Executive summary:

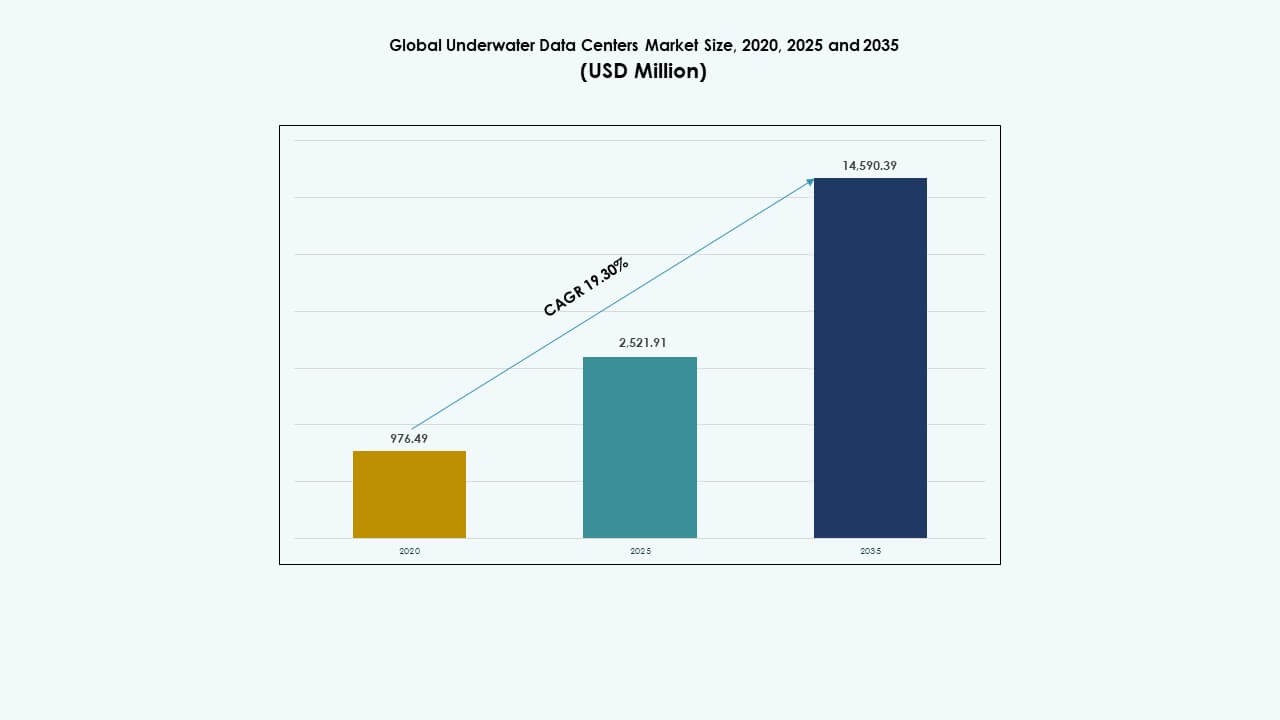

The Global Underwater Data Centers Market size was valued at USD 976.49 million in 2020 to USD 2,521.91 million in 2025 and is anticipated to reach USD 14,590.39 million by 2035, at a CAGR of 19.3% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2035 |

| Underwater Data Centers Market Size 2025 |

USD 2,521.91 Million |

| Underwater Data Centers Market, CAGR |

19.3% |

| Underwater Data Centers Market Size 2035 |

USD 14,590.39 Million |

The market grows due to rising demand for energy‑efficient data infrastructure and low‑latency computing. Underwater systems use natural seawater cooling, which improves efficiency and reduces land use. Advances in subsea engineering, modular design, and remote monitoring support reliable operations. Cloud providers and telecom firms view this model as strategic for edge deployment. Investors value the market for long‑term sustainability, resilience, and alignment with green infrastructure goals.

North America leads due to early pilot projects and strong hyperscaler investment. Europe follows, driven by strict sustainability targets and coastal infrastructure readiness. Asia Pacific is emerging rapidly, led by China, Japan, and South Korea, supported by government‑backed projects and high coastal data demand. Growing digitalization, urban density, and renewable energy integration position these regions as future growth centers for the Global Underwater Data Centers Market.

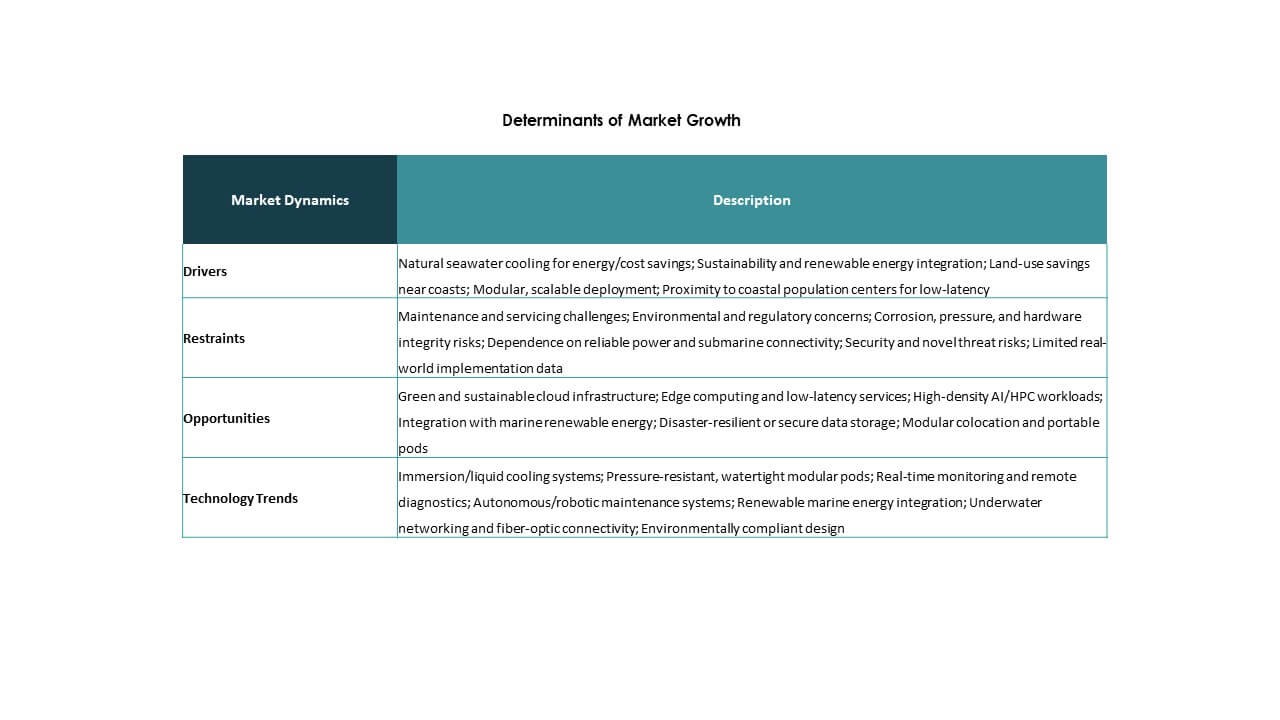

Market Dynamics:

Market Dynamics:

Energy-Efficient Cooling and Environmental Sustainability Goals Drive Adoption of Underwater Data Centers

The Global Underwater Data Centers Market benefits from a strong shift toward energy-efficient infrastructure. Traditional data centers consume vast energy for cooling systems. Underwater data centers use ocean water as a natural coolant, drastically reducing cooling costs and energy usage. This supports environmental targets and lowers carbon emissions. The rising demand for green IT infrastructure aligns with the sustainability goals of global enterprises. Companies and governments favor low-impact data solutions. These submerged data centers operate silently and leave minimal land footprint. Investors see underwater models as strategic for long-term efficiency. It enhances operational sustainability for high-density computing.

- For instance, Nautilus Data Technologies achieved a PUE of 1.15 in its Stockton floating data center using closed-loop river cooling.

Rising Edge Computing and 5G Deployment Encourage Underwater Data Center Integration

The global surge in edge computing and 5G applications fuels demand for compact, low-latency infrastructure. Underwater data centers support edge deployment near coastal cities where data consumption is highest. Their modular form enables faster build-out near urban populations. Telecom operators and hyperscalers seek decentralized systems to improve response times. The Global Underwater Data Centers Market is positioned to deliver on this speed and proximity demand. Real-time apps such as AR/VR, streaming, and autonomous navigation need local processing. Ocean-based locations enable carriers to bypass congested land-based construction. This model complements growing bandwidth demand while saving urban space.

- For instance, Beijing Highlander Digital Technology’s Hainan center processes over 4 million high-definition images in 30 seconds at 35 meters depth.

Technological Advancements in Subsea Engineering and AI-Enabled Monitoring Bolster Market Development

Modern underwater data centers benefit from durable marine-grade construction and AI-based condition monitoring. Subsea enclosures use corrosion-resistant alloys, pressure-tolerant systems, and modular power delivery. AI-driven telemetry systems monitor temperature, humidity, and pressure in real time. The Global Underwater Data Centers Market integrates remote management to avoid on-site maintenance. These systems support full automation with robotic deployment and servicing. Equipment failures can be predicted using embedded sensors and machine learning. This reduces downtime and extends hardware life. The combination of AI and subsea engineering enables scalable underwater infrastructure without human intervention.

Strategic Investment from Tech Giants Positions Underwater Infrastructure as a Long-Term Asset Class

Leading cloud providers are piloting underwater projects to diversify data storage and boost resilience. The Global Underwater Data Centers Market attracts long-term capital for its unique value proposition. It supports data sovereignty, edge services, and disaster recovery zones. Underwater systems are immune to many land-based risks like floods, fire, and civil disruption. Strategic players view this infrastructure as a future-proof alternative in saturated markets. Institutional investors back these innovations for their low overhead and minimal land use. Corporate strategies now include submerged options in coastal expansion plans. It adds flexibility to data center portfolios globally.

Market Trends

Market Trends

Rise in Prefabricated and Modular Designs for Faster Submerged Deployment

The Global Underwater Data Centers Market trends toward prefabricated modules that streamline installation and scalability. These units are designed in controlled environments, then shipped and submerged near coastlines. The modular approach shortens construction timelines and enables repeatable builds. Vendors offer standard enclosures with integrated servers, cooling, and monitoring. Prefabrication cuts down on field labor and risks from harsh marine conditions. These systems can be deployed near key cities or in offshore clusters. The compact footprint aids coastal urban planning. Organizations prefer rapid, low-impact deployment strategies. This modular trend is reshaping underwater data center rollouts globally.

Integration of Renewable Energy Sources into Offshore Data Center Models

Ocean-based data centers increasingly integrate with marine renewable energy systems like tidal, wave, and offshore wind. The Global Underwater Data Centers Market reflects growing interest in self-sufficient infrastructure. Co-location with clean energy projects reduces grid dependence and emissions. Coastal regions with strong wave energy potential are key targets for hybrid setups. Renewable-powered underwater sites enhance ESG compliance. Vendors are testing floating platforms with built-in solar arrays. Wind turbines and wave converters supply auxiliary power or full capacity in select zones. These systems align with national green agendas. Energy synergy marks a rising trend across deployments.

Use of Digital Twin and Simulation Tools for Subsea Performance Optimization

Advanced simulation software is reshaping underwater data center design and operation. The Global Underwater Data Centers Market increasingly uses digital twin technology to predict performance. Engineers simulate fluid dynamics, thermal load, and pressure conditions before deployment. This allows virtual stress testing under real-world oceanic scenarios. Digital twins monitor ongoing operations and enable predictive adjustments. These tools help in capacity planning and fault detection. Simulation-based design reduces prototype costs and boosts lifecycle reliability. Firms use real-time analytics from operational twins for system tuning. It marks a clear trend toward data-driven facility optimization.

Expansion of Regulatory Frameworks and Compliance Standards for Subsea Data Infrastructure

Regulatory bodies are shaping underwater deployment norms, driving standardization and accountability. The Global Underwater Data Centers Market must meet maritime, environmental, and telecom-specific compliance. Governments now assess impact on marine ecosystems, fishing zones, and coastal usage rights. Regulatory approval timelines are being formalized for consistent project evaluation. Countries like Norway, Japan, and the U.S. are defining underwater data rules. This trend enhances transparency for investors and accelerates adoption. Standardization reduces legal risks and improves insurance availability. The presence of clear regulations boosts trust in submerged infrastructure models.

Market Challenges

Market Challenges

Technical Limitations in Maintenance, Scalability, and Long-Term Reliability of Submerged Systems

The Global Underwater Data Centers Market faces major challenges in operational maintenance and scalability. Submerged systems are hard to access, requiring robotic or specialized retrieval. This increases downtime risk in case of hardware failure. Repairs are costlier and take longer than land-based facilities. Thermal cycling and ocean pressure may degrade components over time. Limited scalability constrains high-density installations. Expanding capacity means deploying multiple pods, which adds complexity. Marine conditions also affect signal transmission and latency. Maintenance plans must address salt corrosion, marine growth, and sensor accuracy under extreme environments.

High Capital Expenditure, Regulatory Uncertainty, and Environmental Risk Concerns

Building and deploying underwater data centers involves significant upfront investment. The Global Underwater Data Centers Market contends with high CAPEX compared to standard facilities. Specialized materials, marine transport, and installation drive costs. Environmental assessments and legal clearances vary by region and often delay timelines. Ecosystem disruption fears and community pushback hinder large-scale rollouts. Long-term liability for underwater equipment adds insurance complexity. Few vendors offer mature solutions, limiting competition and buyer choice. These factors create risk for conservative investors and slow market maturity.

Market Opportunities

Expansion into Coastal Smart City Projects and Urban Edge Applications

The Global Underwater Data Centers Market holds strong potential in supporting smart coastal cities. With rising demand for edge computing in urban hubs, underwater systems offer compact, scalable alternatives. Governments seek clean, resilient infrastructure near shorelines. Data centers submerged near smart ports, logistics hubs, and IoT-rich environments serve real-time needs. These applications open new revenue streams for vendors and investors targeting coastal digital transformation.

Collaborations Between Cloud Providers and Marine Engineering Firms for Custom Deployments

Partnerships between hyperscalers and marine contractors unlock tailored deployments. The Global Underwater Data Centers Market benefits from custom-built modules optimized for specific coastal zones. Collaboration ensures designs meet local oceanographic, power, and legal conditions. Cloud players gain geographic flexibility while engineering firms access recurring infrastructure contracts. This synergy builds long-term momentum in offshore digital infrastructure.

Market Segmentation:

Market Segmentation:

By Business Model Segment Analysis

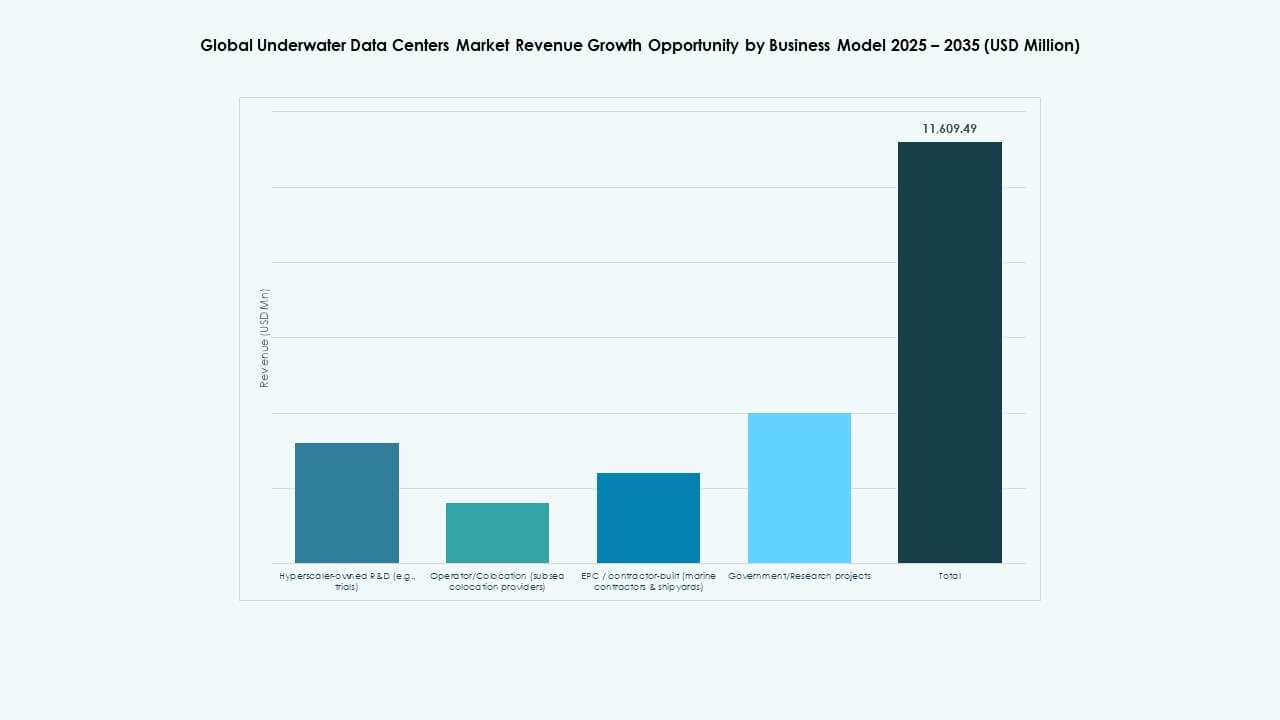

The Global Underwater Data Centers Market shows strong momentum in the Operator/Colocation (subsea colocation providers) segment, holding the largest share. Hyperscaler-owned R&D models lead early pilots and build proof of concepts. EPC/contractor-built models draw steady investment from shipyards and marine firms for custom builds. Government/Research projects support innovation funding in select regions. Others include hybrid or bespoke business models that serve niche requirements. Growth arises from rising demand for reliable, low-latency infrastructure and cost sharing by colocation providers. Firms with broad service ecosystems and partnership networks gain wider adoption and scale faster than single-use players.

By Component Segment Analysis

In the Global Underwater Data Centers Market, Hardware leads the component segment due to substantial CAPEX and technology deployment needs. Cooling systems, subsea enclosures, and server racks drive most spending. Software follows with strong growth through monitoring, remote management, and automation platforms. Services, including installation, maintenance, and consulting, see rising demand through long-term contracts. Growth in software is tied to remote operations and AI analytics. Service expansion reflects extended life-cycle support. Hardware dominance stems from complex engineering and marine durability requirements. Investments center on robust architecture to withstand ocean conditions.

By Deployment Segment Analysis

The Deep Water segment holds a dominant share in the Global Underwater Data Centers Market because it offers scalability and stable thermal environments. Shallow Water deployments attract coastal cities for edge and latency-sensitive applications. Deep Water provides cooler temperatures and reduced human interference, which extends hardware life. Growth in deep water is spurred by rising digital loads and space limits on land. Shallow water usage grows for pilots near major ports. Both segments benefit from improved marine transport and installation tech. Regulations and maritime access influence deployment choice and pace of adoption.

By Tier Segment Analysis

In the Global Underwater Data Centers Market, Tier III and Tier IV facilities lead due to reliability and uptime demands. Tier III offers concurrent maintainability popular with commercial clients. Tier IV suits critical applications with fault tolerance. Tier I and Tier II represent entry-level builds with limited scalability. Growth in higher-tier segments ties to digital growth and enterprise needs for nonstop operations. Demand from IT, telecom, and financial services drives strict uptime standards. Developers prioritize high-tier builds to justify investment and secure long-term service contracts. This trend supports premium pricing and partner trust.

By Thermal Approach Segment Analysis

The Closed-loop liquid cooling segment dominates the Global Underwater Data Centers Market due to better control and broad use cases. Direct seawater heat-sink systems serve passive cooling needs with low energy demand. Zero-water / Recycled cooling systems attract interest for environmental priorities in some regions. Growth in closed-loop cooling stems from efficient temperature control and compatibility with high-performance computing. Passive seawater systems gain from simple design and low operating expenses. Zero-water setups appeal where water purity or reuse policy drives engineering choices. Innovation across these cooling methods improves energy efficiency and uptime.

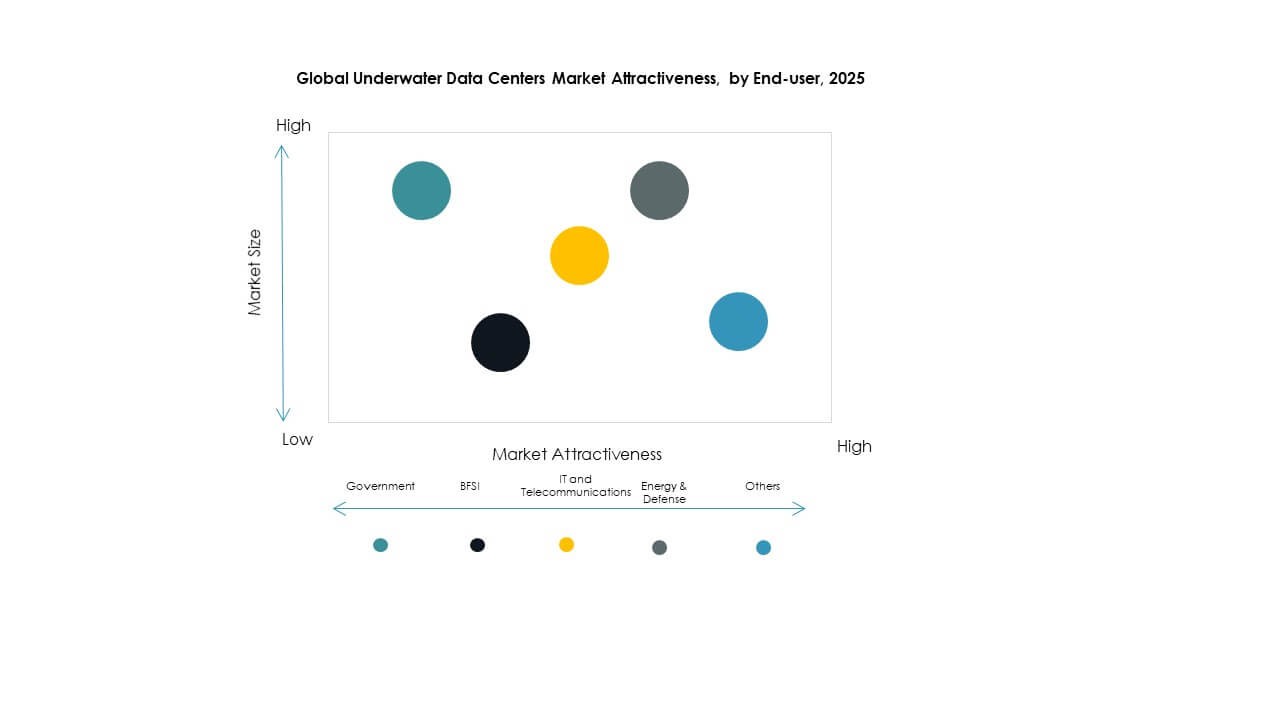

By End-user Segment Analysis

The IT and Telecommunications segment commands the largest share in the Global Underwater Data Centers Market due to massive data traffic and edge needs. Government end-users support national digital infrastructure projects. BFSI relies on secure, low-latency connections for transactions. Energy & Defense require resilient networks in harsh environments. Others include healthcare, media, and research sectors moving toward digital transformation. Growth in IT and telecom flows from 5G expansion and cloud demand. Government policy incentives also push adoption. Each end-user segment invests based on uptime, data speed, and security priorities.

Regional Insights:

Regional Insights:

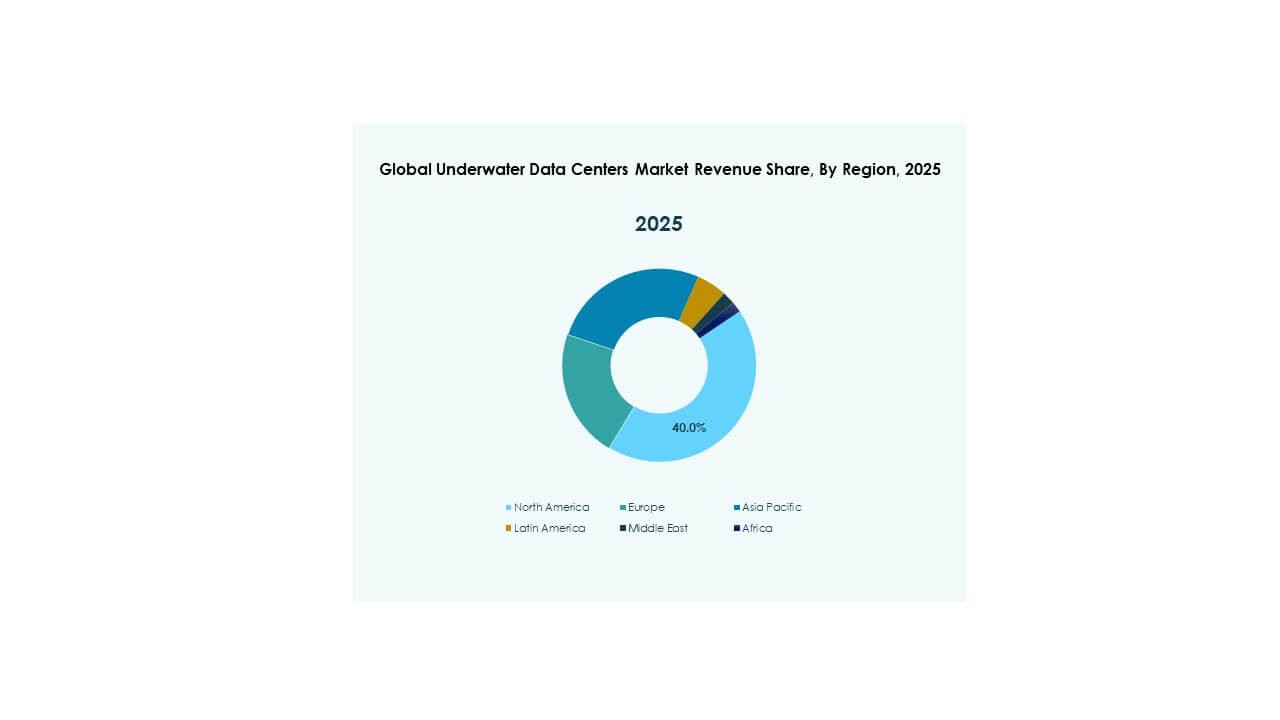

North America – Leading Deployment and Innovation Hub in Underwater Data Center Infrastructure

North America leads the Global Underwater Data Centers Market with a share exceeding 35%, driven by early adoption and large-scale R&D initiatives. The U.S. dominates the regional market due to active trials by Microsoft and growing interest from U.S. Navy-backed research programs. Favorable regulatory support, marine infrastructure, and strong cloud infrastructure investment drive sustained momentum. Colocation firms and hyperscalers seek strategic offshore locations for scalability, energy efficiency, and disaster resilience. Canada also shows growth potential through green energy integration in coastal zones. The region benefits from established subsea cable networks and innovation ecosystems that enable rapid tech rollout. It serves as a testbed for global players seeking performance validation.

- For instance, Microsoft’s Project Natick deployed the Northern Isles datacenter 117 feet underwater off Scotland’s Orkney Islands in June 2018, containing 12 racks with 864 servers that operated reliably for two years with an 8x lower failure rate than equivalent land-based servers and growing interest from U.S. Navy-backed research programs.

Europe – Strong Sustainability Focus and Coastal Expansion Support Growth

Europe holds around 30% share in the Global Underwater Data Centers Market, fueled by strict carbon reduction goals and dense coastal city clusters. Countries like the UK, France, and the Netherlands are advancing pilot deployments through public-private partnerships. Norway and Sweden attract infrastructure developers with access to renewable energy and deep-sea ports. The region supports integration of submerged data centers with offshore wind and marine R&D zones. Regulatory clarity and sustainability-linked incentives enhance investor confidence. Market growth also aligns with Europe’s digital sovereignty and data localization efforts. Environmental compliance and circular economy focus further accelerate deployments in Northern and Western Europe.

Asia Pacific – Emerging Market with Growing Coastal Digitization and Government Backing

Asia Pacific accounts for nearly 25% share of the Global Underwater Data Centers Market and is the fastest-growing region. China leads the region through state-supported clusters like Hainan’s underwater facility. Japan and South Korea invest in edge connectivity and 5G-driven micro data centers near dense coastal hubs. India, Singapore, and Australia explore offshore capabilities tied to national smart city programs. The region’s high population density, urbanization, and digital growth push demand for scalable and resilient infrastructure. Government-backed innovation zones and green tech funding attract both domestic and international players. Asia Pacific is positioned to overtake other regions in capacity expansion over the next decade.

- For instance, China has pursued subsea data center pilots in Hainan since 2020, with state-backed projects demonstrating reliable operation in trials tied to offshore renewable integration, though specific numerical metrics remain limited in public verification.

Competitive Insights:

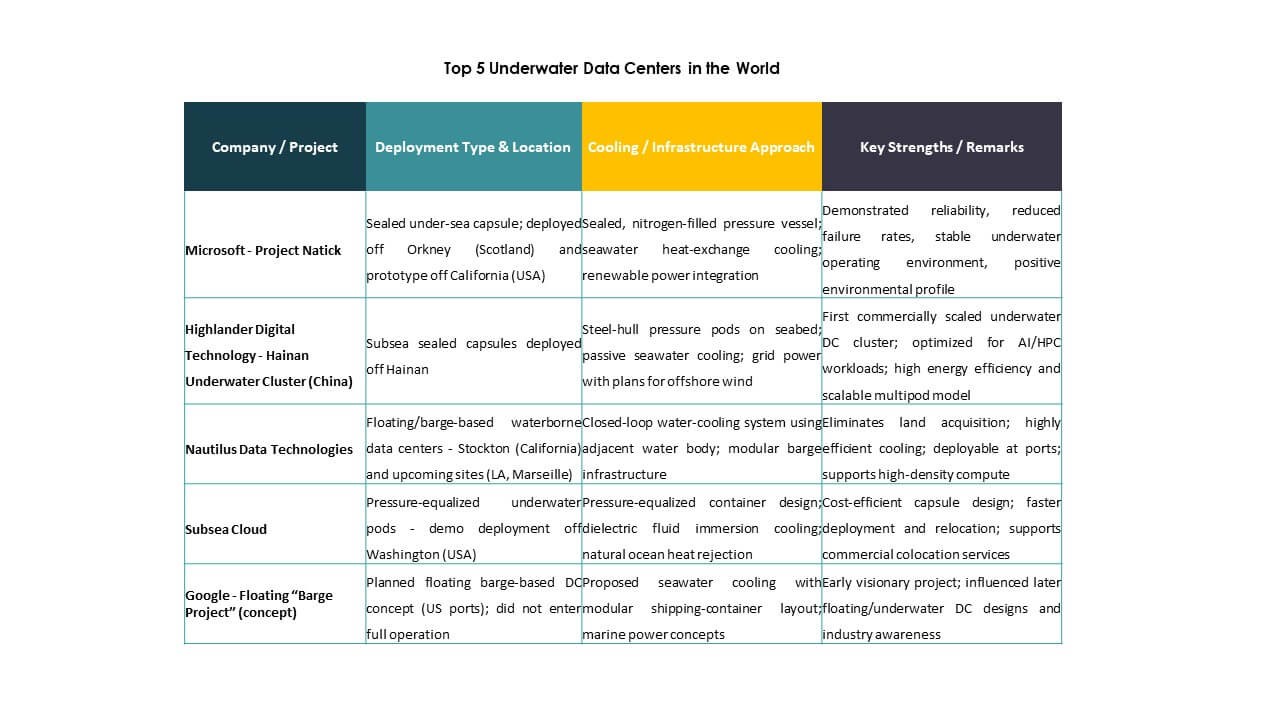

- Microsoft – Project Natick

- Highlander Digital Technology – Hainan Underwater Cluster (China)

- Nautilus Data Technologies

- Subsea Cloud

- Google – Floating Barge Project (concept)

- Naval Group

- Bechtel

- Subsea7

- Aker Solutions / OneSubsea

- Kongsberg Maritime

The Global Underwater Data Centers Market features a mix of technology pioneers, marine engineering specialists, and infrastructure contractors. Microsoft leads with Project Natick, setting early benchmarks in long-term submerged deployment. Highlander Digital and China Telecom drive growth in Asia through state-backed clusters. Nautilus and Subsea Cloud focus on scalable commercial models with modular systems. Naval Group, Subsea7, and Aker Solutions bring deep subsea engineering expertise, offering turnkey deployment. Bechtel and Kongsberg Maritime support design and integration across maritime zones. It remains fragmented but innovation-driven, with partnerships between hyperscalers and marine firms accelerating. Players invest in energy efficiency, structural durability, and regulatory alignment. Competitive advantage depends on lifecycle cost, deployment speed, environmental compliance, and ability to scale across coastal markets.

Recent Developments:

Recent Developments:

- In October 2025, HiCloud commissioned the world’s first wind‑powered underwater data center near Shanghai, powered mainly by offshore wind and cooled by seawater, with expansion plans targeting capacity growth beyond the initial phase

- In June 2025, an agreement was signed to build the first offshore wind‑powered underwater data center in China’s Lin‑gang Special Area near Shanghai. This partnership involving HiCloud and local authorities aims to merge offshore wind energy with subsea cooling, creating a sustainable subsea computing facility.

- In February 2025, HiCloud added a new data center module off the coast of Hainan with around 400 high‑performance servers connected to shore, expanding the capacity and commercial capability of its underwater deployment. The development supports AI workloads and advanced digital services through natural seawater cooling and increased processing throughput.