Executive summary:

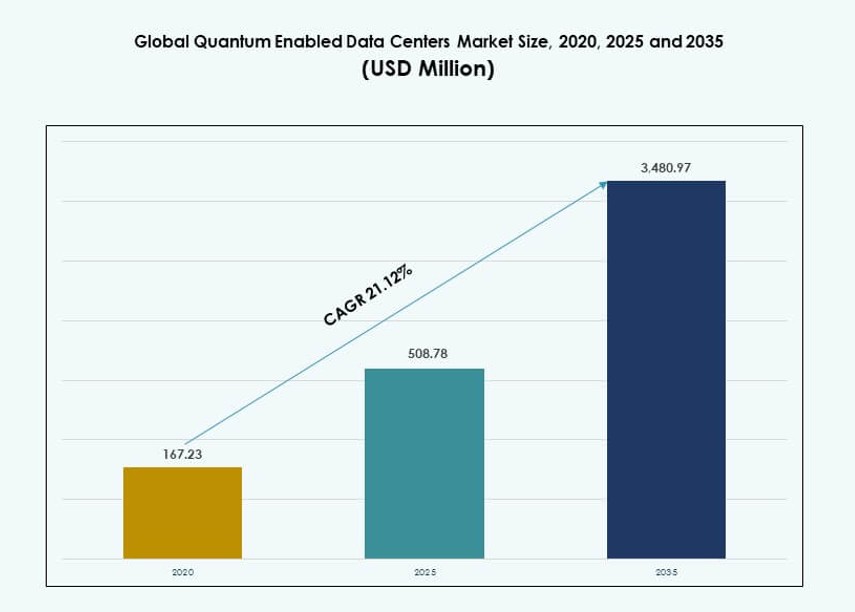

The Global Quantum Enabled Data Centers Market size was valued at USD 167.23 million in 2020, grew to USD 508.78 million in 2025, and is anticipated to reach USD 3,480.97 million by 2035, at a CAGR of 21.12% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2035 |

| Quantum Enabled Data Centers Market Size 2025 |

USD 508.78 Million |

| Quantum Enabled Data Centers Market, CAGR |

21.12% |

| Quantum Enabled Data Centers Market Size 2035 |

USD 3,480.97 Million |

Growing enterprise demand for quantum-secure infrastructure and complex compute acceleration continues to drive the market. Organizations are deploying hybrid quantum-classical systems for data encryption, scientific modeling, and machine learning. Innovation in quantum processors, post-quantum cryptography, and cloud-accessible architectures is reshaping IT strategies. Data centers are adapting to host specialized hardware, supported by increasing public and private investments. Businesses treat these developments as critical to long-term data integrity, compliance, and competitive advantage. Investors view the segment as high-impact and transformative.

North America leads market adoption, supported by early investments in quantum research, strong cloud ecosystems, and government-backed initiatives. Europe follows with emphasis on quantum security regulations and academic-industry collaboration. Asia Pacific is gaining momentum with China, Japan, and India scaling infrastructure and partnerships. The Middle East and Latin America are in early development phases, while Africa explores academic research-led participation. Regional activity aligns with funding access, technology ecosystems, and national digital priorities.

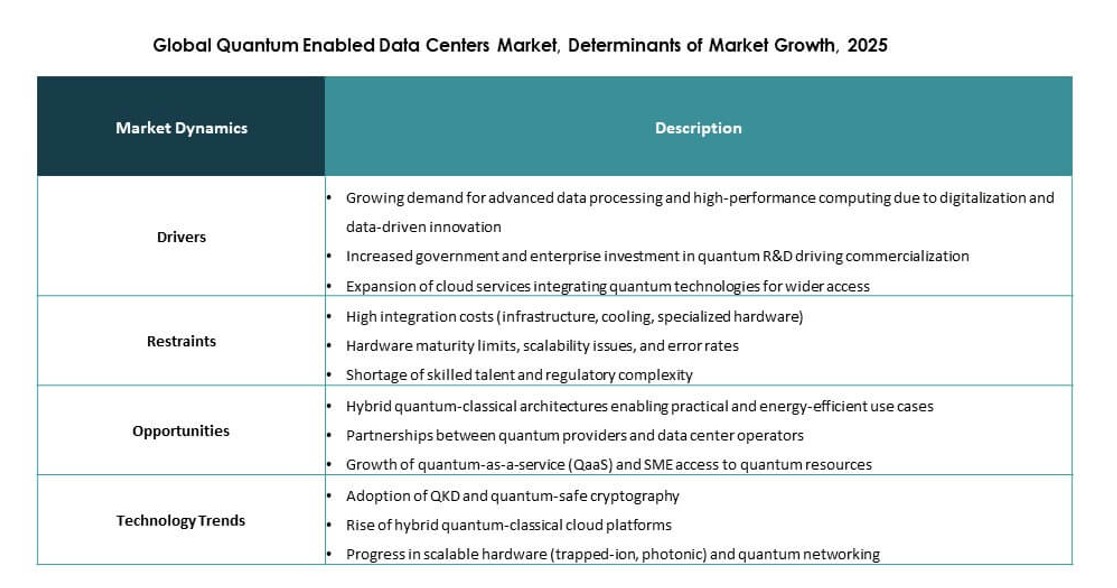

Market Dynamics:

Market Drivers:

Rising Demand For Quantum-Safe Data Security Across Critical Infrastructure

Growing concern over post-quantum cyber threats pushes enterprises to upgrade data center security models. Financial institutions, governments, and defense agencies prioritize quantum-resistant encryption. The Global Quantum Enabled Data Centers Market supports this shift through integrated cryptographic frameworks. Vendors align infrastructure with long-term data protection needs. Investment flows target secure compute environments. Businesses treat quantum readiness as a strategic safeguard. Boards link adoption with risk governance goals. Technology roadmaps now include quantum security layers.

Expansion Of Advanced Computing For Complex Enterprise Workloads

Industries seek higher compute capacity for simulation, optimization, and analytics. Quantum-enabled architectures support complex problem solving beyond classical limits. The Global Quantum Enabled Data Centers Market enables hybrid quantum-classical workflows. Enterprises use it to support research-heavy operations. Cloud providers embed quantum access within data center services. Capital allocation favors scalable compute models. Innovation cycles shorten due to faster processing capability. Investors view compute advantage as a long-term differentiator.

- For example, Google’s 53-qubit Sycamore achieved quantum supremacy in 2019 (200 seconds vs. 10,000 years on Summit supercomputer), per their Nature paper (DOI: 10.1038/s41586-019-1666-5). Scaled to 70 qubits by 2023 in subsequent upgrades for hybrid workloads.

Strong Public And Private Investment In Quantum Infrastructure Development

National programs fund quantum research and infrastructure deployment. Corporations match this effort through private capital commitments. The Global Quantum Enabled Data Centers Market benefits from aligned funding priorities. Infrastructure projects gain policy backing. Research centers partner with commercial operators. Long planning horizons attract institutional investors. Stable funding reduces adoption risk. Market confidence strengthens through visible commitment.

- For instance, the U.S. Department of Energy allocated over $625 million across five national Quantum Information Science Research Centers, including partnerships with IBM, Microsoft, and national labs, aiming to accelerate commercial quantum infrastructure development by 2030.

Integration Of Quantum Technologies Into Hyperscale And Cloud Strategies

Hyperscale operators plan quantum capability within core data centers. Service differentiation drives this integration. The Global Quantum Enabled Data Centers Market supports new service tiers. Enterprises access quantum tools through cloud platforms. Providers align infrastructure with future workloads. Strategic positioning improves competitive standing. Partnerships accelerate deployment cycles. Market entry barriers rise due to technical depth.

Market Trends:

Shift Toward Hybrid Quantum-Classical Data Center Architectures

Enterprises favor hybrid models that balance classical stability with quantum capability. This approach reduces operational risk. The Global Quantum Enabled Data Centers Market reflects this structural trend. Operators deploy modular quantum systems. Workload orchestration improves efficiency. IT teams gain flexibility in compute allocation. Vendors design interoperable platforms. Market adoption follows phased deployment strategies.

Early adopters test quantum modules alongside HPC workloads to assess performance gains under real-world conditions.

Growing Focus On Standardization And Interoperability Frameworks

Industry bodies promote shared quantum standards. Interoperability eases integration across vendors. The Global Quantum Enabled Data Centers Market aligns with these efforts. Standard protocols support scalable adoption. Buyers demand vendor-neutral solutions. Compliance requirements influence procurement decisions. Ecosystem maturity improves confidence. Technology alignment shortens deployment timelines. Collaborative initiatives like QED-C and ISO/IEC JTC 1 fuel consensus around quantum system interfaces and data formats.

Rising Use Of Specialized Cooling For Quantum Hardware Stability

Quantum systems require precise thermal control. Data centers adopt advanced cooling approaches. The Global Quantum Enabled Data Centers Market reflects design shifts. Liquid-based solutions gain attention. Operators focus on system stability. Infrastructure planning prioritizes thermal consistency. Cooling innovation supports uptime goals. Energy efficiency remains a parallel focus. Cryogenic cooling adoption accelerates for superconducting and trapped-ion systems in enterprise-grade quantum facilities.

Emergence Of Managed Quantum Data Center Services

Service providers launch managed quantum offerings. This model lowers entry barriers for enterprises. The Global Quantum Enabled Data Centers Market supports service-led adoption. Clients avoid heavy capital spend. Providers manage complexity and maintenance. Subscription models gain traction. Market demand favors flexible access. Service portfolios expand rapidly.

Major cloud platforms integrate managed quantum options into existing infrastructure-as-a-service models to boost enterprise adoption.

Market Challenges:

High Capital Requirements And Long Technology Payback Cycles

Quantum infrastructure demands significant upfront investment. Hardware, cooling, and security raise costs. The Global Quantum Enabled Data Centers Market faces adoption hesitation. Enterprises assess long-term returns carefully. Budget constraints slow deployment plans. Smaller firms struggle with scale economics. Investors evaluate extended payback periods. Financial risk management remains critical. Procurement decisions are often delayed until cost-benefit benchmarks are validated in real operational settings.

Limited Skilled Workforce And Technology Maturity Constraints

Quantum expertise remains scarce across regions. Talent gaps affect deployment and operations. The Global Quantum Enabled Data Centers Market depends on specialized skills. Training programs lag demand. System complexity increases operational risk. Enterprises rely on vendor support. Technology maturity varies across components. Adoption speed depends on workforce readiness. Global demand for quantum engineers, system architects, and cryogenics specialists continues to outpace academic output and certification pipelines.

Market Opportunities:

Commercialization Of Quantum Services For Enterprise And Research Users

Demand rises for accessible quantum computing services. Enterprises seek shared infrastructure models. The Global Quantum Enabled Data Centers Market enables service commercialization. Providers monetize quantum access. Research institutions expand usage scope. Revenue streams diversify beyond hardware. Managed services gain acceptance. Market reach broadens steadily.

Cloud-based platforms play a key role in lowering technical barriers and accelerating time-to-value for quantum applications.

Strategic Partnerships Between Data Center Operators And Quantum Firms

Collaboration accelerates market entry. Data center operators partner with quantum specialists. The Global Quantum Enabled Data Centers Market benefits from shared expertise. Joint development reduces risk. Infrastructure readiness improves faster. Partners align roadmaps. Investors favor collaborative models. Market scalability improves. These alliances often include co-location agreements, hybrid integration pilots, and joint innovation labs targeting vertical-specific use cases.

Market Segmentation:

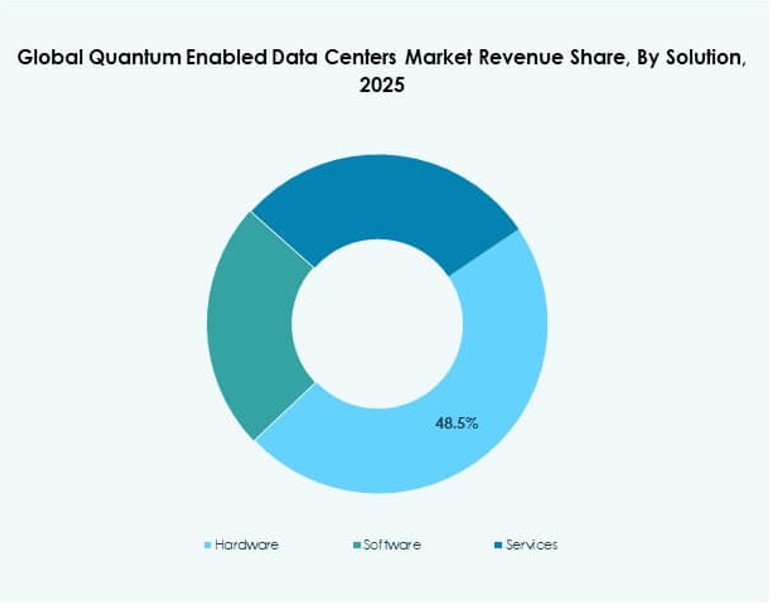

By Solution

Hardware dominates due to core quantum processors, control systems, and supporting infrastructure. The Global Quantum Enabled Data Centers Market shows strong demand for integrated hardware stacks. Software follows with orchestration, security, and workload management platforms. Services grow steadily through consulting, deployment, and managed operations. Hardware leads market share due to capital intensity. Software gains traction through cloud delivery models. Services support enterprise onboarding. Growth aligns with infrastructure expansion cycles.

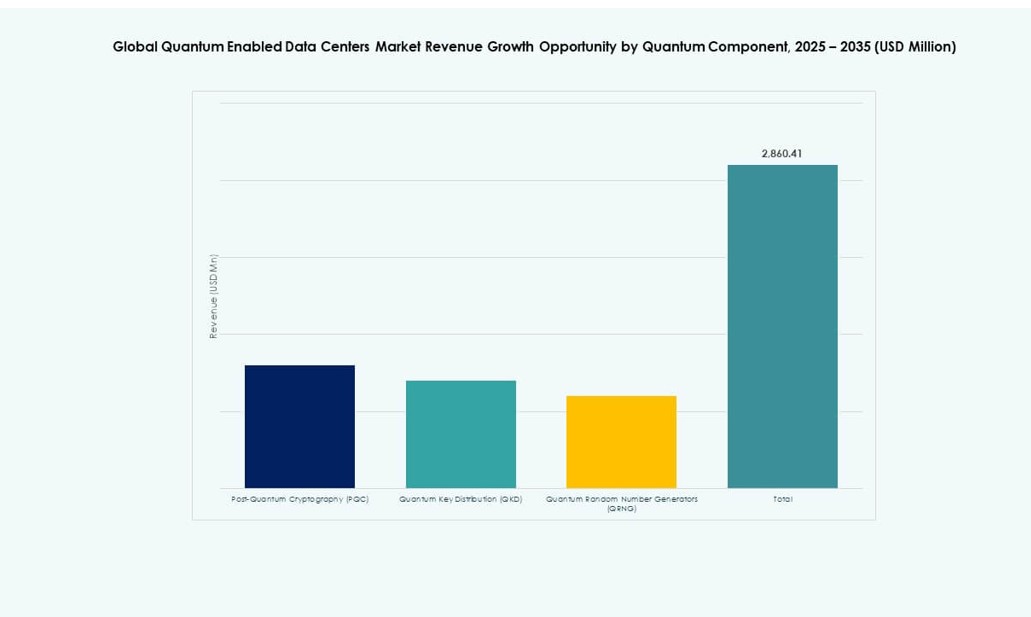

By Quantum Component

Post-Quantum Cryptography leads adoption due to immediate security needs. The Global Quantum Enabled Data Centers Market reflects strong demand for encryption upgrades. Quantum Key Distribution follows with secure communication use cases. Quantum Random Number Generators serve niche security applications. PQC holds the largest share due to regulatory pressure. QKD grows in government and finance sectors. QRNG adoption remains selective. Component choice aligns with risk profiles.

By Cooling Technology

Air cooling remains common for early-stage deployments. The Global Quantum Enabled Data Centers Market shows rising liquid cooling adoption. Liquid systems support higher stability. Operators favor precision thermal control. Air cooling suits smaller installations. Liquid cooling gains share with scale. Energy efficiency drives selection. Infrastructure design evolves rapidly.

By Enterprise Size

Large organizations dominate due to capital capacity. The Global Quantum Enabled Data Centers Market sees early adoption among hyperscalers and multinationals. Small and medium enterprises enter through cloud access. Large firms hold majority share. SMEs rely on service models. Adoption barriers differ by size. Investment focus favors scale. Market penetration widens gradually.

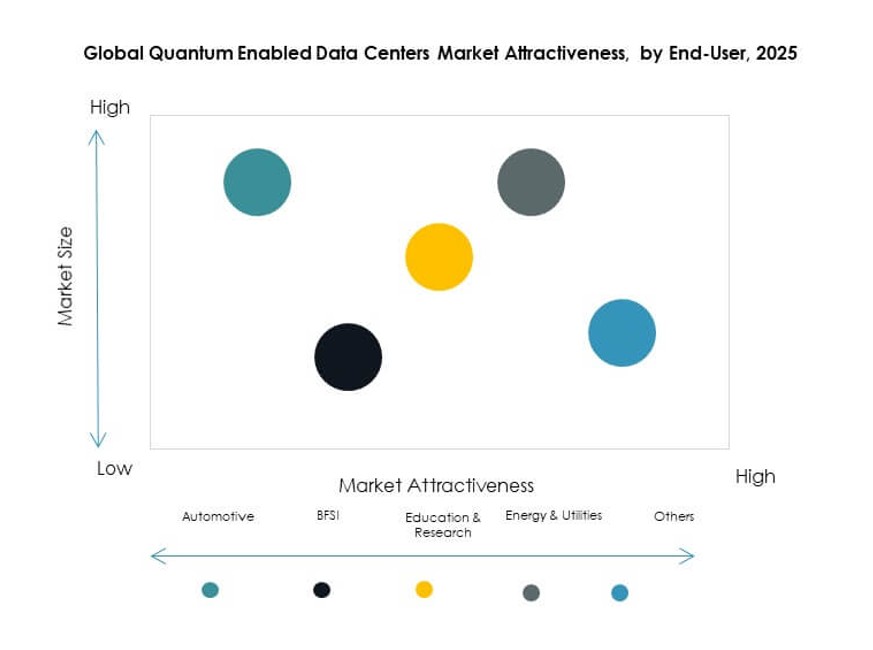

By End-user

Banking and financial services lead usage due to security and analytics needs. The Global Quantum Enabled Data Centers Market serves research and education strongly. Energy and utilities adopt for optimization tasks. Automotive explores simulation use cases. Other sectors remain exploratory. BFSI holds dominant share. Research drives innovation. Use cases diversify steadily.

Regional Insights:

North America And Europe

North America leads with nearly 38% market share due to strong quantum research ecosystems. The Global Quantum Enabled Data Centers Market benefits from U.S. cloud leadership. Canada supports adoption through national programs. Europe holds about 29% share. Germany, France, and the UK drive infrastructure investment. Public funding supports deployment. Regulatory focus strengthens security adoption.

- For instance, in 2025, D‑Wave Quantum signed a €10 million agreement with Swiss Quantum Technology SA to deploy its Advantage2 annealing quantum computer in Europe, making the system accessible through D‑Wave’s Leap cloud platform.

Asia Pacific

Asia Pacific accounts for around 26% market share. The Global Quantum Enabled Data Centers Market gains momentum in China and Japan. South Korea invests in advanced computing. India shows emerging interest through research initiatives. Government-backed programs support growth. Regional vendors expand capabilities. Adoption pace accelerates steadily.

- For instance, in 2025, India sanctioned 6.2 acres of land in Bengaluru for its upcoming “Quantum City,” aimed at hosting national labs and data infrastructure supporting future quantum deployments.

Middle East, Latin America, And Africa

These regions collectively hold about 7% market share. The Global Quantum Enabled Data Centers Market remains at an early stage here. Middle East countries invest through national digital strategies. Latin America shows pilot deployments. Africa focuses on research collaboration. Infrastructure gaps limit rapid growth. Long-term potential remains strong.

Competitive Insights:

- Atos SE

- D-Wave Quantum Inc.

- Google LLC

- IBM (International Business Machines Corporation)

- IonQ, Inc.

- IQM Quantum Computers

- NEC Corporation

- Oxford Instruments plc

- QuEra Computing Inc.

- Quantinuum

The competitive landscape of the Global Quantum Enabled Data Centers Market is shaped by a mix of established tech giants and emerging quantum technology firms. It favors companies with deep R&D capabilities, strategic partnerships, and hybrid data center solutions. IBM, Google, and D-Wave have made significant strides in integrating quantum systems into commercial environments. Firms like Quantinuum and IonQ push innovation with scalable architectures and cloud-accessible quantum services. Vendors focus on security features, cryptographic protocols, and platform integration to stay ahead. Most competitors align with government initiatives or consortium-led frameworks. The pace of hardware improvement and software orchestration defines competitive positioning. It remains dynamic, as new entrants collaborate with hyperscale data center operators and cloud service providers to accelerate deployment and market reach.

Recent Developments:

- In December 2025, Horizon Quantum commissioned its first in-house quantum computer, marking it as the first quantum software company to own and operate such hardware for software infrastructure advancement.

- In October 2025, Quantum Corporation and Entanglement, Inc. signed a strategic Memorandum of Understanding to integrate post-quantum encryption into storage solutions and develop regionalized AI data storage services.

- In January 2025, SoftBank and Quantinuum announced a strategic partnership to integrate quantum computing capabilities into data centers, enhancing processing power and security for large-scale operations.