Executive Summary:

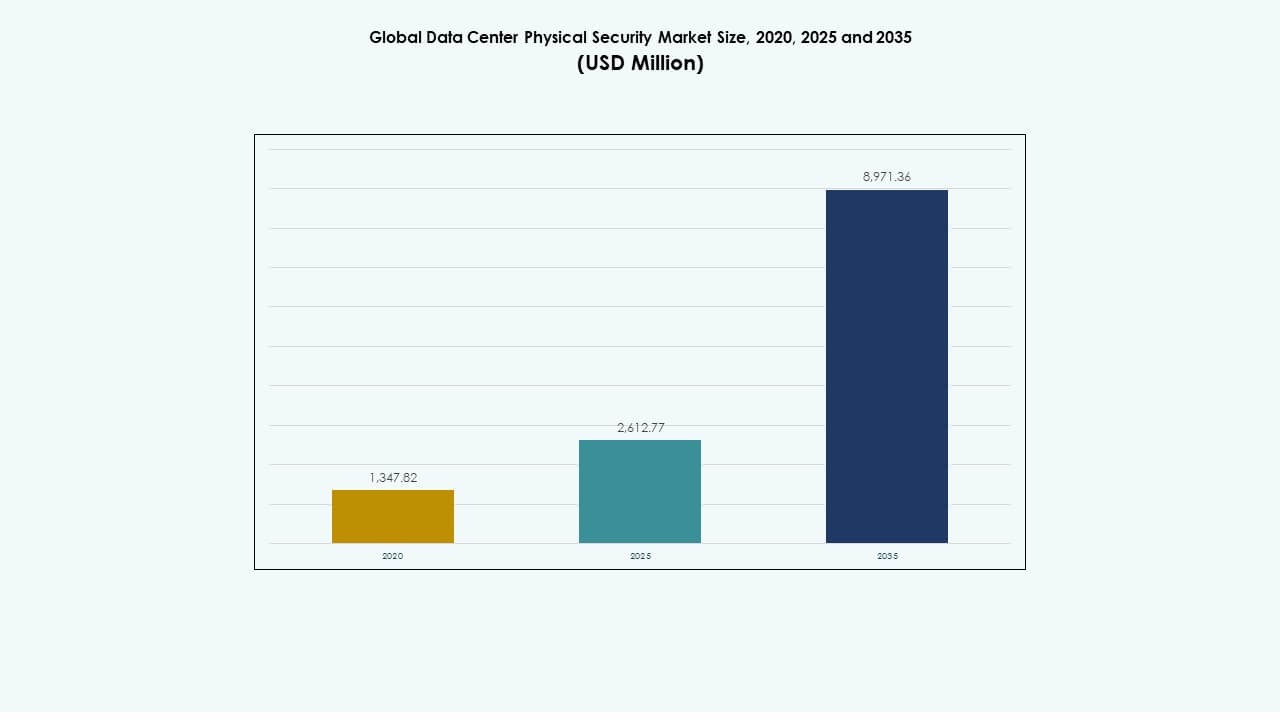

The Global Data Center Physical Security Market size was valued at USD 1,347.82 million in 2020 to USD 2,612.77 million in 2025 and is anticipated to reach USD 8,971.36 million by 2035, at a CAGR of 13.07% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2035 |

| Data Center Physical Security Market Size 2025 |

USD 2,612.77 Million |

| Data Center Physical Security Market, CAGR |

13.07% |

| Data Center Physical Security Market Size 2035 |

USD 8,971.36 Million |

Market expansion is driven by strong adoption of biometric access tools, AI-enabled surveillance units, and integrated monitoring platforms that secure complex facilities. Operators invest in multi-layer defense systems that support high-density workloads and rising data traffic. Innovation in identity intelligence and automated threat detection strengthens operational reliability. The market holds strategic value for businesses due to its ability to protect core digital infrastructure, while investors gain long-term confidence from consistent demand across cloud and colocation development.

North America leads due to mature hyperscale activity and strict regulatory standards that reinforce advanced deployment. Europe maintains strong growth supported by robust compliance frameworks. Asia Pacific emerges as the fastest-growing zone as cloud expansion accelerates across major economies. The Middle East and Latin America build momentum through new digital infrastructure programs. Africa continues to advance with rising telecom-driven data center development.

Market Drivers

Market Drivers

Growing Demand For Advanced Multi-Layer Physical Defense Across High-Density Facilities

Operators invest in stronger protection due to rising intrusion threats and higher data traffic. It pushes firms to deploy multi-layer defense systems that reduce breach risk across core sites. Businesses adopt biometric access tools that strengthen identity validation for restricted rooms. Vendors introduce AI-ready surveillance units that support real-time threat flags. Enterprises link alarms, sensors, and cameras under unified platforms that cut manual errors. Investors view the Global Data Center Physical Security Market as a stable long-term asset due to rising digital reliance. Operators upgrade legacy hardware that no longer meets new compliance rules. Stakeholders seek scalable systems that support diverse layouts and wider operational needs.

- For instance, ASSA ABLOY’s HID iCLASS SEOS ecosystem is deployed across large U.S. data centers and supports secure mobile, card, and biometric credentialing, meeting FIDO and ISO/IEC 7816 standards for encrypted identity management across restricted rooms.

Rapid Expansion Of Cloud, Colocation, And Hyperscale Projects Driving New Security Procurement Cycles

The surge in new facilities fuels demand for smart entry control, automated monitoring, and stronger perimeter zones. Operators seek integrated systems that match high-capacity racks and dense server halls. It encourages wider adoption of motion analytics that help detect route deviation near secure areas. Firms expand procurement to include hardened racks that block unauthorized cabinet access. Cloud regions require high-grade tools that meet global audit rules across multiple tenant groups. The Global Data Center Physical Security Market gains steady traction from rising colocation builds across major hubs. Long-term contracts with carriers push vendors to extend support for diverse architectures. Stakeholders prefer upgrade paths that keep disruption low.

Shift Toward AI-Enabled Surveillance, Identity Intelligence, And Centralized Security Orchestration Platforms

AI tools improve detection accuracy and support real-time tracking across multiple floors. Operators deploy analytics that read abnormal posture, shadow zones, and route breaks. It supports proactive response models that reduce breach time. Identity intelligence systems raise control precision across sensitive data halls. Firms embed continuous verification tools that track user patterns for high-risk zones. The Global Data Center Physical Security Market gains from deeper fusion between video data and access logs. Vendors offer orchestration layers that link every tool under one dashboard. Enterprises push for automation to cut human error.

- For instance, Axis Communications’ Q1656 network camera uses the ARTPEC-8 chip with deep-learning processing and supports real-time object classification for data center corridors, delivering analytics accuracy improvements documented through Axis’s Edge AI benchmarks.

Rising Compliance Pressure, Cyber-Physical Convergence, And Demand For Zero-Trust Facility Governance

Regulators push firms to adopt stronger controls for tenant segregation and asset safety. Operators enforce zero-trust entry rules that validate every movement in secure zones. It drives usage of mobile credentials, anti-tailgating units, and multi-factor access. Cyber-physical alignment helps firms manage breach attempts across networks and entry points. Investors support platforms that reduce legal risk and protect uptime. The Global Data Center Physical Security Market benefits from greater adoption of secure-by-design layouts. Vendors provide audit trails that help firms meet global security frameworks. Stakeholders expect constant upgrades due to evolving threat patterns.

Market Trends

Market Trends

Growing Integration Of Autonomous Patrol Robots, Smart Drones, And Sensor-Rich Perimeter Units

Firms test robotic patrol units that monitor large compounds with steady precision. Operators use perimeter drones that cover long stretches faster than manual rounds. It helps teams detect motion, heat, and vibration changes with high accuracy. Robotic fleets reduce repetitive tasks and raise visibility across external fences. Vendors add smart analytics that help predict breach zones. The Global Data Center Physical Security Market records rising adoption of remote patrol systems across hyperscale parks. Drones create strong deterrence for night-time intrusion attempts. Enterprises explore hybrid fleets that blend robots with fixed sensors.

Higher Adoption Of Cloud-Managed Security Platforms And Remote Visibility For Distributed Sites

Operators shift to cloud systems that manage access rights, video feeds, and alerts from central teams. It supports real-time visibility across multi-region footprints. Firms reduce hardware use by moving storage to cloud vaults. Remote command centers gain control over all doors, racks, and perimeter nodes. Service providers offer configuration tools that handle growing tenants. The Global Data Center Physical Security Market benefits from strong interest in unified cloud dashboards. Vendors enhance encryption for secure data flow. Stakeholders value fast scalability for new sites.

Growing Use Of Digital Twins For Security Planning, Threat Simulation, And Capacity Optimization

Teams build digital twins that map halls, racks, and control zones. It helps operators simulate breach attempts and plan countermeasures. Digital layouts support better placement of cameras, badges, and alarms. Firms use simulation data to fine-tune staffing models. Predictive insights help reduce blind spots before physical changes. The Global Data Center Physical Security Market adopts digital twins across large campuses that manage heavy traffic. Vendors expand toolkits that link real-time feeds to digital models. Decision makers gain stronger insight across complex layouts.

Expansion Of Biometric-First Identity Systems And Mobile-Credential Replacement Models

Operators install facial, iris, and palm-vein systems that deliver high accuracy. It raises identity assurance for critical areas. Mobile credentials reduce dependency on cards that risk loss or misuse. Biometric units restrict entry to verified personnel. Vendors refine algorithms to support faster throughput. The Global Data Center Physical Security Market moves toward full biometric ecosystems across dense sites. Firms deploy multi-factor checks for rack entry. Stakeholders support biometric models due to stronger audit trails.

Market Challenges

Escalating Threat Sophistication, High Deployment Cost, And Complexity Across Multi-Site Environments

Threat actors use advanced breach tools that bypass older access solutions. Operators face rising pressure to upgrade systems across large campuses. It increases cost for specialized sensors and tightly integrated platforms. Firms struggle with varied layouts that need custom deployment. Maintenance cost rises due to nonstop operational hours. The Global Data Center Physical Security Market deals with complex integration needs across legacy rooms. Vendors manage compatibility issues that delay upgrades. Stakeholders need trained teams for round-the-clock oversight.

Regulatory Pressure, Skill Shortages, And Limited Interoperability Between Security Tools

Regulators demand strict audits that challenge firms with weak documentation. It creates tension for operators that manage global sites with diverse rules. Skill gaps slow adoption of AI-ready tools. Security teams face difficulty aligning hardware with software from different vendors. Limited interoperability reduces system efficiency. The Global Data Center Physical Security Market faces integration strain across international projects. Teams spend more time validating data flows. Stakeholders need better vendor coordination.

Market Opportunities

Market Opportunities

Expansion Of Hyperscale Builds, Rising Edge Deployment, And Need For Flexible Multi-Tenant Security Models

Hyperscale growth fuels demand for advanced access control, AI vision, and smart sensors. Edge sites create need for compact platforms that secure small rooms. It raises opportunity for plug-and-play hardware that fits distributed networks. Multi-tenant sites adopt tools that ensure tight segregation. Vendors support dynamic ID rules that fast-track onboarding. The Global Data Center Physical Security Market benefits from new zones in telecom and cloud networks. Firms explore remote operation tools. Stakeholders view distributed nodes as a priority area.

Growth Of Automation, Real-Time Analytics, And Predictive Security Intelligence

Automation tools reduce manual checks and lower security downtime. Predictive engines detect pattern shifts in active hallways. It helps operators stop breaches early. Vendors add analytics that track anomalies across racks and cabinets. Firms invest in unified dashboards that monitor all devices. The Global Data Center Physical Security Market gains momentum from AI-ready upgrades. Teams use insights to redesign floor layouts. Stakeholders value improved uptime.

Market Segmentation

Market Segmentation

By Data Center Size

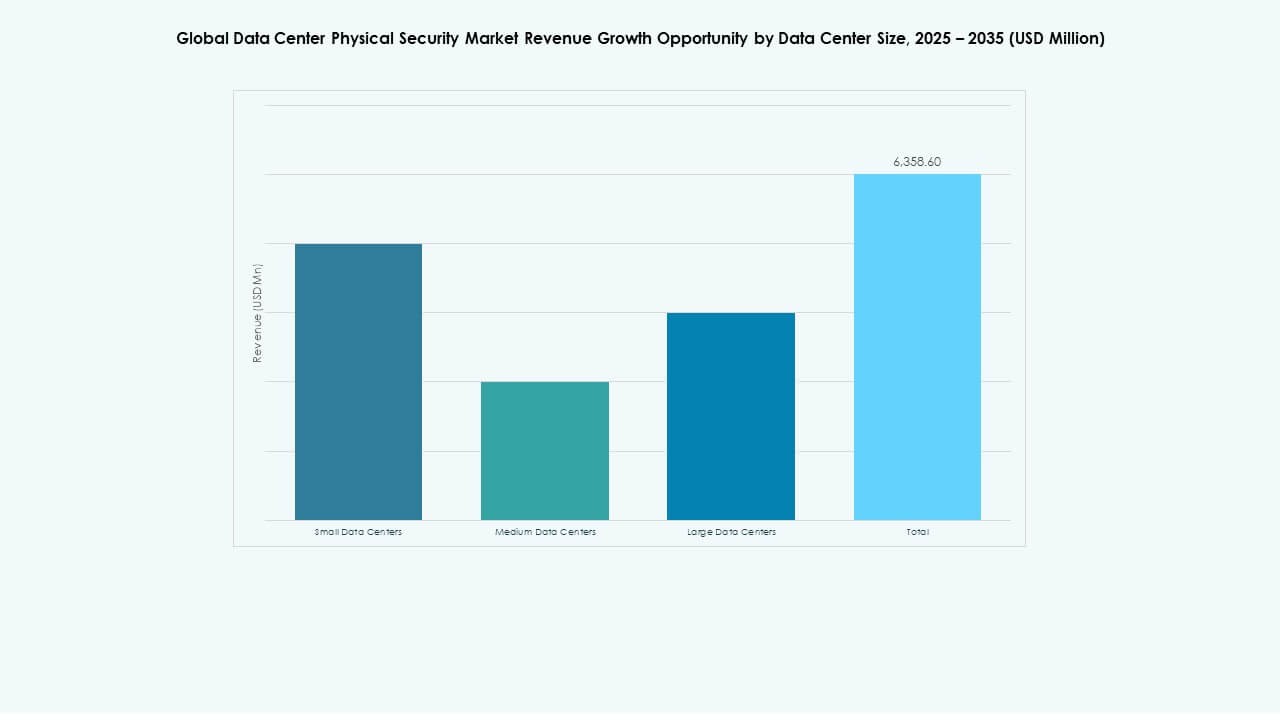

Small data centers record steady growth due to rising demand for compact layouts that support remote workloads. Medium facilities gain stronger traction due to balanced construction cost and reliable expansion capacity. Large data centers hold the dominant share due to higher rack density and stronger investment. The Global Data Center Physical Security Market benefits from rising security need across hyperscale-linked large blocks. Operators deploy advanced controls that protect multiple tenant groups. Strategic upgrades raise visibility across all zones. Vendors focus on automated tools for complex environments.

By Component

The solution segment leads due to strong adoption of surveillance, access control, and detection tools. Firms prefer integrated solutions that manage real-time alerts across diverse halls. Services grow due to higher deployment needs across global sites. The Global Data Center Physical Security Market gains from rising installation support across new builds. Vendors offer consulting models that align designs with global standards. Operators invest in lifecycle maintenance for uptime protection. Solutions continue to hold the largest share due to direct impact on breach control.

By Solution

Video surveillance holds the largest share due to its role in real-time monitoring across large campuses. Access control grows as firms shift to biometric and mobile credential systems. Monitoring and detection gain wider use due to rising sensor accuracy. The Global Data Center Physical Security Market supports multi-layer setups that combine all tools. Operators deploy strong ID systems for high-risk rooms. Vendors expand analytic features across cameras. Firms adopt advanced motion tools for perimeter and hall safety.

By Services

System integration dominates due to the need for unified platforms that manage dense layouts. Consulting plays a key role in planning secure facility upgrades. Maintenance and support grow due to nonstop operations across data halls. The Global Data Center Physical Security Market depends on strong integration for long-term reliability. Vendors help firms link legacy hardware with new modules. Services ensure smoother deployment and lower downtime. Teams rely on expert support for compliance audits.

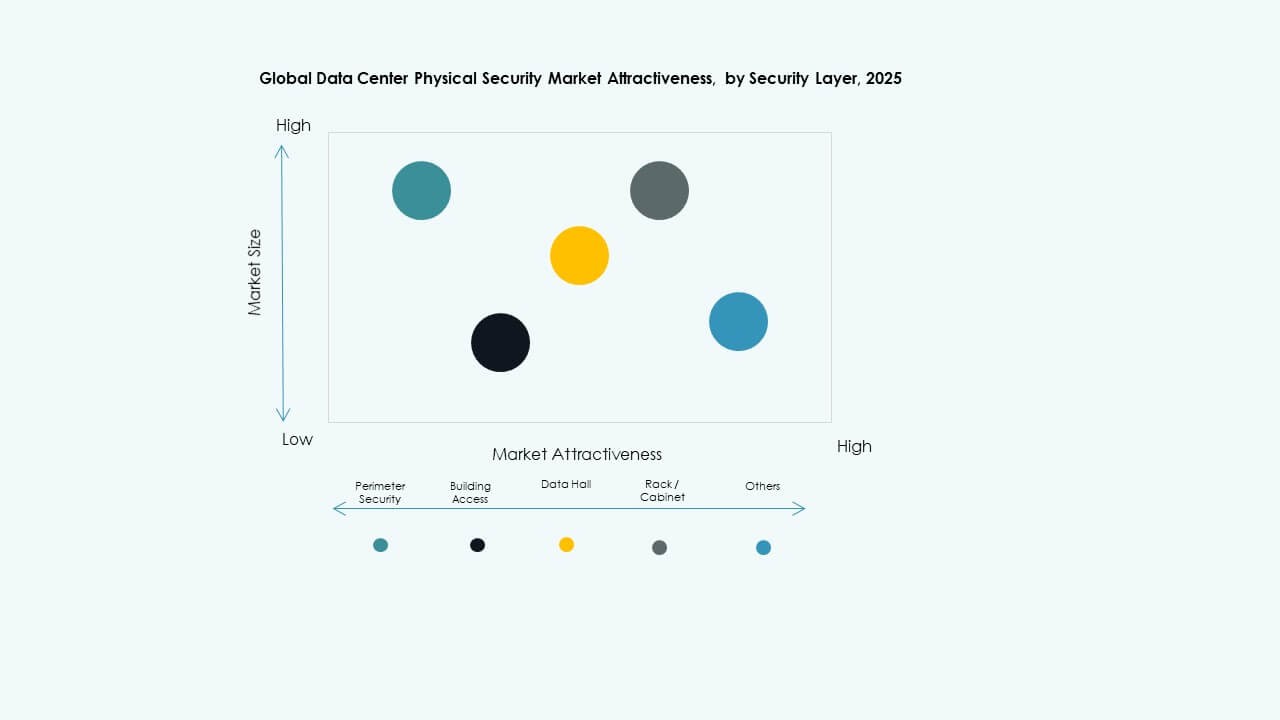

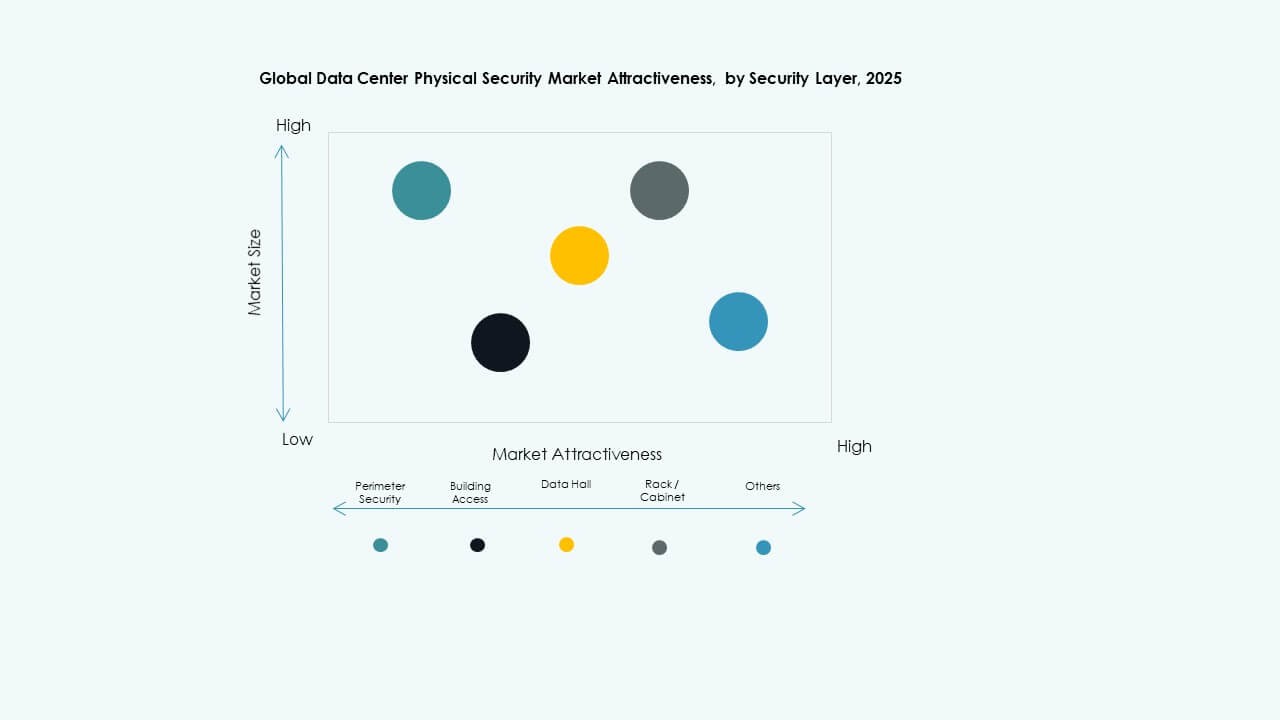

By Security Layer

Perimeter security holds strong share due to high risk at external zones. Building access systems grow with wider use of biometrics and smart IDs. Data hall protection gains traction due to sensitive assets in core rooms. The Global Data Center Physical Security Market supports multi-layer control for large campuses. Rack and cabinet tools rise due to stronger segmentation needs. Operators deploy anti-tailgating units to reduce breach attempts. Vendors deliver layered models that cover every zone.

By Data Center Type

Hyperscale facilities dominate due to massive construction activity and strict security rules. Colocation sites grow with rising tenant volume across global hubs. Enterprise data centers maintain steady demand due to internal workloads. The Global Data Center Physical Security Market expands across edge nodes that support low-latency tasks. Operators secure distributed rooms with compact tools. Vendors supply scalable kits for hybrid setups. Hyperscale remains the leading segment.

By End-user

IT and telecom lead due to heavy reliance on critical digital infrastructure. BFSI follows due to high compliance pressure. Government and defense maintain strong focus on secure rooms. The Global Data Center Physical Security Market sees rising use across healthcare and retail due to growing digital records. Manufacturing sites strengthen access controls across automated lines. Vendors support wide adoption across regulated sectors. Operators invest in high-trust environments.

Regional Insights:

Regional Insights:

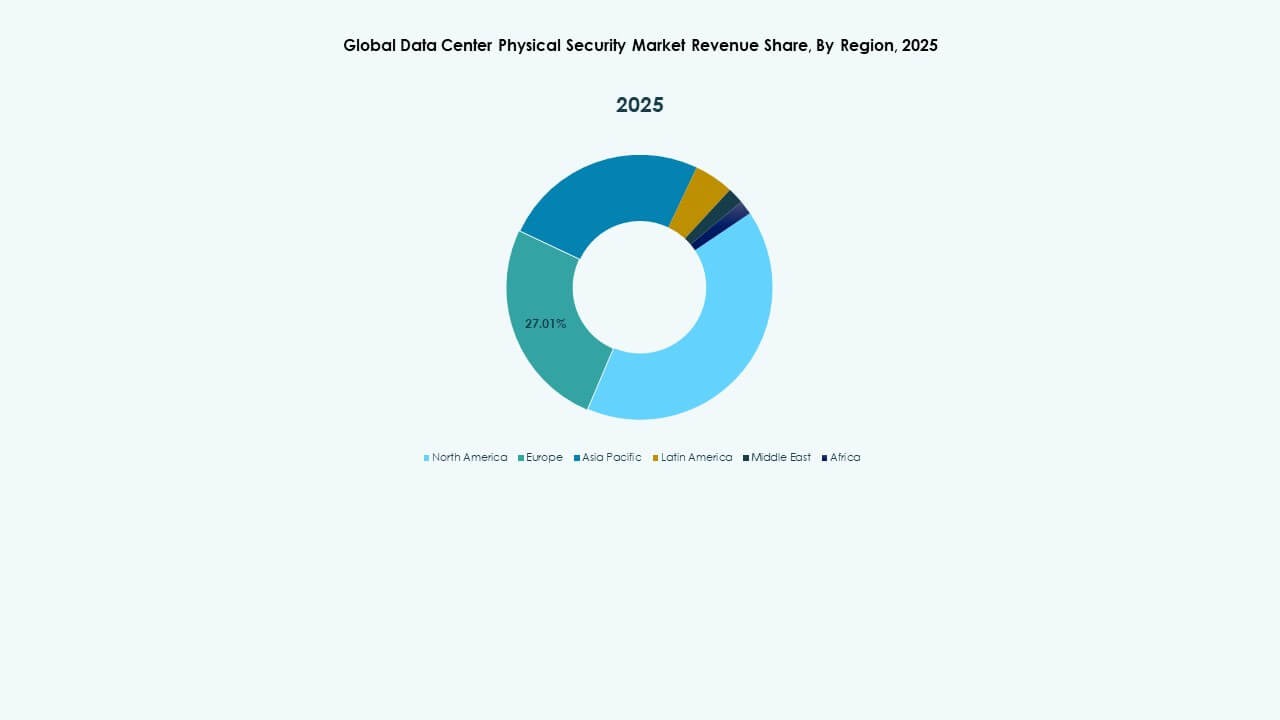

North America

The North America Global Data Center Physical Security Market size was valued at USD 552.88 million in 2018 to USD 1,044.32 million in 2024 and is anticipated to reach USD 3,565.67 million by 2032, at a CAGR of 13.01% during the forecast period. Regional market share in 2024: 39.97%. North America leads due to strong hyperscale expansion and strict compliance rules. Operators deploy biometric systems, AI video tools, and multi-layer access controls across new campuses. It benefits from advanced integration platforms that support real-time visibility. Cloud firms invest in high-grade perimeter units that secure large compounds. Vendors introduce analytics that read behavioral shifts near restricted areas. Regional enterprises enforce rigorous audit trails across racks and halls. The Global Data Center Physical Security Market gains strong momentum from U.S. dominated builds. Investment grows with rising colocation demand across major tech hubs.

- For instance, Honeywell’s Pro-Watch Intelligent Command integrates up to 225,000 access control devices in one platform, supporting unified monitoring across large U.S. data center campuses.

Europe

The Europe Global Data Center Physical Security Market size was valued at USD 388.04 million in 2018 to USD 705.71 million in 2024 and is anticipated to reach USD 2,277.83 million by 2032, at a CAGR of 12.38% during the forecast period. Regional market share in 2024: 27.01%.

Europe holds a strong position due to strict regulatory standards and structured certification rules. Operators upgrade access control, identity tools, and surveillance units to match evolving privacy frameworks. It benefits from rising demand across Germany, the UK, and the Nordics. Edge sites in dense cities need compact tools that maintain high uptime. Vendors deliver integrated systems that connect cyber and physical layers. Colocation operators expand secure halls to support multi-tenant growth. The Global Data Center Physical Security Market grows steadily across regulated sectors. Firms allocate high budgets to maintain operational trust.

Asia Pacific

The Asia Pacific Global Data Center Physical Security Market size was valued at USD 284.39 million in 2018 to USD 632.29 million in 2024 and is anticipated to reach USD 2,457.71 million by 2032, at a CAGR of 14.45% during the forecast period. Regional market share in 2024: 24.20%. Asia Pacific emerges as the fastest-growing region due to rapid cloud adoption across major economies. Operators deploy AI surveillance, perimeter sensors, and biometric entry systems across dense builds. It supports large-scale construction in China, India, Japan, and South Korea. New digital policies drive investment in secure facility infrastructure. Vendors supply scalable hardware that fits diverse layouts. Colocation and hyperscale firms expand aggressively across metro clusters. The Global Data Center Physical Security Market gains traction from telecom-led digital acceleration. Regional growth remains strong due to high data traffic.

Latin America

The Latin America Global Data Center Physical Security Market size was valued at USD 67.12 million in 2018 to USD 128.03 million in 2024 and is anticipated to reach USD 399.23 million by 2032, at a CAGR of 11.99% during the forecast period. Regional market share in 2024: 4.90%. Latin America expands due to rising demand for cloud services and secure colocation sites. Operators adopt video analytics, identity tools, and access barriers across new hubs. It benefits from national digital upgrades across Brazil, Chile, and Mexico. Vendors support modular deployments that suit midsize facilities. Regional firms focus on perimeter reinforcement to counter external risks. Government projects drive investment in controlled environments. The Global Data Center Physical Security Market strengthens through partnerships with global cloud firms. Demand rises from enterprise migration to modern data infrastructure.

- For instance, Genetec’s Security Center unified platform deployed in Latin American facilities supports up to 300,000 cardholder identities in a single system, improving high-density access management.

Middle East

The Middle East Global Data Center Physical Security Market size was valued at USD 36.26 million in 2018 to USD 67.15 million in 2024 and is anticipated to reach USD 185.26 million by 2032, at a CAGR of 10.57% during the forecast period. Regional market share in 2024: 2.57%.

The Middle East grows due to rising national cloud zones and high-security digital programs. Operators deploy biometric entry points, rack protection units, and advanced thermal cameras. It benefits from government-backed digital infrastructure plans. Vendors supply rugged systems suited for large outdoor compounds. Regional firms invest in multi-layer defense to counter physical intrusion risk. Hyperscale builders expand presence across GCC corridors. The Global Data Center Physical Security Market gains traction from new-edge deployments. Growth remains steady with strong interest in compliance-led upgrades.

Africa

The Africa Global Data Center Physical Security Market size was valued at USD 19.14 million in 2018 to USD 35.27 million in 2024 and is anticipated to reach USD 85.68 million by 2032, at a CAGR of 9.31% during the forecast period. Regional market share in 2024: 1.35%.

Africa moves forward with gradual expansion of regional data centers across major economies. Operators add smart surveillance, perimeter sensors, and controlled entry systems to improve site protection. It observes rising interest from telecom-led cloud projects. Vendors introduce compact solutions that meet cost and space limits. Firms enhance cabinet-level security to reduce unauthorized access. Growth links to national digital transformation programs. The Global Data Center Physical Security Market records consistent progress in South Africa, Nigeria, and Kenya. Regional adoption strengthens with new enterprise workloads.

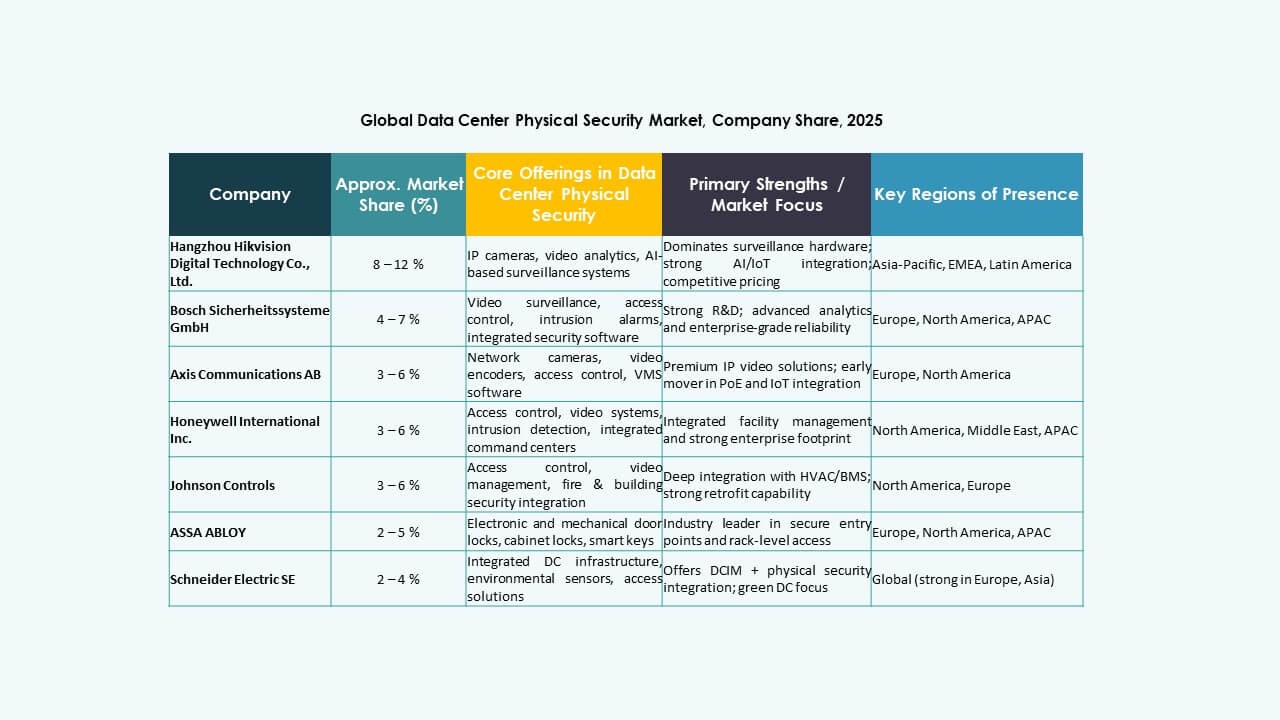

Competitive Insights:

Competitive Insights:

- ABB

- Allied Universal

- ASSA ABLOY

- Axis Communications AB

- Bosch Sicherheitssysteme GmbH

- Cisco Systems, Inc.

- Fortinet

- Genetec

- Hangzhou Hikvision Digital Technology Co., Ltd.

- Honeywell International Inc.

- Johnson Controls

- Palo Alto Networks

- Schneider Electric SE

- Securitas

- Siemens AG

Global Data Center Physical Security Market features a mix of diversified conglomerates and focused specialists. Global leaders such as Honeywell, Johnson Controls, Schneider Electric, and Siemens offer broad portfolios. They bundle access control, surveillance, and building systems into integrated platforms. Network and cybersecurity vendors like Cisco, Fortinet, and Palo Alto Networks extend portfolios into edge gateways and secure connectivity. Physical guarding and managed service firms Securitas expand bundled security operations contracts. Video surveillance specialists Axis Communications and Hikvision drive camera innovation and analytics features. Competition centers on platform openness, API depth, and lifecycle service capability. It pushes vendors toward strategic alliances with cloud providers, colocation operators, and integrators. Price pressure remains strongest in hardware, while recurring software and services sustain margins.

Recent Developments:

Recent Developments:

- In October 2025, ASSA ABLOY acquired Kentix GmbH, a German company specializing in monitoring and access control products designed for data centers, enhancing their capabilities in physical security for this sector.

- In January 2025, ASSA ABLOY also acquired InVue, a Charlotte-based provider of asset protection and access control solutions, aligning with their strategy to expand globally in access control and asset protection.