Executive summary:

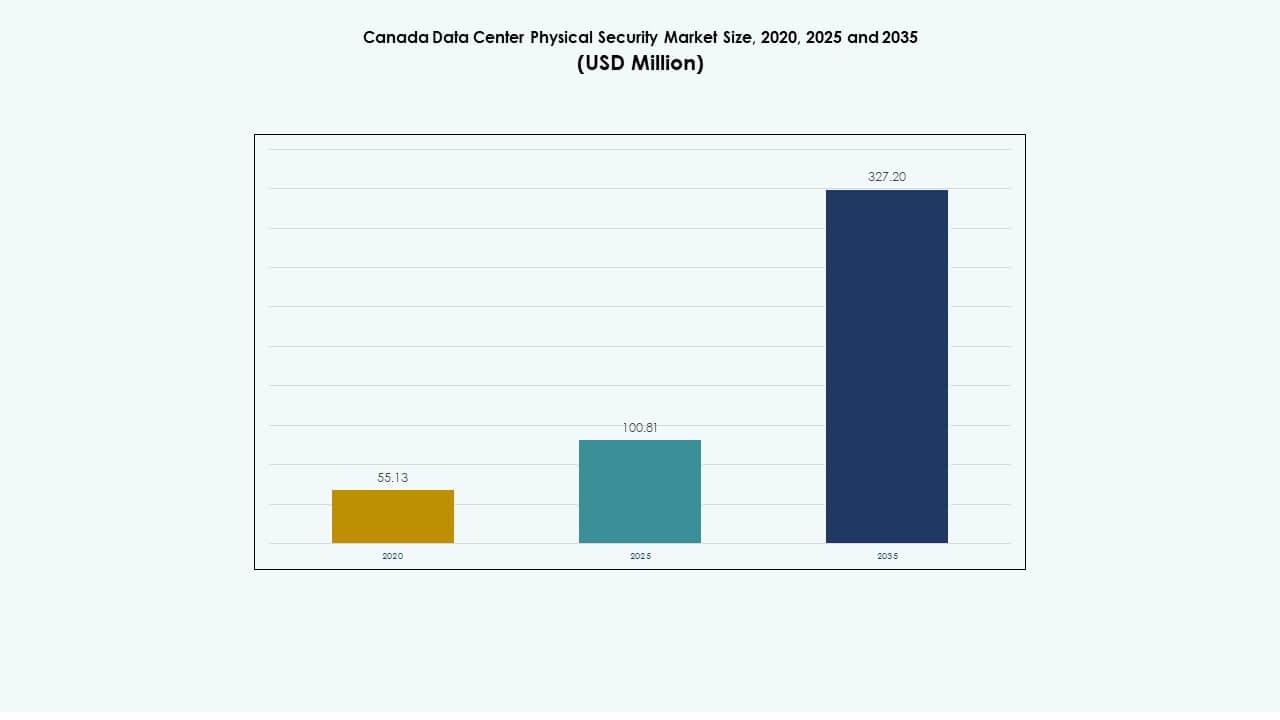

The Canada Data Center Physical Security Market size was valued at USD 55.13 million in 2020 to USD 100.81 million in 2025 and is anticipated to reach USD 327.20 million by 2035, at a CAGR of 12.44% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2035 |

| Canada Data Center Physical Security Market Size 2025 |

USD 100.81 Million |

| Canada Data Center Physical Security Market, CAGR |

12.44% |

| Canada Data Center Physical Security Market Size 2035 |

USD 327.20 Million |

Growth is driven by strong adoption of AI-based surveillance, biometric access systems, and IoT-integrated monitoring tools. The market evolves with rising data traffic, stricter compliance regulations, and expanding hyperscale infrastructure. It plays a strategic role for investors and operators seeking resilient data center operations. Businesses consider advanced physical protection as essential for operational continuity, uptime assurance, and regulatory trust in a digital economy.

Eastern Canada leads due to high data center concentration in Ontario and Quebec, supported by favorable climate and strong energy infrastructure. Western Canada, including Alberta and British Columbia, emerges as a growth zone with expanding edge and colocation facilities. Growing cloud adoption and local hosting policies enhance nationwide investment potential, creating balanced growth across regions.

Market Drivers

Market Drivers

Growing Demand for Advanced Surveillance and Access Control Technologies Across Data Center Facilities

The Canada Data Center Physical Security Market experiences rapid expansion driven by increased use of AI-based surveillance, biometric access systems, and intelligent video analytics. Enterprises prioritize real-time monitoring and automated alert mechanisms to reduce breach incidents. Integration of multi-layer security architecture strengthens defense at entry points, data halls, and racks. It helps operators maintain high operational integrity under rising data traffic. Cloud and colocation players implement unified command centers to manage all security layers efficiently. Demand for physical security grows with stricter compliance norms. Businesses view this evolution as critical to building user trust and regulatory alignment. Investors see consistent returns through recurring maintenance and software integration contracts.

Integration of Artificial Intelligence and IoT to Enhance Predictive Threat Management

AI and IoT integration in physical security tools reshapes monitoring efficiency across hyperscale facilities. Companies use smart sensors and analytics platforms to track anomalies across vast premises. Machine learning models detect irregular movement and temperature variations early. It supports faster decision-making and reduces dependency on manual oversight. Vendors introduce AI-driven access control that learns from activity patterns to predict breaches. Demand for data-driven tools positions security systems as part of strategic IT modernization. The Canada Data Center Physical Security Market gains credibility for its ability to provide adaptive protection. It attracts both infrastructure funds and enterprise buyers investing in resilient operational continuity.

Rising Compliance Pressure and Stringent Government Policies on Data Protection Standards

Government-backed data localization and privacy laws push enterprises to adopt robust physical safeguards. Mandatory audits for critical infrastructure sites encourage adoption of high-grade access barriers. Vendors offer modular compliance frameworks aligning with federal and provincial cybersecurity standards. It improves investor confidence in the long-term sustainability of security infrastructure. Businesses incorporate biometric screening and visitor authentication across Tier III and Tier IV sites. The move toward standardized protection protocols enhances national security posture. Security integration becomes a differentiator among managed data service providers. Compliance-driven growth ensures consistent spending across both private and public sectors.

- For instance, Bell Canada announced its Bell AI Fabric initiative in 2025, developing a data center supercluster in British Columbia with up to 500 MW of hydro-powered AI compute capacity. The project focuses on expanding sovereign AI infrastructure within Canada, reinforcing secure and sustainable data processing capabilities.

Expansion of Hyperscale and Edge Facilities Boosting Physical Security Investments

Hyperscale expansions by global cloud players and rising adoption of edge nodes elevate physical protection requirements. Operators install advanced perimeter detection, thermal cameras, and intrusion alarms to protect distributed assets. It ensures uninterrupted services in remote or urban hubs. The Canada Data Center Physical Security Market benefits from hybrid infrastructure development. Increasing data volume and latency-sensitive applications strengthen the business case for multi-layer systems. Enterprises consider security integration part of capital expenditure planning. Physical resilience directly links to uptime guarantees in service contracts. This trend cements security as a central factor in long-term asset reliability.

- For instance, eStruxture is developing the CAL-3 data center near Calgary, Alberta, with a planned capacity of 90 MW to support high-density AI and cloud workloads. The facility will feature modular design, Tier III standards, and advanced physical security including biometric access and 24/7 surveillance.

Market Trends

Market Trends

Shift Toward Unified Security Management Platforms for Centralized Control and Visibility

Operators move toward integrated command platforms connecting alarms, cameras, sensors, and access logs. The Canada Data Center Physical Security Market witnesses greater adoption of centralized dashboards that consolidate control rooms. Real-time analytics enable teams to track incidents across multiple sites. Unified systems reduce operational delays and maintenance costs. Vendors bundle analytics and automation within the same ecosystem. Centralized management simplifies compliance reporting under strict data privacy acts. Businesses achieve higher situational awareness across distributed facilities. Demand for interoperability between legacy and new systems strengthens long-term upgrade cycles.

Adoption of Cloud-Based Video Surveillance and Access Control Solutions

Cloud-native surveillance platforms gain adoption for scalability and cost efficiency. It enables data centers to manage security operations remotely through secure networks. Service providers host AI-driven video storage with real-time retrieval capabilities. Integration with mobile dashboards improves incident responsiveness for operators. The Canada Data Center Physical Security Market shows increasing shift from on-premise video systems to hybrid setups. Vendors introduce encrypted cloud control interfaces to prevent tampering. Enterprises benefit from seamless updates without disrupting operations. Growing remote work and distributed server models accelerate demand for virtualized physical security management.

Growing Use of Biometric Authentication and Multi-Factor Verification Tools

Enterprises increasingly replace traditional keycards with biometric and multi-factor authentication. Fingerprint, iris, and facial recognition technologies offer stronger protection at restricted zones. It reduces internal threat exposure and enhances accountability. Security developers refine recognition speed and accuracy through AI algorithms. The Canada Data Center Physical Security Market gains from corporate compliance programs mandating strict identity validation. Remote auditing tools record every access attempt, improving traceability. Demand from government and BFSI clients raises the adoption rate of advanced identity verification. Businesses treat access control analytics as a core KPI for operational safety.

Rising Focus on Green Security Infrastructure and Energy-Efficient Hardware Deployment

Operators aim to balance safety and sustainability by using energy-efficient security hardware. Low-power cameras, PoE access points, and intelligent LED perimeter systems reduce carbon footprint. The Canada Data Center Physical Security Market aligns with ESG goals of major operators. Firms introduce recyclable housing for cameras and sensors to meet environmental standards. AI helps optimize resource use during idle monitoring hours. Vendors develop modular devices compatible with renewable energy supply chains. Sustainability reporting drives enterprises to choose eco-friendly surveillance equipment. This trend links energy conservation with long-term brand positioning.

Market Challenges

Market Challenges

High Integration Costs and Complexity of Multi-Layer Security Deployments

The Canada Data Center Physical Security Market faces financial barriers due to high system integration costs. Many mid-tier facilities struggle to align legacy hardware with AI-enabled surveillance systems. Fragmented infrastructure increases setup time and operational overhead. Lack of unified vendor standards limits interoperability between equipment from different suppliers. Skilled technician shortages slow down deployment schedules. Small operators find it difficult to justify large upfront spending for modernization. It restricts overall upgrade momentum in rural or small data parks. Long payback cycles discourage some investors from full-scale automation.

Regulatory Ambiguity and Limited Awareness Among Secondary Operators

Unclear interpretation of certain data privacy mandates creates uncertainty in project planning. Smaller operators lack resources to navigate evolving compliance frameworks. The Canada Data Center Physical Security Market sees uneven adoption between metropolitan and regional centers. Gaps in awareness lead to underinvestment in monitoring technologies. Government subsidies focus on energy efficiency rather than security modernization. Absence of common certification models complicates benchmarking. Many data center tenants underestimate physical breach risks. This imbalance exposes facilities to potential liability during inspection or incident review.

Market Opportunities

Expansion of Colocation and Edge Infrastructure Creating New Security Investment Potential

Rapid rise in distributed data facilities generates a new wave of demand for modular protection systems. Edge and colocation players seek scalable tools to protect geographically dispersed infrastructure. It promotes stronger partnerships between OEMs and service integrators. The Canada Data Center Physical Security Market stands to gain from integrated cloud-managed security. Global investors eye regional projects that blend energy efficiency with cyber-physical resilience. New installations support predictive maintenance and AI-enabled surveillance grids. Enhanced automation opens recurring revenue channels for security software providers.

Rising Preference for Managed Security Services and Predictive Analytics Platforms

Data center operators prefer managed security contracts offering round-the-clock monitoring. Vendors expand service models to include predictive analytics for early risk detection. It allows operators to forecast incidents and reduce downtime. The Canada Data Center Physical Security Market benefits from rising subscription-based models. Predictive analytics help clients quantify ROI through measurable security performance. Partnerships with AI firms deliver faster adoption cycles. Managed services also fill workforce gaps, ensuring consistent system uptime and compliance.

Market Segmentation

By Data Center Size

Large data centers dominate due to heavy investments in hyperscale and colocation projects across major provinces. The Canada Data Center Physical Security Market gains momentum from rising traffic in enterprise facilities needing advanced perimeter defense. Medium-sized data centers expand protection budgets due to new cloud partnerships. Small facilities invest selectively in access control and video analytics. Demand concentrates around operators offering multi-site redundancy and scalable security options.

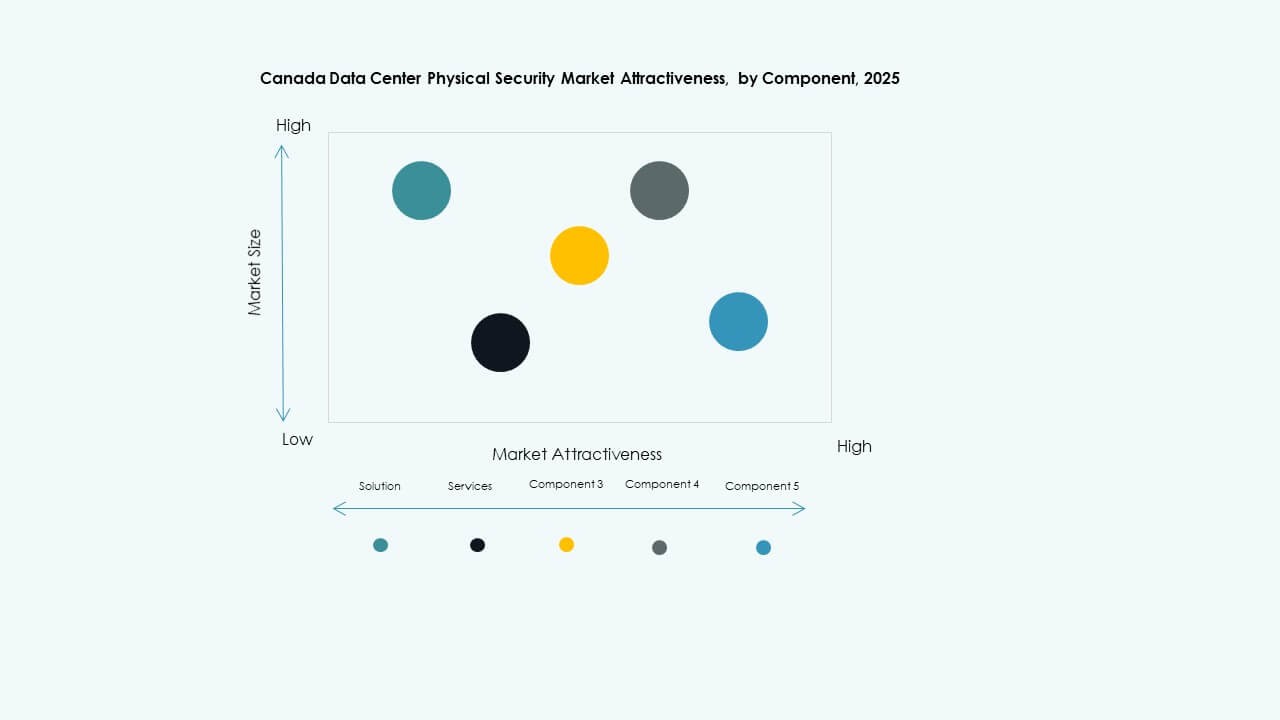

By Component

Solution segment leads the market, accounting for the majority of deployments across hyperscale and enterprise setups. The Canada Data Center Physical Security Market relies on hardware and software systems such as access control and intrusion detection. Service offerings, including consulting and integration, grow steadily as firms optimize their security architectures. Managed service contracts help operators streamline upgrades. Growing need for real-time monitoring sustains demand for end-to-end integrated packages.

By Solution

Access control holds the largest share, driven by widespread deployment of biometrics and card-based authentication systems. The Canada Data Center Physical Security Market also benefits from the rapid integration of video surveillance for visual verification. Monitoring and detection tools record continuous environmental data, improving response accuracy. Other subcategories include motion alarms and anti-tailgating sensors. Increasing complexity in facility layouts supports multi-layered solution adoption.

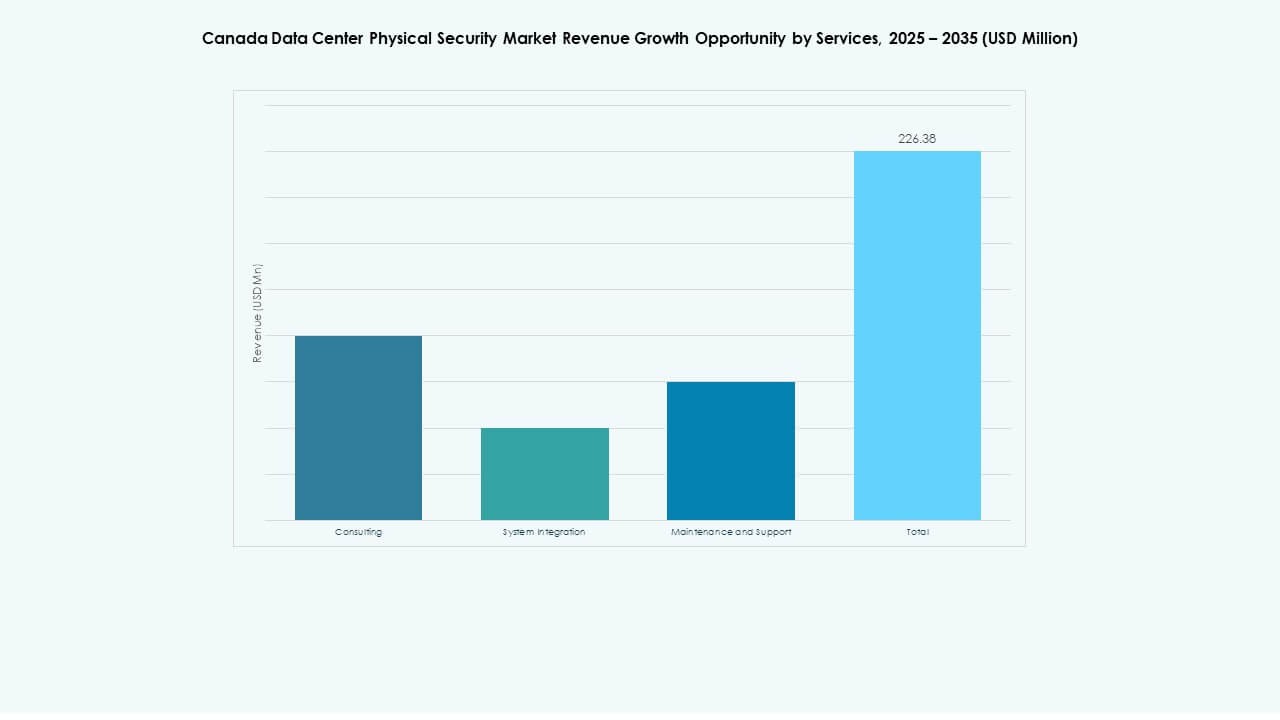

By Services

System integration remains the dominant service category, covering installation, networking, and testing of advanced physical security systems. The Canada Data Center Physical Security Market experiences rising demand for consulting, especially among Tier II data centers planning modernization. Maintenance and support services hold recurring revenue value as operators require continuous uptime. Service providers adopt predictive maintenance analytics to reduce costs. The growth of multi-tenant environments sustains service diversity.

By Security Layer

Perimeter security dominates with strong demand for intrusion detection and intelligent fence systems. The Canada Data Center Physical Security Market sees high growth in building access and data hall protection layers. Rack-level protection rises due to internal threat awareness. Vendors integrate layered security models to meet strict compliance mandates. Facilities deploy compartmentalized controls ensuring minimal breach propagation.

By Data Center Type

Hyperscale facilities lead market share due to global cloud investments. The Canada Data Center Physical Security Market also gains support from enterprise and colocation centers. Edge facilities emerge quickly, requiring compact yet powerful security setups. Vendors tailor hybrid products to meet diverse architectural needs. Growth across multiple data center types drives innovation in modular security solutions.

By End-user

IT & Telecom dominates due to heavy reliance on secure hosting environments for network operations. BFSI follows with demand for Tier IV facilities ensuring complete physical isolation. The Canada Data Center Physical Security Market benefits from healthcare and government demand for data sovereignty compliance. Retail and e-commerce firms modernize logistics platforms to include protected cloud storage. Manufacturing and others adopt industrial IoT safeguards to secure on-premise data infrastructure.

Regional Insights

Regional Insights

Eastern Canada (Ontario and Quebec) – The Core of Data Center Infrastructure Development

Eastern Canada contributes nearly 60% of the Canada Data Center Physical Security Market share. Toronto and Montréal anchor the country’s data hub ecosystem, hosting global hyperscale operators. These provinces prioritize smart perimeter and biometric authentication technologies. It drives partnerships between local integrators and multinational security firms. Favorable energy costs and climate conditions strengthen infrastructure expansion. Provincial governments encourage digital investment, reinforcing the region’s leadership in physical security adoption.

- For instance, QScale’s Q01 campus in Quebec delivers 142 MW of IT capacity and supports liquid-cooled racks exceeding 600 kW per cabinet. The facility operates on renewable hydropower and features a waste-heat recovery system designed to reuse excess energy for nearby applications, reflecting Quebec’s focus on sustainable, high-density data infrastructure.

Western Canada (British Columbia and Alberta) – Emerging Hubs for Edge and Cloud Expansion

Western Canada accounts for about 25% of the market, driven by emerging cloud campuses in Vancouver and Calgary. Rising deployment of edge computing nodes creates fresh demand for modular surveillance systems. It enhances real-time analytics performance in dispersed areas. Energy-efficient equipment supports sustainability-focused infrastructure projects. The Canada Data Center Physical Security Market in these provinces benefits from investment incentives and land availability. Regional connectivity upgrades sustain consistent market expansion.

- For instance, eStruxture’s MTL4 facility in Montreal delivers up to 16 MW of power capacity with Tier III design standards. It features 24/7 on-site security, biometric access, and video surveillance, reflecting strong physical protection measures across scalable, modular data infrastructure in Canada.

Atlantic and Central Canada – Niche Growth Driven by Government and Research Facilities

Atlantic and Central regions together hold close to 15% market share. Growth stems from government data projects and defense communication systems. Public sector initiatives demand high compliance physical security. It encourages use of advanced monitoring and controlled access systems. The Canada Data Center Physical Security Market expands in research zones such as Ottawa and Halifax. Local data hosting and academic networks sustain the region’s long-term relevance.

Competitive Insights:

- CyberSapiens

- Bell Canada

- Telus

- IBM Canada

- ASSA ABLOY

- ABB

- Axis Communications AB

- Bosch Sicherheitssysteme GmbH

- Cisco Systems, Inc.

- Fortinet

- Genetec

- Honeywell International Inc.

- Johnson Controls

- Palo Alto Networks

- Schneider Electric SE

- Securitas

- Siemens AG

- Others

The Canada Data Center Physical Security Market shows strong competition among key providers. ABB offers integrated power and security systems for hyperscale sites. ASSA ABLOY specializes in biometric access control across enterprise campuses. Axis and Bosch deliver robust video surveillance suites with analytics. Cisco and Fortinet embed network security into physical security setups. Genetec focuses on unified security management software solutions. Honeywell ensures presence across global premises with its legacy control systems. Johnson Controls integrates HVAC, fire, and security services to attract large facilities. Schneider Electric tailors modular power and access solutions for edge centers. Buyers benefit from diversified portfolios and competitive pricing across categories.

Recent Developments:

- In September 2025, Bell Canada officially launched Bell Cyber, a new brand focused on AI-powered cybersecurity solutions. Bell Cyber complements Bell’s existing technology services, offering next-generation Security-as-a-Service (SECaaS) with partnerships involving global tech leaders such as Palo Alto Networks, Cisco, Microsoft.

- In December 2024, Bell Canada formed a strategic partnership with Palo Alto Networks , intensifying its security solutions for businesses across Canada. This partnership included offering a full suite of services across Palo Alto Networks’ AI-powered cybersecurity platforms like Cortex XSIAM, which centralizes security operations and automates incident response.

- In July 2024, Bell Canada acquired two tech services companies, Stratejm and CloudKettle Inc., to strengthen its managed cybersecurity and Salesforce capabilities for enterprises. This acquisition enhanced Bell’s platform for end-to-end AI-powered service solutions, focusing on managed security solutions and real-time threat detection, aiming to deliver comprehensive cybersecurity for Canadian businesses.