Executive summary:

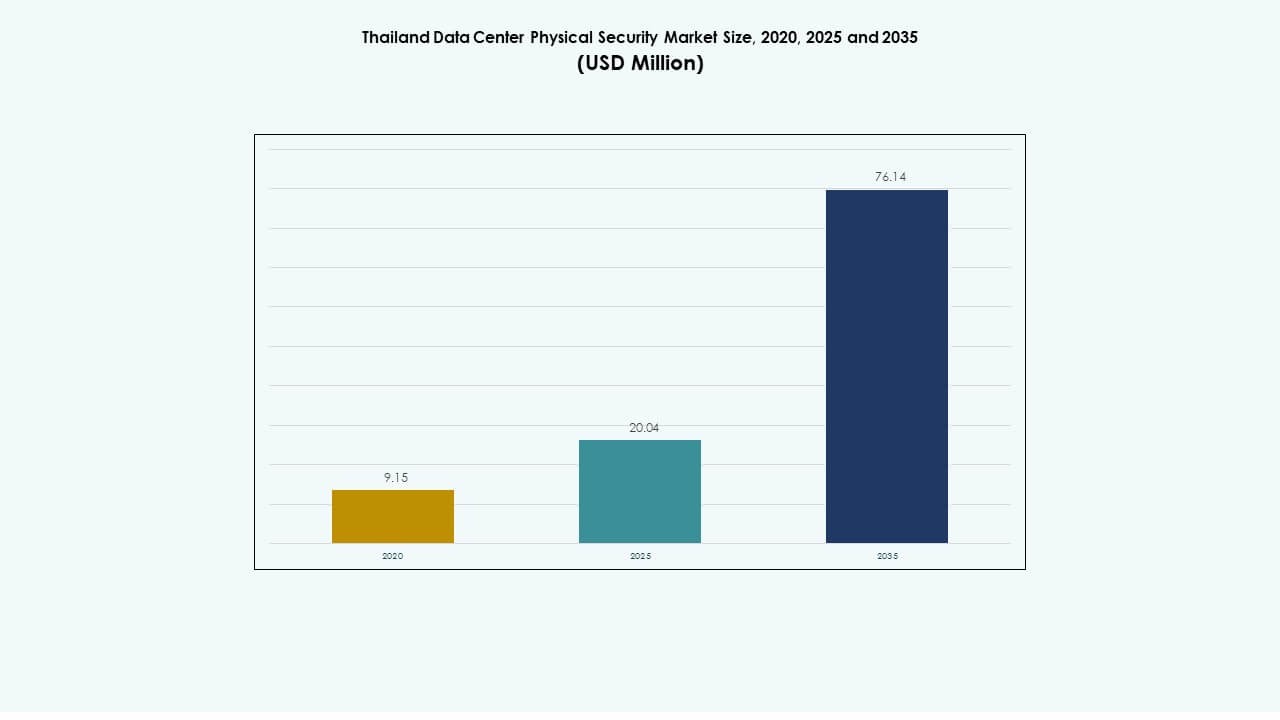

The Thailand Data Center Physical Security Market size was valued at USD 9.15 million in 2020 to USD 20.04 million in 2025 and is anticipated to reach USD 76.14 million by 2035, at a CAGR of 14.19% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2035 |

| Thailand Data Center Physical Security Market Size 2025 |

USD 20.04 Million |

| Thailand Data Center Physical Security Market, CAGR |

14.19% |

| Thailand Data Center Physical Security Market Size 2035 |

USD 76.14 Million |

Growing adoption of cloud computing, digital transformation, and data localization drives investment in secure infrastructure. Operators deploy advanced access control, AI-based surveillance, and biometric verification to protect critical assets. Rising regulatory compliance requirements and the push for green data centers support innovation in energy-efficient security systems. The market holds strategic value for investors as Thailand strengthens its position as a regional digital hub for Southeast Asia.

Bangkok leads the market with the highest concentration of hyperscale and colocation facilities due to strong connectivity and infrastructure readiness. The Eastern Economic Corridor follows, supported by government incentives and industrial growth. Secondary regions such as Chiang Mai and Phuket are emerging as potential hubs for edge data centers. This regional diversification enhances Thailand’s role in building resilient and secure digital infrastructure across the nation.

Market Drivers

Market Drivers

Growing Demand for Advanced Security Infrastructure in Expanding Data Ecosystem

The Thailand Data Center Physical Security Market benefits from growing data traffic, cloud services, and digital transformation initiatives. Increasing deployment of hyperscale and colocation centers pushes the need for multi-layered security. Operators invest in biometric authentication, perimeter protection, and AI-based surveillance systems. The government promotes digital economy policies that reinforce cybersecurity and data integrity. Businesses focus on compliance with international standards like ISO 27001 and PCI DSS. Security system providers collaborate with telecom operators to ensure resilient access management. Integration of intelligent video analytics enhances incident response speed. The market gains momentum from stronger policy frameworks and private investments.

Rising Focus on AI-Driven Surveillance and Predictive Threat Management

AI adoption transforms Thailand’s data center protection landscape with predictive monitoring and automated response. Machine learning tools identify anomalies across access points and network systems. Vendors introduce edge-enabled cameras that analyze real-time behavior patterns. Investors prioritize facilities with lower downtime risks and proactive security intelligence. Integration of IoT-based sensors enhances situational awareness for large campuses. Cloud-based control centers allow remote supervision and analytics sharing among multiple sites. It supports stronger operational visibility and faster decision-making. The market evolves toward self-learning surveillance ecosystems across critical facilities.

- For instance, ThaiCERT has reported a steady rise in cybersecurity incidents nationwide, highlighting growing risks to digital infrastructure and data centers. The agency emphasized the need for stronger monitoring systems and AI-based threat detection tools to enhance national resilience against evolving attacks.

Shift Toward Green and Energy-Efficient Security Systems

Sustainability initiatives drive deployment of low-power, efficient surveillance and access solutions. Smart lighting integration reduces operational costs across secured environments. Facilities deploy renewable energy sources to power security networks. Thailand’s data center operators emphasize compliance with green building standards such as LEED and EDGE. Manufacturers introduce eco-friendly enclosures and temperature-controlled systems to reduce waste. Remote energy monitoring ensures balance between security reliability and environmental goals. It reflects a broader regional trend toward sustainable digital infrastructure. Green innovation strengthens the market’s appeal to environmentally responsible investors.

Regulatory Push and Compliance Standards Supporting Market Growth

Stringent national policies elevate adoption of certified security solutions in data infrastructure. The Personal Data Protection Act (PDPA) enforces stricter monitoring and access requirements. Government-backed initiatives encourage investment in certified data center designs. Compliance mandates drive demand for advanced alarm management and log tracking systems. Security audits become part of standard operational practices across service providers. It improves investor confidence and transparency in operations. Collaboration between regulators and enterprises fosters innovation within compliance boundaries. These frameworks shape Thailand’s transition toward globally aligned security standards.

- For instance, Thailand’s Personal Data Protection Act (PDPA) enforces strict requirements for both digital and physical data security, compelling organizations to strengthen access control and compliance frameworks. These regulations have driven higher adoption of ISO 27001-certified and PCI DSS-compliant systems across Thailand’s expanding data center infrastructure.

Market Trends

Market Trends

Expansion of Hyperscale Facilities with Integrated Security Architectures

The Thailand Data Center Physical Security Market experiences strong growth from hyperscale facility construction. Major cloud operators expand regional footprints with integrated digital and physical security systems. AI-based visitor authentication replaces manual verification processes. Continuous surveillance integration supports zero-trust facility designs. Large campuses adopt modular security frameworks to match rapid capacity expansions. Investors fund scalable projects that align with smart city objectives. Energy-efficient surveillance infrastructure supports sustainability benchmarks. It transforms Thailand into a regional hub for advanced, high-density data infrastructure investments.

Adoption of Digital Twins for Security Planning and Simulation

Digital twin technology supports advanced modeling of security infrastructure before implementation. Operators simulate potential breaches to identify vulnerabilities within facility layouts. Predictive analytics enhance system maintenance and response planning. Real-time data integration allows instant feedback on access control performance. System integrators use simulation insights to refine response protocols. It improves efficiency in resource allocation and design optimization. These tools lower project costs while improving protection reliability. The trend strengthens Thailand’s position in adopting next-generation infrastructure intelligence.

Integration of Multi-Factor and Biometric Authentication Systems

Multi-factor authentication gains momentum across enterprises seeking higher access accountability. Facilities deploy retina scanners, facial recognition, and fingerprint readers to secure entry points. Smart card systems integrate with centralized monitoring platforms for unified control. Vendors collaborate with IT security teams to synchronize digital and physical identity management. AI algorithms reduce false positives during high-traffic hours. These tools improve operational transparency and personnel safety. It accelerates digital transformation across mission-critical facilities. Thailand becomes a model for secure and efficient data access management systems.

Collaboration Between Local Operators and Global Cloud Providers

Strategic partnerships drive infrastructure modernization across Thailand’s data ecosystem. Global players collaborate with regional providers to deploy tier-certified facilities. Shared investments ensure technology transfer and compliance with global security benchmarks. This cooperation encourages local workforce skill development in security technologies. Investors gain exposure to advanced operational frameworks that match international standards. The collaboration expands market visibility and competitiveness. It positions Thailand as an emerging hub for hybrid cloud and secure colocation services.

Market Challenges

High Initial Costs and Limited Local Expertise in Advanced Security Systems

The Thailand Data Center Physical Security Market faces high capital requirements for deployment of next-generation systems. Small operators struggle to fund upgrades to AI-enabled cameras, biometric devices, and intrusion prevention networks. Limited local expertise in system integration increases dependence on foreign vendors. Maintenance costs rise due to complex multi-layer architectures. The shortage of certified technicians delays project timelines and operational readiness. It impacts scalability across mid-sized and edge data facilities. Vendors focus on skill training programs to bridge the capability gap. Financial barriers remain a concern for sustainable adoption across smaller enterprises.

Complex Regulatory Environment and Data Sovereignty Constraints

Regulatory fragmentation poses compliance challenges for multinational data center operators. Frequent policy revisions delay investment decisions and licensing approvals. Data sovereignty rules complicate cross-border information management. Enterprises require continuous updates to align with PDPA and cybersecurity guidelines. Coordination gaps between agencies create procedural delays. It limits operational flexibility for hybrid and multi-tenant data centers. Global providers often seek joint ventures to ensure local compliance. Standardization of certification and audit processes is essential for consistent market expansion.

Market Opportunities

Market Opportunities

Rising Edge Data Center Investments Supporting Regional Expansion

Edge computing expansion opens new opportunities across provincial zones. Telecom providers deploy micro-data centers with integrated physical protection layers. These installations strengthen local connectivity for smart cities and 5G deployment. It enables faster response times for latency-sensitive applications. Businesses invest in compact, energy-efficient protection systems suitable for distributed networks. The expansion beyond Bangkok diversifies revenue sources and increases infrastructure density. Regional investors gain long-term value from scalable and low-cost deployments. This shift reinforces Thailand’s role in decentralized digital infrastructure.

Adoption of AI and Robotics in Security Automation Systems

Automation and robotics redefine monitoring and maintenance across secured data environments. AI-driven patrol robots perform perimeter inspections and detect anomalies with precision. Integrated drones enhance aerial surveillance coverage across large campuses. It reduces labor dependency and minimizes security lapses. Vendors experiment with hybrid models combining AI, robotics, and predictive analytics. Automated systems also support 24/7 operational continuity. The opportunity enhances efficiency while addressing manpower shortages in high-security zones.

Market Segmentation

By Data Center Size

Large data centers dominate Thailand’s market due to hyperscale and colocation expansion. Operators like ST Telemedia and NTT establish massive facilities supporting enterprise workloads. Medium-sized data centers contribute through managed service providers and regional hosting firms. Small centers serve niche and edge applications. It benefits from growing SME digitalization and IoT adoption. Large facilities capture the majority share due to robust investments and global client base. Growth in this segment accelerates demand for integrated security frameworks and advanced surveillance systems.

By Component

Solutions hold a higher market share compared to services, driven by hardware and software adoption. Access control, surveillance cameras, and intrusion systems form the backbone of physical protection. Service providers offer integration and maintenance support for seamless operation. Enterprises prioritize scalable, cloud-integrated solutions for multi-site monitoring. It strengthens long-term reliability and uptime. Growth in managed security services complements equipment sales. This segment benefits from rising automation and predictive analytics integration.

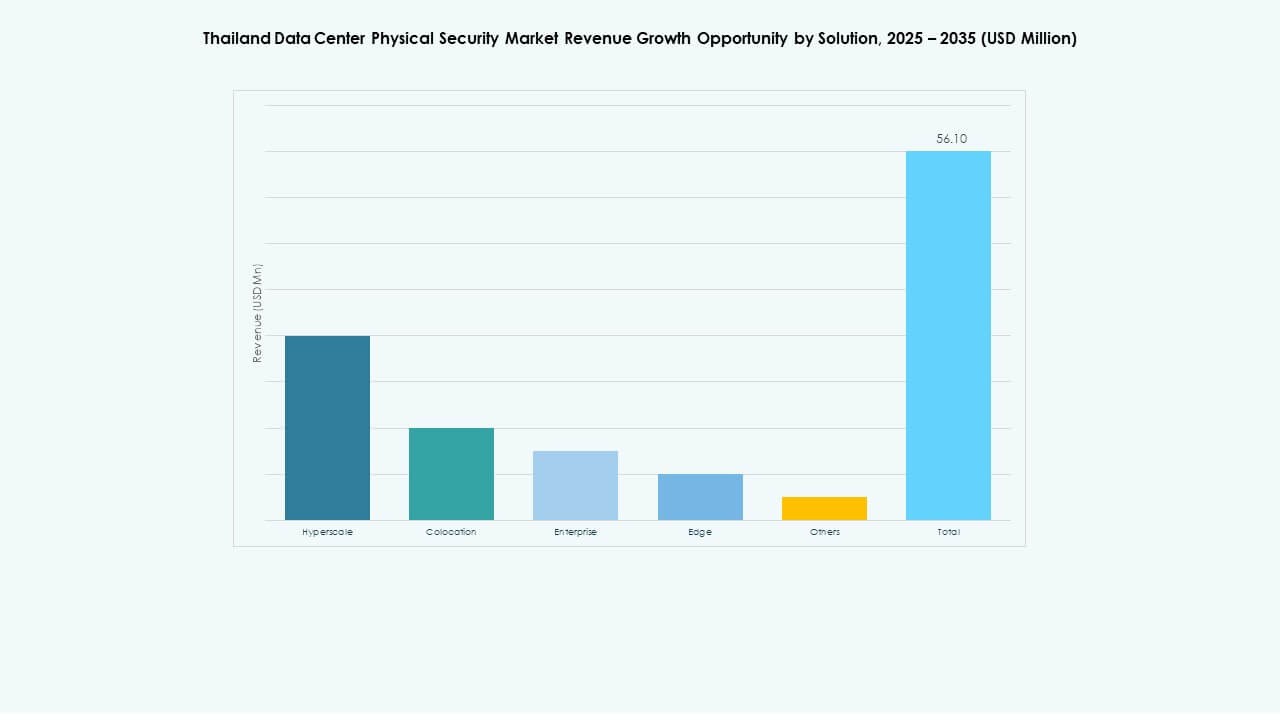

By Solution

Video surveillance leads due to continuous demand for high-resolution and analytics-driven monitoring. Access control systems follow with biometric and RFID-based upgrades. Monitoring and detection tools enhance layered security through real-time alerts. Other segments include intrusion sensors and environmental control devices. It reflects Thailand’s shift toward integrated, smart surveillance ecosystems. Advanced AI integration allows faster response to potential threats. The trend supports higher operational visibility across hyperscale environments.

By Services

System integration dominates among service categories, ensuring seamless deployment across facilities. Consulting services guide design and risk assessments during initial phases. Maintenance and support play key roles in lifecycle management. Vendors provide predictive maintenance contracts for critical hardware. It improves system reliability and minimizes downtime risks. Automation tools streamline maintenance processes for efficiency. Growing demand for end-to-end managed solutions boosts this segment’s relevance in ongoing expansions.

By Security Layer

Perimeter and building access security remain crucial for large-scale campuses. Data hall and rack security gain traction in colocation and enterprise facilities. It supports granular access monitoring for critical servers. Integration between digital ID systems and cabinet-level locking enhances compliance. Video and sensor-based alerts reduce manual supervision needs. Demand for unified dashboards across layers grows. Each layer contributes to a zero-trust environment that reinforces infrastructure resilience.

By Data Center Type

Hyperscale data centers dominate due to rapid digital growth and cloud provider expansion. Colocation facilities serve enterprises seeking flexibility and cost efficiency. Edge data centers emerge to handle latency-sensitive operations in secondary cities. Enterprise centers focus on private workloads with high customization. It shows balance between scalability, control, and agility. Hyperscale developments drive higher security spending per square meter. Continuous hybrid adoption strengthens the segment’s market leadership.

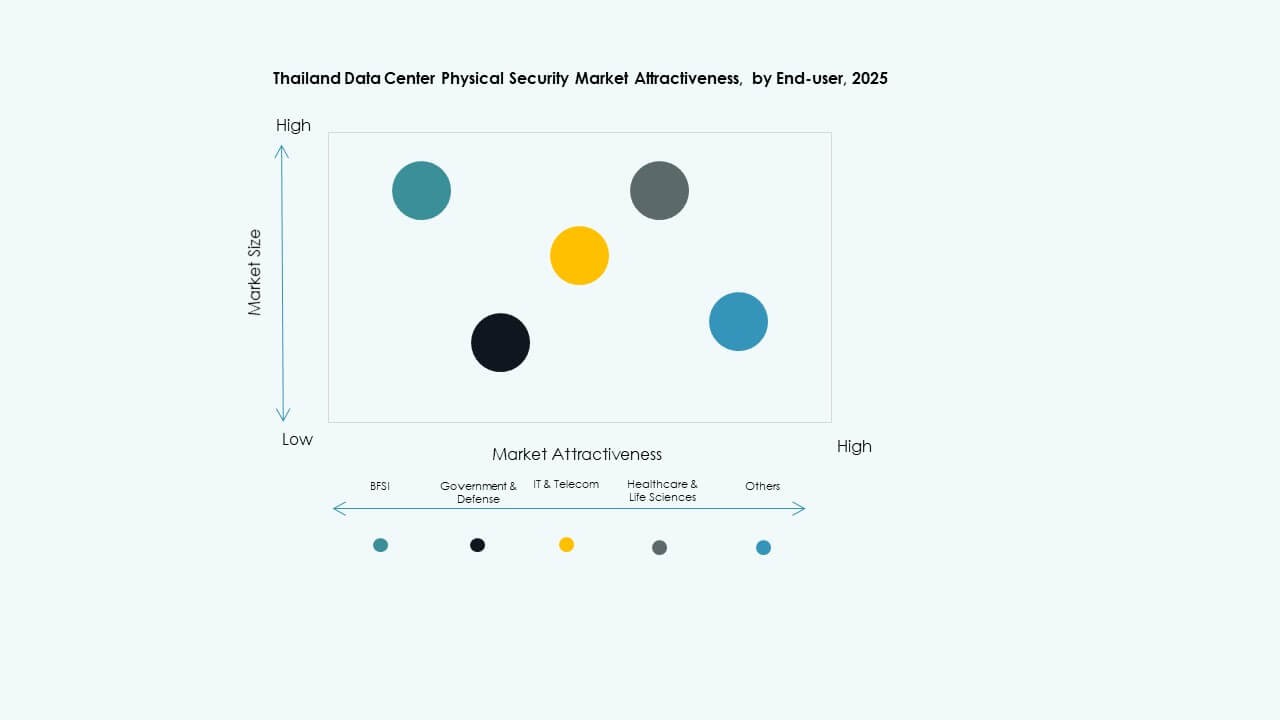

By End-User

IT and telecom sectors lead with large data handling requirements. BFSI follows due to compliance-driven investments in advanced monitoring systems. Government and defense prioritize secure facilities for critical data sovereignty. Healthcare, manufacturing, and retail sectors also adopt physical security tools. It reflects digital maturity across industries adopting AI and automation. Cloud service providers enhance data resilience and uptime assurance. The market expands with strong enterprise digital infrastructure modernization.

Regional Insights

Regional Insights

Bangkok Metropolitan Region – Leading Data Center Hub (65% Market Share)

Bangkok dominates the Thailand Data Center Physical Security Market due to superior connectivity and infrastructure. The area hosts hyperscale and colocation facilities supported by strong fiber networks. Government initiatives and international investment flow fuel development. It benefits from advanced logistics and availability of skilled workforce. Most tier-certified facilities operate within the capital region. The concentration of cloud providers accelerates security technology deployment. Bangkok’s ecosystem anchors Thailand’s position as a regional digital powerhouse.

- For instance, Empyrion Digital operates a 12 MW data center facility in Bangkok, marking one of Thailand’s notable new builds. According to Research & Markets, the country hosts 32 operational colocation data centers and 17 upcoming projects, with total investments expected to exceed USD 2.3 billion by 2027. These developments reflect Thailand’s rapid infrastructure growth fueled by cloud and AI demand.

Eastern Economic Corridor – Emerging Industrial and Digital Cluster (25% Market Share)

The Eastern Economic Corridor (EEC) shows rapid expansion in industrial and technology zones. Infrastructure incentives attract data-driven enterprises to Chonburi and Rayong provinces. Large industrial estates integrate smart surveillance and access systems for secure operations. It supports hybrid data hosting models for manufacturing and logistics clients. Connectivity with neighboring ASEAN markets enhances the EEC’s strategic appeal. The area’s proximity to Bangkok ensures operational synergy with national networks. Investments here strengthen Thailand’s edge infrastructure foundation.

- For instance, Chonburi hosts DayOne’s 120 MW Chonburi Tech Park and Bridge Data Centres’ planned 200 MW campus, integrating smart surveillance and biometric access systems.

Northern and Southern Regions – Growing Edge Data Center Development (10% Market Share)

Secondary regions like Chiang Mai and Phuket witness rising micro-data center projects. Edge deployments target smart city development and local content delivery. It ensures faster data access and reduced latency for users outside the capital. Investments in renewable energy and cooling systems attract eco-conscious operators. Government digital inclusion programs support infrastructure decentralization. Growing regional cloud zones balance national data capacity and enhance overall resilience. These trends drive nationwide digital equity and network efficiency.

Competitive Insights:

- ABB Ltd

- Johnson Controls

- Honeywell International Inc.

- Bosch Sicherheitssysteme GmbH

- Siemens AG

- Cisco Systems, Inc.

- Axis Communications AB

- Genetec Inc.

- ASSA ABLOY

- Securitas AB

The competitive landscape of the Thailand Data Center Physical Security Market shows a mix of global heavyweights and specialized system providers competing for infrastructure contracts. Major firms such as ABB, Johnson Controls, Honeywell, and Bosch lead with broad portfolios that cover video surveillance, access control, intrusion detection, and integrated security solutions. Siemens and Cisco bring strong automation and networking expertise, which data center operators value for converged cyber-physical security. Specialized players like Axis Communications and Genetec focus on advanced IP-based surveillance and unified security management. ASSA ABLOY and Securitas AB provide niche strength in door access and manned security services. Competition centers on solution breadth, integration capabilities, vendor reliability, and compliance readiness. This environment drives innovation and encourages firms to offer turnkey, scalable security platforms to meet evolving data center requirements.

Recent Developments:

- In November 2025, Cisco Systems, Inc. expanded its Security Cloud Control platform by adding managed service provider features and AI-driven automation to enhance hybrid firewall integration and scalability for data center security management.

- In October 2025, ASSA ABLOY acquired Kentix GmbH, a German company specializing in monitoring and access control products designed for data centers, enhancing their capabilities in physical security for this sector.

- In April 2025, Security 101 acquired ISSI, a security integrator specializing in high-security systems for enterprise clients, boosting its data center security capabilities. Although Security 101 wasn’t in your list, it highlights active acquisition trends in the market.

- In January 2025, ASSA ABLOY also acquired InVue, a Charlotte-based provider of asset protection and access control solutions, aligning with their strategy to expand globally in access control and asset protection.

- In June 2024, Honeywell International Inc. completed the acquisition of Carrier Global Corporation’s Global Access Solutions business for $4.95 billion, enhancing its building automation portfolio with advanced access control solutions like LenelS2, Onity, and Supra, which support security needs in data centers including those in Spain.

- In December 2024, Bosch Sicherheitssysteme GmbH sold its security and communications technology product business to the European investment firm Triton. The transaction included three business units Video, Access and Intrusion, and Communication as Bosch aims to focus more on systems integration business.