valex, Hanley Controls and Steel & O’Brien Manufacturing compete through fittings, tubing, valves, stainless steel assemblies, polymer flow systems and custom engineered manifolds. nVent and Delta Electronics strengthen competition through data center infrastructure, rack systems and liquid cooling solutions. CoolIT Systems lists rack manifolds among its liquid cooling products for HPC, AI and enterprise systems, highlighting the importance of manifolds within complete cooling platforms.

Recent Developments:

- In March 2025, GF Piping Systems announced that it would present direct liquid cooling solutions for AI next-generation data centers at Data Centre World London, strengthening its positioning in mission-critical cooling infrastructure for high-density environments.

- In September 2025, Schneider Electric unveiled a liquid cooling portfolio with Motivair featuring solutions and services for HPC and AI workloads. The company said Motivair’s CDU technology supports six of the world’s top 10 supercomputers and is certified for NVIDIA’s latest hardware.

- In November 2025, nVent Electric unveiled liquid cooling solutions for data centers, including enhanced CDU offerings with row and rack-based designs and technology cooling system manifolds.

- In November 2025, Vertiv announced it would acquire PurgeRite for about USD 1 billion to expand its liquid cooling services portfolio, reflecting rising demand for efficient cooling systems in AI data centers.

- In January 2026, JetCool Technologies published guidance describing a liquid manifold as a central hub for coolant distribution in data center liquid cooling systems, highlighting its role in reliable and balanced liquid delivery.

- In March 2026, Ecolab announced it would acquire CoolIT Systems from KKR for about USD 4.75 billion in cash to strengthen its position in AI data center liquid cooling.