Executive summary:

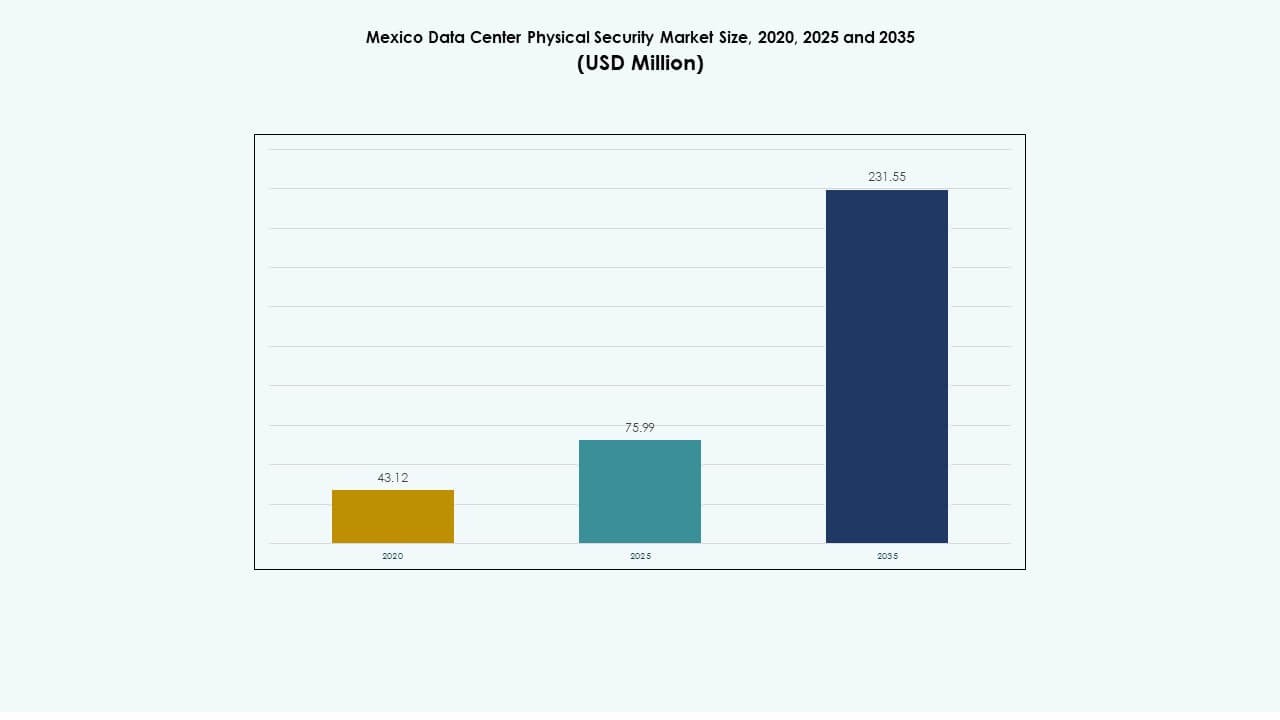

The Mexico Data Center Physical Security Market size was valued at USD 43.12 million in 2020 to USD 75.99 million in 2025 and is anticipated to reach USD 231.55 million by 2035, at a CAGR of 11.74% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2035 |

| Mexico Data Center Physical Security Market Size 2025 |

USD 75.99 Million |

| Mexico Data Center Physical Security Market, CAGR |

11.74% |

| Mexico Data Center Physical Security Market Size 2035 |

USD 231.55 Million |

Strong demand for multi-layer defense, AI-driven surveillance, and biometric access systems drives adoption across hyperscale and enterprise facilities. Continuous innovation in automated monitoring, intrusion detection, and unified security platforms enhances data protection. The market’s strategic value lies in its ability to safeguard digital assets and support investor confidence amid rapid infrastructure expansion and tightening compliance standards. Businesses see long-term gains in resilience and operational assurance through security modernization.

Northern Mexico leads growth due to high industrial activity, cross-border trade, and proximity to U.S. hyperscale investments. Central Mexico emerges as a core hub driven by government-backed digital programs and new colocation facilities. Southern regions show rising traction supported by renewable energy availability and affordable land for future data infrastructure expansion.

Market Drivers

Market Drivers

Rising Demand for Advanced Physical Security Infrastructure in Data Facilities

The Mexico Data Center Physical Security Market gains momentum from expanding data center networks and growing digital transformation. Enterprises prioritize advanced systems such as multi-layer access controls, motion sensors, and biometric scanners to ensure uninterrupted operations. It benefits from stronger awareness of physical vulnerabilities that can lead to data breaches. Vendors provide integrated consoles linking surveillance, alarms, and monitoring systems. The country’s hyperscale and colocation providers strengthen resilience through security modernization. Investors view this expansion as a sign of sector maturity. Mexico’s regulatory push for cyber-physical compliance also lifts adoption. Demand for continuous monitoring systems remains high among operators managing large campuses.

- For example, Telmex Triara data centers cover more than 74,000 square meters built area with over 17,000 square meters of certified computer equipment rooms. They deploy physical access controls such as proximity card gates, 24/7 CCTV surveillance, and security doors with airlocks.

Integration of AI-Driven Security and Smart Infrastructure Upgrades

Artificial intelligence supports predictive surveillance and automated detection workflows. Operators deploy machine learning algorithms to interpret video feeds and detect anomalies faster. The Mexico Data Center Physical Security Market evolves as firms integrate AI-enabled analytics with existing infrastructure. Edge analytics minimizes response times for incidents within large complexes. Vendors invest in interoperability between old and new systems. Cloud-based control centers help manage multiple sites in real time. Rising energy efficiency goals drive integration of automated lighting and security coordination. The market’s progress indicates Mexico’s strategic shift toward intelligent facility ecosystems. It highlights the country’s readiness for high-reliability infrastructure.

Growing Adoption of Biometric Access Systems and Layered Defense Models

Biometric tools strengthen accountability and precision in access management. Companies use facial recognition, fingerprint verification, and iris scans to replace traditional cards. The Mexico Data Center Physical Security Market benefits from strict audit trails that enhance operational visibility. Layered models combine perimeter, building, and rack-level security under unified systems. Integrators provide real-time reporting dashboards for rapid response. Facilities focus on dual-authentication policies to block unauthorized entries. Colocation providers extend protection to customer-specific zones. Businesses recognize physical defense as a competitive differentiator in compliance-driven sectors. Investors consider these developments a marker of regional data infrastructure maturity.

Regulatory Alignment and Strategic Infrastructure Investment by Enterprises

Government frameworks push operators toward certified compliance for high-risk sectors like BFSI and telecom. The Mexico Data Center Physical Security Market expands with corporate investment in infrastructure modernization. Firms target certifications aligning with ISO and Tier standards. Public-private collaboration fosters development of secure digital parks. Regional players expand certified facilities to meet multinational client requirements. Security innovations align with corporate sustainability and efficiency mandates. Domestic firms attract foreign partnerships for design and system integration. The rising focus on resilient networks underpins investor confidence. Strategic funding supports growth in national and cross-border digital infrastructure.

- For example, Ascenty, a prominent data center operator in Mexico, exemplifies regional investment aligning with industry standards such as ISO and Tier certifications. Their Mexico 2 facility incorporates dual authentication access controls combining biometric and card systems, along with tri-bus power redundancy supporting operational resilience and compliance with regulatory mandates.

Market Trends

Shift Toward Unified Security Platforms and Cloud-Based Management Models

Centralized systems unify alarm, video, and access data into one management interface. The Mexico Data Center Physical Security Market experiences stronger demand for SaaS-based command centers. Enterprises adopt remote control and alerting platforms to monitor dispersed facilities. Cloud analytics improves incident visibility and response accuracy. Vendors launch scalable modules that fit enterprise or colocation environments. Operators seek simplified management of multi-site networks under secure connections. Integration with existing IT infrastructure enhances system performance. The convergence of cybersecurity and physical security drives deeper alignment. Businesses emphasize efficiency through centralized governance and monitoring.

Expansion of Edge Data Centers Requiring Compact Security Solutions

Edge deployments in Mexico create demand for lightweight, modular protection systems. Compact video analytics units and mobile-based access platforms support fast setup. The Mexico Data Center Physical Security Market adapts to these decentralized models through smart automation. Vendors provide rugged sensors suitable for remote and high-temperature zones. Operators prefer plug-and-play architectures for flexible scalability. Edge growth boosts local production and integration services. Firms install solar-powered cameras to minimize dependency on grid supply. Hybrid operations link central control with edge-specific alerts. This trend increases efficiency and coverage across emerging regional data zones.

Growth in AI-Powered Surveillance and Predictive Incident Analysis

AI cameras now dominate new deployments across hyperscale and enterprise facilities. The Mexico Data Center Physical Security Market embraces AI for pattern recognition and anomaly detection. Smart analytics systems anticipate risk rather than react to it. Vendors develop customizable dashboards that filter alerts by severity. Advanced object detection enhances protection around restricted zones. Machine learning optimizes response time by tracking movement trends. Operators report higher accuracy in threat identification. Integration with existing VMS platforms ensures smooth migration. This trend signals a transition toward preventive physical defense systems.

Sustainability and Energy-Efficient Security Technology Integration

Energy-efficient security systems emerge as a key procurement criterion. The Mexico Data Center Physical Security Market incorporates low-power sensors and LED-based surveillance systems. Operators align sustainability goals with operational reliability. Solar-enabled access controls reduce grid load. Vendors introduce recyclable enclosures and low-carbon production lines. Smart automation lowers idle power consumption in security infrastructure. Companies aim to balance safety and environmental impact through smart design. Facilities adopt AI-driven optimization to regulate resource usage. The trend connects green initiatives with high-performance security standards.

Market Challenges

Market Challenges

High Implementation Costs and Complexity of Multi-Layer Integration

The Mexico Data Center Physical Security Market faces barriers due to high installation and integration costs. Multi-layer designs demand advanced equipment, certified components, and skilled staff. Small operators struggle to match enterprise-level protection. Integration between legacy and modern systems remains complex. Procurement delays occur due to long approval cycles. Vendors must tailor solutions to site-specific layouts. Budget limitations restrict upgrades in older buildings. Coordination between security and IT teams often causes project slowdowns. This cost structure limits smaller firms from adopting next-generation solutions.

Skilled Workforce Shortage and Evolving Compliance Requirements

Mexico’s fast-growing digital economy lacks adequate trained professionals for physical security management. The Mexico Data Center Physical Security Market needs more expertise in integration and AI-based control systems. Frequent regulatory updates create confusion about compliance pathways. Businesses struggle to maintain certification readiness. Vendors spend resources on staff training and audit preparation. Complex cross-border standards hinder multinational collaboration. Maintenance of advanced systems requires regular software updates and technical calibration. Firms face risks of downtime during system transitions. Addressing these gaps remains critical for achieving long-term reliability.

Market Opportunities

Expansion of Hyperscale and Colocation Facilities Across Mexico

The Mexico Data Center Physical Security Market benefits from rapid growth in hyperscale and colocation centers. Global cloud providers expand presence across key metropolitan zones. Security solution providers gain new revenue from integrated project deployments. Government incentives promote digital infrastructure investment. AI-driven monitoring systems attract long-term contracts from hyperscale firms. Domestic integrators build partnerships with global players. Rising demand for secure hosting supports steady capital inflow. Foreign entrants prioritize Mexico as a gateway for Latin American expansion. The trend enhances security innovation and job creation.

Adoption of Predictive Analytics and Integrated Risk Management Platforms

Organizations deploy predictive analytics for real-time decision-making. The Mexico Data Center Physical Security Market evolves toward platforms linking physical and cyber intelligence. Vendors develop dashboards that analyze event patterns and risk scores. Investors see potential in modular systems that scale with facility size. Demand rises for cross-domain collaboration between IT and physical teams. Predictive alerts help avoid service disruption during maintenance. Enterprises use data visualization to enhance situational awareness. This evolution strengthens operational transparency across Mexico’s digital infrastructure ecosystem.

Market Segmentation

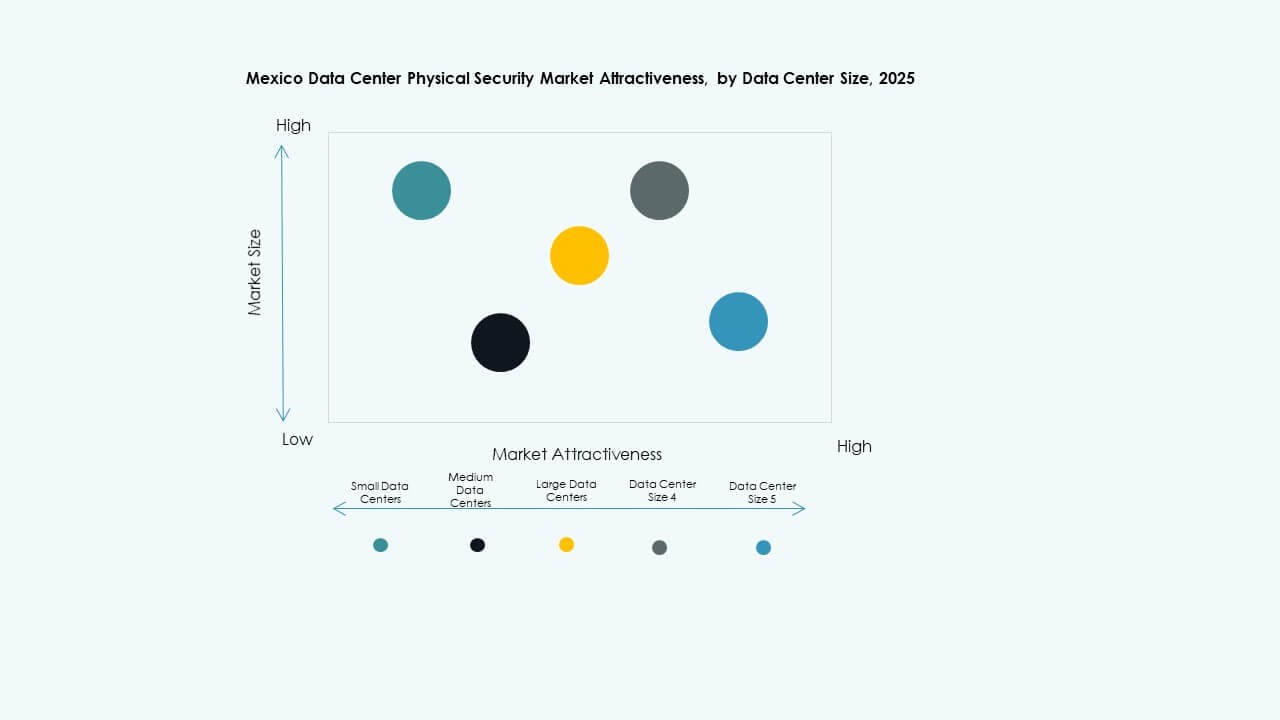

By Data Center Size

Large data centers dominate the Mexico Data Center Physical Security Market due to hyperscale expansion and heavy investment in Tier III and IV facilities. Medium centers gain momentum from enterprise digital transformation programs. Small centers focus on affordable surveillance and access systems. The segment’s growth links to national connectivity goals and industrial digitization. Vendors design modular solutions for scaling across capacities. Demand for continuous monitoring drives service contracts. Regional facilities adopt hybrid models for flexibility. Rising urban deployments boost medium-size data centers’ market appeal.

By Component

Solution components hold the largest share in the Mexico Data Center Physical Security Market. Operators prioritize hardware such as surveillance cameras, control panels, and sensors. Services grow steadily as integration and maintenance become vital for uptime. Firms demand vendor-led consulting to improve system coordination. Continuous upgrades fuel recurring revenue streams. Service quality influences customer retention in long contracts. Vendors offer flexible subscription models for maintenance. Both components combine to build holistic defense systems. Market players invest in end-to-end lifecycle support.

By Solution

Video surveillance leads in the Mexico Data Center Physical Security Market, supported by AI analytics and motion detection. Access control expands with fingerprint, RFID, and facial authentication systems. Monitoring and detection technologies gain traction due to predictive maintenance integration. Vendors provide modular control rooms combining live and archived data. Other tools such as perimeter alarms and asset tagging improve operational discipline. Continuous R&D focuses on reducing latency in visual monitoring. Real-time alerts strengthen response time across facilities. These combined solutions enhance overall resilience and audit efficiency.

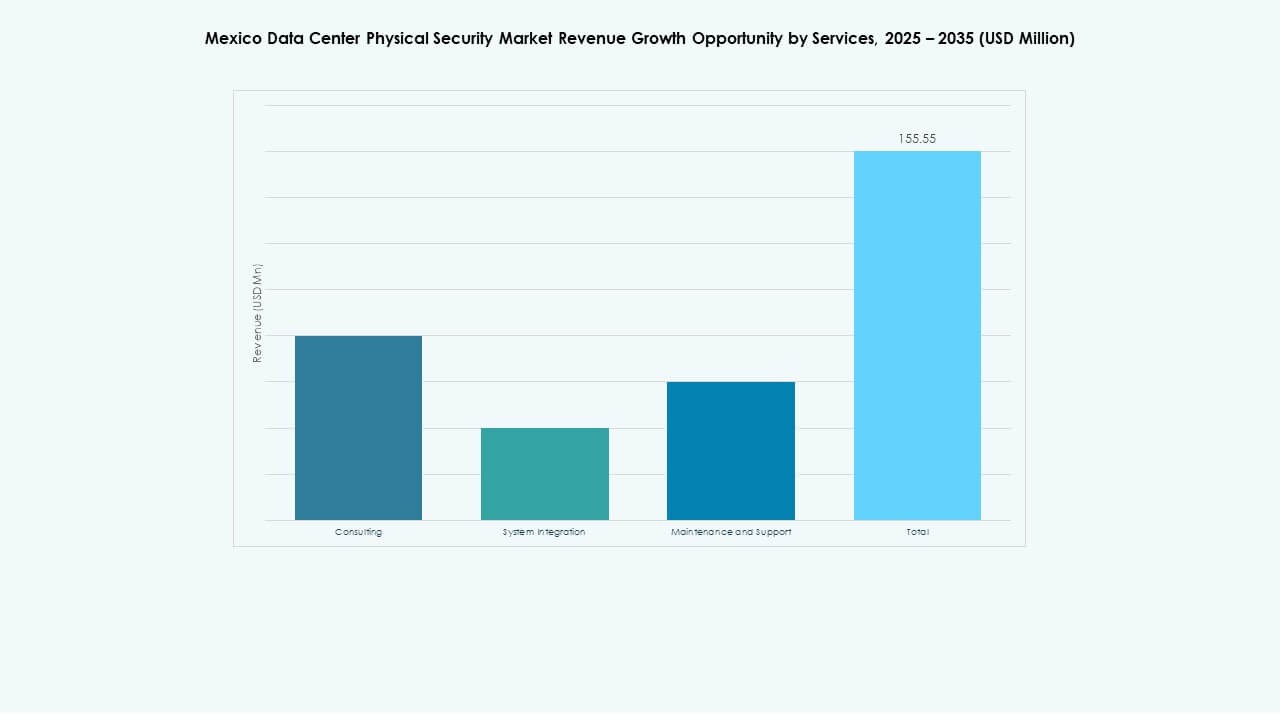

By Services

System integration dominates the Mexico Data Center Physical Security Market due to the complexity of multi-layer coordination. Consulting services gain importance during new project design stages. Maintenance and support retain steady growth as compliance and audits increase. Operators demand remote diagnostic features to reduce site visits. Vendors develop predictive maintenance models to lower downtime. Integration ensures unified control of diverse technologies. Service providers differentiate through faster incident recovery. Continuous partnerships ensure seamless performance upgrades. The shift emphasizes quality over cost-driven outsourcing.

By Security Layer

Perimeter security remains the most significant layer in the Mexico Data Center Physical Security Market. It prevents unauthorized entry and physical intrusion. Building access systems integrate biometric and smart card authentication. Data hall security gains importance due to increasing server density. Rack-level controls add granularity for customer-specific access. Vendors develop real-time dashboards displaying multi-zone alerts. The focus on multi-layer defense enhances overall resilience. New installations favor adaptive perimeter sensors. Operators deploy integrated detection grids to maintain full-site visibility.

By Data Center Type

Hyperscale data centers lead the Mexico Data Center Physical Security Market, followed by colocation and enterprise facilities. Edge data centers rise due to low-latency demand near cities. Vendors supply modular solutions for distributed architectures. Hyperscale operators emphasize automation and centralized control. Colocation providers target multi-client customization for access security. Enterprise facilities modernize infrastructure to align with compliance norms. Edge sites prioritize compact, energy-efficient systems. New entrants focus on serving cloud service expansion across Mexico. Each type fuels different adoption priorities and spending levels.

By End-user

IT & Telecom dominates the Mexico Data Center Physical Security Market due to heavy reliance on data reliability. BFSI follows with stringent regulatory needs. Healthcare facilities increase investment in secure patient data hosting. Government projects require high assurance for classified data. Retail and e-commerce grow with transaction monitoring needs. Manufacturing adopts integrated systems to safeguard production data. Vendors provide tailored solutions per sector. Rising multi-sector digitization drives broad-based adoption. End-user diversity ensures steady revenue across project lifecycles.

Regional Insights

Northern Mexico: Industrial and Cross-Border Data Infrastructure Expansion

Northern Mexico holds over 40% share of the Mexico Data Center Physical Security Market. Monterrey and Chihuahua host industrial clusters driving strong infrastructure demand. Operators install large-scale facilities to support manufacturing and logistics. It benefits from cross-border trade and strong energy availability. Security vendors establish partnerships with regional integrators. Proximity to the U.S. border enhances foreign investment attraction. Industrial growth directly drives continuous upgrades to physical protection systems.

- For example, KIO Networks’ Monterrey (MTY1) data center spans a 306 m² data hall and uses reinforced concrete walls with anti-seismic design for structural resilience. It operates on a redundant 2N power configuration supported by dual 225 kVA UPS units and 500 kW generators, providing high physical protection and operational reliability in line with Tier III standards.

Central Mexico: Rising Urban Data Hubs and Government-Backed Modernization

Central Mexico accounts for nearly 35% of the Mexico Data Center Physical Security Market. Mexico City, Querétaro, and Guadalajara form the region’s data triangle. It supports hyperscale development and colocation growth. Government-led smart city programs promote security modernization. Vendors deploy unified access and perimeter systems for new urban facilities. Demand rises from public and private collaborations. Central positioning offers high connectivity, making it a key digital core for enterprises.

- For example, in Querétaro, Microsoft operates a hyperscale data center campus that incorporates advanced physical security systems, including mantrap access control and biometric authentication mechanisms.

Southern Mexico: Emerging Growth Supported by Renewable Energy Projects

Southern Mexico holds roughly 25% of the Mexico Data Center Physical Security Market. Development accelerates with renewable energy availability and lower land costs. New facilities attract investors looking for sustainable data operations. Vendors introduce modular security for mid-sized and green facilities. It benefits from growing infrastructure near industrial corridors. Local workforce expansion supports regional integration projects. Southern Mexico becomes a new frontier for resilient, energy-efficient data infrastructure.

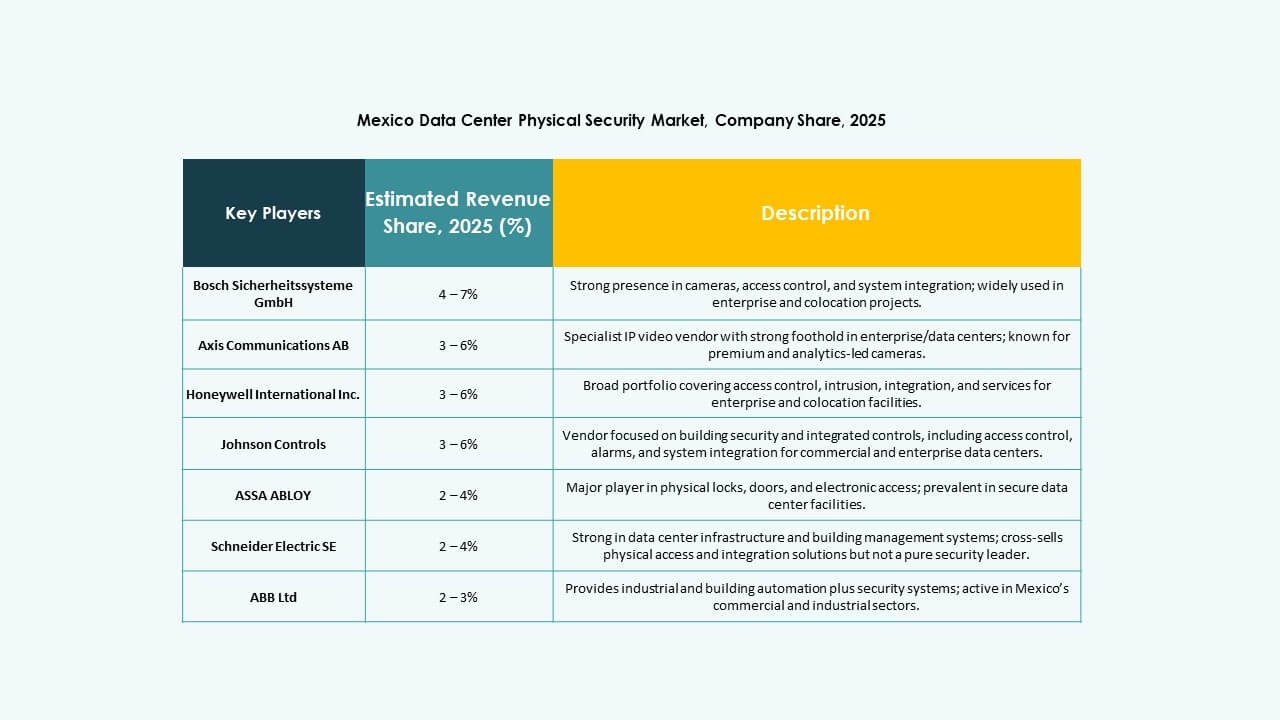

Competitive Insights:

- IBM Mexico

- ASSA ABLOY

- ABB

- Axis Communications AB

- Bosch Sicherheitssysteme GmbH

- Cisco Systems, Inc.

- Fortinet

- Genetec

- Honeywell International Inc.

- Johnson Controls

- Palo Alto Networks

- Schneider Electric SE

- Securitas

- Siemens AG

The competitive landscape of the Mexico Data Center Physical Security Market features a mix of global multinationals and specialist security firms. Leaders such as Cisco and Genetec offer unified platforms that integrate video surveillance, access control, and analytics, appealing to hyperscale and enterprise data centers looking for scalable, cyber-hardened solutions. Firms like Bosch, Honeywell, and Schneider Electric leverage strong reputations and broad product portfolios to compete on reliability and total lifecycle support. Niche players such as ASSA ABLOY and ABB focus on access control and automation, giving operators modular options. Intense rivalry drives continual product upgrades, service bundling, and competitive pricing which benefits operators and spurs wider adoption across mid-size and large data centers.

Recent Developments:

- In November 2025, Palo Alto Networks and IBM planned to launch a joint solution to accelerate enterprise-wide quantum-safe readiness, further advancing security technologies relevant for data centers.

- In September 2025, the U.S. tech firm CloudHQ announced an investment of $4.8 billion to build six data centers in the central Querétaro state of Mexico, marking a significant expansion in the country’s data center infrastructure. This project aims to leverage Mexico’s growing role as a digital hub in Latin America and support increasing demand driven by cloud computing and AI workloads.

- In February 2025, AWS confirmed a $5 billion commitment to a new Mexican cloud region, boosting hyperscale data center demand and security measures. This investment is driving competitive developments in physically securing data centers in Mexico, reflecting global trends in digital infrastructure growth.