Executive summary:

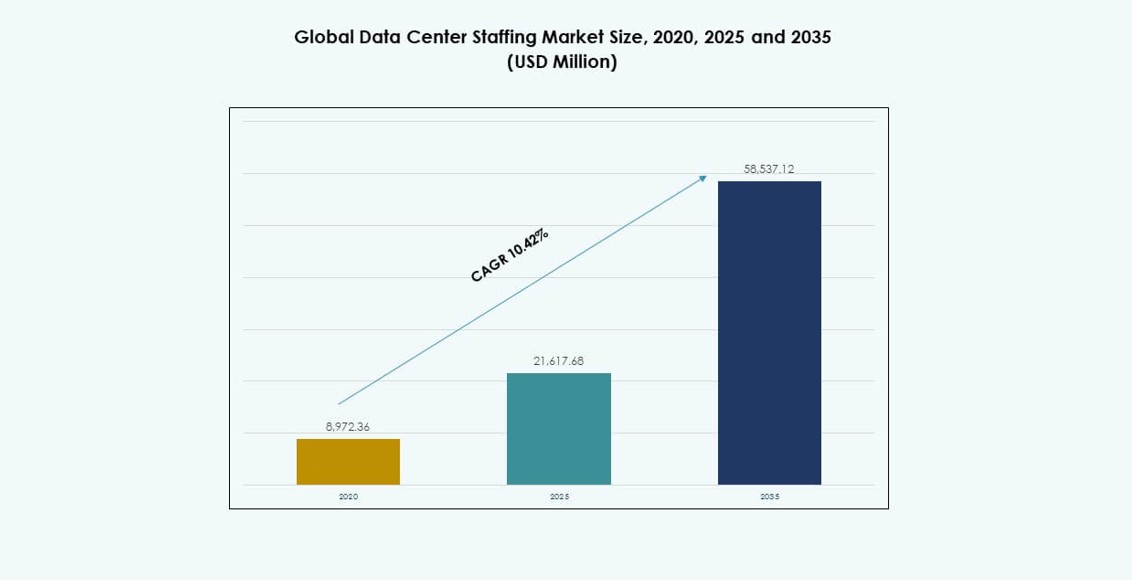

The Global Data Center Staffing Market size was valued at USD 8,972.36 million in 2020 to USD 21,617.68 million in 2025 and is anticipated to reach USD 58,537.12 million by 2035, at a CAGR of 10.42% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2035 |

| Data Center Staffing Market Size 2025 |

USD 21,617.68 Million |

| Data Center Staffing Market, CAGR |

10.42% |

| Data Center Staffing Market Size 2035 |

USD 58,537.12 Million |

It expands as hyperscale and colocation operators scale capacity and raise demand for critical facilities operations, commissioning, and construction talent. AI-ready infrastructure lifts requirements for power, cooling, controls, and safety skills, which drives specialized hiring and certification-led recruitment. Automation and digital monitoring tools reshape role profiles, increasing demand for hybrid IT-OT expertise. Businesses treat staffing as a strategic lever to protect uptime and delivery schedules, while investors track labor availability because it influences project execution and margin outcomes.

Regionally, North America leads due to deep hyperscale build pipelines, dense colocation hubs, and mature staffing ecosystems that support fast mobilization. Europe follows with strong interconnection markets and compliance-driven operations that raise demand for reliability and safety roles. Asia-Pacific emerges as the fastest growth engine, led by China, Japan, India, and Southeast Asian hubs where rapid capacity additions create sustained hiring needs. Latin America and the Middle East gain momentum as new campuses launch and local talent programs expand.

Market Dynamics:

Market Drivers

Hyperscale Expansion And Capacity Build Programs Raise Workforce Demand

The Global Data Center Staffing Market expands because hyperscale and colocation operators add sites, halls, and power capacity across major metros. It drives steady demand for engineers, technicians, and construction specialists who can meet aggressive delivery timelines. Operators raise headcount to support 24/7 uptime, higher rack density, and larger facility footprints. Firms also need talent for commissioning, handover, and early-life operations to stabilize new builds. Site portfolios spread across regions, which increases multi-location staffing needs and travel-ready teams. Developers prefer partners that provide vetted talent pools and fast mobilization. Large capex cycles create long contract durations that support predictable revenue for staffing vendors.

AI Compute, High-Density Power, And Advanced Cooling Require Specialized Skills

The Global Data Center Staffing Market grows with AI clusters that raise power draw, thermal loads, and operational complexity. It pushes operators to hire specialists in electrical distribution, high-voltage systems, and critical cooling design. Teams must manage liquid cooling rollouts, containment strategies, and tighter environmental controls. Facilities add monitoring systems, sensors, and control layers that require technicians with OT and controls expertise. Service providers seek staff who can troubleshoot mixed environments that combine legacy and next-gen infrastructure. Training needs rise because procedures change with new cooling loops, safety requirements, and maintenance regimes. Staffing firms that certify talent for these tasks gain stronger client retention.

- For instance, Google disclosed that its new +/-400 VDC architecture is designed to scale IT racks from 100 kW to 1 MW, that machine learning workloads will require more than 500 kW per rack before 2030, and that it has already deployed liquid cooling at gigawatt scale across more than 2,000 TPU Pods with about 99.999% uptime, highlighting why operators now need highly specialized power and thermal-management talent.

Cloud And Network Modernization Increases Demand For IT Infrastructure Specialists

The Global Data Center Staffing Market benefits from cloud migration, edge rollouts, and network upgrades inside facilities. It increases hiring for cloud platform skills, network engineering, storage administration, and security operations. Operators align infrastructure with software-defined control and automation tools, which raises demand for hybrid IT-OT profiles. Teams must manage cross-connect growth, interconnection services, and customer onboarding at higher volume. Colocation providers add service layers such as managed connectivity and remote hands, which raises staffing intensity per site. Employers prefer candidates with vendor certifications and practical deployment experience. Staffing partners that curate these profiles shorten hiring cycles and reduce onboarding friction.

- For instance, Digital Realty said ServiceFabric had expanded to 70 members providing more than 100 services, supported by a global footprint of 300+ facilities in 50+ metros across 25+ countries, which reflects the rising need for specialists who can handle interconnection, service orchestration, and customer onboarding at scale.

Regulatory, Safety, And Reliability Standards Push Structured Hiring And Compliance Coverage

The Global Data Center Staffing Market advances because operators face tighter safety rules, audit expectations, and customer SLA requirements. It increases demand for compliance managers, safety officers, and quality leads who enforce standard operating procedures. Firms require specialists who can manage permits, hazardous work controls, and contractor governance on active sites. Reliability programs need maintenance planners, incident managers, and shift supervisors who keep operations stable. Clients also expect clear documentation for uptime practices, testing protocols, and change control. Staffing firms that supply screened candidates with industry training reduce risk for operators.

Market Trends

Shift Toward Managed Staffing, RPO, And Outcome-Based Talent Programs

The Global Data Center Staffing Market shows a shift from ad hoc hiring to managed staffing and RPO models. Clients prefer vendors that own requisition flow, screening, and onboarding at scale. It supports consistent quality across multi-site rollouts and reduces internal HR load. Providers bundle workforce planning, skills mapping, and compliance checks into one engagement. Contracts often include service metrics such as time-to-fill, retention, and safety adherence. This trend favors firms with strong account management and standardized delivery playbooks. Buyers also seek pricing structures that align with project milestones and staffing utilization. Businesses gain cost predictability and faster mobilization across peaks. Investors favor these models because they improve revenue visibility and client stickiness.

Growth Of Certifications, Micro-Credentials, And Role-Based Skill Pathways

The Global Data Center Staffing Market trends toward formal credentials that validate operational readiness. Employers ask for role-based certification in electrical safety, critical environment operations, and network tools. It increases demand for candidates who can prove competence through testing and supervised practice. Staffing firms build training partnerships to expand supply and reduce skill mismatch. Clients also use skills frameworks to standardize job families across regions. This creates clearer wage bands and more transparent career progression. Workers respond with higher mobility across operators and service providers. Businesses benefit because certified hires reduce error rates and shorten ramp time. Investors watch credential depth because it indicates scalable labor supply.

Use Of Talent Analytics And Digital Platforms For Faster Hiring Decisions

The Global Data Center Staffing Market adopts digital tools that improve sourcing, screening, and dispatch. Clients use analytics to forecast staffing by site phase, shift pattern, and service line. It supports faster shortlists and reduces vacancy duration during build and ramp cycles. Vendors deploy digital onboarding, background checks, and compliance documentation to cut process time. Some providers use skills databases to match candidates to facility type and equipment mix. This trend raises transparency on performance, retention, and safety metrics across accounts. It also helps operators benchmark vendor outcomes and refine workforce plans. Businesses value these tools because they protect schedule and reduce hiring friction. Investors see data-driven delivery as a differentiator that lifts margins.

Rise Of Multi-Region Mobility Programs And Standardized Workforce Pods

The Global Data Center Staffing Market trends toward mobile teams that move between projects and regions. Operators build “pod” structures for commissioning, controls, and operations ramp to speed site launches. It supports consistent methods and faster knowledge transfer across new builds. Staffing vendors maintain travel-ready rosters and standardized shift rotations. Clients also favor vendors that can cover surge demand without long local recruiting cycles. This trend supports cross-border compliance support for visas, safety rules, and labor standards. It also increases demand for workforce coordinators and site logistics roles. Businesses gain agility during rapid expansion phases. Investors track mobility capacity because it reduces delivery risk across pipelines.

Market Challenges

Persistent Skill Gaps In Critical Facilities, Power Systems, And High-Density Operations

The Global Data Center Staffing Market faces a tight supply of experienced talent across critical facilities operations and high-voltage electrical roles. It limits hiring speed for operators that scale multiple sites at once. Candidates with hands-on commissioning exposure remain scarce in many regions. Wage pressure rises, which affects project budgets and operating costs for clients. Employers compete with adjacent industries such as utilities, renewables, and industrial automation. Training takes time, and it slows readiness for complex environments with liquid cooling and advanced controls. Turnover risk increases when demand spikes across the same metros. Staffing firms must invest in vetting and upskilling to protect placement quality. This challenge matters to investors because labor scarcity can delay revenue ramp and reduce margin stability.

Compliance Complexity, Security Requirements, And Project Volatility Create Delivery Risk

The Global Data Center Staffing Market operates under strict access controls, background checks, and customer-driven security policies. It raises cycle time for onboarding and constrains rapid mobilization in secure facilities. Clients also require safety documentation and adherence to site-specific work permits. Demand can swing with permit delays, power availability, and supply chain constraints for equipment. Staffing providers face bench cost risk when projects shift or pause. Contract terms often transfer schedule risk to vendors through performance metrics. Labor laws differ across countries, which complicates mobility and contractor use. Service quality can drop if vendors prioritize speed over fit during surge periods.

Market Opportunities

Build Scalable Training Pipelines And Apprenticeship Programs For New Entrants

The Global Data Center Staffing Market offers strong upside for firms that create structured training pipelines for technical roles. It supports faster conversion of adjacent-industry workers into critical facilities technicians. Providers can partner with OEMs and certification bodies to standardize curricula. Clients value these programs because they expand supply and improve retention. Vendors that link training to placement can secure multi-year contracts. It also improves safety outcomes through consistent procedures. Businesses gain a dependable talent funnel for expansion plans. Investors favor training-led models because they can lift utilization and margin.

Expand Specialized Offerings For AI Facilities, Compliance, And Commissioning Services

The Global Data Center Staffing Market creates opportunity for niche staffing in AI-ready facilities and high-density power environments. It rewards firms that supply specialists for commissioning, controls, and liquid cooling operations. Vendors can package compliance support, safety leadership, and documentation services into premium bundles. Clients pay for expertise that reduces downtime risk and protects SLA commitments. Regional expansion also opens roles in emerging hubs where local talent pools remain shallow. Vendors that build local networks early can gain share. Businesses treat specialized coverage as a competitive advantage in bids. Investors see premium skill segments as a path to higher revenue per placement.

Market Segmentation

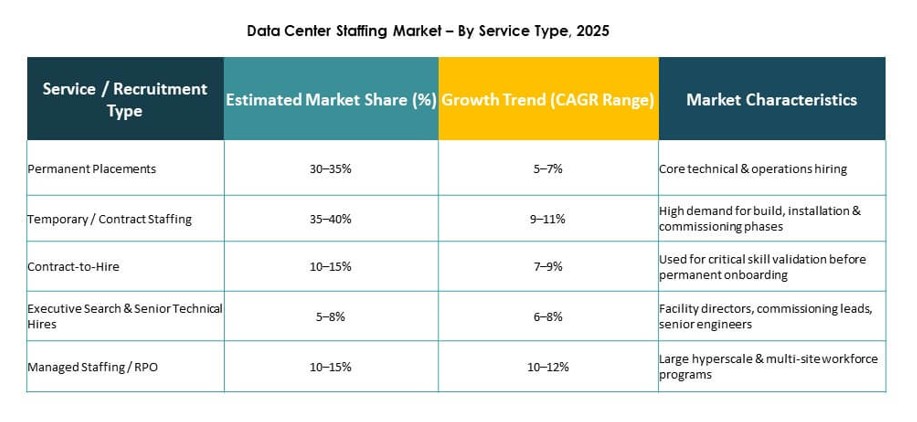

By Service Or Recruitment Type

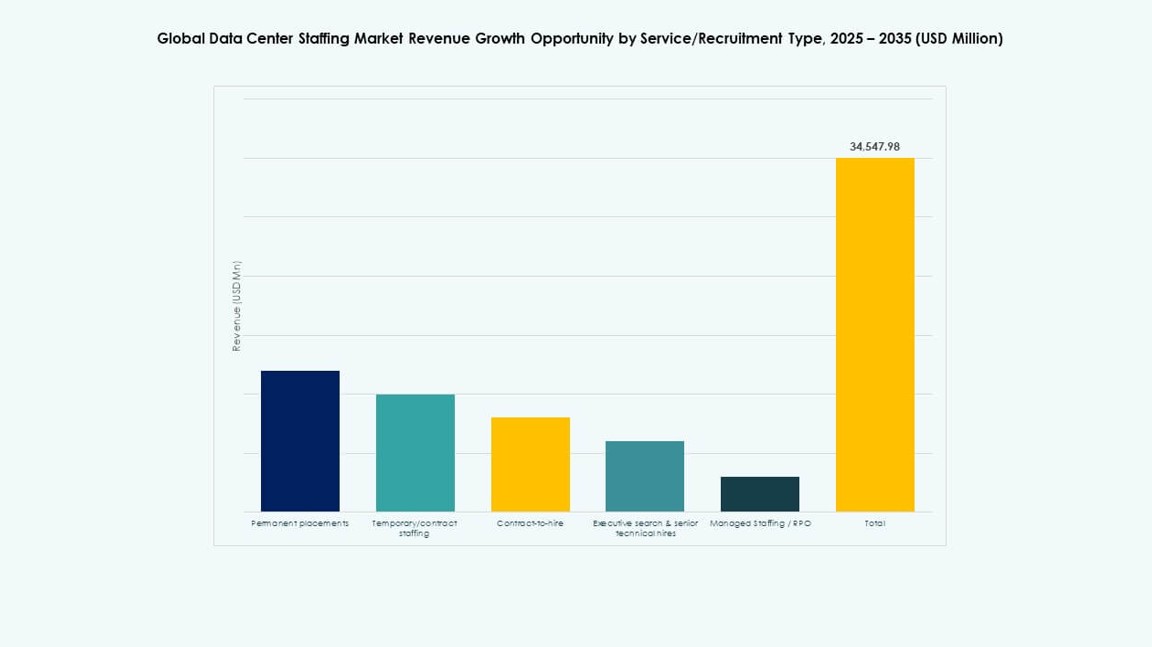

The Global Data Center Staffing Market sees permanent placements as the dominant segment at about 40–45% share because operators need stable teams for 24/7 critical operations and compliance coverage. Temporary or contract staffing holds 30–35% share due to project-based construction, commissioning, and surge needs during site ramp. Contract-to-hire contributes 10–12% share as firms test fit for high-risk roles before long-term conversion. Executive search and senior technical hires account for 6–8% share driven by leadership demand in multi-site portfolios. Managed staffing or RPO reaches 8–10% share, supported by centralized hiring programs and outcome-based vendor models.

By Role Or Skill Type

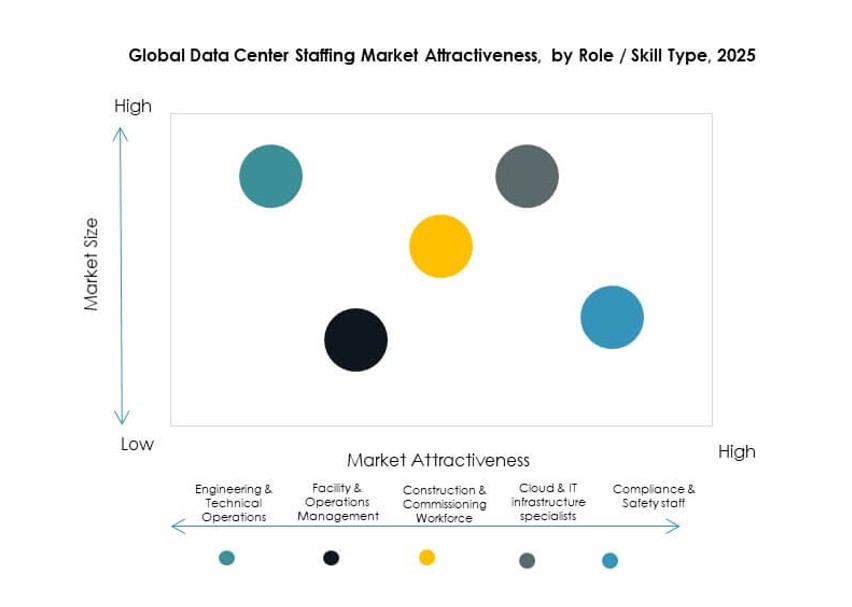

The Global Data Center Staffing Market is led by engineering and technical operations at 32–36% share due to uptime focus, power distribution work, and preventive maintenance needs. Facility and operations management holds 20–24% share because large campuses require shift leadership, reliability governance, and vendor coordination. Construction and commissioning workforce contributes 18–22% share tied to build pipelines and accelerated go-live schedules. Cloud and IT infrastructure specialists represent 14–18% share as providers expand interconnection services and managed IT layers. Compliance and safety staff takes 8–12% share driven by audit needs, safe work controls, and client security requirements.

By Vertical

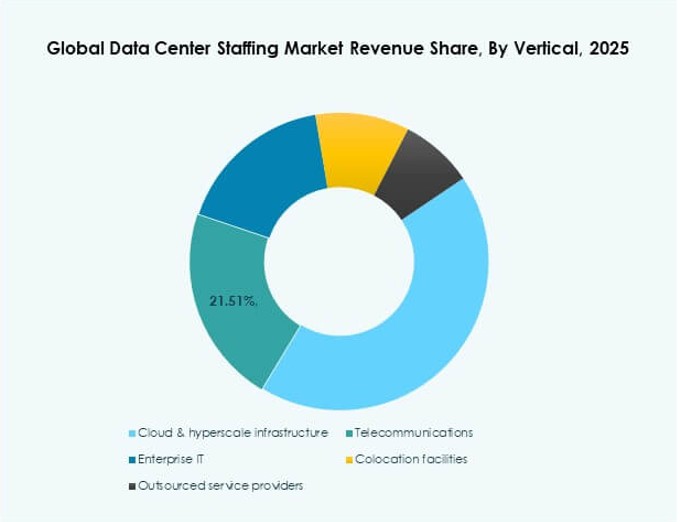

The Global Data Center Staffing Market is dominated by cloud and hyperscale infrastructure with 38–42% share due to the highest build intensity and staffing density per campus. Colocation facilities follow with 24–28% share because they scale multi-tenant operations and remote hands services across metros. Enterprise IT accounts for 14–18% share driven by modernization of private facilities and hybrid deployments. Telecommunications contributes 10–13% share through edge expansion and network upgrades inside data centers. Outsourced service providers hold 8–11% share as operators expand managed services and third-party operations support.

Regional Insights

North America And Europe Maintain Leadership Through Mature Ecosystems And Large Pipelines

The Global Data Center Staffing Market remains concentrated in North America at about 36% share due to deep hyperscale capacity, strong colocation density, and established staffing ecosystems. Europe holds around 26% share supported by expanding regional cloud zones and major interconnection hubs. It benefits from standardized operations practices and strong demand for compliance, safety, and reliability roles. Hiring intensity stays high in mature metros where capacity additions stack across multiple operators. Wage pressure remains notable in top hubs, which increases demand for managed staffing and RPO. Employers also prioritize certified talent to reduce incident risk.

- For instance, Equinix stated that its Americas xScale joint venture is expected to add more than 1.5 GW of new U.S. hyperscale capacity, while NorthC said its European buildout includes a second Frankfurt facility starting at 1.5 MW and scaling to 10.5 MW, a first Frankfurt site at 3 MW, a Berlin site launching at 3 MW with growth to 8 MW, and an additional 11 MW across Dutch locations in 2025.

Asia Pacific Expands Fast With New Hubs And Rising Need For Specialized Skills

The Global Data Center Staffing Market in Asia Pacific represents about 24% share, supported by rapid capacity build in China, Japan, India, and Southeast Asian hubs. It draws demand for construction, commissioning, and operations teams that can support accelerated schedules. Talent gaps persist in newer hubs, which raises the role of training and travel-ready teams. Operators seek hybrid IT-OT profiles to support automation and complex facility controls. Colocation growth increases needs for remote hands, customer onboarding, and interconnection support. Firms also invest in safety and compliance leadership to meet global customer expectations.

Latin America, Middle East, And Africa Offer White Space With Rising Localization Needs

The Global Data Center Staffing Market allocates about 7% share to Latin America, 5% to the Middle East, and 2% to Africa as new hubs develop and regional capacity rises. It creates demand for local talent development and vendor networks that support first-wave builds. Middle East projects often require rapid mobilization and strong compliance culture, which favors experienced staffing providers. Latin America sees increasing colocation activity that boosts operations and customer support roles. Africa remains smaller yet shows momentum in select countries where connectivity improves. Workforce localization requirements raise demand for training and certification pathways. Investors view these regions as option value markets where early presence can secure long-term accounts.

- For instance, ODATA said its QR03 campus in Querétaro is designed for up to 300 MW across five buildings, with 72 MW in the first building and 200 MW energized in phase one, while Khazna said its UAE expansion plan scales from 40 MW across three data centers to 200 MW of IT load capacity.

Competitive Insights

- Adecco Group

- Randstad NV

- ManpowerGroup

- Allegis Group

- Recruit Holdings

- Hays plc

- PERSOL Holdings

- Robert Half International

- TEKsystems Inc.

- ASGN Incorporated

The competitive landscape of the Global Data Center Staffing Market features large global staffing groups and IT-focused specialists that compete on speed, skill depth, and multi-site delivery. It rewards firms with strong client access in hyperscale and colocation accounts, plus proven ability to mobilize teams across project phases. Vendors differentiate through credential programs, compliance screening, and account-managed delivery models such as managed staffing and RPO. Scale leaders use broad talent pools and regional branch networks to reduce time-to-fill, while specialists win with deep technical screening and domain-aligned recruiting. Pricing pressure rises in high-demand hubs, which increases focus on retention and workforce planning. Consolidation and partnerships remain likely where providers seek niche skills, training assets, or geographic reach.

Recent Developments:

- In October 2025, Vertiv partnered with IIT Madras and IITM Pravartak to provide upskilling in data center operations and maintenance, with the stated goal of developing a stronger digital talent pool for India’s growing critical infrastructure sector.

- In July 2025, ManpowerGroup announced that ManpowerGroup Talent Solutions had entered a strategic partnership with Carv to embed agentic AI into recruiter workflows and speed up hiring operations.

- In March 2025, Accenture announced that it had agreed to acquire Soben, a global construction consultancy, to strengthen its capital projects capabilities, including expertise in data center development; this matters for the data center staffing market because it expands Accenture’s ability to support hyperscalers and colocation providers that need specialized project and delivery talent.

- In February 2025, Microsoft Arabia and the National IT Academy launched the first Microsoft Datacenter Academy in the Middle East in Saudi Arabia, a two-year initiative focused on building applied datacenter skills and improving employability for high-demand technical roles.