Executive summary:

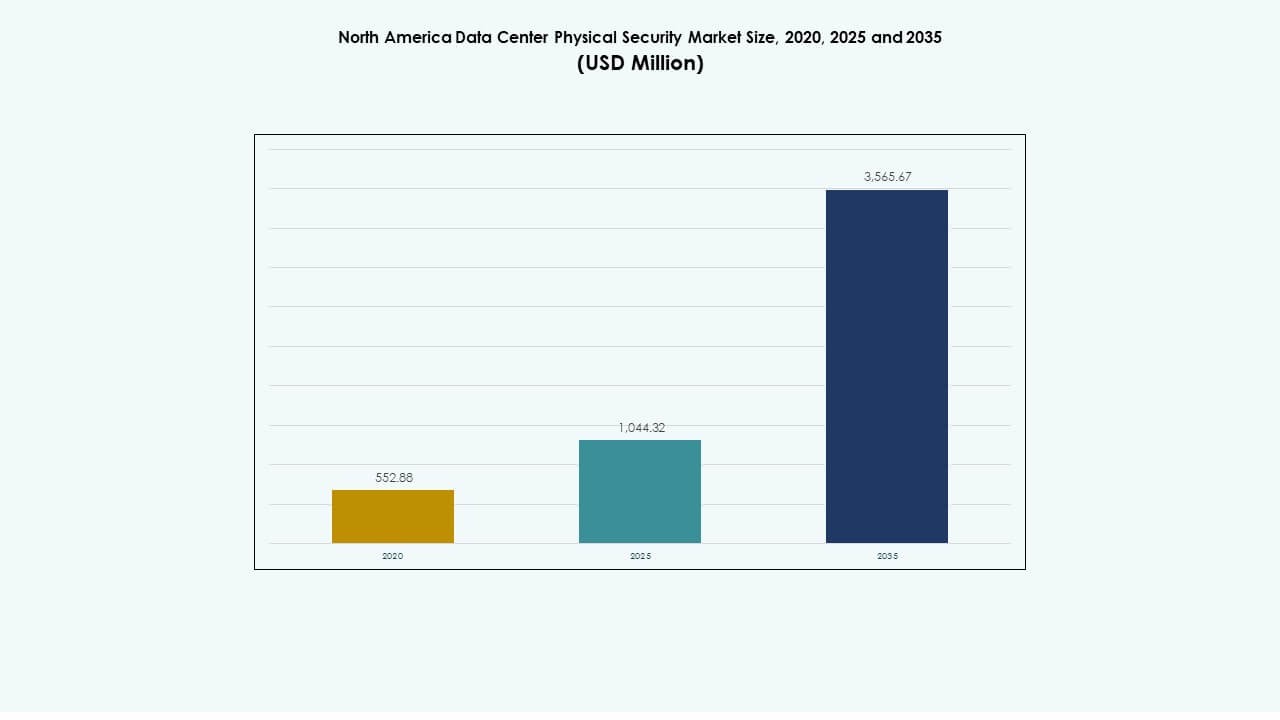

The North America Data Center Physical Security Market size was valued at USD 552.88 million in 2020, reached USD 1,044.32 million in 2025, and is anticipated to reach USD 3,565.67 million by 2035, at a CAGR of 13.01% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2035 |

| North America Data Center Physical Security Market Size 2025 |

USD 1,044.32 Million |

| North America Data Center Physical Security Market, CAGR |

13.01% |

| North America Data Center Physical Security Market Size 2035 |

USD 3,565.67 Million |

Strong investment in advanced surveillance, biometric access control, and integrated monitoring platforms drives steady growth. Data center operators upgrade legacy systems to meet higher compliance and uptime standards. Rapid expansion of hyperscale and colocation facilities lifts demand for modular, cloud-connected defense systems. It strengthens operational resilience and protects mission-critical assets for businesses and investors seeking long-term value creation.

The United States leads the market due to large hyperscale deployments and strict regulatory enforcement. Canada follows with strong investment in colocation and green data centers. Mexico shows rapid expansion through industrial digitalization and emerging edge computing sites. These combined efforts reinforce regional leadership in next-generation data infrastructure protection.

Market Drivers

Market Drivers

Growing Deployment of Advanced Access Control and Surveillance Infrastructure

The North America Data Center Physical Security Market grows through continuous innovation in surveillance and access systems. Facilities adopt biometric recognition, AI-based cameras, and multi-layer verification to reduce breach probability. Operators prioritize tools that link physical and logical access data under unified monitoring dashboards. Integration of AI analytics strengthens event correlation and threat prediction. These systems help prevent unauthorized entry in real time. Data center owners enhance transparency for audits and compliance reviews. Investors see sustained security automation as a strategic asset. It reinforces confidence in uptime reliability and compliance resilience.

- For instance, Vectra AI’s Threat Certainty Index™ analyzes thousands of security events to prioritize threats by severity and confidence, reducing analyst workload by up to 37×. Its AI platform tracks attacker behavior across data center environments, delivering actionable insights that support real-time responses to unauthorized access attempts.

Rising Data Center Investments Supporting Robust Infrastructure Expansion

Continuous investments from hyperscale and colocation operators strengthen the regional infrastructure base. Construction of new sites across key metro clusters lifts demand for integrated security systems. Providers deploy fiber-connected perimeter controls and smart sensors that track every movement. Governments push for higher resilience standards across critical digital assets. Firms focus on predictive maintenance to cut human dependency. These capital flows create lasting growth opportunities for vendors of access control and surveillance tools. It drives steady adoption of layered protection models. Long-term investors treat these facilities as essential infrastructure for the digital economy.

Integration of AI and IoT to Enable Predictive Physical Security

AI and IoT convergence transforms security operations across advanced facilities. Smart devices connect cameras, alarms, and sensors into single network ecosystems. Predictive algorithms flag irregular movements before escalation. Operators reduce false alarms and maintain precise situational awareness. Machine learning tools analyze large data sets to predict vulnerabilities. Such proactive defense reduces manual intervention and error risks. The North America Data Center Physical Security Market benefits from automation-driven accuracy. It reinforces the importance of scalable, adaptive frameworks in mission-critical environments. Investors value this transition as a long-term cost stabilizer and risk mitigator.

- For instance, Cobalt AI integrates robotics, AI, and IoT sensors to strengthen physical security in high-risk environments. Its autonomous patrol systems analyze real-time video and sensor data to detect anomalies, improve situational awareness, and support proactive threat response across data center facilities.

Strengthening Compliance and Risk Management Standards in Data Infrastructure

Evolving regulations such as SOC 2, ISO 27001, and NIST elevate the need for verifiable controls. Operators enhance monitoring systems to meet multi-jurisdictional standards. Compliance-linked audits drive upgrades to existing access and alarm networks. Integrated security systems support continuous assessment through digital logs and audit trails. Firms adopt certification-ready frameworks to win enterprise contracts. Security verification aligns closely with customer assurance goals. The region’s investors back vendors that simplify governance workflows. It ensures alignment between operational safety and enterprise trust goals.

Market Trends

Adoption of Cloud-Integrated Security Management Platforms

Hybrid data center networks drive interest in cloud-based control consoles. These systems unify data from diverse cameras, locks, and sensors into a central platform. Operators gain visibility across multiple locations through secure web dashboards. Vendors embed encrypted APIs for integration with incident response tools. Cloud orchestration supports seamless software updates and system scaling. The North America Data Center Physical Security Market reflects this transition toward flexible security models. It creates value through reduced downtime and centralized oversight. Such platforms ensure faster decision-making in dynamic threat landscapes.

Growing Preference for AI-Enabled Video Analytics and Behavioral Detection

AI algorithms support deeper detection accuracy and automatic event classification. Cameras identify unusual body language, tailgating, or forced entry attempts instantly. Video feeds generate metadata that informs long-term security policies. Real-time alerts allow faster coordination between physical and digital teams. Firms reduce costs tied to manual review and surveillance fatigue. Machine vision models strengthen data reliability across high-traffic environments. It supports predictive maintenance and early fault identification. These changes signal a shift from reactive to intelligent surveillance frameworks.

Expansion of Edge and Modular Data Centers Requiring Decentralized Security

Edge infrastructure expansion creates demand for distributed protection layers. Smaller sites located near user clusters require compact, remote-monitored systems. Vendors design modular access control and low-power sensors for ease of installation. Real-time network visibility helps coordinate multiple edge nodes. Companies link security feeds to regional command hubs for active tracking. The North America Data Center Physical Security Market evolves toward multi-site resilience. It allows quicker recovery during incidents and lowers maintenance complexity. Edge-driven architectures reshape physical security design standards.

Shift Toward Unified Physical and Cybersecurity Integration Models

Businesses merge physical and cyber risk management under shared governance frameworks. Security teams handle both intrusion alerts and network anomalies through integrated platforms. Data from physical access logs informs digital credential analysis. These combined insights enhance threat investigation accuracy. Vendors release products that map real-world movements with network activity. Such integration helps maintain regulatory consistency across hybrid systems. It ensures tighter response coordination during high-priority incidents. The approach highlights a fundamental maturity shift in digital infrastructure defense.

Market Challenges

Market Challenges

High Integration Costs and Limited Interoperability Between Legacy and Modern Systems

Integrating old analog hardware with advanced digital surveillance poses financial and operational strain. Operators face high retrofit costs while maintaining continuous uptime. Diverse hardware brands often lack seamless interoperability. Maintenance becomes complex across large campuses with mixed systems. Vendors must standardize protocols to ensure scalable security infrastructure. The North America Data Center Physical Security Market faces recurring challenges in aligning vendor ecosystems. It pressures service providers to design plug-and-play modules. Investors seek scalable cost models that reduce transition risk.

Growing Complexity of Regulatory Compliance Across Jurisdictions

Different states enforce distinct privacy and data protection mandates. Facilities managing cross-border operations face overlapping inspection and audit rules. Operators struggle to maintain unified compliance documentation for authorities. Non-compliance leads to costly downtime and reputation risks. Vendors must design adaptive software to automate policy updates. Complex certifications create barriers for smaller players entering the market. It requires sustained investment in governance automation and staff training. Meeting these standards remains a key operational challenge for large-scale facilities.

Market Opportunities

Market Opportunities

Emergence of AI-Powered Security Analytics and Predictive Defense Platforms

AI applications create measurable efficiency in monitoring and anomaly detection. Vendors design solutions that anticipate threats using deep learning algorithms. Predictive insights minimize false alarms and support faster containment. The North America Data Center Physical Security Market benefits from this analytical expansion. Companies integrate predictive dashboards into central control systems for real-time visibility. Investors target firms developing adaptive analytics and low-latency video AI. It enhances value creation through smarter, autonomous risk management.

Growing Need for Resilient Edge Security Infrastructure Across Distributed Networks

Edge computing growth demands localized protection layers for compact nodes. Firms deploy cloud-linked security consoles for remote verification. Compact sensor networks ensure perimeter safety under minimal human oversight. Emerging players provide mobile-controlled entry systems for temporary edge modules. Vendors expanding into micro-facility protection see strong potential. It promotes scalable infrastructure design across diverse industrial zones. This opportunity aligns with the long-term decentralization of data ecosystems.

Market Segmentation

By Data Center Size

Large data centers dominate due to high capital deployment and advanced hardware installations. These facilities require extensive multi-layer security that integrates video, biometrics, and AI analytics. Medium facilities follow with strong demand from regional colocation and managed service providers. Small centers gain traction through modular security designs. The North America Data Center Physical Security Market benefits from balanced demand across all tiers supporting scalable architectures.

By Component

Solutions lead the segment, including access control and surveillance technologies forming the market core. Services grow steadily through consulting, integration, and post-deployment support. Enterprises prefer turnkey packages that combine hardware and software under single contracts. The service model enhances lifecycle efficiency and compliance monitoring. It reflects industry preference for outcome-based contracts ensuring continuous operation.

By Solution

Video surveillance holds a leading share due to growing AI-based analytics integration. Access control follows closely with biometric and RFID system upgrades. Monitoring and detection tools gain importance for real-time event correlation. The North America Data Center Physical Security Market witnesses consolidation around unified platforms. Vendors focus on linking these tools under interoperable software layers for improved response accuracy.

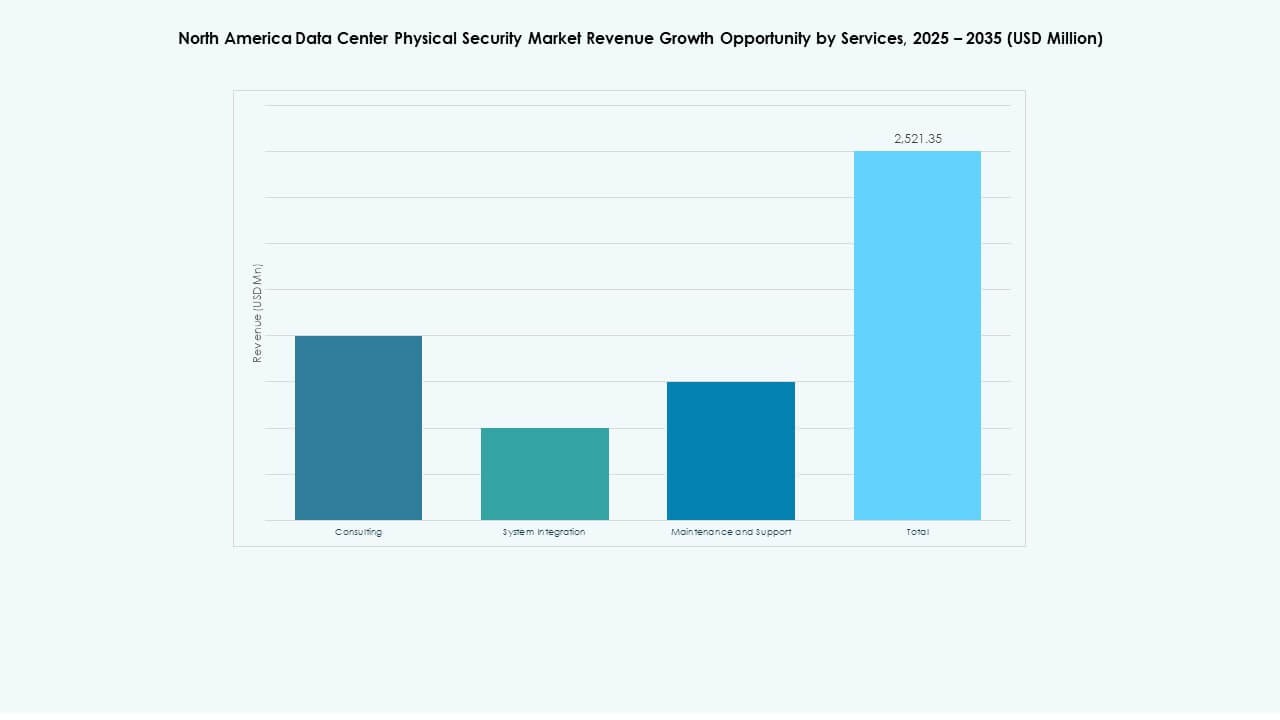

By Services

System integration dominates due to the need for seamless technology deployment across multi-site environments. Consulting supports strategic planning for compliance alignment. Maintenance and support ensure consistent uptime across critical systems. Vendors deliver modular service models covering software updates and remote diagnostics. It strengthens customer retention through reliability-focused operations.

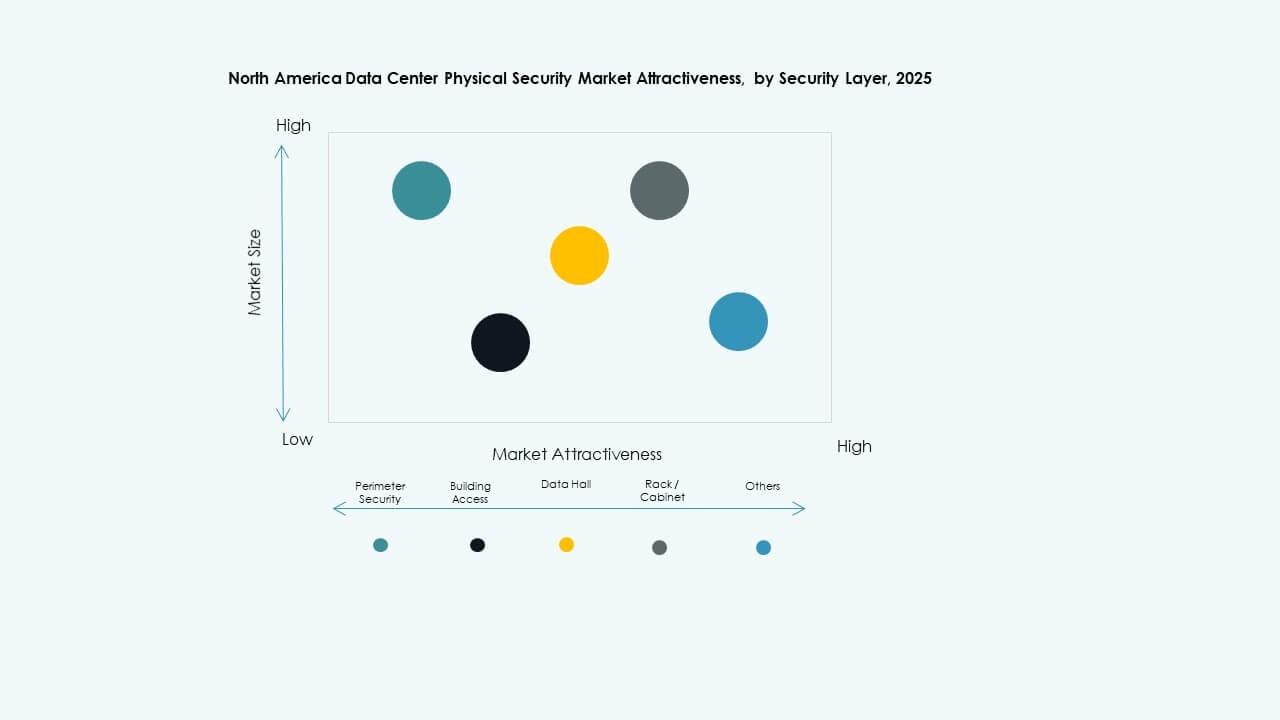

By Security Layer

Perimeter security leads due to increasing external threat complexity and site protection needs. Building access systems secure key operational areas through multi-factor authentication. Data hall monitoring ensures constant surveillance of core compute zones. Rack and cabinet systems enable fine-grained control of server-level access. The North America Data Center Physical Security Market relies on this layered framework to reduce breach risks effectively.

By Data Center Type

Hyperscale centers dominate with heavy investment in automation and predictive analytics. Colocation providers follow through multi-tenant infrastructure upgrades. Enterprise centers adopt hybrid models linking on-premises and cloud setups. Edge facilities gain importance for supporting decentralized digital services. The diversity of data center formats strengthens market maturity across verticals.

By End-user

IT and telecom remain dominant due to massive cloud and network operations. BFSI institutions emphasize compliance-driven monitoring frameworks. Healthcare invests in tamper-proof access and continuous surveillance. Government and defense focus on critical infrastructure integrity. Retail, manufacturing, and e-commerce sectors expand coverage for warehouse and transaction data hubs. The North America Data Center Physical Security Market benefits from widespread end-user diversity.

Regional Insights

Regional Insights

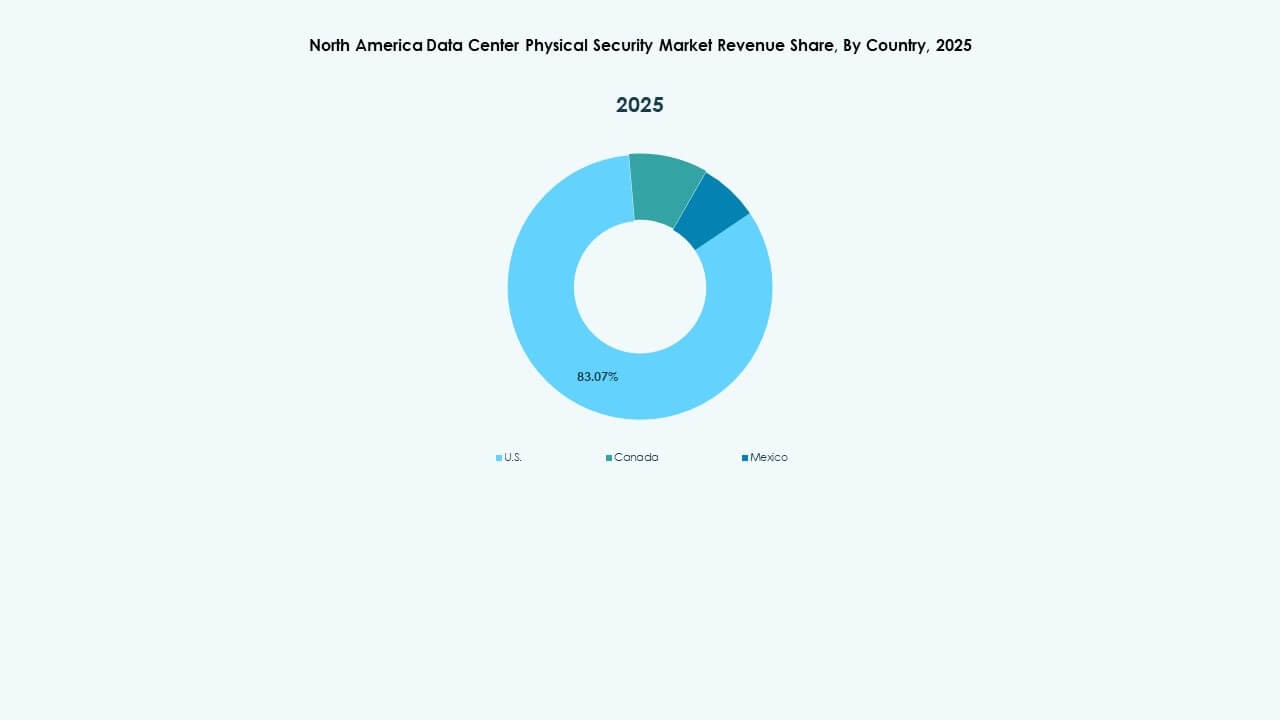

United States – The Core Hub with Over 70% Regional Market Share

The United States leads due to extensive hyperscale deployments and high compliance standards. Major cloud operators invest heavily in physical defense modernization. Facilities across Virginia, Texas, and California adopt multi-factor access systems and AI surveillance. Federal and state cybersecurity regulations drive continuous upgrades. It reinforces the nation’s leadership in digital infrastructure safety. The North America Data Center Physical Security Market derives over 70% of its value from the U.S.

Canada – Growing Colocation and Edge Data Center Network Expansions

Canada secures around 18% of the regional market, backed by new colocation hubs in Ontario and Quebec. Government programs supporting cloud adoption create favorable conditions for infrastructure spending. Firms emphasize renewable-powered facilities paired with advanced perimeter controls. Integration of physical security with environmental monitoring strengthens sustainability metrics. Canadian providers gain cross-border clients through reliability-driven service models. It supports balanced regional competition across North America.

- For instance, Microsoft announced major hyperscale cloud infrastructure investments across Canada, including a US$500 million data center expansion in Quebec in November 2023 and continued development in Ontario. The projects emphasize renewable energy sourcing, advanced perimeter security, and alignment with federal cloud adoption and sustainability initiatives in partnership with utilities such as Ontario Power Generation.

Mexico – Emerging Growth Region with 12% Share Driven by Industrial Digitalization

Mexico contributes roughly 12% of the market, driven by expanding data connectivity and manufacturing digitalization. Industrial parks adopt modular data centers with enhanced access control. Cloud providers expand presence to support cross-border trade ecosystems. Security vendors introduce scalable, low-cost systems for emerging operators. Demand rises from public sector cloud projects requiring multi-layer protection. It positions Mexico as a strategic emerging contributor to the region’s security ecosystem.

- For instance, industrial and logistics hubs in Monterrey are attracting new modular data center developments designed with biometric access controls and multi-layer perimeter protection. These projects support Mexico’s expanding cloud infrastructure and digital manufacturing initiatives linked to cross-border trade modernization.

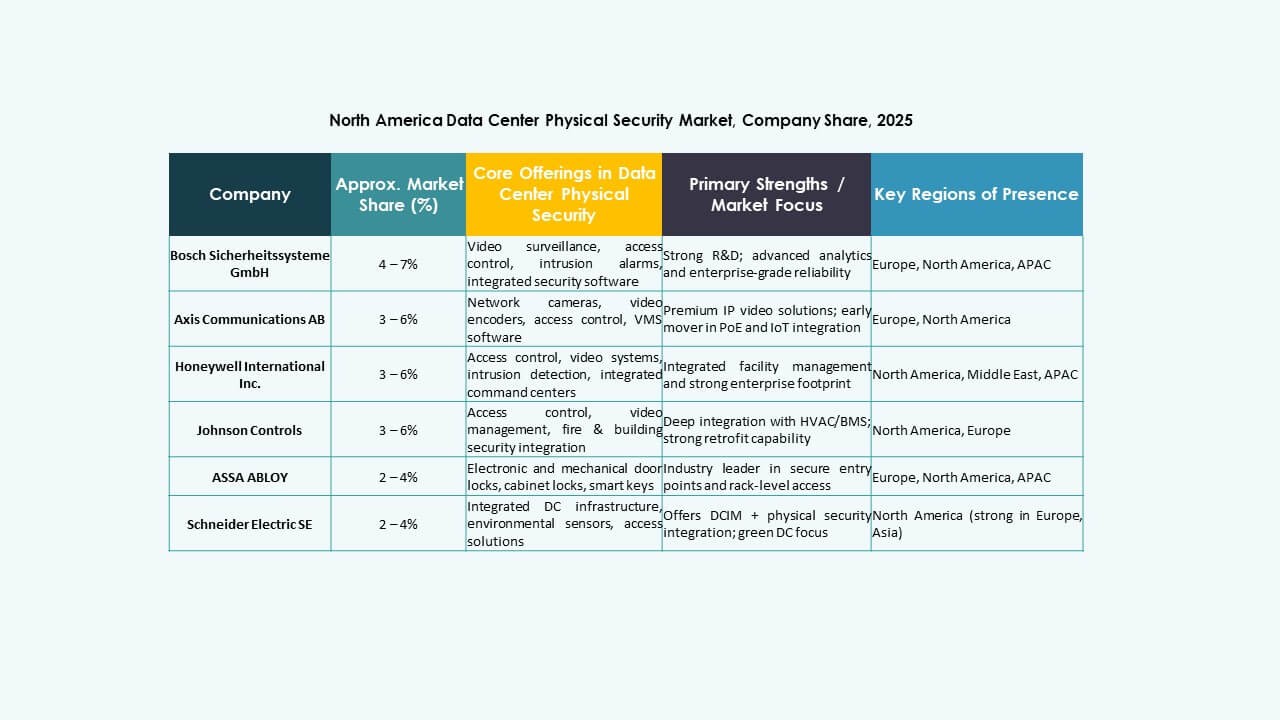

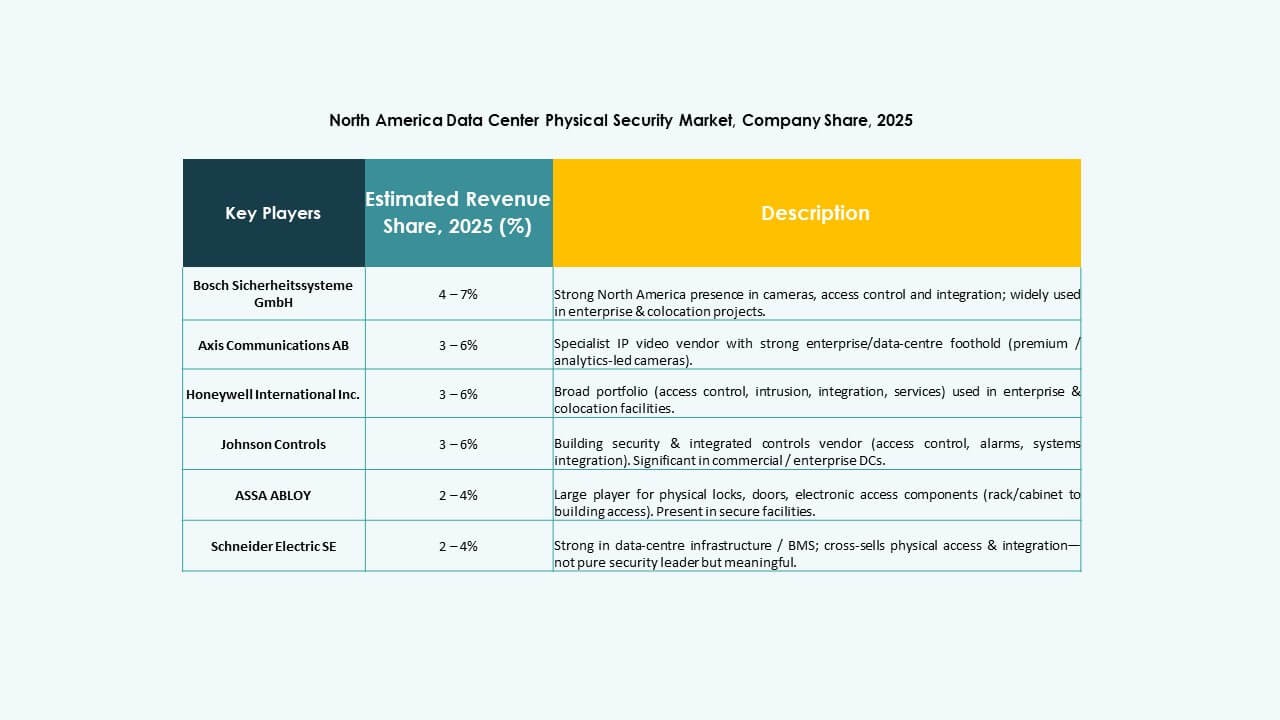

Competitive Insights:

- ABB Ltd.

- Allied Universal

- ASSA ABLOY AB

- Axis Communications AB

- Bosch Sicherheitssysteme GmbH (Bosch Security Systems)

- Cisco Systems, Inc.

- Fortinet, Inc.

- Genetec Inc.

- Honeywell International Inc.

- Johnson Controls International plc

- Palo Alto Networks, Inc.

- Schneider Electric SE

- Securitas AB

- Siemens AG

The competitive landscape centers on a mix of global security giants and specialized solution providers. Firms such as ABB, Bosch, and Schneider Electric invest heavily in integrated physical-security solutions combining access control, surveillance, and environmental monitoring. Companies like Axis Communications, Cisco, Genetec, and Fortinet leverage network and cybersecurity strength to offer converged physical-and-digital security systems. Service specialists such as Allied Universal and Securitas add value through managed security and on-site support. The market rewards players that deliver scalable, interoperable, compliance-ready security platforms. It drives consolidation and strategic partnerships. The overall environment remains fast-evolving, with constant innovation shaping vendor positioning. The North America Data Center Physical Security Market demands broad offerings that meet regulatory, operational, and threat-adaptation needs.

Recent Developments:

Recent Developments:

- In November 2025, Cisco Systems, Inc. announced new multi-customer management capabilities in its Security Cloud Control platform, enhancing hybrid mesh firewall deployment for Managed Service Providers.

- In June 2025, Genetec Inc. released updates to its Security Center SaaS platform, adding support for direct-to-cloud cameras, improved edge recording, and third-party analytics integrations.