Executive summary:

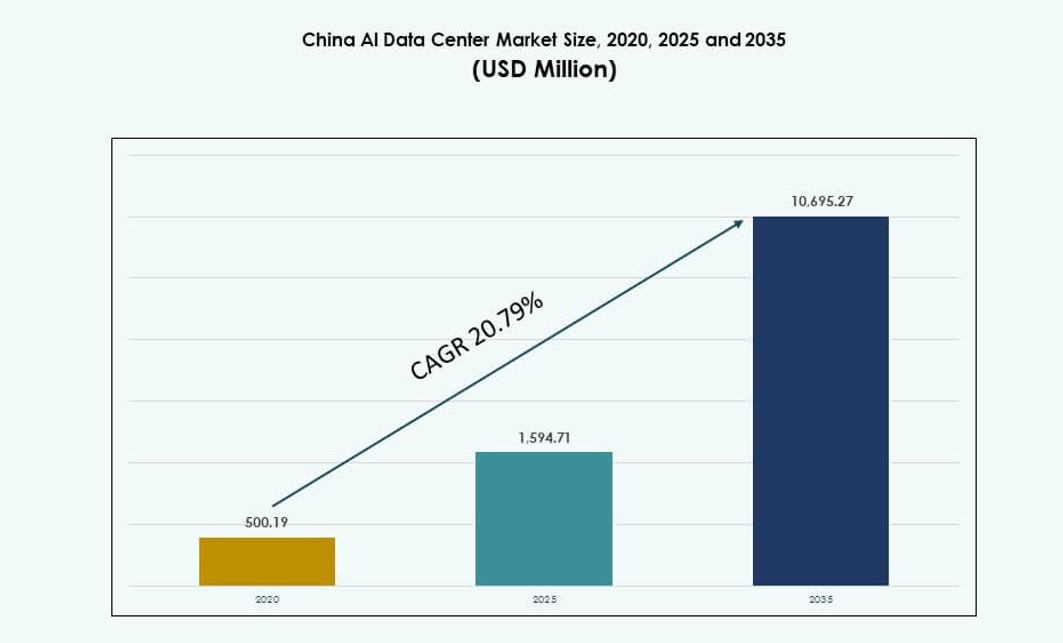

The China AI Data Center Market size was valued at USD 500.19 million in 2020 to USD 1,594.71 million in 2025 and is anticipated to reach USD 10,695.27 million by 2035, at a CAGR of 20.79% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2035 |

| China AI Data Center Market Size 2025 |

USD 1,594.71 Million |

| China AI Data Center Market, CAGR |

20.79% |

| China AI Data Center Market Size 2035 |

USD 10,695.27 Million |

The market is witnessing strong momentum due to rapid AI workload growth, driven by large language models, machine learning, and enterprise automation. Operators are deploying high-density GPU clusters with advanced cooling to meet compute demands. Policy support for sovereign AI infrastructure is accelerating hyperscale data center buildouts across key provinces. Liquid cooling, software orchestration, and green energy integration are becoming standard features. The market plays a strategic role in China’s digital and AI leadership ambitions. Businesses depend on this infrastructure for scalable AI deployments. Investors view it as a core asset in China’s evolving digital economy. The sector aligns with long-term national innovation goals.

Northern China leads the market due to strong government support, favorable policies, and early deployment zones in Beijing and Hebei. Eastern regions such as Shanghai and Hangzhou follow closely, driven by enterprise AI adoption and robust connectivity. Southwestern provinces like Guizhou and Sichuan are emerging hubs due to low-cost renewable power and land availability. These areas attract AI data center investments from hyperscalers and telecoms. Central China is also expanding, supported by urban digitization projects. This geographic spread enables balanced national coverage and resilience. The China AI Data Center Market benefits from this multi-regional push toward AI infrastructure scale.

Market Dynamics:

Market Drivers

Accelerated AI Workload Growth Driving Demand for High-Performance, AI-Optimized Infrastructure

The China AI Data Center Market is experiencing robust growth due to surging demand for high-density compute infrastructure to support AI training and inference workloads. Enterprises and cloud providers are deploying powerful GPU clusters to process large-scale AI models, particularly for natural language processing and computer vision. Rising demand for generative AI models, including LLMs, is pushing infrastructure design toward liquid cooling and ultra-low latency interconnects. Domestic tech giants are investing in AI-first infrastructure to reduce reliance on foreign compute. This shift supports national goals for digital sovereignty. It is fueling significant capital investment into new data center campuses tailored for AI. China’s Five-Year Plans have embedded AI as a core growth pillar, aligning regulatory support with infrastructure expansion. The market enables enterprises to scale AI capabilities in line with global leaders.

- For instance, at the Apsara Conference in September 2025, Alibaba Cloud unveiled its Qwen3-Max model with over 1 trillion parameters, featuring advanced reasoning and agentic capabilities. The company also introduced Qwen3-Omni and Qwen3-VL, reinforcing its position as a full-stack AI provider alongside major investments in AI-optimized data center infrastructure.

Strategic Push Toward Sovereign Compute Driving Domestic Innovation and Chip Self-Sufficiency

China’s push for self-reliant AI infrastructure is advancing innovation in chip design and system architecture. National initiatives are supporting the development of domestic alternatives to foreign GPUs, including AI-accelerated chips from firms like Huawei and Cambricon. Local vendors are optimizing server configurations for AI-heavy loads while ensuring compliance with evolving cybersecurity and data localization laws. The China AI Data Center Market benefits from state-backed efforts to localize supply chains and reduce import dependence. Sovereign compute has emerged as a strategic priority, prompting localized infrastructure zones. It helps companies meet regulatory standards for critical AI workloads. Innovation extends across hardware, cooling systems, and orchestration platforms. These developments are reshaping the competitive landscape in China’s AI infrastructure sector.

Expansion of Hyperscale AI Zones and Provincial Incentives Bolstering Infrastructure Buildout

AI-specialized zones across China’s major provinces are accelerating greenfield data center development through incentives and regulatory fast-tracking. Regions like Beijing, Hebei, and Inner Mongolia offer favorable policies, tax breaks, and access to renewable power. Local governments are aligning AI infrastructure growth with regional innovation hubs, increasing deployment speed and scale. The China AI Data Center Market is seeing a surge in hyperscale campus activity tailored for AI. Operators are building multi-phase campuses capable of supporting liquid-cooled racks and modular AI pods. It is drawing investment from cloud hyperscalers, telecom operators, and private equity firms. Provinces are racing to become AI compute hubs by integrating fiber networks, edge access, and grid support. These factors are unlocking capital flow into AI-optimized sites.

- For instance, China Mobile has expanded its hyperscale data center presence in Inner Mongolia, including large facilities in Hohhot designed to support AI workloads. These sites integrate high-efficiency cooling systems and scalable power infrastructure aligned with national AI development goals.

Digital Belt and Road Strategy Expanding China’s AI Infrastructure Footprint Across APAC

China’s Digital Belt and Road initiative is encouraging AI infrastructure expansion beyond domestic borders. AI-ready data centers in countries like Laos, Pakistan, and Malaysia are supported by Chinese investment, often managed by Chinese operators. This outward push strengthens cross-border data flows and aligns with regional AI ecosystem building. It reinforces China’s leadership in regional AI cloud services. The China AI Data Center Market plays a foundational role in anchoring these efforts. It provides the compute backbone required for international AI model deployment and regional workload sharing. By developing cross-border capacity, operators support real-time AI applications with latency-sensitive demands. China’s AI data centers are acting as central nodes in a growing regional compute network.

Market Trends

Adoption of Liquid Cooling and Thermal Innovations to Support High-Density AI Clusters

Thermal management is evolving rapidly to support growing rack densities and GPU clusters. Direct-to-chip liquid cooling and immersion systems are becoming common across AI-focused facilities. Operators are investing in high-efficiency cooling to maintain performance and meet PUE targets. These technologies allow for better management of thermal loads generated by AI training workloads. The China AI Data Center Market is seeing strong adoption of advanced thermal design. It improves operational efficiency and supports compliance with carbon neutrality goals. Vendors are offering modular liquid cooling platforms to retrofit or scale dense deployments. Heat reuse systems are emerging to recover and redirect energy to nearby facilities. AI training loads are pushing traditional cooling systems beyond capacity, prompting widespread innovation.

Rise of AI-Oriented Edge and Micro Data Centers for Latency-Sensitive Use Cases

Edge computing is playing a key role in enabling AI inference closer to data sources and end users. AI workloads in sectors like retail, healthcare, and manufacturing require ultra-low latency and high bandwidth at the edge. Micro data centers equipped with GPU accelerators are being deployed in smart cities and industrial parks. The China AI Data Center Market is witnessing growth in AI-capable edge nodes. It supports localized model inference, real-time analytics, and data filtering at scale. Operators are building AI inference pods within 5G base stations and metro nodes. Edge deployments enhance responsiveness and reduce strain on core infrastructure. Compact systems with AI-optimized cooling are expanding beyond tier-1 cities.

Shift Toward AI Cloud Services Integration and Disaggregated Infrastructure Models

AI cloud offerings are becoming more modular, scalable, and industry-specific. Service providers are integrating GPU-as-a-Service and AI platform layers into their infrastructure models. Disaggregation of compute, storage, and networking is optimizing utilization and workload placement. The China AI Data Center Market supports these shifts by enabling composable infrastructure design. It improves infrastructure flexibility for handling dynamic AI workloads. Operators are deploying software-defined networking and storage orchestration tools. API-based resource provisioning supports multitenant AI environments. These trends allow for cost-effective scaling and efficient hardware reuse. Enterprises gain better control over workload mapping and optimization.

Growth of AI Model Training-as-a-Service and Academia-Industry Infrastructure Collaboration

The rise of AI model training services is transforming how compute is consumed in academic and enterprise settings. Institutions and startups rely on shared compute clusters managed by universities or AI parks. Collaborative training centers offer access to large-scale infrastructure for algorithm development. The China AI Data Center Market facilitates this ecosystem through shared facilities with GPU clusters. It lowers entry barriers for AI model innovation and testing. Government-backed research labs are partnering with data center operators for national AI programs. High-performance compute zones are being linked with universities and incubators. Shared infrastructure models are strengthening AI R&D nationwide.

Market Challenges

High Power Demand, Resource Allocation, and Grid Stability Remain Persistent Infrastructure Constraints

High-density AI workloads are creating extreme power demand per rack, challenging energy infrastructure limits. Maintaining power availability in constrained urban zones is increasingly difficult. Grid limitations and inconsistent power supply in certain provinces hinder data center performance. The China AI Data Center Market faces pressure to secure green and reliable energy. It requires continuous coordination with utilities and provincial governments. Operators must design for redundancy and invest in on-site backup systems. Cooling-related power consumption adds further stress on overall efficiency. Delays in power approvals and load caps affect project timelines and operational scalability.

Regulatory Barriers, Export Controls, and Hardware Dependency Impact Infrastructure Continuity

Geopolitical tensions and export controls on advanced semiconductors restrict access to top-tier AI chips. Sanctions limit procurement of high-performance GPUs from U.S. firms, impacting model training capacity. Domestic chipmakers are still scaling production to match global benchmarks. The China AI Data Center Market depends on policy workarounds, local R&D, and supply diversification. Regulatory uncertainties around cybersecurity, AI ethics, and data localization add complexity. Operators must ensure compliance across evolving national and regional frameworks. Infrastructure investments face delays when navigating licensing and audit protocols. Data sovereignty requirements require onshore hosting, restricting cross-border optimization.

Market Opportunities

Rising Demand for Sovereign AI Compute Zones Creates Investment Opportunities Across Core Provinces

Government push for sovereign AI compute is unlocking investment opportunities in AI-ready campuses across key provinces. Beijing, Shanghai, and Hebei are seeing multi-phase project announcements by public and private stakeholders. The China AI Data Center Market offers long-term returns for investors aligned with national compute strategy. It supports deployment of strategic AI services across industries. Provincial alignment with central AI goals helps accelerate land access and approval timelines. Operators can benefit from demand certainty and long-term usage contracts.

Expansion of AI-Driven Smart Cities, Industrial Parks, and Edge Zones Unlocks New Revenue Models

AI use in smart cities and connected infrastructure is driving demand for decentralized, high-availability compute. Municipal bodies are incorporating data center infrastructure in planning models for AI-powered surveillance, transport, and governance. The China AI Data Center Market plays a key role in delivering localized compute for these initiatives. Operators can build revenue models around low-latency services, micro-facilities, and tiered access. Edge deployments in industrial parks support predictive maintenance, quality control, and real-time decision-making.

Market Segmentation

By Type

The hyperscale segment dominates the China AI Data Center Market, driven by large-scale AI training and cloud deployment needs. Hyperscalers like Alibaba, Tencent, and Baidu operate multi-megawatt campuses with AI-optimized architecture. Edge/micro data centers are gaining traction in smart city deployments and latency-sensitive workloads. Colocation and enterprise segments cater to regulated industries and private infrastructure preferences. Hyperscale remains the core focus due to its scalability, energy efficiency, and ability to support sovereign compute mandates.

By Component

Hardware holds the largest market share, driven by demand for GPU servers, accelerators, and cooling systems. AI workloads require specialized compute, pushing investments into liquid-cooled racks and high-speed interconnects. Software & orchestration solutions are growing rapidly due to increasing need for AI resource scheduling, workload automation, and DCIM integration. Services such as facility design, remote operations, and compliance monitoring are also expanding. The China AI Data Center Market reflects strong hardware-led infrastructure growth with rising software orchestration support.

By Deployment

Cloud deployment dominates the China AI Data Center Market as enterprises shift AI training and inference to public cloud platforms. On-premise models remain critical in government, finance, and defense due to data control requirements. Hybrid deployments are increasing across regulated sectors, combining public cloud scalability with on-premise compliance. Operators are offering flexible AI-as-a-Service models integrated across deployment types. Cloud models benefit from scalability and fast provisioning, while hybrid models address workload-specific governance needs.

By Application

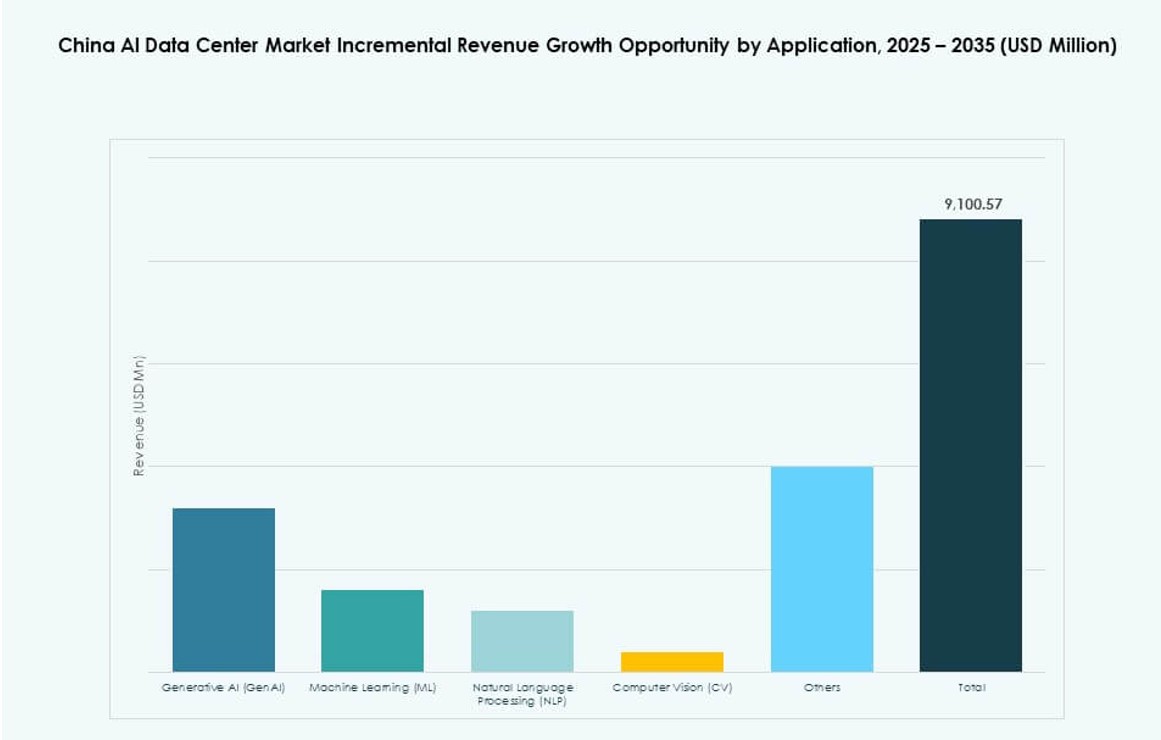

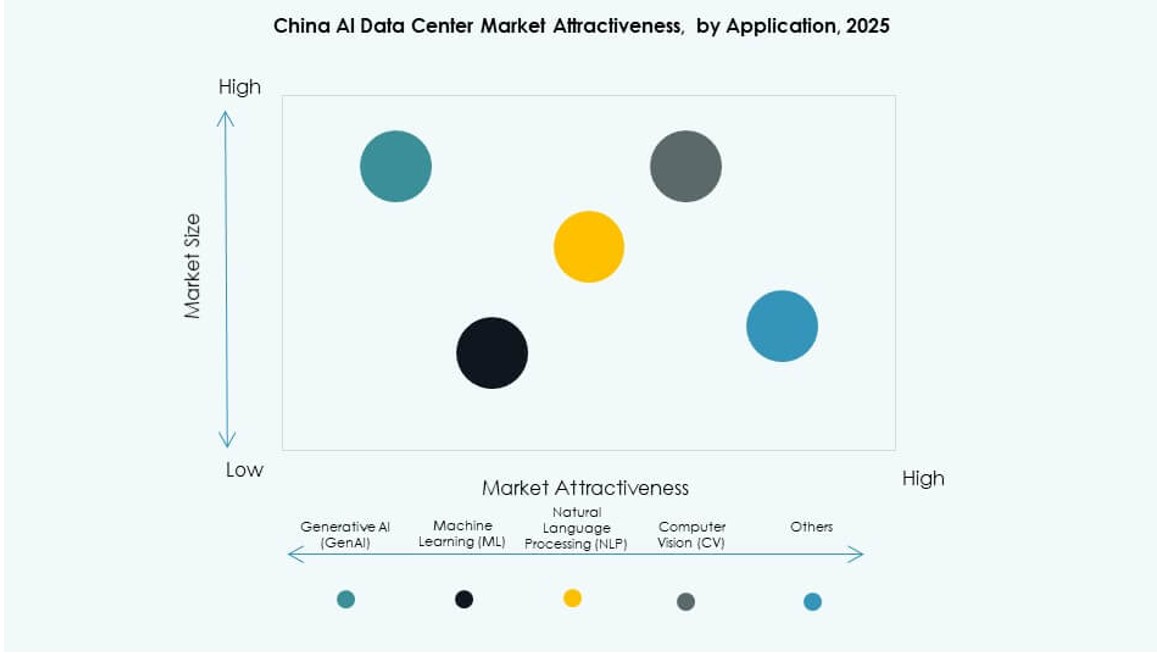

Machine Learning (ML) leads in deployment volume, driven by widespread use across industry verticals. Generative AI (GenAI) is seeing the fastest growth with rising adoption of large language models. Natural Language Processing (NLP) is widely used in e-commerce, government, and customer service applications. Computer Vision (CV) is vital in manufacturing, surveillance, and healthcare use cases. The China AI Data Center Market reflects an expanding workload mix, with GenAI and ML driving infrastructure scale and customization.

By Vertical

IT and telecom dominate demand, followed by BFSI, healthcare, and manufacturing. AI services in IT and telecom include chatbot deployment, fraud detection, and predictive analytics. Healthcare uses AI for imaging analysis, diagnostics, and operational efficiency. Manufacturing adopts AI for quality inspection, predictive maintenance, and robotics. BFSI sectors rely on AI for risk scoring and customer personalization. The China AI Data Center Market supports vertical-specific deployments through modular design and flexible service tiers.

Regional Insights

Northern China Leads the Market with Over 35% Share Due to Policy Support and High Compute Density

Northern China, led by Beijing, holds over 35% market share due to its dense concentration of hyperscale zones and state-aligned AI projects. The region hosts major AI parks and research centers with access to national-level funding and academic partnerships. It benefits from regulatory fast-tracking and early 5G rollouts. The China AI Data Center Market finds strong demand from government, telecom, and cloud majors concentrated in this subregion. Operators in Beijing, Tianjin, and Hebei focus on sovereign compute infrastructure. Energy grid modernization supports high-density rack deployment.

- For instance, in April 2025, Baidu confirmed that it had deployed a large‑scale cluster of 30,000 third‑generation Kunlun AI chips to support training of advanced large language models. The company stated that the cluster is operational and capable of handling high‑intensity AI training workloads, reflecting progress in domestic AI compute infrastructure development.

Eastern China Holds Over 30% Share Fueled by Enterprise AI Demand and Strong Cloud Ecosystem

Eastern China accounts for over 30% of market share, anchored by cities like Shanghai, Hangzhou, and Suzhou. The region is home to large enterprise AI deployments in fintech, retail, and logistics. It supports hybrid infrastructure models for multinational firms and domestic unicorns. The China AI Data Center Market benefits from strong data center ecosystems and access to skilled digital talent in the east. Proximity to industrial clusters drives demand for vertical-specific AI applications. Eastern China leads in green data center development and commercial AI services.

Southwest and Central Regions Are Emerging with Around 20% Share Each Due to Strategic Location and Energy Availability

Southwest provinces such as Guizhou and Sichuan offer low electricity prices, access to hydropower, and abundant land. Central provinces like Hubei and Henan benefit from expanding fiber networks and government-backed innovation zones. Each region holds approximately 20% market share and is gaining traction among operators seeking cost-effective AI infrastructure sites. The China AI Data Center Market is seeing investment into second-tier cities in these zones. These subregions support edge deployment, energy-efficient campuses, and long-term AI hub development strategies.

- For instance, in April 2025, Huawei confirmed the expansion of its Ascend 910C chip deployment strategy, highlighting advancements in AI training infrastructure using domestically developed processors. The company emphasized that these chips were ready for mass shipment to support AI clusters across China.

Competitive Insights:

- Chindata Group

- GDS Holdings

- 21Vianet

- Microsoft (Azure)

- Amazon Web Services (AWS)

- Google Cloud / Alphabet

- Meta Platforms

- Digital Realty Trust

- Equinix

- NVIDIA

The China AI Data Center Market features a dynamic mix of domestic operators and global cloud hyperscalers competing across scale, performance, and AI readiness. Chindata, GDS Holdings, and 21Vianet dominate local infrastructure with strong land banks and partnerships. Global leaders like AWS, Azure, and Google are expanding selectively in compliance with regulatory limits. Tech firms such as NVIDIA and Meta are driving demand for AI-specific compute and infrastructure optimization. It reflects growing investment in GPU clusters, liquid cooling, and sovereign compute zones. Competitive differentiation now hinges on scalability, power efficiency, and vertical AI service integration. Market leaders are aligning with government-backed zones to gain access to power and incentives. Strategic partnerships and edge deployments are helping firms expand into emerging provinces and second-tier cities.

Recent Developments:

- In January 2026, Lenovo announced a partnership with Nvidia at CES 2026 to launch the “Lenovo AI Cloud Gigafactory with NVIDIA,” a co‑developed data center solution that integrates liquid‑cooled hybrid AI infrastructure with Nvidia’s advanced computing platforms. This initiative aims to reduce AI environment deployment time drastically and enhance cloud provider capabilities.

- In September 2025, Alibaba announced a strategic partnership with Nvidia that includes collaboration on AI products and a broader plan to expand its data center footprint internationally. The alliance supports Alibaba’s efforts to scale AI solutions and related infrastructure, reinforcing its positioning in high‑performance compute services.

- In September 2025, Huawei unveiled innovations for AI data centers at its Data Center Innovation Summit during HUAWEI CONNECT 2025, releasing solutions like Xinghe AI Fabric 2.0 and next-gen AI data lake products in collaboration with partners such as Cineca and Yazhouwan National Laboratory.

- In April 2025, China launched its first commercial underwater data center off Hainan Province, optimizing colocation for AI workloads with advanced cooling amid rapid market growth projected through 2030.