Executive summary:

Market Insight

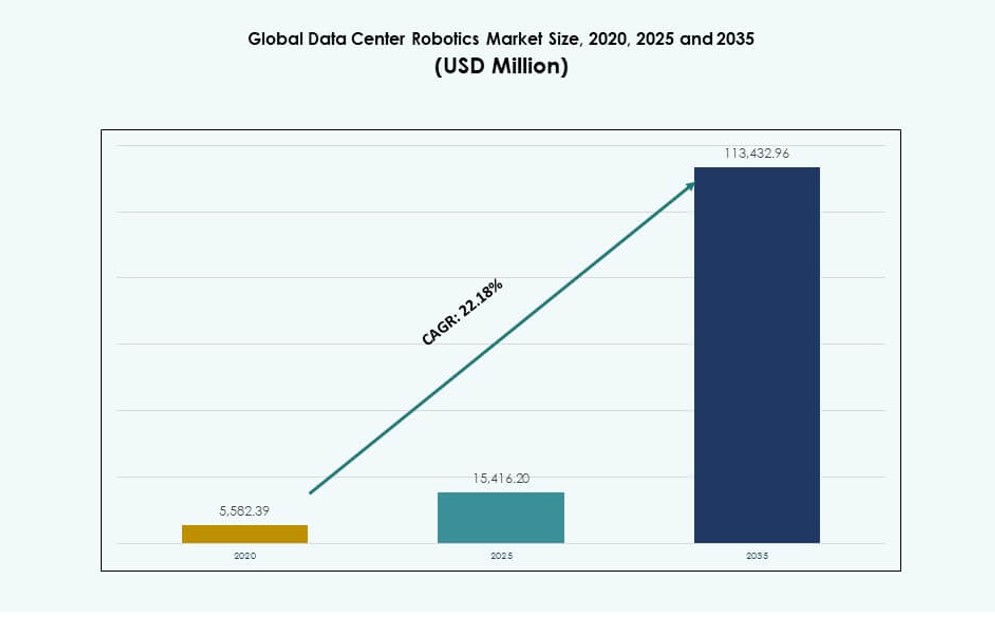

The Global Data Center Robotics Market size was valued at USD 5,582.39 million in 2020 to USD 15,416.20 million in 2025 and is anticipated to reach USD 113,432.96 million by 2035, at a CAGR of 22.18% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2035 |

| Data Center Robotics Market Size 2025 |

USD 15,416.20 Million |

| Data Center Robotics Market, CAGR |

22.18% |

| Data Center Robotics Market Size 2035 |

USD 113,432.96 Million |

Data center operators adopt robotics to raise uptime, cut manual error, and improve safety in high-density facilities. It supports automated inspection, asset movement, and routine maintenance that aligns with higher rack power, liquid cooling, and tighter service-level expectations. Innovation in sensing, autonomy, digital twins, and AI-based diagnostics boosts task accuracy and response speed. Businesses gain labor efficiency and resiliency, while investors track it as a scalable enabler of next-generation infrastructure operations.

North America leads due to hyperscale buildouts, advanced automation budgets, and strong robotics ecosystems. Europe follows with structured compliance, energy-efficiency priorities, and growing colocation demand. Asia Pacific emerges fast as cloud expansion accelerates across China, India, and Southeast Asia, where new facilities can design for automation from day one. Latin America, the Middle East, and Africa show earlier adoption, driven by new builds, telecom upgrades, and selective enterprise modernization in major metros.

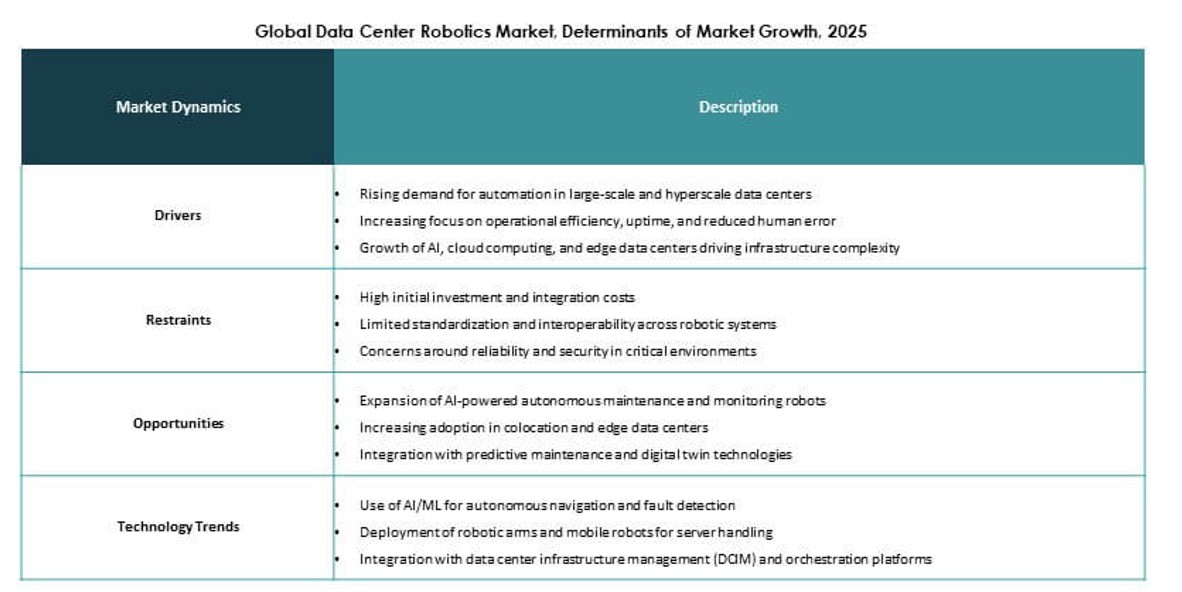

Market Dynamics

Market Drivers

Hyperscale Expansion Forces Automation-First Operations Across Critical Infrastructure

The Global Data Center Robotics Market grows as hyperscale operators expand campuses and push for repeatable operating models. Operators seek higher availability with fewer manual interventions in critical spaces. Robotics supports routine inspections, alarm verification, and rapid response to prevent minor faults from escalating. It reduces human exposure to hot aisles, battery rooms, and high-voltage zones. Standard workflows improve service quality across sites. Procurement favors solutions that integrate with facility management and DCIM systems. Vendors win by proving reliability and clear performance KPIs. Investors view this driver as a durable demand base tied to cloud growth.

- For instance, Boston Dynamics’ published Spot specifications show up to 90 minutes of runtime, payload capacity up to 14 kg, and top speed of 1.6 m/s, which supports standardized inspection rounds across large multi-building data center campuses.

Rising Rack Density And Cooling Complexity Drive Need For Precision Maintenance

The Global Data Center Robotics Market benefits from higher rack power and advanced cooling architectures. Dense deployments tighten tolerances for temperature, airflow, and leak detection. Robots equipped with thermal cameras, acoustic sensors, and environmental probes can patrol at a cadence that teams cannot match. It helps identify hotspots, obstructions, and early signs of component stress. Automated reporting speeds root-cause analysis and supports preventative maintenance. Operators also value repeatable data capture for audit and trend analysis. Solution providers differentiate through sensor fusion and actionable analytics. This shift raises strategic value for firms that manage high-performance compute estates.

Labor Constraints And Safety Requirements Increase ROI For Robotic Task Execution

The Global Data Center Robotics Market advances due to shortages in skilled technicians and rising labor costs in major hubs. Operators must cover 24/7 operations, yet staffing models face pressure. Robotics handles predictable tasks, which frees experts for higher-value work. It strengthens safety compliance by reducing exposure to confined spaces and heavy lifting. Consistent task execution lowers risk of outage from procedural drift. Enterprises also use it to standardize training and reduce onboarding time. Providers that package robots with managed services simplify adoption for buyers. Investors track margin improvement and recurring service revenue tied to this driver.

- For instance, ANYbotics’ ANYmal X is certified for ATEX and IECEx Zone 1hazardous areas, carries payloads up to 10 kg, and operates for about 90minutes per battery cycle, which highlights how autonomous inspection can reduce technician exposure in battery, power, and other high-risk utility spaces.

Security, Compliance, And Audit Pressure Push Continuous Monitoring At Scale

The Global Data Center Robotics Market gains momentum as customers demand stronger physical security and documented controls. Continuous patrol and automated evidence capture support compliance expectations in regulated industries. Robots can validate access zones, detect open cabinets, and monitor environmental thresholds. It also supports chain-of-custody workflows for hardware movement within secure areas. Operators want tools that produce searchable logs and integrate with SOC processes. Strong cybersecurity design and secure update paths influence vendor selection. This driver elevates solutions with enterprise-grade identity, encryption, and lifecycle management. Businesses see it as a differentiator in premium colocation and regulated workloads.

Market Trends

Autonomy Paired With AI-Based Condition Intelligence Replaces Basic Remote Telepresence

The Global Data Center Robotics Market shifts from simple camera-on-wheels devices toward autonomous systems with embedded intelligence. Buyers expect robots to navigate complex aisles, avoid obstacles, and self-dock for charging. AI supports anomaly detection for heat, noise, vibration, and visual cues. Operators value alerts that prioritize risk and recommend actions. Vendors increasingly bundle analytics with the robot and a cloud control plane. Feature roadmaps emphasize reliability, fleet management, and audit-grade reporting. Partnerships with DCIM and BMS platforms accelerate deployment. This trend favors suppliers that prove low false alarms and strong operational uptime.

Fleet Management And Robotics-As-A-Service Models Gain Share In Buying Decisions

The Global Data Center Robotics Market sees procurement shift toward subscription models that lower upfront cost and speed adoption. Robotics-as-a-service aligns expenses with operating budgets and site expansion plans. Providers include maintenance, software updates, and remote monitoring under one contract. Buyers prefer SLAs that specify coverage, response times, and device availability. Multi-site fleet dashboards support consistent operations across regions. Service-led models also reduce internal skill barriers for configuration and tuning. Vendors compete on deployment speed and measurable outcomes. This trend supports recurring revenue and improves visibility for investors.

Integration With Digital Twins And Automated Work Orders Becomes A Standard Expectation

The Global Data Center Robotics Market trends toward tighter integration with digital twins, ticketing, and maintenance workflows. Robots feed structured data into models that simulate thermal and power behavior. Automated work orders trigger when sensors detect drift beyond thresholds. This reduces time from detection to resolution. Operators also use historical robot data for capacity planning and risk forecasting. Vendors build connectors for ITSM tools and facility systems to reduce integration friction. Deployment success now depends on workflow fit, not just hardware capability. The trend rewards platforms that offer APIs and proven integrations.

Specialized Robots Emerge For Cable Management, Inventory, And Micro-Repair Tasks

The Global Data Center Robotics Market expands beyond inspection into niche task automation. New designs target inventory scans, barcode and RFID tracking, and cage-level audits. Some solutions focus on assisted cable routing and guided installation support. Mobile manipulators and end-effectors broaden use cases where small physical actions matter. Operators evaluate these tools for speed, accuracy, and reduced rework. Vendors prioritize modular attachments and safety features for shared spaces. Buyers demand minimal disruption to live operations. This trend signals a move toward higher-value robotic labor inside facilities.

Market Challenges

Complex Facility Layouts And Operational Constraints Limit Rapid, Uniform Deployments

The Global Data Center Robotics Market faces hurdles because many sites were not built with robotics in mind. Narrow aisles, mixed flooring, and changing obstructions complicate navigation. Security zones and restricted access require careful route planning and permissions. Live operations limit testing windows and slow rollout. Edge cases such as reflective surfaces and low lighting can reduce sensor confidence. Operators also vary in workflow maturity across sites. Vendors must tune systems per facility, which raises deployment cost. Buyers demand proof of stable performance before scaling. This challenge favors suppliers with strong site assessment and commissioning playbooks.

Integration Burden, Cyber Risk, And Reliability Expectations Raise Adoption Barriers

The Global Data Center Robotics Market must address strict reliability demands because failures can disrupt critical operations. Integration with DCIM, BMS, ticketing, and security systems often requires custom work. Cybersecurity review cycles delay procurement and increase documentation needs. Patch management and secure remote access require disciplined governance. Robotics hardware also needs ruggedization for continuous operation and safe interaction with staff. Maintenance logistics across multi-site fleets add complexity. Buyers scrutinize vendor viability and long-term support. Overcoming this challenge requires mature software, strong security posture, and clear lifecycle commitments.

Market Opportunities

Brownfield Retrofitting Packages Create A Large Addressable Upgrade Cycle

The Global Data Center Robotics Market can grow through retrofit kits that adapt older facilities to automation. Buyers want navigation aids, mapping services, and workflow templates that reduce commissioning time. Sensor upgrades and edge processing can improve performance without major construction. Vendors can offer standardized “site readiness” assessments with clear remediation steps. Fleet management platforms can unify mixed hardware generations. Colocation operators can use retrofit automation to differentiate premium service tiers. This opportunity supports repeatable deployment programs across large portfolios. It also opens services revenue tied to assessments and integration.

Robotics-Enabled Sustainability And Energy Optimization Expands Value Beyond Labor Savings

The Global Data Center Robotics Market can capture demand through sustainability use cases that link monitoring to efficiency actions. Robots can detect airflow inefficiencies, cooling drift, and underutilized zones. Data feeds can support dynamic setpoint tuning and maintenance prioritization. Operators can reduce waste through earlier detection of leaks and equipment stress. Vendors can package insights with recommendations that tie to energy and uptime KPIs. Buyers value reporting that supports ESG disclosure and customer audits. This opportunity aligns with regulatory pressure and energy cost volatility. It can expand budgets beyond operations into sustainability programs.

Market Segmentation

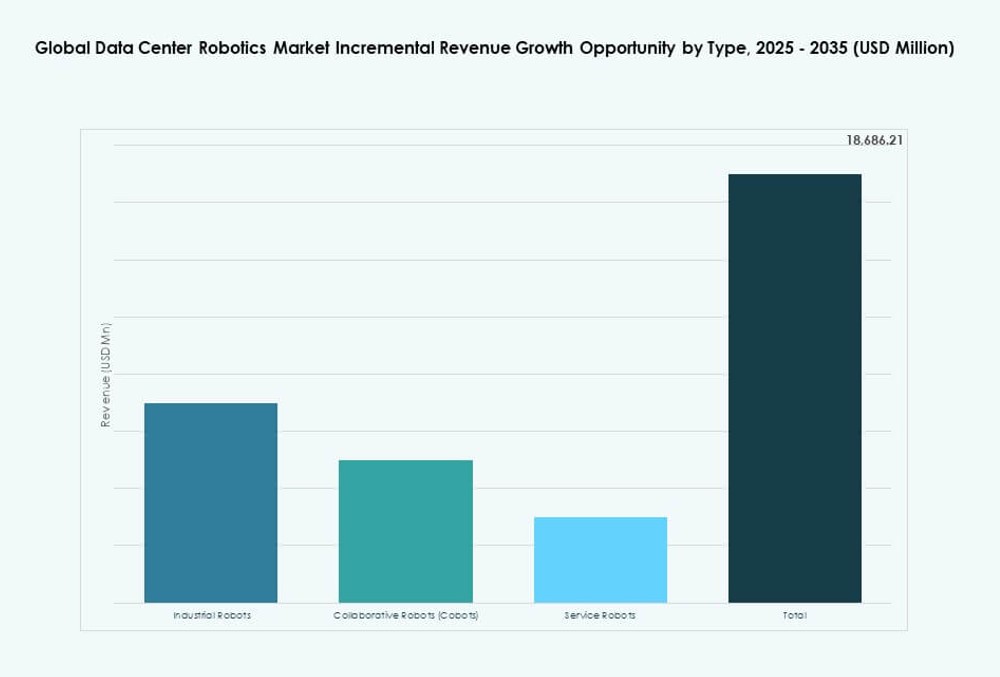

By Robot Type

The Global Data Center Robotics Market segments by industrial robots, collaborative robots, and service robots, with service robots holding the dominant share in most deployments. Buyers prefer mobile service robots for inspection, surveillance, environmental sensing, and remote verification tasks because they fit live operational constraints. Cobots gain traction in controlled maintenance zones where staff need assisted handling and repeatable procedures. Industrial robots remain more niche, mainly for structured automation in staging areas and specialized tasks. Growth rises where vendors offer autonomy, safe navigation, and fleet tools that scale across multi-site portfolios.

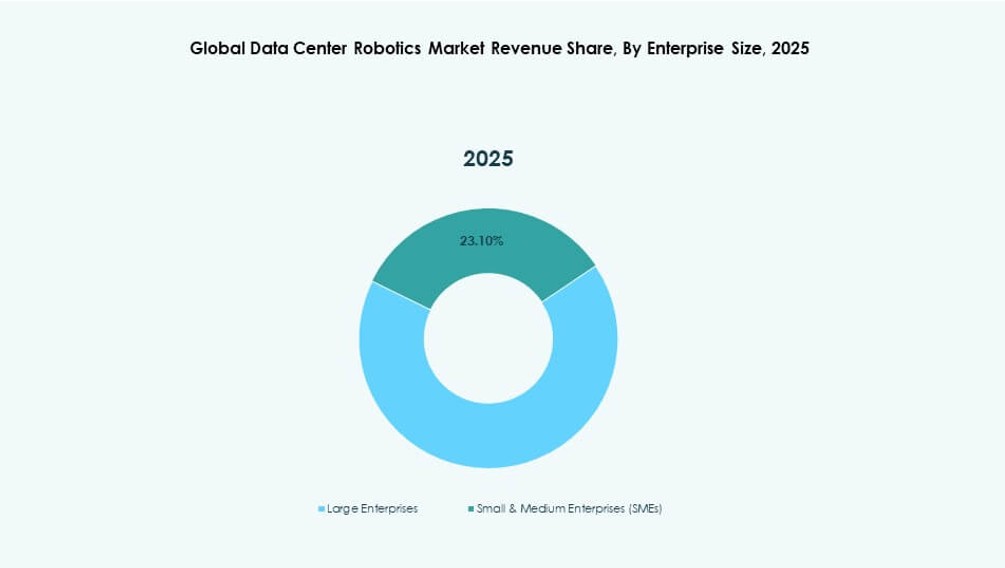

By Enterprise Size

The Global Data Center Robotics Market shows large enterprises as the leading segment due to hyperscale footprints, standardized operating models, and higher automation budgets. Large operators deploy fleets across campuses and measure ROI through uptime, labor optimization, and faster incident response. SMEs adopt at a smaller scale, often through managed services or subscription models that reduce upfront cost and complexity. SMEs also focus on quick-win use cases such as inspection rounds and security patrol. Growth accelerates as RaaS packages simplify procurement and as integration templates reduce deployment time for smaller teams.

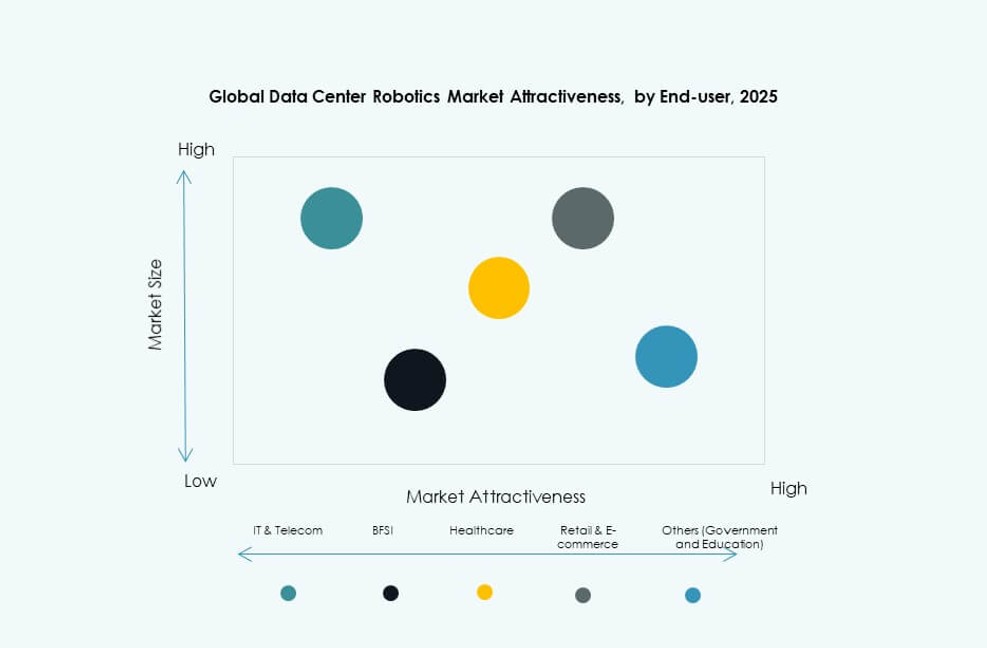

By End-User / Vertical

The Global Data Center Robotics Market is led by IT and telecom due to continuous network uptime requirements and heavy use of colocation and edge facilities. BFSI and healthcare drive adoption through compliance, audit needs, and strong security controls around sensitive workloads. Retail and e-commerce adopt to support peak-season resiliency and logistics-driven compute demand. Government use rises where secure facilities require documented physical controls. Education remains smaller but grows with research compute and campus data centers. “Others” includes energy and industrial firms that run private data centers and seek predictable operations.

By Component

The Global Data Center Robotics Market segments into hardware, software, and services, with software and services taking a growing share as buyers prioritize outcomes over devices. Hardware includes robots, sensors, docking stations, and ruggedized components. Software covers autonomy, fleet orchestration, analytics, and integrations with DCIM and security systems. Services include site mapping, commissioning, maintenance, remote monitoring, and workflow optimization. Growth comes from packaged solutions that reduce time to value and support multi-site rollouts. Vendors that combine robust software with responsive service networks improve retention and expand recurring revenue.

By Deployment

The Global Data Center Robotics Market splits into cloud-based and on-premises deployments, with hybrid approaches common due to security and latency needs. Cloud-based platforms lead in fleet management, analytics updates, and multi-site visibility, especially for operators with distributed portfolios. On-premises deployments remain critical for regulated environments and facilities with strict data residency rules. Buyers evaluate deployment models based on cyber risk, integration ease, and operational governance. Growth increases as vendors offer secure, segmented architectures and support offline operations when connectivity is limited. Deployment choice often tracks customer maturity and regulatory exposure.

Regional Insights

North America (40.05%)

The Global Data Center Robotics Market is led by North America due to hyperscale concentration, mature automation practices, and deep vendor ecosystems. Operators deploy robotics to standardize operations across large campuses and meet strict uptime targets. Strong investment in AI infrastructure raises demand for continuous monitoring and precision maintenance. Buyers also expect tight integration with security and facility systems, which supports platform-led vendors. The U.S. leads adoption, while Canada and Mexico expand with colocation growth and regional cloud zones.

- For instance, U.S.-based Boston Dynamics states that its Spot robot has more than 1,500 units in customer hands, supports payloads up to 14 kg, and delivers about 90 minutes of average runtime, highlighting the region’s readiness for scalable robotic inspection across large data center estates.

Europe (28.15%)

The Global Data Center Robotics Market holds a strong position in Europe, supported by compliance rigor and energy-efficiency focus. Colocation providers adopt robotics to differentiate service quality and strengthen audit readiness for regulated customers. Major markets such as the UK, Germany, France, and the Netherlands lead due to dense data center clusters and structured procurement. Operators prioritize safety, documentation, and repeatable processes, which aligns with robotic inspection and monitoring. Adoption expands in Southern and Eastern Europe as new builds increase and operators seek lean operating models.

- For instance, at Digital Realty’s Zurich site, ANYbotics reports that ANYmal performs 9 inspection missions daily, monitors up to 70 elements per mission, and runs 2-hour inspection cycles with docking-based recharging for 24/7 operability, demonstrating measurable automation in European colocation environments.

Asia Pacific (23.10%), Latin America (4.78%), Middle East (2.10%), Africa (1.82%)

The Global Data Center Robotics Market sees Asia Pacific as the fastest-emerging region, led by China, Japan, South Korea, India, and Southeast Asia due to rapid cloud expansion and greenfield builds that can embed automation. Buyers seek scalable operations across distributed metros and edge nodes. Latin America grows from Brazil, Mexico, Chile, and Colombia as colocation investment rises and operators modernize processes. The Middle East advances through UAE and KSA megaprojects and sovereign cloud programs. Africa remains early-stage, with adoption concentrated in South Africa and emerging hubs where new capacity drives modernization.

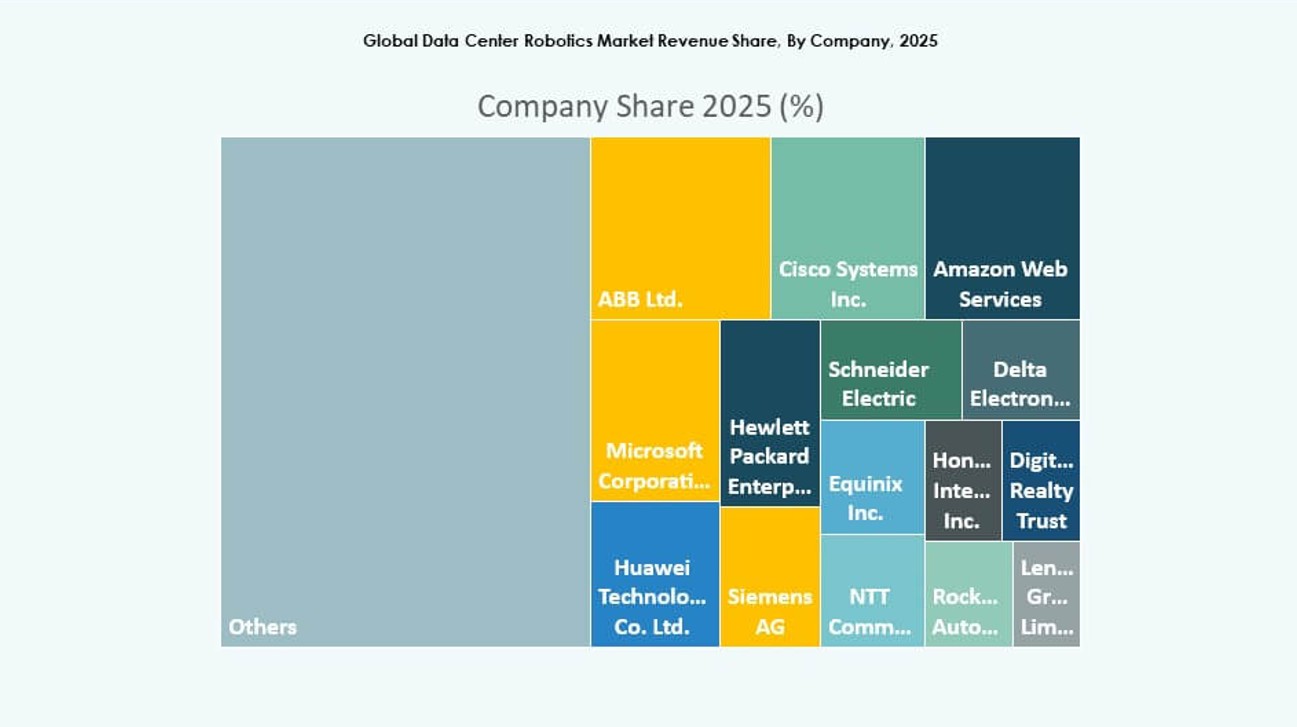

Competitive Insights:

- ABB Ltd.

- Schneider Electric

- Siemens AG

- Honeywell International Inc.

- Rockwell Automation

- Cisco Systems Inc.

- Hewlett Packard Enterprise

- Huawei Technologies Co. Ltd.

- Microsoft Corporation

- Amazon Web Services

Competition in the Global Data Center Robotics Market centers on platform depth, site integration, and service reliability. Large automation vendors position robotics as part of broader power, cooling, and building management portfolios, which helps them win enterprise rollouts with standardized workflows. Cloud and infrastructure providers push software control planes, AI diagnostics, and ecosystem partnerships that improve fleet orchestration and remote operations. Differentiation depends on autonomy performance in dense aisles, sensor quality for thermal and environmental checks, and cybersecurity controls that pass strict customer reviews. Vendors also compete on deployment speed through repeatable commissioning methods and prebuilt connectors to DCIM, BMS, and ITSM tools. Service-led models and outcome-based SLAs influence deal selection and renewals.

Recent Developments:

- In January 2026, DEWALT, a Stanley Black & Decker brand, announced with August Robotics the launch of the world’s first downward-drilling, fleet-capable robot designed to accelerate data center construction. The companies said the robot had already been used in pilot work across 10 data center projects and is expected to become commercially available in mid-2026.

- In March 2026, Hyperscale Data launched Omnipresent Robotics as a wholly owned subsidiary for U.S. commercial rollout. The company said its Michigan data center and access to NVIDIA GPU infrastructure could support future robotics operations, and it also signaled that additional partnerships across the robotics ecosystem were expected.

- In March 2026, NVIDIA announced its Physical AI Data Factory Blueprint, a new open reference architecture created to accelerate robotics, vision AI agents, and autonomous vehicle development. NVIDIA said Microsoft Azure and Nebius were the first cloud platforms to offer the blueprint, while companies including FieldAI and Teradyne Robotics were already using it to speed robotics development.

- In March 2026, ABB entered a partnership with NVIDIA to integrate Omniverse technology into ABB’s RobotStudio platform to improve robot training accuracy between simulation and real-world deployment. ABB said the new system is scheduled for launch in the second half of 2026 and is intended to reduce costs and speed time to market for robot deployments.

- In April 2026, Agile Robots confirmed it had recently closed a deal to acquire assets from thyssenkrupp Automation Engineering in Europe and North America. The company said the acquisition combines Agile Robots’ AI-powered automation capabilities with thyssenkrupp’s long-standing engineering expertise and adds roughly 650 employees to strengthen its global automation footprint.