Executive summary:

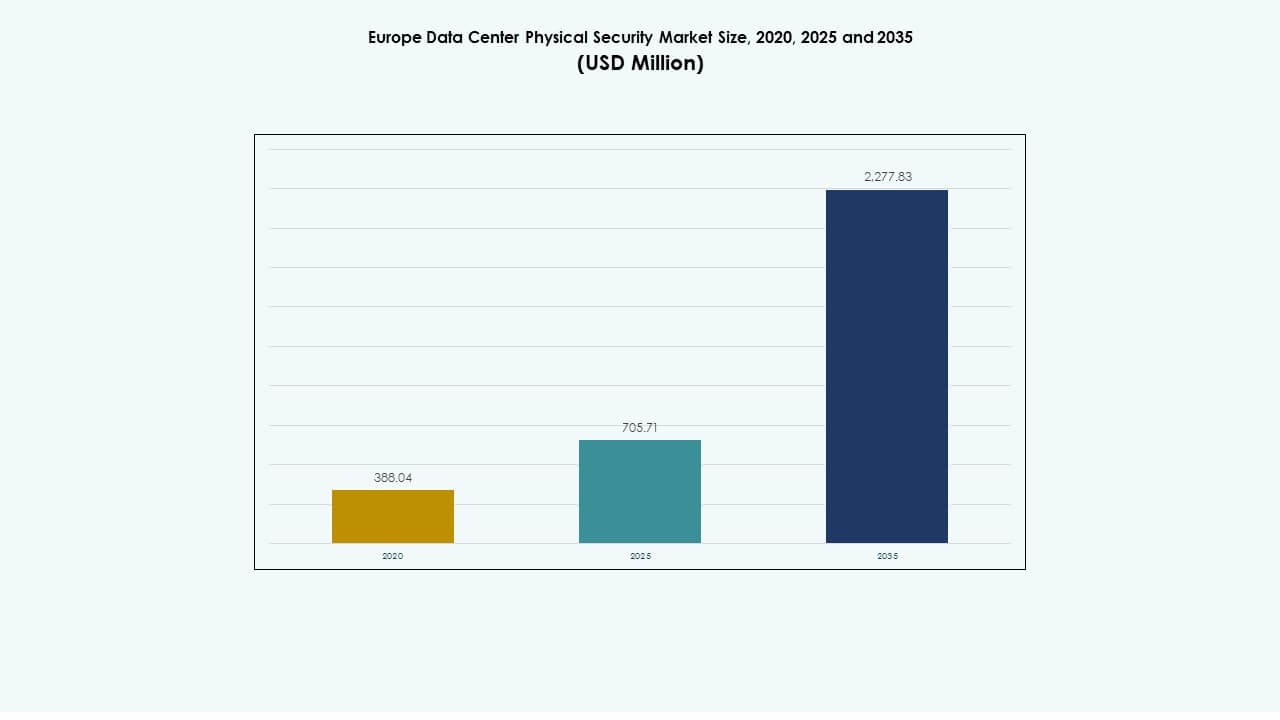

The Europe Data Center Physical Security Market size was valued at USD 388.04 million in 2020, reached USD 705.71 million in 2025, and is anticipated to hit USD 2,277.83 million by 2035, growing at a CAGR of 12.38% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2035 |

| Europe Data Center Physical Security Market Size 2025 |

USD 705.71 Million |

| Europe Data Center Physical Security Market, CAGR |

12.38% |

| Europe Data Center Physical Security Market Size 2035 |

USD 2,277.83 Million |

Rising digitization and strict regulatory compliance have accelerated demand for advanced access control, video surveillance, and AI-driven monitoring tools. Businesses invest in layered security to mitigate breach risks, while innovation in automation and sensor integration enhances system reliability. The Europe Data Center Physical Security Market holds strategic importance for investors focusing on resilient infrastructure and data protection.

Western Europe leads due to its strong hyperscale and colocation footprint in the UK, Germany, and France. Northern and Central Europe gain traction with sustainable data parks, while Southern and Eastern Europe emerge with new edge and colocation investments. Growing energy efficiency and regulatory alignment support balanced regional expansion.

Key Market Drivers

Key Market Drivers

Rising Investments in Data Center Infrastructure Modernization Across Europe

The Europe Data Center Physical Security Market expands with major infrastructure upgrades across hyperscale and enterprise facilities. Operators invest in biometric access, AI surveillance, and thermal analytics to enhance threat detection. Growing cloud adoption from banking, telecom, and healthcare sectors strengthens deployment of physical security hardware. It reflects the region’s focus on compliance and data protection laws. The market sees increased integration of automation in security management. Vendors design scalable solutions compatible with hybrid and multi-cloud architectures. Rising capital inflow into colocation hubs in Western Europe drives rapid adoption. Businesses seek enhanced protection against physical breaches and unauthorized access.

- For instance, Vantage Data Centers raised €720 million in June 2025 through the first euro-denominated asset-backed securitization covering four data centers in Germany, including sites in Berlin and Frankfurt, highlighting growing investment in secure and scalable physical infrastructure across Europe.

Integration of AI and IoT Enhancing Physical Security Intelligence

Artificial intelligence and IoT technologies strengthen real-time monitoring within facilities. Machine learning models analyze access logs and environmental data to predict risks. AI cameras automate intrusion detection and improve response accuracy. The Europe Data Center Physical Security Market benefits from early implementation of predictive analytics in mission-critical systems. Operators adopt connected sensors to monitor door activity and perimeter zones. Vendors promote AI-based command platforms for unified security visualization. It drives operational efficiency and compliance alignment across multi-tenant facilities. Demand for intelligent surveillance grows as energy-efficient data centers expand.

Regulatory Compliance Driving Advanced Security System Adoption

Strict regulations under GDPR and national cybersecurity laws push operators to invest in high-grade physical protection. It ensures compliance and reduces risk of audit penalties. The market evolves around stringent physical and logical access requirements. The Europe Data Center Physical Security Market attracts attention from investors seeking regulated asset growth. Governments promote frameworks for securing critical digital infrastructure. Vendors introduce certified access control and video systems supporting multi-factor authentication. European standards emphasize redundancy and access transparency. Security solutions align with sustainability goals to meet modern data infrastructure policies.

Growing Demand for Colocation and Edge Facilities Strengthening Security Infrastructure

Edge and colocation growth increases demand for advanced security installations. Operators secure distributed nodes to protect latency-sensitive data. The Europe Data Center Physical Security Market gains traction as enterprises expand to regional edge zones. Providers deploy modular access grids and smart surveillance to secure remote facilities. Strategic partnerships with integrators drive holistic infrastructure protection. AI-ready access systems improve uptime and operational reliability. Energy efficiency remains a key consideration in system design. Rising outsourcing of IT workloads accelerates the need for trusted and compliant environments.

- For instance, Vantage Data Centers announced in October 2025 a plan to build its second Italian campus (MXP2) near Milan with an investment of over €350 million, adding 32 MW IT capacity to support hyperscale and colocation growth while expanding its secure European data center footprint.

Key Market Trends

Key Market Trends

Adoption of AI-Powered Access and Surveillance Systems in Hyperscale Facilities

Hyperscale operators integrate AI-based analytics to enhance situational awareness. These systems detect irregular movements and predict breach attempts. Smart cameras, embedded with neural processing, enable faster incident response. The Europe Data Center Physical Security Market witnesses strong uptake of AI surveillance suites among Tier III and IV sites. Vendors collaborate with automation providers to link physical systems with cybersecurity networks. This hybrid security layer strengthens governance frameworks. Predictive analytics lowers operational risks and improves scalability. AI-driven infrastructure paves the path for intelligent, adaptive monitoring across Europe.

Rising Popularity of Multi-Layered Physical Defense Frameworks

Operators emphasize multi-layered protection across perimeter, building, and cabinet levels. The Europe Data Center Physical Security Market accelerates toward integration of redundant security zones. Each layer combines access control, sensors, and real-time monitoring. Advanced perimeter barriers and facial recognition systems reduce human error. Vendors introduce modular frameworks supporting quick deployment across multiple facilities. These configurations ensure compliance and cost control. Stakeholders value layered systems for preventing downtime and ensuring business continuity. Continuous upgrades sustain resilience across hybrid colocation and cloud environments.

Increasing Role of Managed Security Services and Remote Monitoring

Enterprises adopt managed security services to minimize internal complexity. Remote monitoring centers now handle access control, video analytics, and alarm validation. The Europe Data Center Physical Security Market observes strong traction from firms outsourcing facility management. Managed providers integrate cloud-based dashboards for real-time visualization. It supports scalability for growing multi-site networks. Service-level agreements guarantee 24×7 uptime and swift incident response. The trend aligns with rising emphasis on efficiency and predictive maintenance. Continuous monitoring improves audit readiness for high-compliance industries.

Shift Toward Green and Sustainable Security Solutions

Sustainability principles extend to physical protection systems. The Europe Data Center Physical Security Market adopts energy-efficient hardware and low-emission materials. Vendors design eco-friendly surveillance units and LED-powered monitoring systems. Facilities integrate renewable-powered security grids to align with corporate ESG goals. Recyclable enclosures and passive cooling reduce energy consumption. Manufacturers implement smart power control to extend component life. Sustainability-driven innovations attract government incentives and investor interest. Security modernization aligns with the region’s carbon-neutral targets and long-term digital policies.

Market Challenges

Market Challenges

High Cost of Integration and Maintenance Across Distributed Networks

Deploying physical security across multiple sites presents high capital expenditure. Many operators struggle to synchronize hardware with legacy systems. The Europe Data Center Physical Security Market faces rising costs from complex integration processes. Maintaining compatibility between access control, monitoring, and IT management tools increases operational burden. Service contracts require specialized technicians, raising expenses for smaller operators. Power and maintenance costs remain high due to redundant configurations. It challenges return on investment timelines. Continuous hardware upgrades also strain annual budgets for hyperscale and enterprise operators.

Data Sovereignty and Regulatory Complexity Slowing Uniform Implementation

Different nations maintain varied compliance frameworks, complicating system deployment. The Europe Data Center Physical Security Market operates under fragmented standards affecting scalability. Vendors must adapt to local certification, fire safety, and privacy laws. This diversity delays installation cycles and inflates project timelines. Cross-border facilities face limitations on data residency and control system integration. Regulatory reviews often extend approval for critical assets. Vendors face growing documentation and validation efforts. Harmonizing standards remains essential for seamless cross-European infrastructure development.

Market Opportunities

Market Opportunities

Expansion of Edge Infrastructure Creating New Security Demand Corridors

Edge computing expansion generates strong demand for compact, intelligent security systems. The Europe Data Center Physical Security Market benefits from distributed deployments near urban and industrial zones. Edge nodes require advanced cabinet-level protection and biometric access tools. Vendors explore modular security packages for scalability. Compact AI-enabled devices improve response accuracy and uptime. Service providers gain new revenue through adaptive security consulting. Edge security investment supports resilience for smart city and 5G networks.

Growth in Managed Services and Cloud-Native Security Platforms

Managed services emerge as a growth vector for regional operators. The Europe Data Center Physical Security Market experiences demand for subscription-based monitoring and maintenance packages. Cloud-native platforms simplify system updates and compliance tracking. Businesses prefer service-based contracts to reduce upfront costs. Vendors design multi-tenant dashboards supporting instant alerts and analytics. Integration with cybersecurity tools enhances incident visibility. These developments create sustainable revenue and attract institutional investors.

Market Segmentation

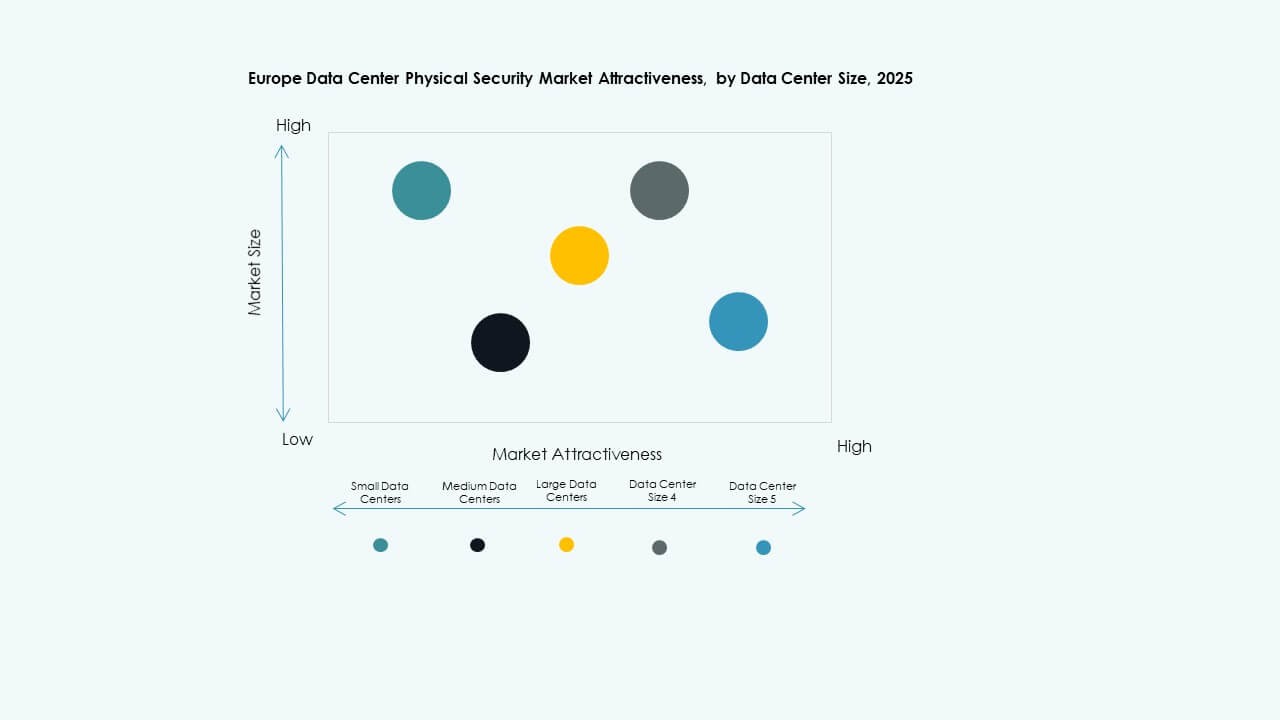

By Data Center Size

Large data centers dominate the Europe Data Center Physical Security Market due to vast infrastructure investments and regulatory focus. These sites prioritize advanced perimeter and cabinet-level defense. Medium centers expand rapidly in secondary cities to support regional workloads. Small centers adopt compact security solutions suitable for modular deployments. The segment’s growth correlates with rising enterprise digitization and hyperscale expansion.

By Component

The solution segment leads due to higher spending on physical access systems and surveillance hardware. The Europe Data Center Physical Security Market witnesses steady demand for integrated consoles and analytics tools. Services gain traction from growing reliance on consulting and integration support. Vendors enhance remote management capabilities to meet multi-site needs. The shift toward digital service contracts fuels ongoing maintenance adoption.

By Solution

Video surveillance systems hold dominant share driven by compliance and incident response needs. Access control solutions expand through biometric integration. Monitoring and detection technologies improve situational awareness. The Europe Data Center Physical Security Market evolves with adoption of AI-powered cameras and motion sensors. Hybrid solutions combining analytics and cloud storage improve audit transparency.

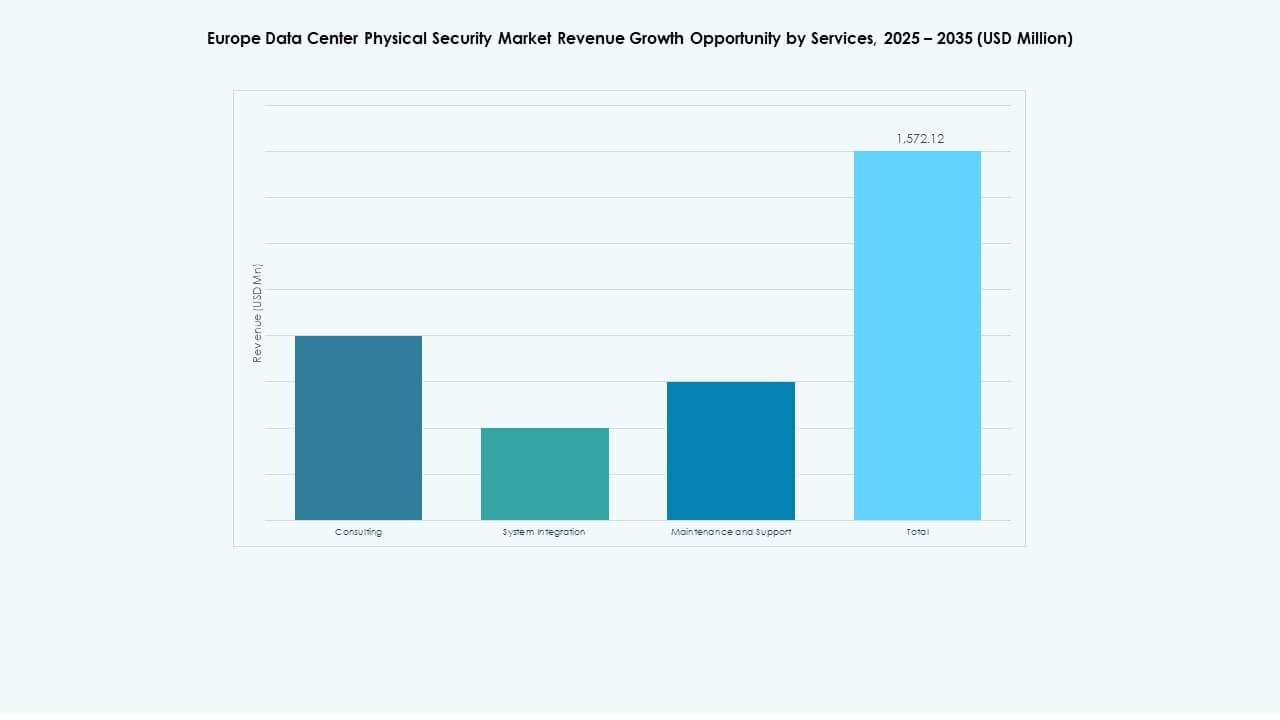

By Services

System integration services lead due to demand for seamless hardware-software alignment. Consulting remains vital for compliance and site design. The Europe Data Center Physical Security Market experiences growth in maintenance contracts supporting uptime reliability. Vendors offer 24×7 monitoring assistance and predictive maintenance analytics. Service bundling strengthens long-term client engagement and asset protection.

By Security Layer

Perimeter security dominates, supported by advanced fencing, surveillance towers, and intrusion sensors. Building access and data hall layers follow due to expanding entry-point control requirements. The Europe Data Center Physical Security Market benefits from demand for cabinet-level sensors and keyless locks. Layered security ensures redundancy and reduces breach risks. Operators implement tiered defense aligned with international standards.

By Data Center Type

Hyperscale facilities hold the largest share due to dense infrastructure and strict compliance demands. Colocation data centers expand fastest through shared client environments. Enterprise centers integrate modular controls for internal IT needs. The Europe Data Center Physical Security Market supports edge centers securing regional nodes. Growth in hybrid deployment strengthens demand for flexible security systems.

By End-user

The BFSI sector leads driven by strong data protection mandates. IT & telecom follows due to cloud and AI infrastructure growth. Government and defense prioritize controlled access and perimeter defense. The Europe Data Center Physical Security Market gains traction from healthcare, retail, and manufacturing adoption. These sectors demand continuous uptime and strict compliance with regional standards.

Regional Analysis

Regional Analysis

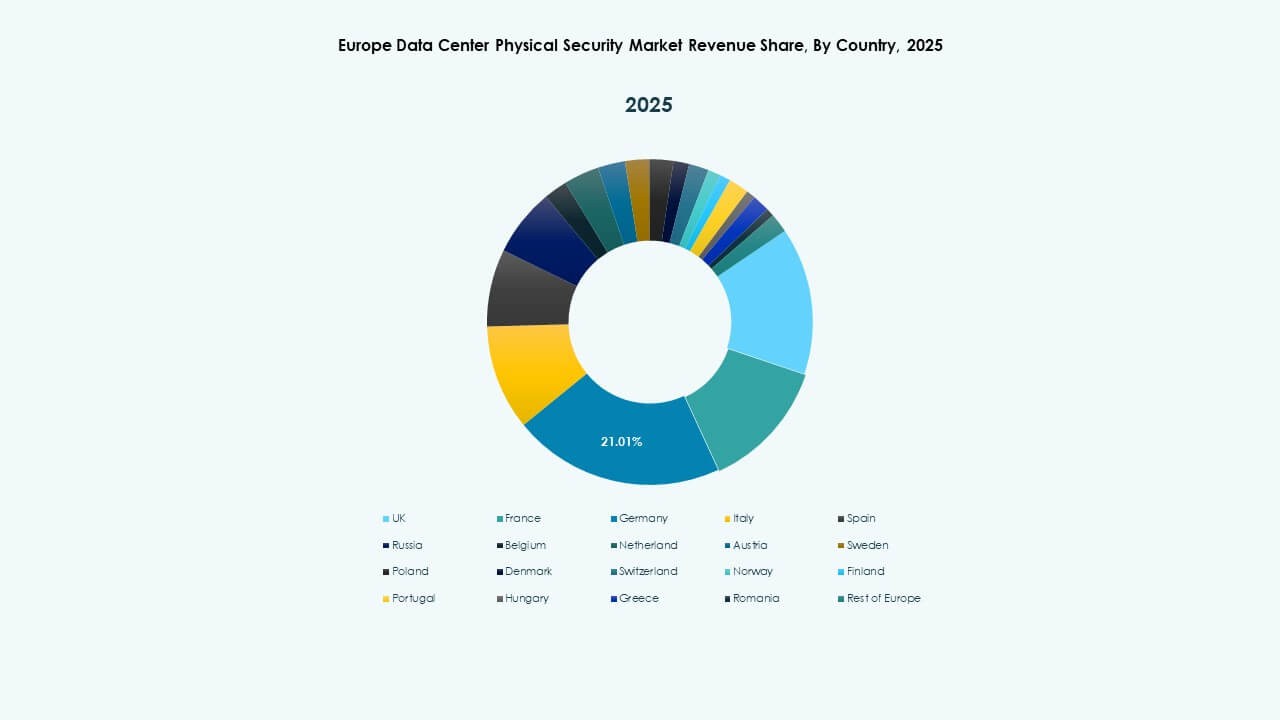

Western Europe: Established Infrastructure and Stringent Compliance Frameworks

Western Europe dominates the Europe Data Center Physical Security Market with nearly 45% share. The UK, Germany, and France lead through dense hyperscale deployments. Strict regulatory structures drive investment in AI and biometric-based protection. Colocation providers in London and Frankfurt upgrade systems to meet energy efficiency and ESG targets. The region remains the epicenter for innovation in surveillance and access technology.

- For instance, Equinix data centers across Western Europe maintain multi-layer physical security, including 24/7 on-site personnel, mantraps, biometric access control, and continuous video surveillance, ensuring strict protection of mission-critical infrastructure and alignment with the company’s global security and operational standards.

Northern and Central Europe: Rising Hyperscale Expansion and Cloud Integration

Countries like the Netherlands, Sweden, and Denmark experience strong demand due to renewable energy integration. The Europe Data Center Physical Security Market grows as hyperscale firms develop green data parks. Northern Europe benefits from sustainable energy use and political stability. Central Europe attracts investment from international cloud providers. Strategic location and cooling efficiency make it a preferred data corridor for future projects.

Southern and Eastern Europe: Emerging Investment Hubs for Edge Deployments

Southern and Eastern Europe gain share driven by new edge data centers in Spain, Italy, and Poland. The Europe Data Center Physical Security Market strengthens with government-backed digital infrastructure programs. Affordable land and connectivity upgrades attract foreign players. Local firms adopt modular security systems for distributed operations. These regions evolve as critical growth zones supporting the continent’s expanding digital backbone.

- For instance, Digital Realty implemented the Symmetry Access Control system across multiple global data centers, integrating it with centralized video management to strengthen physical access monitoring and site protection, a framework also adopted in several European facilities to enhance operational security and compliance.

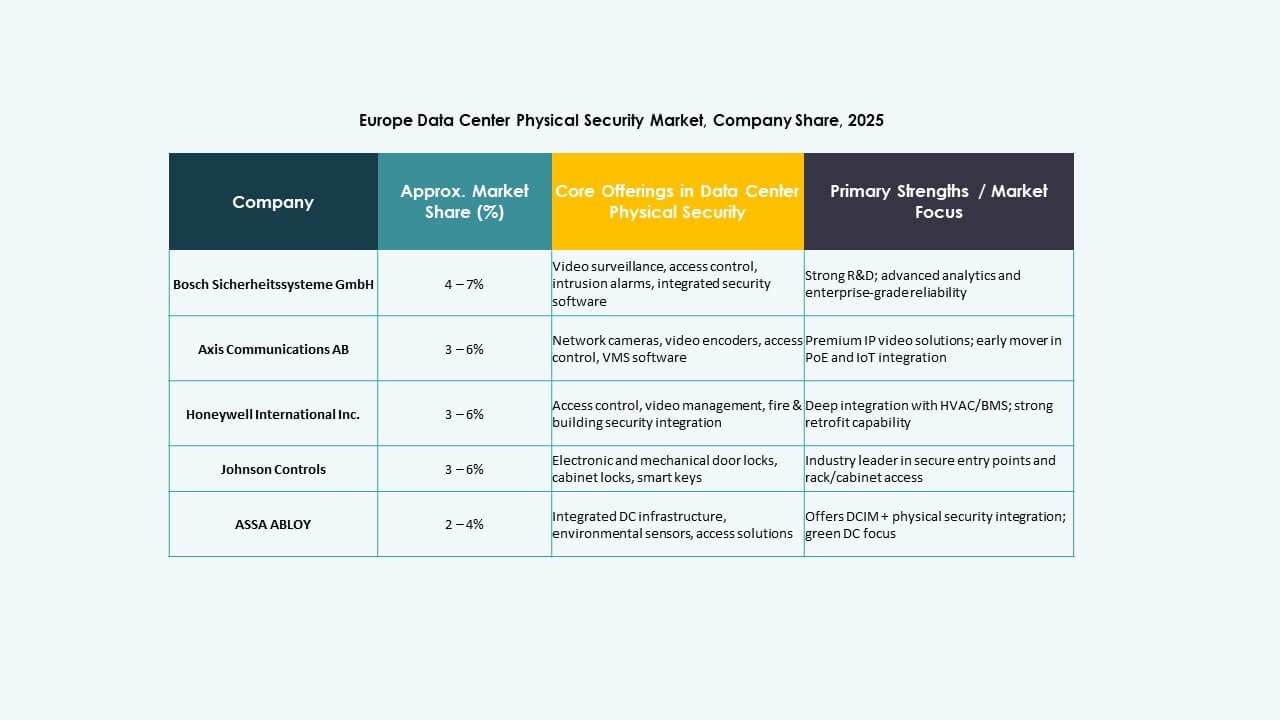

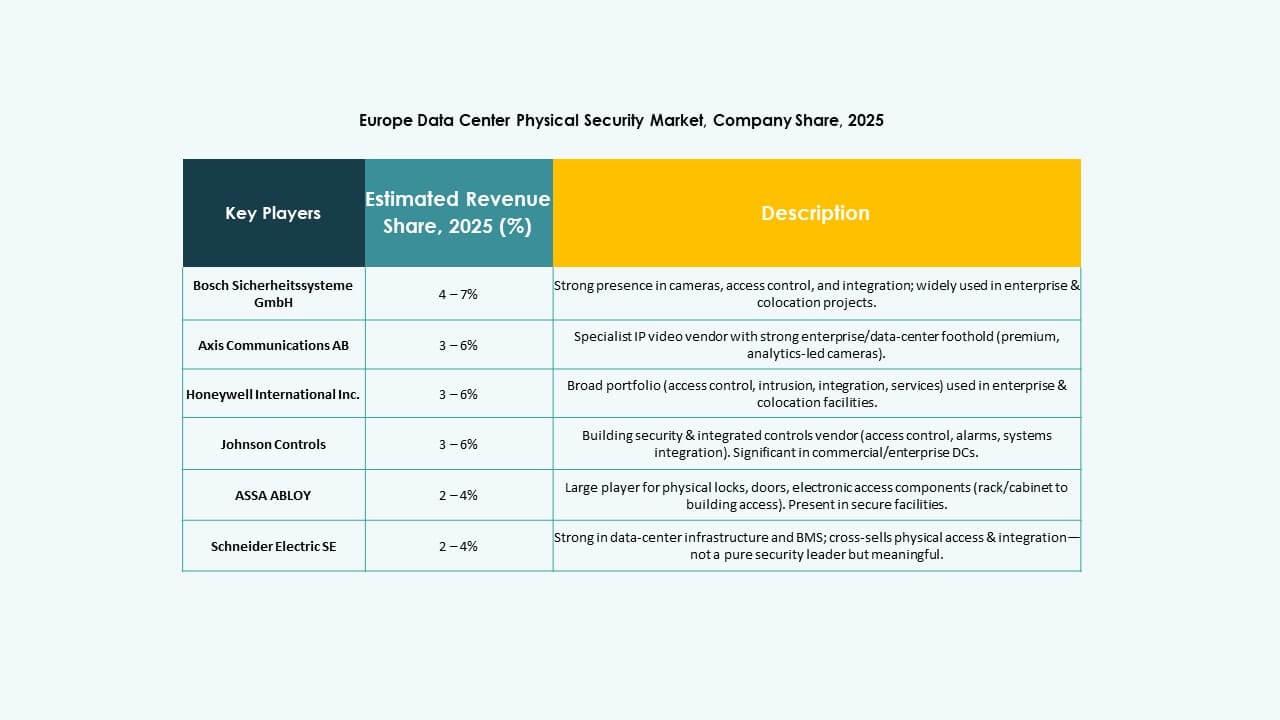

Competitive Insights:

- Bosch Sicherheitssysteme GmbH

- Securitas AB

- Axis Communications AB

- Honeywell International Inc.

- Johnson Controls

- Schneider Electric SE

- ABB Ltd

- Siemens AG

- Cisco Systems, Inc.

- Genetec

- Fortinet

- Palo Alto Networks

- Dahua Technology Co. Ltd.

- Hanwha Vision Co. Ltd.

- Secom Co. Ltd.

- Teledyne FLIR LLC

Competition among major security vendors remains intense. Companies deploy broad product portfolios covering access control, video surveillance, intrusion detection, and integrated facility management. This diversity gives buyers flexible options tailored to facility size and compliance needs. Many players expand through mergers, partnerships, or new product launches to strengthen presence in data-center and colocation facilities. Mid-size and large operators often prefer established brands for reliability and service support. Smaller data-center operators lean toward flexible, modular solutions from emerging vendors. It highlights the growing demand for robust, scalable security solutions across Europe’s evolving data infrastructure landscape.

Recent Developments:

Recent Developments:

- In June 2025, Vantage Data Centers secured EUR 720 million through Europe’s inaugural data-center asset-backed securitization to refinance four sites in Germany, underscoring rising investments in secure physical infrastructure within the Europe data center physical security market.

- In December 2024, Bosch Sicherheitssysteme GmbH sold its security and communications technology product business to the European investment firm Triton. The transaction included three business units Video, Access and Intrusion, and Communication as Bosch aims to focus more on systems integration business.