Executive summary:

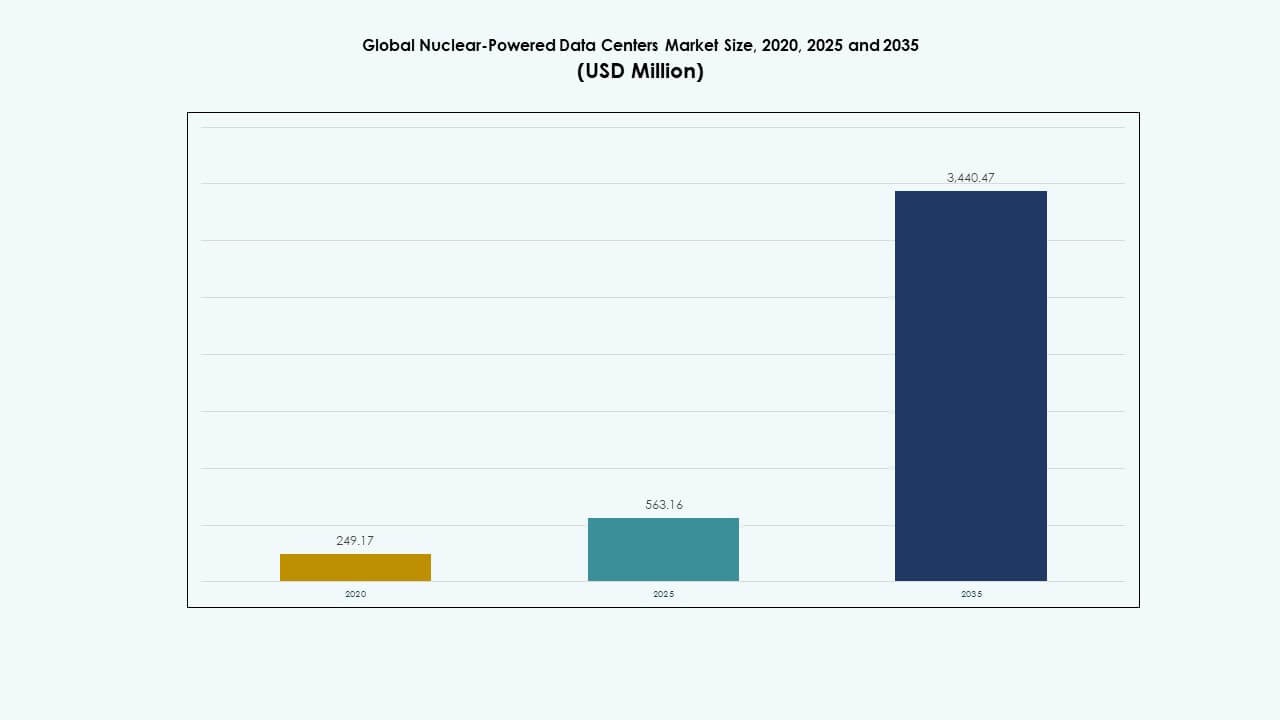

The Global Nuclear-Powered Data Centers Market size was valued at USD 249.17 million in 2020, reached USD 563.16 million in 2025, and is anticipated to reach USD 3,440.47 million by 2035, at a CAGR of 20.26% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2035 |

| Nuclear-Powered Data Centers Market Size 2025 |

USD 563.16 Million |

| Nuclear-Powered Data Centers Market, CAGR |

20.26% |

| Nuclear-Powered Data Centers Market Size 2035 |

USD 3,440.47 Million |

Market growth is driven by the need for reliable, carbon-free energy to support growing AI and cloud workloads. Small modular reactors (SMRs) and microreactors are gaining traction due to their scalability and ability to provide uninterrupted power in remote and hyperscale environments. Regulatory support, rising data demands, and energy security concerns are pushing operators to consider nuclear solutions. The shift toward long-term sustainability and digital resilience positions this market as strategically critical for future data infrastructure investments.

North America leads the market due to strong nuclear infrastructure, hyperscale expansion, and government-backed SMR pilots. Europe is accelerating adoption through energy diversification strategies and digital sovereignty goals, with France and the Netherlands showing early deployment activity. Asia-Pacific is emerging, led by China, South Korea, and Japan investing in SMR innovation and edge deployments. These regions drive growth through technology readiness, policy alignment, and demand for uninterrupted power.

Market Dynamics:

Market Dynamics:

Demand for Sustainable and Resilient Power Solutions in Digital Infrastructure

The Global Nuclear-Powered Data Centers Market is driven by rising demand for sustainable and continuous power. Large-scale data centers require 24/7 electricity with minimal disruption. Nuclear energy offers a stable, low-carbon source that meets uptime needs without dependency on weather conditions. Conventional renewables face intermittency, while diesel backup fails sustainability tests. Government climate goals push operators toward zero-emission strategies. Nuclear systems, especially small modular reactors (SMRs), align well with these requirements. Their compact design fits within existing campus footprints. Long fuel cycles reduce logistical complexity in remote operations. This shift positions nuclear as a strategic asset for next-gen data infrastructure.

Adoption of Small Modular Reactors for Scalable Onsite Deployment

SMRs enable flexible integration of nuclear energy into hyperscale and edge computing facilities. Traditional large reactors are impractical for urban or space-constrained areas. SMRs, by contrast, support modular expansion with reduced siting risks. Vendors are designing nuclear units specifically for mission-critical environments like data centers. This approach supports both remote and urban sites with grid-independence. The technology offers multi-decade operational lifespans with low maintenance requirements. It appeals to hyperscale developers seeking operational predictability. Several governments support SMR pilot deployments, lowering initial barriers. The Global Nuclear-Powered Data Centers Market benefits from this regulatory and design momentum.

- For example, Standard Power announced a 2023 agreement with NuScale Power to develop nearly 2 GW of SMR capacity at sites in Ohio and Pennsylvania, with first modules targeting deployment by 2029 for hyperscale data center power needs.

Regulatory Support and Private-Sector Investment in Nuclear Digitization Projects

Public policy frameworks are evolving to support non-utility nuclear energy users. National energy security policies now include provisions for industrial and data workloads. Licensing pathways for small reactors near data campuses are under development in multiple regions. Regulatory sandbox initiatives fast-track demonstration projects. Private firms are investing in partnerships with nuclear developers for long-term site power. This collaboration helps reduce reliance on fossil-fuel grids. Financial institutions are offering green financing tied to nuclear integration. The Global Nuclear-Powered Data Centers Market reflects these growing alliances between energy and digital sectors. This convergence opens new long-term value channels for stakeholders.

Rising Global Data Traffic Demands Supporting Onsite Power Independence

Explosive growth in AI, cloud, and 5G workloads increases demand for distributed compute. Traditional power grids face growing stress from peak loads and climate variability. Data center operators seek energy independence to protect against instability and outages. Nuclear options offer both independence and emissions-free baseload operation. Integrated nuclear systems reduce the need for large grid interconnections. It enables faster deployment of Tier IV data centers in underserved regions. Operators gain resilience from internalized power ecosystems. The Global Nuclear-Powered Data Centers Market supports this trend through enabling localized power control. It helps reduce energy costs and improve service reliability.

- For instance, Green Energy Partners acquired 641 acres in Virginia in 2023 to develop a nuclear-powered energy park featuring 4–6 SMRs and 20–30 data centers, targeting resilient, emissions-free infrastructure for next-generation computing.

Market Trends

Market Trends

Integration of Digital Twins and Predictive Monitoring in Nuclear Systems

Vendors are embedding digital twin technology in nuclear microgrids for data centers. These models simulate real-time operations, allowing predictive fault detection and optimization. AI-enhanced diagnostics improve performance forecasting and component life tracking. Predictive analytics reduce downtime risk and optimize fuel cycles. Data centers gain visibility into thermal, electrical, and safety systems. This trend ensures tight integration between IT workloads and reactor behavior. It enables automation of load balancing and cooling systems. The Global Nuclear-Powered Data Centers Market incorporates such tools to ensure efficiency. This digital-physical integration supports advanced operational intelligence at scale.

Use of Heat Reuse and Cogeneration from Nuclear-Linked Facilities

Heat reuse is gaining interest in nuclear-powered data centers as part of energy efficiency efforts. Nuclear plants generate substantial low-grade heat during operation. Co-located data centers now explore heat recovery for district heating or industrial processes. This cogeneration approach offsets local utility loads and creates energy-sharing ecosystems. Projects in colder regions are especially suitable for this reuse. Infrastructure vendors develop thermally integrated campus designs. It helps reduce carbon footprints across the full energy chain. The Global Nuclear-Powered Data Centers Market taps into this synergy to expand sustainability metrics. It enhances value through multi-use energy systems.

Emergence of Nuclear-Marine Platforms for Offshore Data Operations

Some developers are exploring marine nuclear data centers for offshore or coastal operations. These platforms offer secure locations with direct cooling access. Naval-style compact reactors power the systems with enhanced shielding and containment. These offshore models reduce land footprint concerns in dense cities. Autonomous operation allows remote control with minimal staff. Underwater cables connect the platform to internet backbone hubs. It reduces latency for transoceanic traffic routes. The Global Nuclear-Powered Data Centers Market is observing early tests in this segment. It may evolve into a strategic deployment mode for global operators.

Growth of Nuclear-Energy-as-a-Service for Data Center Operators

New business models offer nuclear power through service-based frameworks. Vendors provide full lifecycle support, from reactor deployment to maintenance and decommissioning. Data center operators avoid the burden of plant ownership. Power purchase agreements (PPAs) tailor nuclear output to computing needs. Long-term contracts ensure price predictability and uptime guarantees. Vendors optimize output to match dynamic workloads. These models reduce capital requirements for hyperscale entrants. The Global Nuclear-Powered Data Centers Market supports this transition through flexible energy financing. It helps democratize nuclear adoption for smaller or multi-tenant facilities.

Market Challenges

Market Challenges

High Regulatory Complexity and Safety Standards in Nuclear Deployment

Strict regulatory oversight limits the speed of new nuclear facility deployment. Licensing, environmental assessments, and public consultations extend project timelines. Data centers must align with nuclear safety codes, emergency protocols, and radiation zoning. These compliance factors add complexity compared to traditional energy solutions. Political opposition and community resistance further delay approvals in some regions. Cost escalations may occur from prolonged approval cycles. The Global Nuclear-Powered Data Centers Market must navigate these layers to scale efficiently. Streamlined regulatory frameworks will be critical for faster integration and broader adoption.

Capital-Intensive Nature of Nuclear Infrastructure Investments

Initial setup costs remain a barrier for many operators considering nuclear options. SMR and microreactor technologies require high upfront capital even with modular benefits. Procurement, installation, and long-term waste handling add to costs. Financing structures are still evolving to match the digital sector’s ROI timelines. Many hyperscale operators prefer opex-focused models over capex-heavy utilities. Securing long-term return requires confidence in reactor lifespan, technology stability, and regulatory continuity. Market adoption depends on aligning funding mechanisms with data center growth models. Until nuclear solutions achieve cost parity, uptake may remain limited outside pilot projects.

Market Opportunities

Deployment of Modular Nuclear Units in Edge and Remote Data Centers

Edge computing requires power resilience in off-grid or unstable grid zones. Modular nuclear reactors offer compact, transportable solutions for such sites. This opens new geographies for low-latency data services. The Global Nuclear-Powered Data Centers Market sees opportunity in serving defense, mining, and telecom sectors. These sectors need secure compute infrastructure beyond metro areas. Vendors can scale nuclear units to site-specific needs. This flexibility increases addressable market scope. It enables decentralized expansion of critical digital services.

Integration of AI and Automation for Fully Autonomous Operations

AI enables automated control of nuclear-linked infrastructure with minimal human intervention. Predictive tools monitor thermal behavior, fuel use, and safety parameters in real-time. Data centers benefit from intelligent load shaping and demand-response capabilities. These technologies reduce operational overhead and staffing costs. It improves uptime while enhancing safety margins. The Global Nuclear-Powered Data Centers Market aligns with this digital automation shift. Smart systems support seamless integration between compute and energy environments.

Market Segmentation:

Market Segmentation:

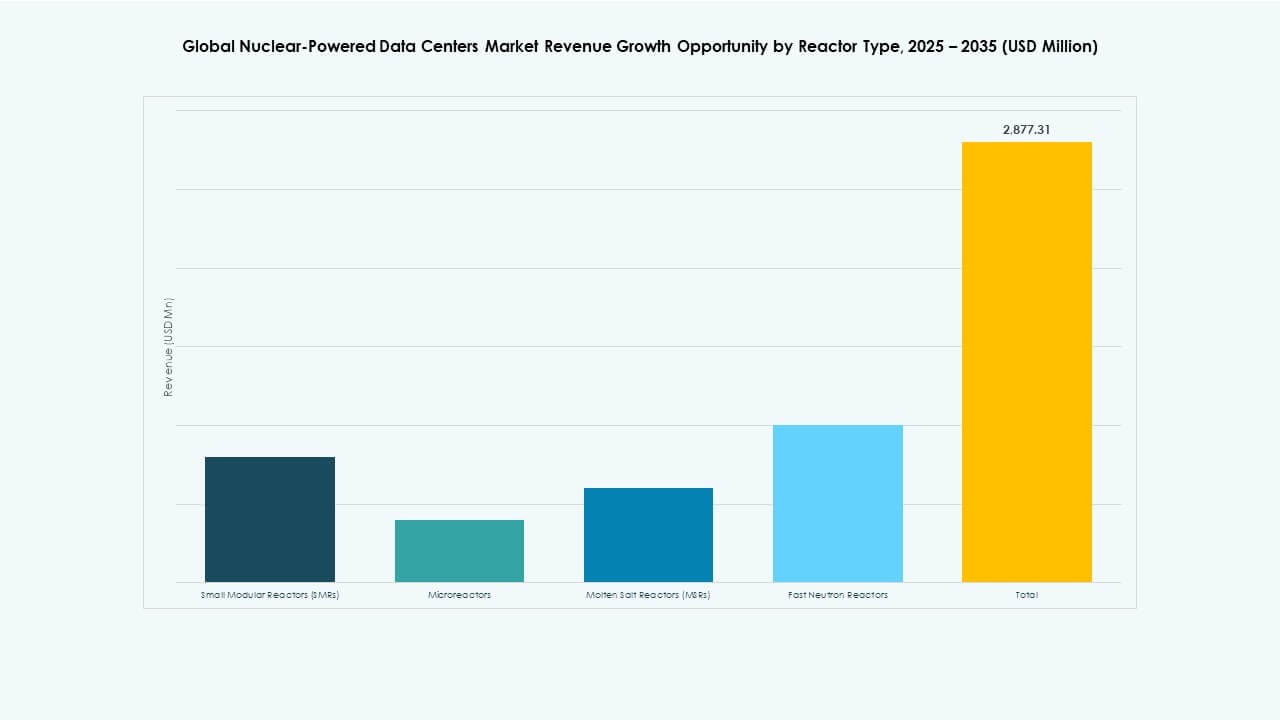

By Reactor Type

Small Modular Reactors (SMRs) dominate the Global Nuclear-Powered Data Centers Market due to their scalable design and strong regulatory traction. SMRs accounted for the largest market share in 2025, supported by commercial readiness and wide deployment potential across remote and urban sites. Microreactors are emerging with pilot testing, especially for edge deployments and defense-linked sites. Molten Salt Reactors (MSRs) and Fast Neutron Reactors remain in R&D stages, with limited commercial integration. The market growth is strongly anchored in SMR investments by players like NuScale, Rolls-Royce, and GE Hitachi targeting cloud data infrastructure.

By Cooling Technology

Liquid cooling holds the largest share in the Global Nuclear-Powered Data Centers Market, driven by its high efficiency in managing thermal loads from AI and HPC environments. It supports compact reactor integration while reducing energy loss. Air cooling remains relevant in small-scale deployments and retrofitted facilities, but faces limitations in power-dense setups. Heat reuse integration systems are gaining traction, particularly in colder regions where excess reactor heat supports local heating grids. Growth in this segment reflects both environmental optimization and circular energy use trends in hyperscale and government-owned campuses.

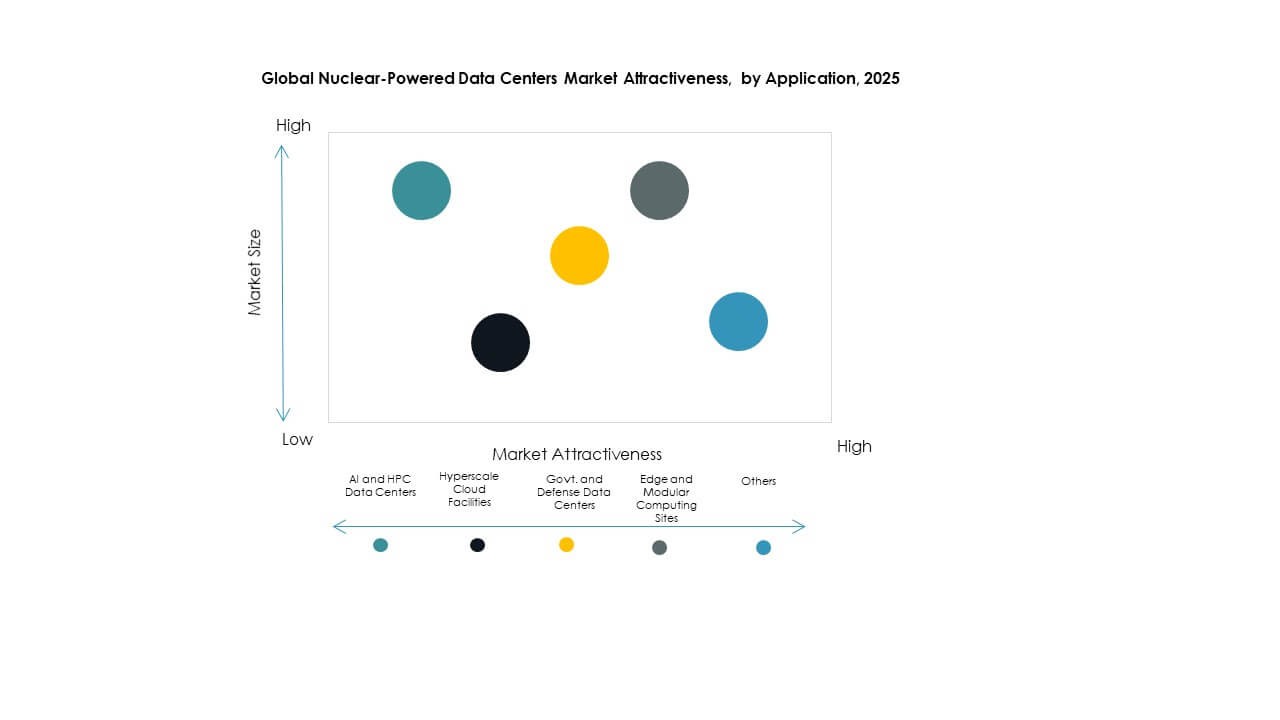

By Application

Hyperscale cloud facilities lead the Global Nuclear-Powered Data Centers Market in application share due to massive compute requirements and demand for reliable, on-site power. Tech giants seek carbon-free baseload energy to support data sovereignty, AI training, and global cloud delivery. AI and HPC data centers are also major contributors, with rising demand for real-time analytics and scientific computing driving nuclear co-location. Government and defense data centers benefit from secure and independent energy sources, while edge and modular computing sites are early adopters of microreactors to power remote or mobile installations.

By End User Industry

Cloud service providers represent the largest end-user segment in the Global Nuclear-Powered Data Centers Market, as hyperscale operators seek to meet net-zero goals without compromising uptime. Companies like Amazon, Microsoft, and Google are exploring nuclear-backed energy supply models to offset growing energy footprints. Government agencies follow closely, leveraging nuclear power for strategic infrastructure resilience. Research institutions adopt such models for high-performance workloads in physics, climate, and defense. Industrial enterprises, particularly those in manufacturing and defense, are adopting nuclear-powered microgrids to support digital twins and factory automation with uninterrupted, sustainable power.

Regional Insights:

Regional Insights:

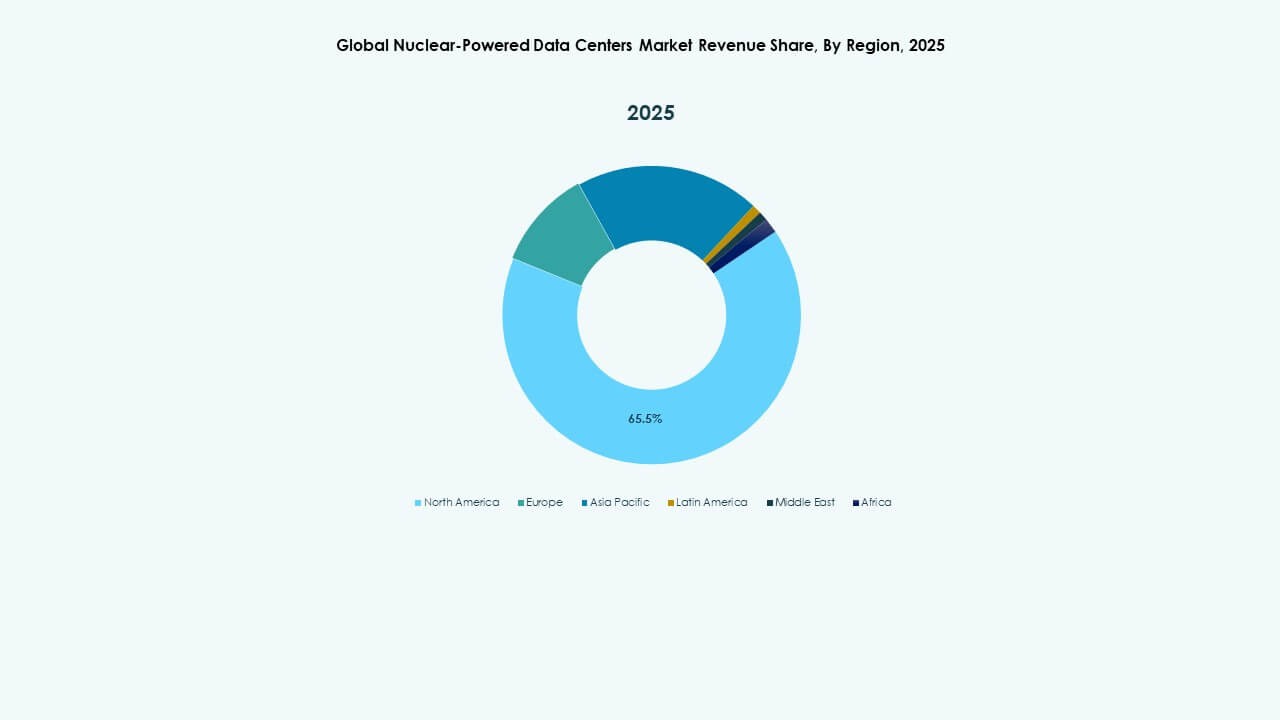

North America leads the Global Nuclear-Powered Data Centers Market with a dominant market share of 42% in 2025. The United States drives adoption through active small modular reactor (SMR) projects and supportive regulatory frameworks. Major cloud providers in the U.S. are partnering with nuclear technology vendors to secure stable power for hyperscale sites. Government incentives and federal funding for clean energy integration strengthen the region’s growth. Canada is also progressing in this space, with research institutions and industrial clusters exploring nuclear-backed computing infrastructure. The region benefits from mature nuclear infrastructure and high digital infrastructure demand.

- For instance, X-energy partnered with Korea Hydro & Nuclear Power and Doosan Enerbility to advance deployment of its Xe-100 small modular reactors, focusing on fuel supply, component manufacturing, and international expansion, supporting future clean energy applications including data centers.

Europe holds the second-largest share at 28%, supported by strong climate policies and nuclear energy transition strategies. Countries like France and the Netherlands are advancing SMR integration for government and research data centers. Europe’s energy diversification efforts, driven by geopolitical shifts, are encouraging nuclear-based digital infrastructure investments. The European Commission’s data sovereignty agenda fuels demand for localized, secure data facilities. France’s leadership in nuclear technology accelerates its domestic deployment. The region’s focus on sustainability and energy independence will sustain steady growth in this segment.

- For instance, Westinghouse Electric Company has developed digital platforms like HiVE™ and bertha™ to optimize nuclear plant performance, applying AI and advanced analytics to improve operational efficiency, predictive maintenance, and reactor lifecycle management across global deployment sites.

Asia-Pacific follows with a 22% share, driven by innovation and rising demand for AI and cloud infrastructure. China leads in pilot deployments and nuclear innovation, while South Korea and Japan show growing interest in microreactor-enabled edge and military applications. The region’s dense urban areas and manufacturing zones create strong use cases for onsite, emissions-free power. Governments are funding SMR R&D and collaborating with hyperscale operators. Asia-Pacific presents long-term potential for market expansion. The Global Nuclear-Powered Data Centers Market in this region benefits from rapid digitalization and advanced nuclear technology programs.

Competitive Insights:

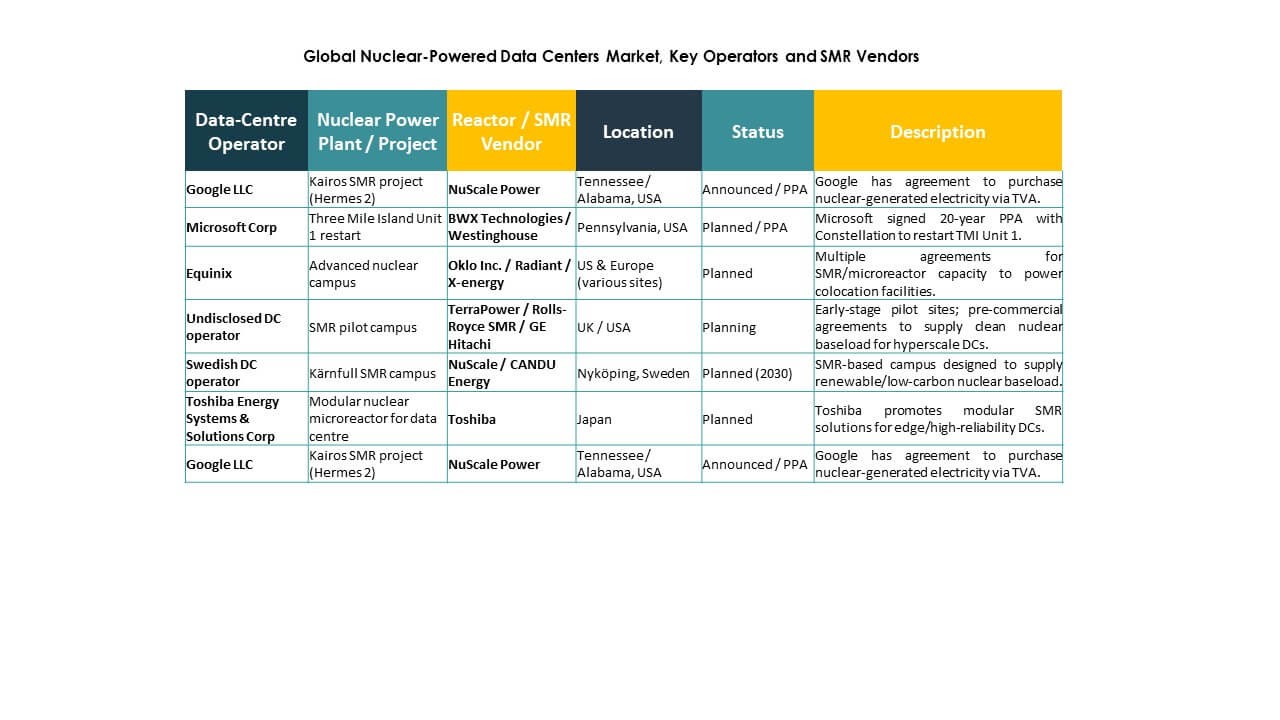

- NuScale Power Corporation

- Westinghouse Electric Company LLC

- TerraPower, LLC

- Rolls-Royce SMR Ltd.

- GE Hitachi Nuclear Energy

- BWX Technologies, Inc.

- Oklo Inc.

- X-energy, LLC

- Toshiba Energy Systems & Solutions Corporation

- CANDU Energy Inc.

The Global Nuclear-Powered Data Centers Market is highly specialized and driven by a blend of nuclear engineering firms and emerging clean-energy startups. NuScale Power and Westinghouse Electric lead the space with operational SMR designs and data center partnerships. TerraPower and Rolls-Royce SMR are advancing reactor platforms tailored for modular computing environments. Oklo and X-energy focus on microreactors, targeting edge and mobile data facilities. GE Hitachi, Toshiba, and BWX Technologies bring global nuclear expertise, integrating scalable systems with long-term safety protocols. CANDU Energy supports projects in regions adopting heavy water reactor models. Competition revolves around speed of deployment, cost-effectiveness, licensing advantage, and integration with cloud and AI workloads. The market rewards firms that combine compact nuclear technology with energy-as-a-service models and digital automation, creating room for strategic alliances between data operators and nuclear vendors.

Recent Developments:

- In October 2025, BWX Technologies, Inc. signed a nuclear steam generator detailed design contract and Memorandum of Understanding with Rolls-Royce SMR Ltd. to support SMR development for clean energy demands, including potential data center applications.

- In August 2025, X-energy, LLC formed a strategic partnership with Amazon, Korea Hydro & Nuclear Power, and Doosan Enerbility to accelerate Xe-100 SMR deployment and TRISO fuel production in the U.S., targeting data center and AI power needs with up to $50 billion in investment.

- In June 2025, Amazon signed a long-term Purchase Power Agreement (PPA) with Talen Energy for 1.9 GW of nuclear energy from the Susquehanna nuclear power plant in Pennsylvania to power AWS data centers, including plans to explore small modular reactors.