Executive Summary:

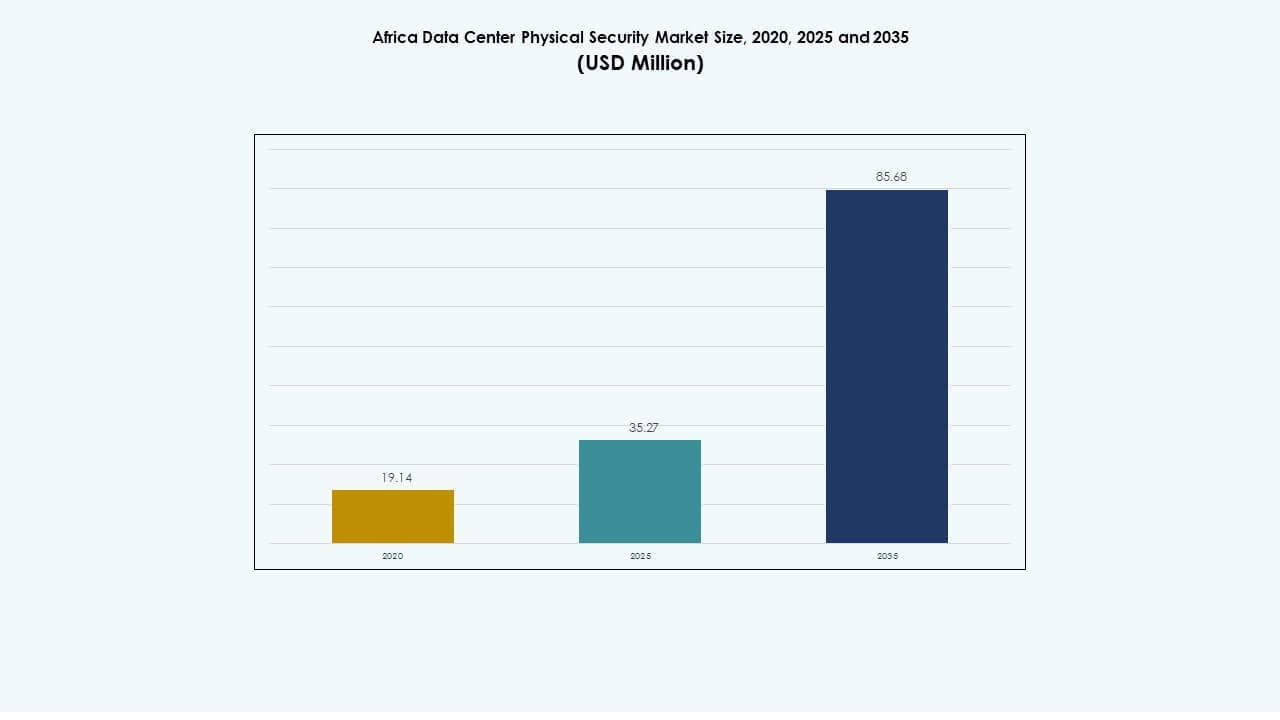

The Africa Data Center Physical Security Market size was valued at USD 19.14 million in 2020 to USD 35.27 million in 2025 and is anticipated to reach USD 85.68 million by 2035, at a CAGR of 9.31% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2035 |

| Africa Data Center Physical Security Market Size 2025 |

USD 35.27 Million |

| Africa Data Center Physical Security Market, CAGR |

9.31% |

| Africa Data Center Physical Security Market Size 2035 |

USD 85.68 Million |

Rising cloud adoption, stronger regulatory focus, and wider deployment of AI-enabled surveillance drive security modernization across African facilities. Operators integrate biometrics, automated access control, and unified monitoring tools to strengthen infrastructure resilience. Innovation accelerates as providers adopt automation and intelligent analytics for incident response. The market holds strong strategic value because secure operations support enterprise growth and regional digital transformation. Investors focus on long-term opportunities linked to hyperscale, colocation, and edge expansion across major cities.

West and Southern Africa lead due to high enterprise demand and strong hyperscale and telecom activity. North Africa follows with growing adoption across Egypt and Morocco supported by rising digitization efforts. East Africa emerges as a fast-developing hub driven by Kenya, Rwanda, and Ethiopia expanding their digital ecosystems. Regional momentum increases as countries push for improved connectivity, secure cloud zones, and compliant data infrastructure.

Market Drivers

Market Drivers

Growing Investment in Secure Digital Infrastructure Across Emerging African Hubs

The Africa Data Center Physical Security Market strengthens as many countries expand digital infrastructure. Operators deploy advanced access control to support rising enterprise workloads. Investors prioritize secure facilities to reduce risks linked to rapid cloud growth. AI-driven surveillance tools help teams detect threats faster across large campuses. Edge facilities adopt integrated monitoring to improve incident response in remote areas. Automation improves physical security planning for multi-site deployments. Regional upgrades lift expectations for compliance-driven operations. The shift drives confidence among global cloud providers. Businesses view the market as a critical layer for operational resilience.

- For example, Teraco’s parent company, Digital Realty, operates carrier-neutral data centers across Africa that follow global security standards, including strict access controls, 24/7 monitoring, and audited procedures aligned with ISO/IEC 27001. In East Africa, Africa Data Centres (ADC) reinforces security through controlled entry systems, surveillance coverage, and compliance with international data-center protection frameworks. These measures ensure secure environments for cloud, telecom, and enterprise workloads.

Adoption of Intelligent Surveillance and Biometric Systems for Risk Prevention

Demand rises for smart surveillance systems that manage real-time threats across growing data centers. AI-powered analytics support security staff with quick decision-making and event classification. Biometrics replace legacy systems to reduce unauthorized access and identity misuse. Operators integrate thermal imaging to track irregular activities near secure zones. Automated alerts lead to faster prevention of perimeter breaches. Remote security dashboards allow unified oversight for dispersed facilities. Investors recognize the Africa Data Center Physical Security Market as a backbone for safe digital expansion. It supports stronger uptime targets for large enterprises. The shift encourages long-term modernization across major regions.

- For example, The Nigerian government has used biometric enrollment systems to verify identities across major national programs, including the National Identity Management Commission (NIMC), which has registered over 100 million Nigerians using fingerprint and facial recognition technologies. These platforms strengthen identity accuracy and reduce fraud across government services.

Shift Toward Compliance-Driven Security Design and Standardized Operations

Regulated industries demand robust physical controls to support data protection rules. Operators implement structured zoning to restrict movement inside sensitive halls. Data centers streamline audits with centralized access logs and automated reporting engines. National cybersecurity policies push providers to upgrade surveillance frameworks. Companies adopt unified control rooms to manage access points and equipment rooms. Investors support these upgrades to maintain international compliance benchmarks. The Africa Data Center Physical Security Market gains traction through tighter regulatory focus. It accelerates security standardization across new and existing facilities. Enterprises value predictable audit performance for regional operations.

Expansion of Cloud, Colocation, and Edge Deployments Driving Wider Security Needs

Cloud platforms build more colocation sites, creating gaps that demand advanced security solutions. Operators add multi-layer barriers to support hyperscale-style protection in urban regions. Edge sites need compact physical systems that manage power events, intrusion, and environmental risks. AI-driven monitoring increases visibility over remote halls with limited staff. Energy-efficient cameras help reduce operational overhead in hotter climates. Integration with building management systems improves resilience against on-site disruptions. The Africa Data Center Physical Security Market benefits from rising diversification of facility types. It supports long-term capacity planning across enterprises. Investors value the region as a strong growth corridor.

Market Trends

Market Trends

Rise of Smart Perimeter Technologies and AI-Controlled Access Systems

New perimeter tools integrate AI models to detect route deviations, unusual motion, and tampering. Many operators deploy radar-based units to monitor exterior spaces in low-visibility areas. Smart fences support real-time intrusion alerts with fewer false positives. Cloud-linked access systems help manage identity permissions faster. Facial recognition tools enhance authentication in high-traffic colocation sites. Energy-efficient sensors reduce load on power systems during peak hours. The Africa Data Center Physical Security Market gains depth through these innovations. It guides next-generation facility design across major regions. Users adopt these tools to protect growing high-value digital assets.

Integration of Physical Security with Cyber Monitoring Platforms

Operators merge physical data streams with cybersecurity dashboards for unified threat oversight. Automated workflows help teams respond quickly to badge misuse or irregular login attempts. Integrated logs support forensics during breach investigations. Hybrid control rooms gain traction among hyperscale and telecom operators. Access and network anomalies trigger coordinated alerts to prevent internal threats. AI analytics track data patterns that reveal external risks near facility grounds. The Africa Data Center Physical Security Market benefits from this convergence. It helps enterprises maintain secure digital ecosystems. The trend supports long-term resilience across public and private sectors.

Adoption of Green and Energy-Efficient Security Hardware

Facility leaders seek low-power cameras to reduce operational overhead. LED-based perimeter lights replace older systems, lifting energy efficiency across large campuses. Solar-powered sensors grow in remote areas with limited grid reliability. Smart HVAC-linked controls reduce heat buildup around sensitive equipment. Operators deploy sustainable materials in door frames and racks to meet green mandates. Energy ratings influence procurement decisions for new projects. The Africa Data Center Physical Security Market aligns with green data center goals. It supports sustainability-driven planning frameworks. Global entrants prefer regions showing strong environmental compliance progress.

Growth of Modular and Scalable Security Architectures for Multi-Site Expansion

Modular components help operators scale security layers faster during phased expansion. Compact badge units support multi-door authentication in small sites. Smart cabinets add high-security locking tools for colocation customers. Modular sensor kits reduce deployment delays across remote areas. Pre-integrated software packages simplify setup for cross-border projects. Multi-site dashboards consolidate access records for better audit control. The Africa Data Center Physical Security Market uses modularity to strengthen long-term adoption. It supports fast growth across secondary hubs. The trend encourages flexible investment strategies for global and local operators.

Market Challenges

Market Challenges

Infrastructure Gaps and Limited Skilled Workforce Across Key African Regions

Many facilities face delays due to inconsistent power reliability and aging infrastructure. Remote regions struggle with stable connectivity required for advanced monitoring tools. Operators depend heavily on imported equipment with long lead times. Limited skilled workforce slows deployment of high-grade security systems. Training gaps weaken incident response capabilities during peak load periods. Rising operational demands strain small teams handling multi-site surveillance. Investors assess these gaps before initiating regional expansion. The Africa Data Center Physical Security Market balances these challenges with stepwise upgrades. It continues to adjust to regional capability differences across major countries.

High Upfront Costs and Variable Regulatory Enforcement Slowing Adoption

Advanced physical systems require significant investment in sensors, biometrics, and AI platforms. Small operators face budget constraints that delay modernization efforts. Regulatory enforcement varies, creating uneven compliance expectations across regions. This inconsistency leads to slower adoption of strict access control rules. Some markets lack clear guidelines for data hall zoning and audit trails. Providers must align internal standards with global benchmarks to avoid compliance risks. Cost pressures influence procurement choices in developing economies. The Africa Data Center Physical Security Market faces adoption hurdles in price-sensitive regions. It still retains strong growth potential across major industry clusters.

Market Opportunities

Growing Hyperscale and Cloud Expansion Unlocking Security Modernization

Hyperscale providers expand footprints, creating new opportunities for advanced security tools. Operators adopt integrated control rooms to handle complex access environments. AI-driven surveillance attracts major global partners seeking safer cloud ecosystems. Scalable authentication systems support new edge and colocation builds. Investors explore opportunities across emerging technology parks and digital corridors. Demand for resilient infrastructure encourages faster deployment of modern security layers. The Africa Data Center Physical Security Market benefits from wider cloud penetration. It drives long-term modernization across new and existing hubs. Many enterprises seek enhanced security to support digital transformation projects.

Rising Digital Policies and Public-Sector Investments Supporting Security Upgrades

Governments promote stronger cybersecurity frameworks that link directly to physical security mandates. Public-sector projects prioritize integrated access systems to reduce breach risks. National cloud strategies encourage higher security standards across data halls. Telecom-led expansions open new markets for surveillance and perimeter technology vendors. International investors support compliant designs for cross-border data flow. Local integrators gain momentum through policy-driven demand. The Africa Data Center Physical Security Market gains new growth pathways through these shifts. It encourages broader deployment of modern tools across regulated sectors. Stronger policies reinforce long-term investment confidence.

Market Segmentation

Market Segmentation

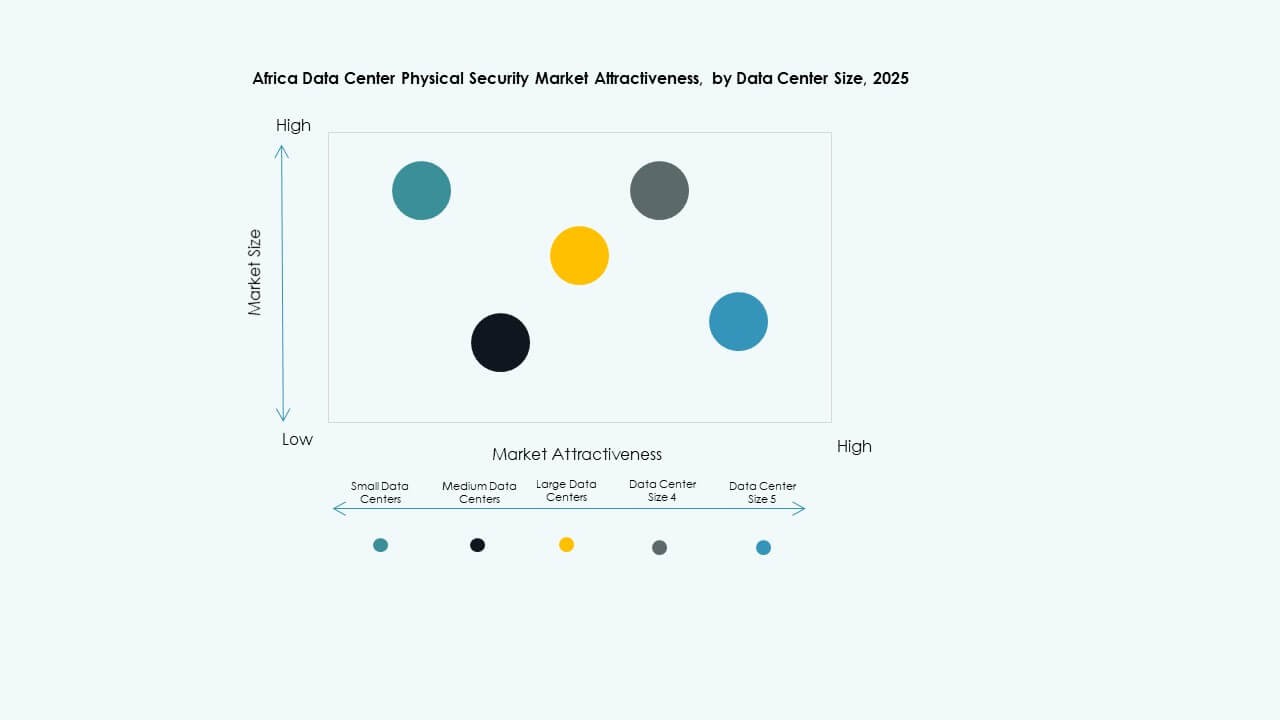

By Data Center Size

Small data centers grow steadily due to rising regional digital services. Medium data centers dominate with higher deployment of structured access and monitoring frameworks. Large data centers expand fastest as global cloud firms invest across Africa. The Africa Data Center Physical Security Market supports all three tiers with scalable solutions. Medium sites hold the highest share due to widespread enterprise adoption. Large facilities require advanced surveillance for multi-hall operations. Regional clusters influence size-based demand patterns. Smaller sites adopt compact biometric tools for cost efficiency. Each tier benefits from improved integration capabilities.

By Component

Solutions dominate due to strong demand for access control, surveillance, and monitoring platforms. Services grow as operators seek integration, consulting, and lifecycle support. The Africa Data Center Physical Security Market relies on mixed offerings to maintain operational continuity. Solution providers lead adoption in urban hubs with dense enterprise activity. Service firms manage complex rollouts across cross-border deployments. Strong focus on uptime drives demand for integrated service frameworks. Global vendors influence solution quality benchmarks. Local partners support long-term maintenance cycles. The component mix ensures balanced market expansion.

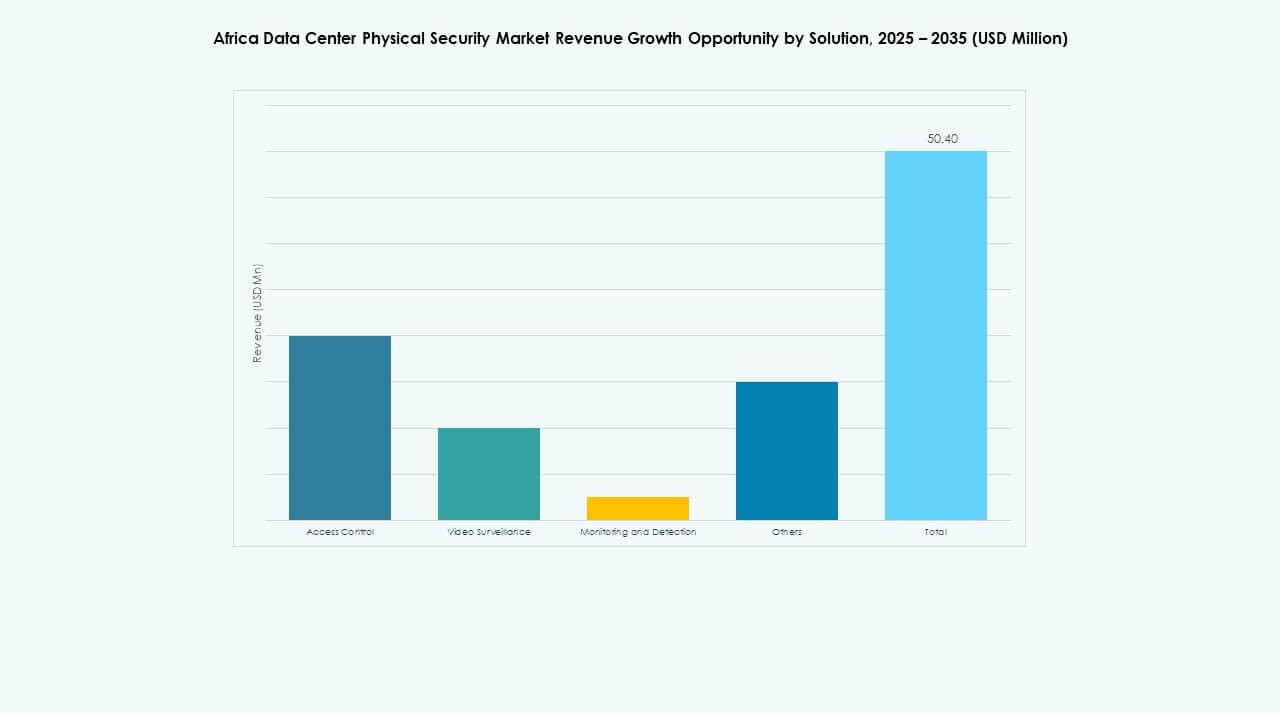

By Solution

Access control tools lead due to rising compliance needs and identity protection demands. Video surveillance grows with adoption of AI analytics. Monitoring and detection systems expand as operators track environmental and intrusion risks. Other solutions support specialized needs across hyperscale and edge facilities. The Africa Data Center Physical Security Market benefits from strong access and surveillance uptake. Operators prioritize hybrid solutions for multi-layer environments. Growth accelerates through enhanced automation across data halls. AI-supported features shape next-generation procurement choices. Facilities adopt continuous monitoring to protect critical loads.

By Services

Consulting services help operators understand compliance needs and design strong security frameworks. System integration gains traction with new deployments across major hubs. Maintenance and support grow due to lifecycle requirements and equipment complexity. The Africa Data Center Physical Security Market uses service expertise to enhance operational performance. Integration services dominate due to rapid project expansions. Consulting supports early design choices for zones and access routes. Maintenance ensures long-term reliability for multi-device networks. Service-led adoption grows across regulated industries. Providers support resilience strategies for broad facility types.

By Security Layer

Perimeter security holds strong share due to high focus on external threat control. Building access systems manage movement across shared and sensitive areas. Data hall protection expands with stricter zoning policies. Rack and cabinet layers gain traction with colocation customers. Other layers support custom site needs across diverse regions. The Africa Data Center Physical Security Market strengthens all layers through unified solutions. Perimeter tools lead deployments in large campuses. Hall and rack layers grow through cloud-driven demand. Multi-layer architecture ensures controlled access across expansions. Operators value depth across all zones.

By Data Center Type

Hyperscale facilities lead adoption with advanced biometric and AI-driven systems. Colocation centers grow as enterprise demand rises. Edge sites need compact tools for remote monitoring. Enterprise sites maintain steady upgrades to meet internal policies. Other formats support sector-specific functions. The Africa Data Center Physical Security Market gains traction across all types with scalable designs. Hyperscale drives the highest adoption intensity. Colocation attracts diverse customers requiring strict controls. Edge sites shape innovation for lightweight security. Enterprises prioritize resilience for long-term operations.

By End-User

BFSI leads adoption due to strict regulatory and audit expectations. Government and defense projects expand with stronger security mandates. IT and telecom drive high-volume demand through rapid cloud growth. Healthcare increases adoption due to sensitive data requirements. Retail, manufacturing, and other sectors display steady growth. The Africa Data Center Physical Security Market aligns solutions with each sector’s risk profile. BFSI maintains top share due to compliance-heavy needs. Government projects influence regional policy direction. Telecom ensures high-speed expansion in urban hubs. Each sector shapes demand through industry-specific priorities.

Regional Insights

Regional Insights

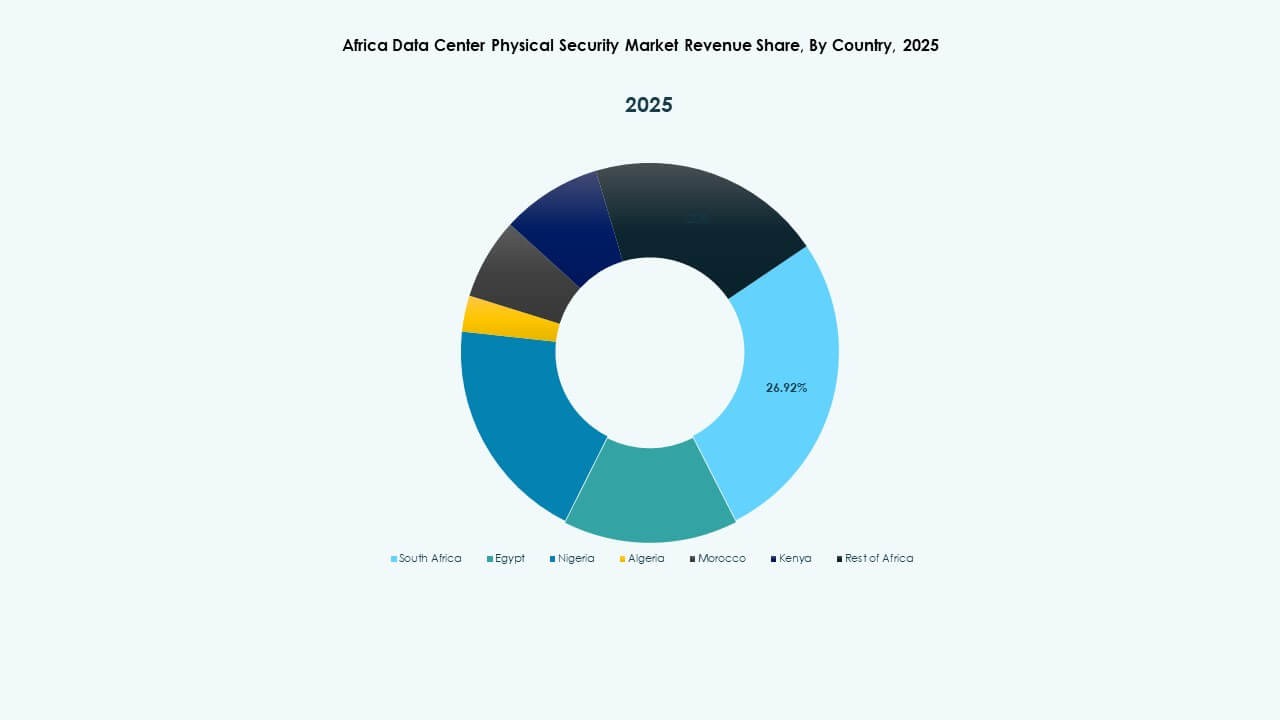

North Africa

North Africa holds around 25% regional share driven by enterprise growth and public-sector digitization. Countries like Egypt and Morocco lead through rising cloud adoption. The Africa Data Center Physical Security Market supports this growth with advanced access systems. Operators invest in AI-enabled surveillance to secure expanding hubs. Cross-border connectivity improves strategic positioning of regional campuses. Compliance-focused sectors lift demand for multi-layer controls. The region maintains steady momentum through ongoing infrastructure development.

East Africa

East Africa secures about 20% regional share due to investments in Kenya, Rwanda, and Ethiopia. Colocation growth pushes demand for scalable security layers. The Africa Data Center Physical Security Market aligns with the region’s push for digital services. Operators adopt unified control rooms to manage distributed facilities. Telecom expansions support construction of new edge hubs. Governments increase focus on data protection frameworks. Regional stability supports long-term investments in secure infrastructure.

- For example, Safaricom received the ISO 27701 Privacy Information Management System certification in 2024, confirming its compliance with global standards for privacy governance. The certification covers Safaricom’s data-handling and processing practices across its digital platforms and operational systems. It demonstrates the company’s commitment to strengthened privacy controls and audited information-management processes.

West & Southern Africa

West and Southern Africa hold the largest combined share of roughly 55% driven by Nigeria and South Africa. Strong enterprise activity influences adoption of advanced access, surveillance, and detection tools. The Africa Data Center Physical Security Market expands through strong cloud and telecom presence. Operators invest in multi-layer security to support high-volume workloads. Cross-industry digitization fuels demand for modernized infrastructure. Investors view these regions as high-opportunity clusters. New development zones strengthen long-term growth potential.

- For example, MTN Group operates Tier III–certified data centers across Africa, including facilities in South Africa designed to support cloud, fintech, and telecom workloads. The company adheres to international standards such as ISO/IEC 27001 for information security management. MTN’s data-center investments emphasize controlled access, environmental monitoring, and audited security processes aligned with global compliance requirements.

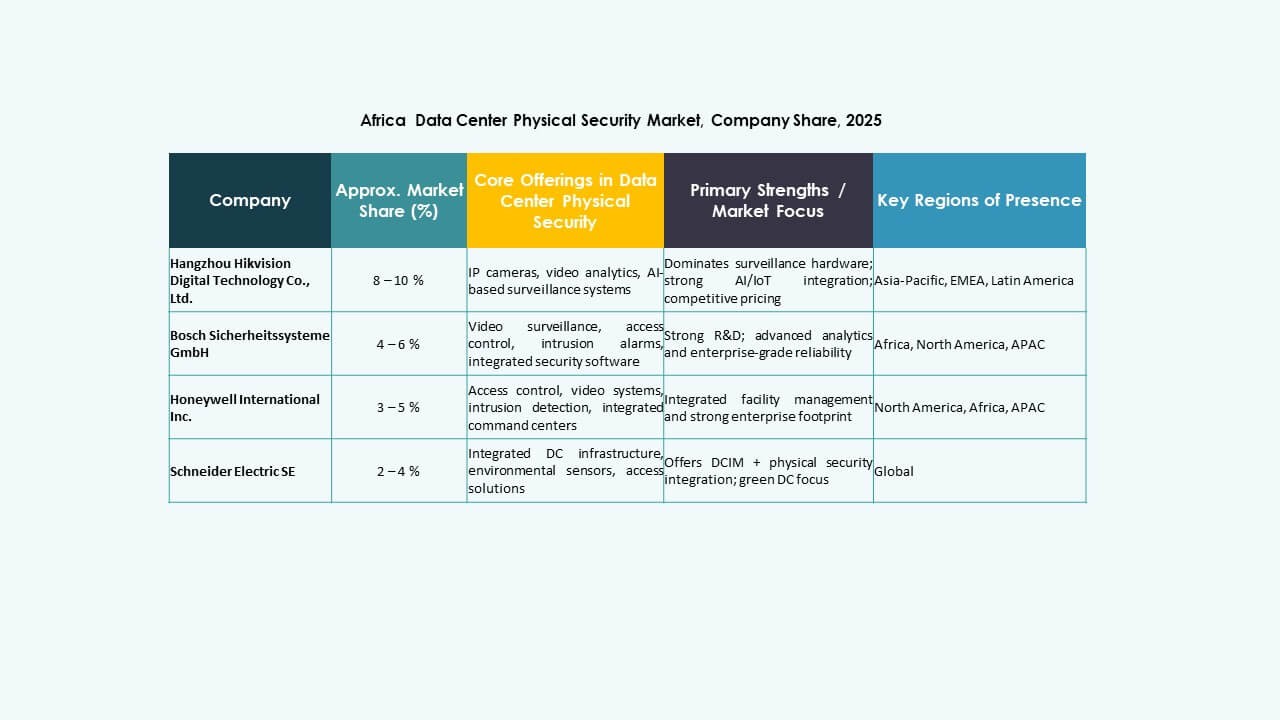

Competitive Insights:

Competitive Insights:

- Bosch Sicherheitssysteme GmbH

- Honeywell International Inc.

- Axis Communications AB

- Schneider Electric SE

- ABB Ltd

- Siemens AG

- Cisco Systems, Inc.

- Genetec Inc.

- Dahua Technology Co., Ltd.

- Hanwha Vision Co., Ltd.

The competitive landscape in the Africa Data Center Physical Security Market features global OEMs, regional integrators, and cybersecurity-aligned vendors competing for multi-layer deployments. Many providers focus on integrated access control and AI-powered surveillance to support modern facilities. Global brands strengthen their presence through reseller networks and large project partnerships. Regional system integrators secure traction by offering customization for local compliance needs. Vendors expand portfolios to link cyber and physical monitoring platforms, creating unified command capabilities. The market grows more competitive as hyperscale and colocation projects demand advanced authentication, thermal imaging, and scalable detection tools. It relies on innovation, service quality, and long-term lifecycle support to differentiate strong players.

Recent Developments:

- In October 2025, ASSA ABLOY acquired Kentix GmbH, a German company specializing in monitoring and access control products designed for data centers, enhancing their capabilities in physical security for this sector.

- In January 2025, ASSA ABLOY also acquired InVue, a Charlotte-based provider of asset protection and access control solutions, aligning with their strategy to expand globally in access control and asset protection.

- In June 2024, Honeywell International Inc. completed the acquisition of Carrier Global Corporation’s Global Access Solutions business for $4.95 billion, enhancing its building automation portfolio with advanced access control solutions like LenelS2, Onity, and Supra, which support security needs in data centers including those in Spain.

- In December 2024, Bosch Sicherheitssysteme GmbH sold its security and communications technology product business to the European investment firm Triton. The transaction included three business units Video, Access and Intrusion, and Communication as Bosch aims to focus more on systems integration business.