Executive summary:

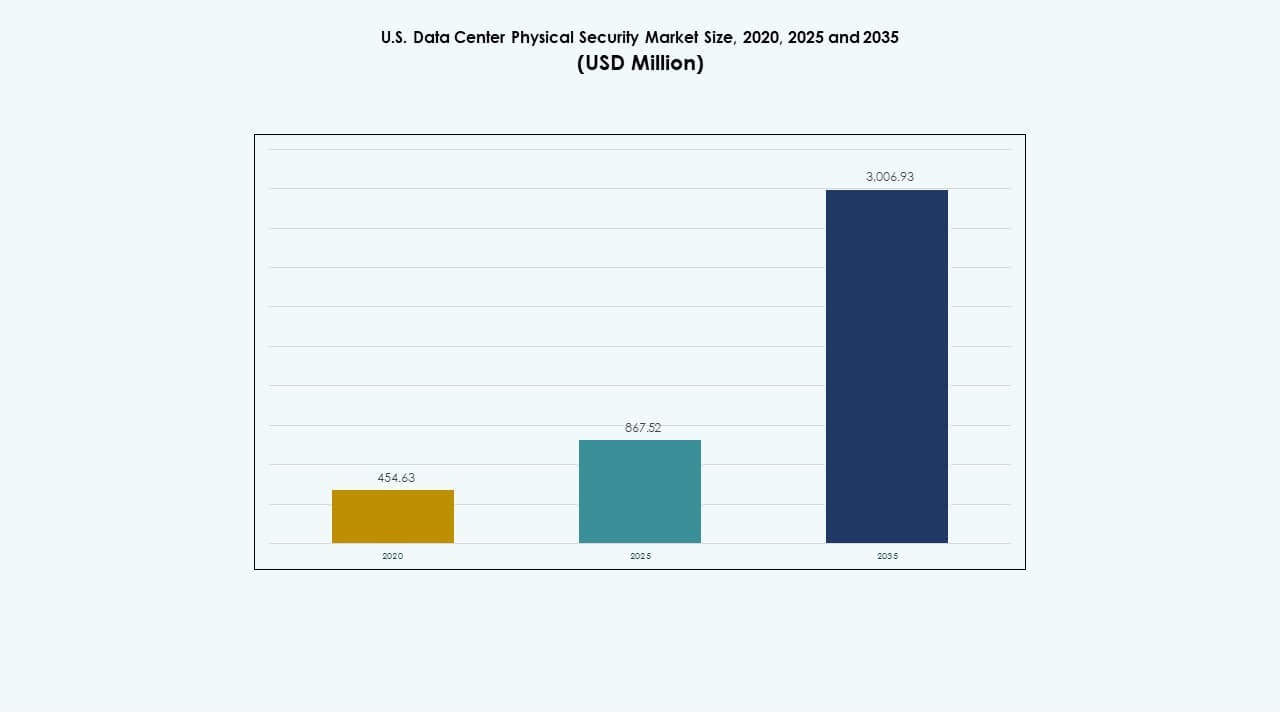

The U.S. Data Center Physical Security Market size was valued at USD 454.63 million in 2020 to USD 867.52 million in 2025 and is anticipated to reach USD 3,006.93 million by 2035, at a CAGR of 13.17% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2035 |

| U.S. Data Center Physical Security Market Size 2025 |

USD 867.52 Million |

| U.S. Data Center Physical Security Market, CAGR |

13.17% |

| U.S. Data Center Physical Security Market Size 2035 |

USD 3,006.93 Million |

Growing reliance on digital infrastructure drives strong adoption of modern physical protection systems across high-density facilities. Operators upgrade surveillance, biometric access, and automated monitoring tools to control rising breach risks. AI-powered platforms improve detection speed and help teams maintain compliance. The U.S. Data Center Physical Security Market gains strategic value for investors due to its role in supporting cloud, colocation, and enterprise networks. Innovation accelerates deployment of unified consoles that enhance visibility across large campuses.

The Northeast leads due to its dense presence of hyperscale clusters and strong enterprise demand. The South and Southwest emerge rapidly as expanding cloud corridors supported by new data center construction. The U.S. Data Center Physical Security Market also benefits from rising investment in the West, where major technology hubs strengthen perimeter and building access controls. Growth spreads across states with strong power availability, fiber routes, and lower land constraints.

Market Drivers

Market Drivers

Growing Deployment of Multi-Layer Defense Systems to Protect Expanding Digital Infrastructure

Operators raise investment in multi-layer controls to reduce breach risk across core facilities. Firms deploy biometric tools that strengthen identity checks at sensitive points. AI-driven cameras help teams detect threat patterns with stronger clarity. Integrated consoles support faster coordination across security units. The U.S. Data Center Physical Security Market gains strategic value due to rising cloud traffic. Investors monitor upgrades that lift operational stability. Businesses view stronger defense as a core requirement for compliance. Tier-IV sites adopt hardened designs that support safe growth. Hyperscale growth lifts demand for smarter preventive tools.

- For instance, Genetec’s Security Center platform unifies video, access, and ALPR data under a single console and supports more than 300 camera and sensor integrations, enabling large data campuses to consolidate multi-layer security workflows at scale.

Rising Use of Intelligent Access Control Driven by Higher Compliance Pressure

Companies deploy advanced access tools to keep critical rooms under strict supervision. Multi-factor checks create stronger barriers against unauthorized entry. Smart card grids help teams monitor user movement across halls. AI-based credential audits highlight misuse patterns in seconds. Industry players upgrade legacy panels that limit real-time insight. The segment gains relevance due to higher regulatory standards across data-sensitive sectors. The U.S. Data Center Physical Security Market strengthens its role in risk reduction plans for many operators. Investors track deployments that improve audit quality. Teams value uniform visibility across large campuses.

Expansion of Remote Monitoring and Automated Surveillance Platforms Across Large Campuses

Operators adopt remote consoles that deliver instant oversight of large footprints. Cloud-linked tools allow teams to supervise sites from central hubs. Automation supports quick threat detection in wider halls. Firms deploy thermal cameras that track abnormal heat signals. Access logs merge with video feeds to improve investigation clarity. The U.S. Data Center Physical Security Market gains support from digital-first growth strategies. Investors consider automated systems essential for scaling infrastructure safely. Many operators replace older cameras that limit detection depth. Unified tools reduce manual screening pressure on security units.

- For instance, Axis Communications’ Q29 thermal series provides temperature detection across ranges up to 400°C with real-time alerts, enabling remote operators to identify hotspots and equipment risk across large data campuses.

Growing Reliance on AI-Enabled Threat Analytics for Faster Incident Response

AI platforms study motion, entry data, and user behavior to flag anomalies. Smart alerts reduce delay between detection and response. Operators use machine learning models that refine accuracy with new data. Enterprises view predictive analytics as a long-term stabilizer. Control rooms rely on visual dashboards that highlight real-time patterns. The U.S. Data Center Physical Security Market secures stronger interest from firms with large workloads. Investors link strong analytics to lower breach probability. Security teams gain confidence from faster verification cycles. Data traffic growth pushes operators toward smarter automated tools.

Market Trends

Market Trends

Shift Toward Integrated Security Ecosystems That Unify Access, Video, and Analytics

Companies use integrated consoles that merge access logs, camera feeds, and alerts. Unified tools reduce system fragmentation across large environments. Operators rely on single dashboards that simplify cross-team coordination. Access events link with video playback for deeper clarity. Predictive tools support early risk detection across zones. The U.S. Data Center Physical Security Market gains traction from this shift. Vendors refine interoperability to reduce downtime risk. Strong interest rises from sites with multi-vendor networks. Integrators promote scalable setups that support long-term expansion.

Focus on Zero-Trust Physical Architecture Across High-Value Data Environments

Security plans move toward zero-trust layers that validate each user repeatedly. Entry rights adapt to user role, location, and time. Dynamic controls restrict access beyond required points. Camera grids help track movement across sensitive rooms. Alerts rise when deviations break predefined policies. The U.S. Data Center Physical Security Market aligns with strong zero-trust adoption. Teams benefit from enhanced oversight across critical zones. Vendors design access panels that support granular control. Demand grows from regulated sectors with strict security norms.

Rise in Demand for Cloud-Delivered Security Platforms Across Distributed Sites

Enterprises prefer cloud tools that support oversight across multiple campuses. Remote consoles allow security teams to respond faster. Camera networks stream data into secure hubs for analysis. Software updates deploy across devices without field delays. Unified hosting supports consistent policy control. The U.S. Data Center Physical Security Market shifts toward flexible deployment. Firms reduce reliance on local servers that limit scalability. Vendors improve resilience of cloud-linked tools. Demand rises among operators expanding across new regions.

Increased Use of Intelligent Perimeter Defense in High-Density Data Corridors

Operators secure outer zones with radar units, motion sensors, and thermal grids. Perimeter tools detect movement patterns with strong accuracy. Multi-layer fences add depth to physical security posture. Video towers connect with central dashboards for quick alerts. Teams track unusual activity across wider land areas. The U.S. Data Center Physical Security Market supports upgrades in dense data corridors. Vendors design perimeter units with higher range. Growth accelerates near markets with rising hyperscale expansion. Investors support upgrades that reduce large-area risk.

Market Challenges

High Integration Complexity and Rising Cost Pressure During Large-Scale Deployment

Teams face integration issues due to diverse hardware and legacy panels. Older systems lack compatibility with modern tools. Operators invest more capital to unify control modules. Coordination between vendors slows major upgrades. The U.S. Data Center Physical Security Market deals with rising hardware cost pressure. Skilled labor gaps limit smooth implementation across large campuses. Enterprises struggle to align deployment speed with compliance timelines. Multi-site rollouts take longer due to network constraints. Many operators face long evaluation cycles before final selection.

Growing Cyber-Physical Convergence Risk Across Connected Security Systems

Connected consoles expose physical tools to digital intrusion threats. Attackers target camera feeds and access logs to hide activity. Teams must protect APIs that link devices with monitoring hubs. Encryption gaps weaken system resilience across older networks. The U.S. Data Center Physical Security Market highlights the need for stronger cyber hygiene. Operators invest in network segmentation to reduce exposure. Security teams train staff to manage dual-layer risks. Vendors strengthen firmware controls across high-risk devices. Compliance audits push firms to improve configuration accuracy.

Market Opportunities

Market Opportunities

Expansion of AI-Driven Access and Monitoring Platforms Across Emerging Data Hubs

AI models help operators refine access patterns with stronger accuracy. Smart dashboards highlight unusual movement with quick precision. Firms adopt automated verification systems for critical rooms. Vendors design tools that support scalable cloud oversight. The U.S. Data Center Physical Security Market positions AI as a high-value growth lever. Growth rises across emerging data hubs that seek predictive defense. Investors monitor the shift toward machine-trained supervision. Teams gain more insight without raising manual workload. Many operators replace outdated tools that limit insight depth.

High Demand for Modular and Remote-Managed Security Solutions for Enterprise Edge Sites

Edge sites need compact tools that support fast deployment. Modular panels help firms expand protection without large rebuilds. Remote consoles deliver oversight across wide footprints. Vendors promote cloud updates that cut service delay. The U.S. Data Center Physical Security Market gains traction at new edge corridors. Investors view modular systems as cost-efficient assets. Operators improve network safety with linked devices. Growth expands with rising enterprise edge adoption. Smart modules attract firms with limited field teams.

Market Segmentation

By Data Center Size

Small data centers gain attention for simplified access tools, while medium centers secure stronger demand due to balanced scale and higher room counts. Large data centers hold the dominant share due to dense equipment halls and strict compliance needs. Many operators invest in unified platforms that support high-volume activity. The U.S. Data Center Physical Security Market strengthens interest in large centers due to rising hyperscale growth.

By Component

Solution components lead due to stronger demand for surveillance, access control, and perimeter defense. Services grow due to rising consulting and integration needs across complex networks. Many operators depend on service partners to optimize deployment speed. Firms replace outdated equipment through structured service plans. The U.S. Data Center Physical Security Market gains long-term value from full-cycle solution adoption.

By Solution

Video surveillance holds leadership due to wide use across halls and perimeter zones. Access control supports identity verification across sensitive rooms. Monitoring and detection tools rise due to higher breach risk across large campuses. Operators upgrade sensor grids that enhance situational awareness. The U.S. Data Center Physical Security Market gains steady use of multi-solution stacks across hyperscale sites.

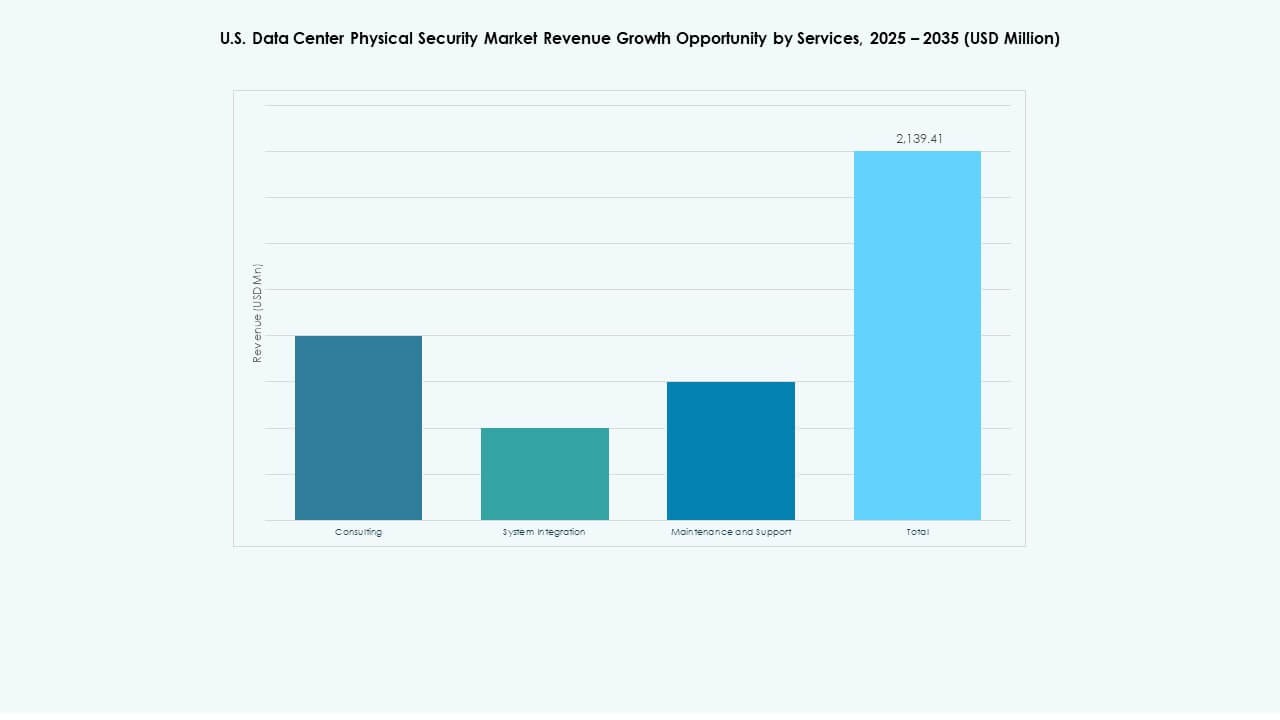

By Services

System integration leads due to high complexity across modern environments. Consulting supports design optimization for regulated sectors. Maintenance and support maintain stable system health across wide networks. Operators renew service plans to reduce downtime. The U.S. Data Center Physical Security Market strengthens service demand across multi-vendor setups.

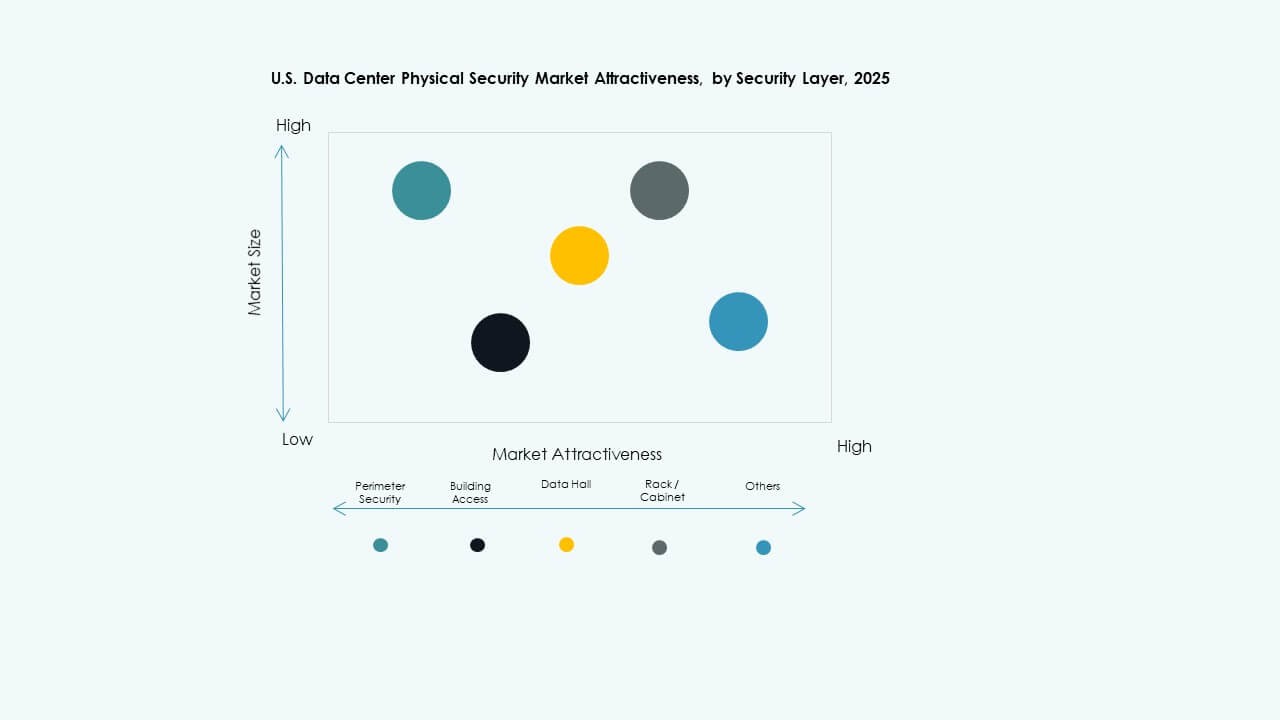

By Security Layer

Perimeter security holds strong demand due to wide-zone risk. Building access gains traction through multi-factor controls. Data halls secure deeper investment for critical workloads. Rack and cabinet controls rise due to rising insider threat concerns. The U.S. Data Center Physical Security Market supports multi-layer adoption across dense campuses.

By Data Center Type

Hyperscale centers dominate due to high capacity and rigorous security needs. Colocation centers grow due to diverse tenant profiles. Enterprise sites adopt structured upgrades for improved control. Edge centers rise with compact deployments near user zones. The U.S. Data Center Physical Security Market aligns with strong hyperscale and colocation expansion.

By End-user

IT and telecom lead due to heavy digital traffic across core networks. BFSI invests more to secure transaction systems. Government and defense demand strict access control for sensitive rooms. Healthcare and life sciences secure more data hall activity. The U.S. Data Center Physical Security Market supports broad industry adoption with tiered tools.

Regional Insights

Regional Insights

Northeast Region

The Northeast holds close to 32% share due to dense data corridors and strong enterprise presence. Operators invest in high-grade surveillance and access control tools across major hubs. The U.S. Data Center Physical Security Market supports growth in states with strong digital maturity. Many hyperscale operators choose this region for network proximity. Compliance pressure drives tighter physical controls. Investment clusters around major financial and telecom centers. Firms adopt uniform policies to reduce facility risk.

- For instance, CoreSite deploys eight-foot perimeter fencing with 360-degree high-resolution exterior cameras and 24/7 video surveillance at NY2 Secaucus, NJ facility.

South and Southwest Region

The region secures around 29% share driven by Texas, Arizona, and growing edge corridors. Operators expand new campuses due to land availability and robust power supply. The U.S. Data Center Physical Security Market aligns with rapid cloud provider expansion. Firms use smart perimeter tools to protect wide land footprints. Growth rises in areas preferred for low-latency routes. Vendors deploy scalable systems for new hyperscale parks. Demand stays strong across high-traffic cloud zones.

- For instance, CoreSite PH2 Phoenix facility uses key cards, biometric scanners, eight-foot perimeter fencing, and perimeter/interior IP-DVR cameras for controlled access.

West Region

The West captures nearly 27% share due to Silicon Valley, Oregon, and emerging Pacific hubs. Operators deploy multi-layer controls to protect high-value AI workloads. The U.S. Data Center Physical Security Market grows due to rising investment from large technology firms. Teams use AI-driven surveillance for high-density halls. Edge centers expand near coastal routes to support digital growth. Vendors upgrade systems to manage high equipment load. Compliance norms strengthen demand for controlled access.

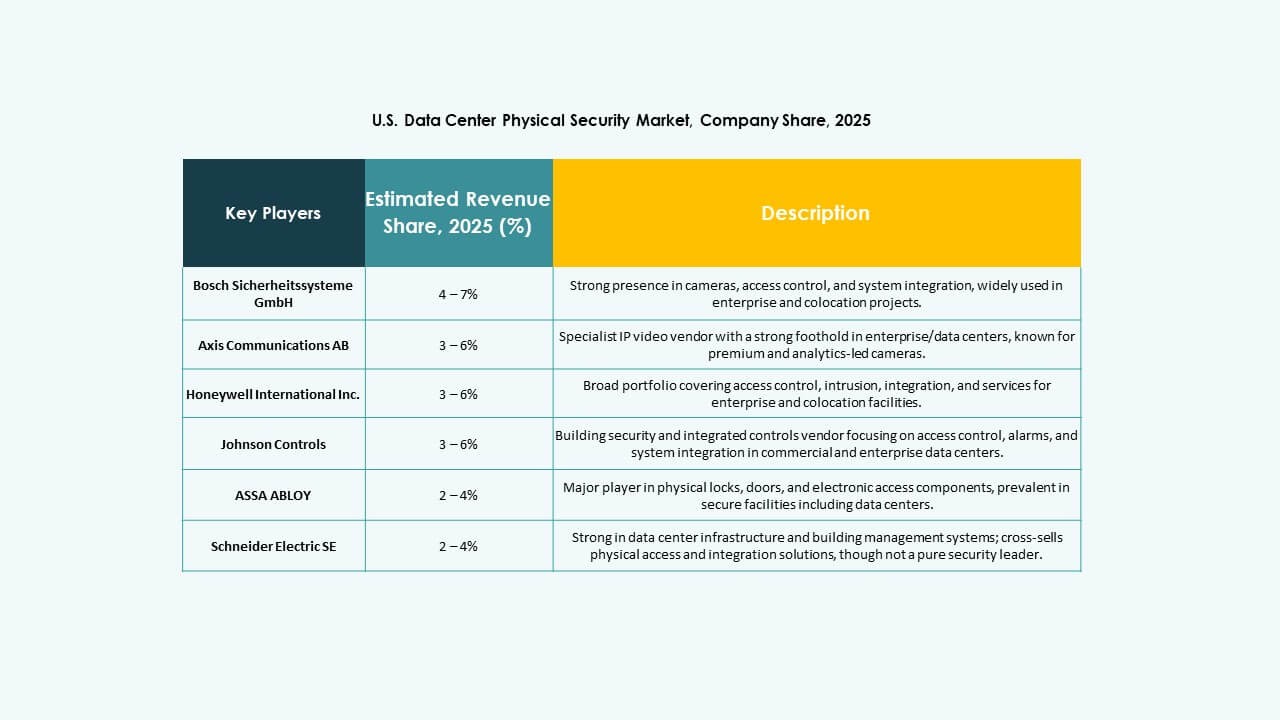

Competitive Insights:

- ABB

- Allied Universal

- ASSA ABLOY

- Axis Communications AB

- Bosch Sicherheitssysteme GmbH

- Cisco Systems, Inc.

- Fortinet

- Genetec

- Hangzhou Hikvision Digital Technology Co., Ltd.

- Honeywell International Inc.

- Johnson Controls

- Palo Alto Networks

- Schneider Electric SE

- Securitas

- Siemens AG

The U.S. Data Center Physical Security Market features strong competition shaped by global security vendors and specialized technology providers. Each company focuses on integrated access systems, advanced surveillance tools, and real-time monitoring platforms that support high-density data environments. Firms expand portfolios through AI-based analytics and cloud-enabled consoles that improve threat response. Many players strengthen alliances with colocation and hyperscale operators to secure long-term contracts. Product differentiation grows through biometric upgrades, cyber-physical integration, and hardened perimeter controls. Several vendors pursue mergers to widen geographic reach and technical depth. New entrants target niche layers such as rack-level authentication and mobile credential systems. The market deepens competition through rapid innovation across software, hardware, and managed security layers.

Recent Developments:

- In October 2025, ASSA ABLOY acquired Kentix GmbH, a German company specializing in monitoring and access control products designed for data centers, enhancing their capabilities in physical security for this sector.

- In January 2025, ASSA ABLOY also acquired InVue, a Charlotte-based provider of asset protection and access control solutions, aligning with their strategy to expand globally in access control and asset protection.

- In May 2025, CPX acquired TSI Tech to bolster its physical security portfolio, including data center protection through enhanced critical infrastructure solutions that converge physical and cybersecurity with AI-driven innovations.