Executive summary:

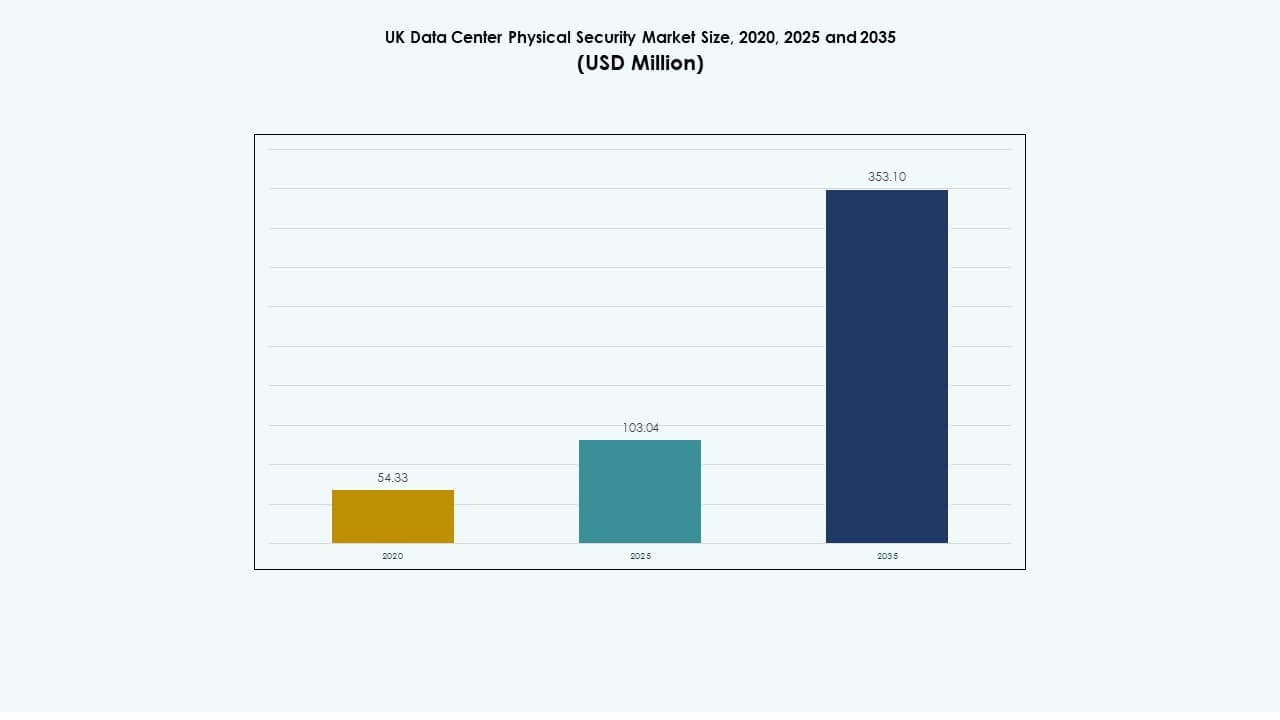

The UK Data Center Physical Security Market size was valued at USD 54.33 million in 2020, increased to USD 103.04 million in 2025, and is anticipated to reach USD 353.10 million by 2035, at a CAGR of 13.04% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2035 |

| UK Data Center Physical Security Market Size 2025 |

USD 103.04 Million |

| UK Data Center Physical Security Market, CAGR |

13.04% |

| UK Data Center Physical Security Market Size 2035 |

USD 353.10 Million |

Growing digital transformation, AI integration, and IoT-enabled protection systems strengthen the need for multi-layer security in data centers. Enterprises adopt biometric authentication, video analytics, and automated perimeter defense to reduce intrusion risks. Innovation in predictive monitoring enhances operational control, helping operators maintain uptime and compliance. The market gains strategic importance as investors prioritize resilient infrastructure that safeguards expanding cloud and colocation ecosystems.

London and South East England lead the UK Data Center Physical Security Market due to the concentration of hyperscale and colocation hubs. The Midlands and Northern England follow with new infrastructure supported by favorable land and energy costs. Scotland and Wales emerge as secondary growth zones driven by renewable energy access and regional data expansion. This geographic spread reflects strong investment in nationwide digital security infrastructure.

Market Drivers

Rising Emphasis on Integrated Multi-Layer Security Architecture for Critical Data Hubs

The UK Data Center Physical Security Market gains strength from the adoption of integrated security frameworks combining biometric access, advanced analytics, and AI-driven surveillance. Operators implement multi-factor authentication and smart card systems to restrict unauthorized access. Growing digital transformation across BFSI and government sectors drives investment in physical perimeter protection. AI-powered analytics reduce manual supervision errors and improve incident response. The market reflects a shift toward proactive defense strategies that mitigate breach risks. High-value data centers adopt unified command platforms integrating video, intrusion, and environmental controls. It enhances situational awareness and operational consistency across sites. Businesses recognize such investments as essential for regulatory compliance and service assurance.

- For example, Avigilon’s Alta cloud-based Video Management System (VMS) provides AI-powered video analytics that enable real-time detection of security events across multiple sites. The platform eliminates the need for on-site servers by using secure cloud infrastructure, supporting organizations that require scalable and intelligent physical security management.

Adoption of AI-Driven Threat Detection and Predictive Monitoring

Rapid innovation in AI-enabled monitoring tools transforms site security operations. Modern facilities deploy machine-learning algorithms that identify behavioral anomalies before physical intrusion occurs. Biometric systems integrate with predictive analytics to provide early alerts and real-time data insights. This shift improves response speed and reduces false alarms in complex networked environments. The UK Data Center Physical Security Market benefits from automation that improves uptime and efficiency. Enterprises allocate higher budgets for automated consoles that support 24/7 control room operations. Smart sensors and IoT-linked barriers form the foundation of modern defense layers. It allows operators to achieve higher protection levels without adding manual workload. The strategic appeal lies in scalability and reduced total ownership costs.

Growing Influence of Regulatory Frameworks and Data Compliance Mandates

Government-backed standards and cybersecurity frameworks shape procurement priorities for data center operators. Firms must comply with ISO 27001, GDPR, and the UK’s National Cyber Security Centre directives. This compliance focus accelerates spending on physical security that complements digital safeguards. Cloud providers and colocation firms deploy certified access and video solutions to ensure audit readiness. The UK Data Center Physical Security Market aligns with public safety goals that encourage secure digital growth. Investors view this alignment as a key stability factor. Demand grows for vendors offering compliance-driven, modular systems that adapt to audit cycles. It boosts trust and strengthens vendor relationships across critical infrastructure sectors. Compliance-linked capital allocation has become a long-term strategic differentiator.

Rising Role of Private Equity and Institutional Investors in Infrastructure Security

Institutional investors channel funds into advanced security upgrades to future-proof digital estates. Strategic investments target hyperscale expansions and Tier IV facilities with automation-first defense systems. These projects emphasize operational continuity and risk avoidance. The UK Data Center Physical Security Market attracts sustained interest due to its predictable growth and compliance-backed resilience. Firms focus on end-to-end resilience, from physical entry points to rack-level surveillance. This capital influx accelerates standardization of intelligent monitoring across networks. Infrastructure operators integrate access control with remote management dashboards for scalability. It transforms data centers into secure, asset-backed investments. Long-term investors recognize these facilities as reliable income sources supported by digital expansion and compliance momentum.

- For example, Equinix’s LD-series data centers in London feature multi-layer physical security, including biometric access controls, mantrap entry systems, and 24/7 on-site security monitoring. These facilities maintain high compliance standards and support mission-critical operations for enterprises requiring secure, interconnected infrastructure.

Market Trends

Shift Toward Touchless and Biometric-Integrated Access Control Solutions

Demand grows for frictionless entry systems using facial recognition, iris scans, and digital key credentials. Operators seek hygiene-friendly and faster identification solutions following remote work and automation adoption. Biometric access ensures consistent identity validation across restricted areas. The UK Data Center Physical Security Market embraces these upgrades to optimize flow management. Integration with centralized dashboards improves audit precision and entry record retention. Enterprises integrate mobile credentialing for faster workforce mobility within multi-tenant data centers. Growing vendor innovation in secure algorithmic recognition supports privacy compliance. It improves physical site agility while minimizing operational risk. Touchless authentication reshapes how large facilities manage security efficiency.

Expansion of AI-Enabled Video Surveillance and Cloud-Based Monitoring Systems

Cloud migration drives the use of centralized AI-enhanced video analytics to manage multiple sites remotely. Security operators apply visual intelligence to detect anomalies such as motion patterns or perimeter breaches. The UK Data Center Physical Security Market sees growing adoption of smart surveillance that integrates edge computing. Remote dashboards enable predictive alerts, optimizing resource use and reducing downtime. Vendors enhance platforms with 360-degree thermal imaging for round-the-clock visibility. Organizations deploy redundant video feeds across multiple layers to ensure fail-safe monitoring. It supports proactive threat detection and facility resilience. Edge and cloud video platforms deliver scalable data security while simplifying compliance. Continuous visual oversight builds client confidence in managed infrastructure.

Integration of IoT and Smart Sensor Networks Across Security Ecosystems

IoT-based devices transform static systems into responsive protection networks. Smart sensors track temperature, vibration, and motion within secured halls. These real-time indicators trigger alerts for irregular activity or environmental changes. The UK Data Center Physical Security Market leverages sensor analytics to automate detection processes. It reduces response latency and optimizes staff coordination during incidents. Integration with centralized platforms enhances transparency across large data estates. Facilities use low-power networks to connect thousands of endpoints securely. This interconnected design lowers operational costs and strengthens resilience against intrusion. The evolution of IoT-based control systems makes adaptive security more achievable across distributed architectures.

Growing Popularity of Modular and Scalable Physical Security Infrastructure

Operators prefer modular setups to match phased data center expansions. Security vendors now design flexible configurations that adapt to capacity growth or site replication. The UK Data Center Physical Security Market experiences higher demand for plug-and-play components. Quick-deploy surveillance and access systems support time-sensitive colocation builds. Modular systems also simplify compliance upgrades during re-certification phases. This design flexibility minimizes capital waste and future retrofitting. Vendors promote pre-tested, standards-compliant frameworks that integrate easily with existing IT environments. It allows hyperscale and enterprise operators to expand coverage without disrupting uptime. Such scalability has become a key procurement factor across major data center developments.

Market Challenges

High Capital Expenditure and Integration Complexity for Legacy Sites

Modernization of legacy data centers remains capital-intensive and technically complex. Operators face high costs when upgrading traditional infrastructure to meet modern standards. Integration of biometric access, video analytics, and AI monitoring often demands system re-engineering. The UK Data Center Physical Security Market faces hurdles in aligning old hardware with cloud-native platforms. Many mid-sized facilities still rely on analog surveillance and fragmented access systems. This misalignment reduces overall efficiency and operational transparency. Cost constraints delay adoption across smaller enterprises with tight budgets. Vendors must provide cost-efficient retrofitting solutions to maintain competitiveness. Balancing modernization with continuity becomes a key operational challenge across maturing facilities.

Shortage of Skilled Personnel and Cyber-Physical Convergence Risks

Security operations require skilled technicians familiar with both physical and digital systems. Limited workforce availability slows the adoption of advanced integrated controls. The UK Data Center Physical Security Market faces dual challenges from cyber-physical convergence. Complex platforms that merge digital access and facility management demand multi-domain expertise. Human error and inconsistent procedures increase exposure risk during transitions. Training gaps make remote management setups harder to sustain securely. Organizations must invest in workforce upskilling to ensure reliable operations. Automation helps reduce dependency, but oversight remains critical. Industry collaboration in certification programs could bridge the skill divide effectively.

Market Opportunities

Emergence of Edge and Modular Data Centers Creating New Security Demand

Edge deployments across the UK increase demand for compact and resilient security systems. The UK Data Center Physical Security Market benefits from this decentralization trend. Compact sensors and mobile-controlled systems fit smaller facilities needing enterprise-grade protection. Vendors offering adaptive systems gain traction among regional operators. The shift supports flexible, energy-efficient, and compliant infrastructure expansion. It creates avenues for managed service providers to deliver subscription-based physical protection. Future investments will focus on scalable models that balance cost and control flexibility. The rise of edge networks fuels demand for lightweight access and remote defense frameworks.

Growing Use of AI and Robotics for Automated Threat Response

AI integration continues to improve response speed and security accuracy across large sites. Robots equipped with cameras and sensors patrol perimeters autonomously. The UK Data Center Physical Security Market aligns with these shifts by embedding robotics into daily operations. This automation reduces labor dependency and supports continuous monitoring. Vendors explore hybrid models combining human oversight with AI analytics. Early adopters gain efficiency and lower operational expenditure. It transforms facility security from reactive to predictive. The ongoing evolution ensures stronger resilience against physical breaches.

Market Segmentation

By Data Center Size

Large data centers dominate the UK Data Center Physical Security Market due to higher asset concentration and complex infrastructure. These facilities demand advanced monitoring and multi-layer access systems. Medium data centers experience steady adoption supported by modular technology integration. Small data centers remain limited to basic access control setups due to budget constraints. Large facilities lead due to hyperscale growth and enterprise colocation expansion. Demand aligns with sustainability standards and uptime assurance. Future focus remains on scalable protection solutions across all facility sizes.

By Component

Solutions hold the majority share, driven by hardware and software integration within critical infrastructure. Vendors deliver unified command platforms linking sensors, alarms, and access systems. Services gain momentum through consulting and ongoing maintenance contracts. The UK Data Center Physical Security Market benefits from higher solution sales as operators upgrade facility systems. Demand for service-based contracts rises with system complexity. Managed service models grow due to outsourcing preferences among small operators. Overall, the component mix favors hardware-driven modernization combined with lifecycle service support.

By Solution

Access control dominates due to growing preference for biometric and mobile-enabled authentication. Video surveillance expands rapidly with AI-based analytics and thermal monitoring. Monitoring and detection systems support continuous oversight and environmental analysis. The UK Data Center Physical Security Market records balanced growth across all categories. Access systems remain critical due to high audit and compliance demand. Vendors integrate multiple modules for cohesive performance. Future development centers on interoperability between access, video, and monitoring tools.

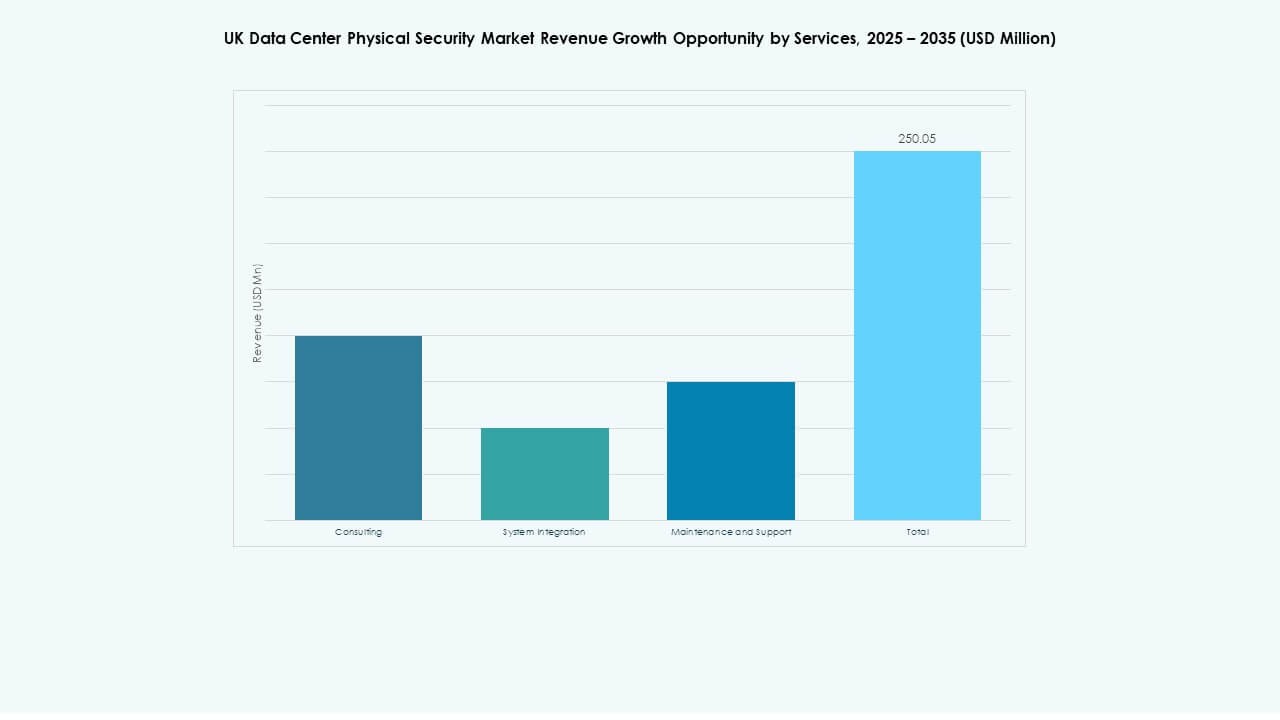

By Services

System integration leads due to rising need for end-to-end solutions linking legacy and modern systems. Consulting services guide compliance readiness and design frameworks. Maintenance and support ensure equipment reliability and software continuity. The UK Data Center Physical Security Market reflects service growth through recurring contracts. Clients seek full-service vendors managing infrastructure updates and audits. Integration services gain preference due to complex technology environments. Service diversity supports consistent uptime and long-term reliability.

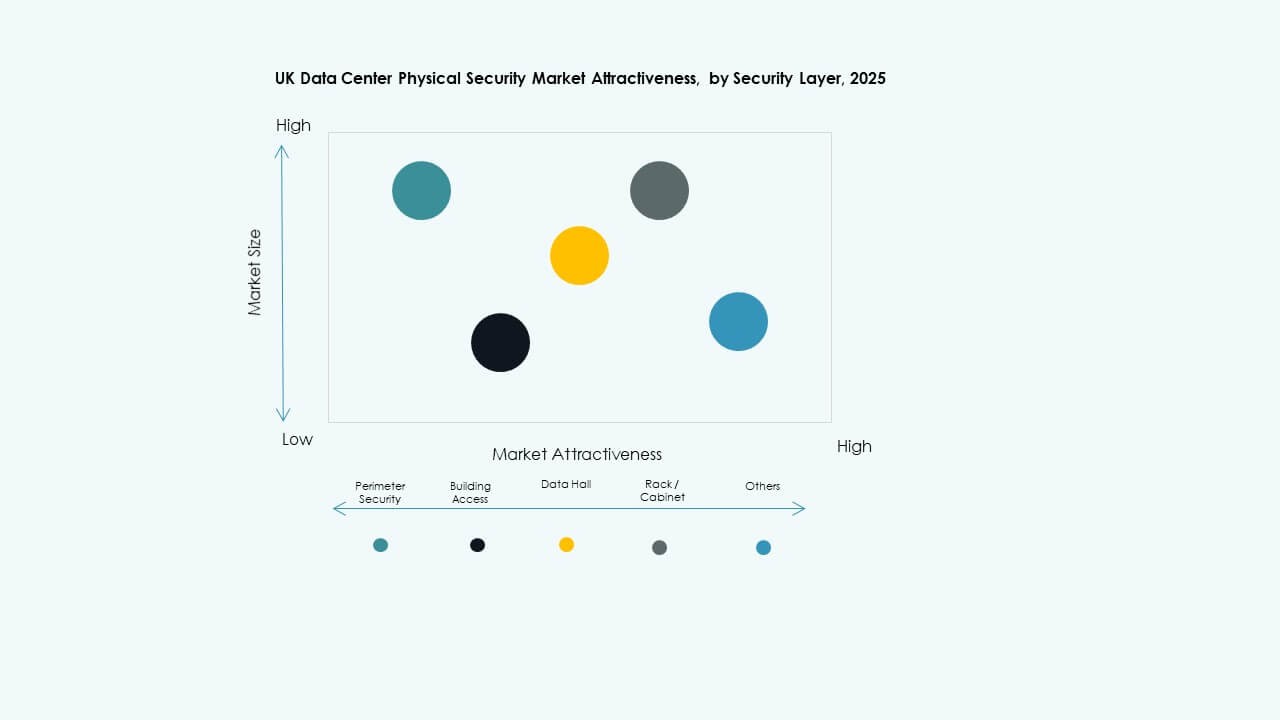

By Security Layer

Perimeter security holds the largest share with rising emphasis on early intrusion detection. Building access and data hall layers follow due to internal security prioritization. Rack-level surveillance gains traction with cabinet-level monitoring in hyperscale environments. The UK Data Center Physical Security Market benefits from multi-layer coverage that minimizes exposure. Vendors introduce layered protection stacks combining analytics and sensors. Growing regulatory pressure pushes deeper integration across all levels. Layered defense remains a core investment principle.

By Data Center Type

Hyperscale facilities dominate due to large capacity and regulatory scrutiny. Colocation centers record fast adoption of smart security for multi-tenant operations. Enterprise and edge centers display modular adoption patterns. The UK Data Center Physical Security Market aligns with evolving digital infrastructure needs. Hyperscale demand drives adoption of AI-driven control and predictive defense. Colocation operators focus on client-specific compliance frameworks. Each data center type contributes to market diversification and resilience.

By End-User

IT and telecom remain dominant due to high digital workloads and strict compliance standards. BFSI and government sectors maintain strong security budgets. Healthcare and retail accelerate adoption for data integrity and customer safety. The UK Data Center Physical Security Market sees balanced participation across end-users. Manufacturing and ecommerce embrace automation for supply chain continuity. Cross-sector investment builds strong demand for AI-driven monitoring. End-user diversity drives continuous technology enhancement.

Regional Insights

London and South East England Leading the Market with Over 45% Share

London remains the core data center hub due to dense enterprise clusters and network proximity. South East England supports major colocation and hyperscale projects. The UK Data Center Physical Security Market sees over 45% share from this corridor. High investments from AWS, Google, and Equinix drive advanced security deployment. Facilities here integrate biometric access and AI monitoring systems extensively. Robust energy supply and fiber density sustain continued expansion. Strategic focus on compliance and uptime keeps this subregion at the forefront.

- For example, Equinix LD9, located at Powergate Business Park in London, spans approximately 283,575 sq ft with 107,639 sq ft of raised floor colocation space and a 21 MW power capacity. The facility features biometric access controls, 24/7 on-site security, and CCTV surveillance, complying with ISO 27001 and PCI DSS standards while hosting major cloud providers such as AWS, Microsoft Azure, and Google Cloud.

The Midlands and Northern England Exhibiting Expanding Data Infrastructure Base (Around 30%)

Midlands and Northern England show strong momentum with new hyperscale and enterprise facilities. Lower real estate and power costs attract developers to Leeds, Manchester, and Birmingham. The UK Data Center Physical Security Market benefits from spreading demand outside London. Operators deploy modular designs with scalable security solutions to support new builds. AI-based perimeter systems reduce staffing needs and ensure rapid detection. Investment in regional grids and renewable integration enhances site resilience. Local policy support accelerates expansion across secondary hubs.

Scotland, Wales, and Northern Ireland Emerging as Growth-Oriented Regions (About 25%)

Scotland leads the emerging segment with renewable-powered data infrastructure projects. Wales and Northern Ireland follow through public-private partnerships enhancing connectivity. The UK Data Center Physical Security Market witnesses gradual adoption of advanced systems in these regions. Smaller-scale facilities integrate edge security solutions tailored to rural connectivity. Energy-efficient builds align with sustainability mandates. Strategic incentives attract investors exploring decentralized cloud zones. These regions represent the next frontier for secure and efficient data infrastructure deployment.

- For example, Scotland has become a growing hub for renewable-energy-powered data centers, supported by government incentives promoting sustainable digital infrastructure. Several facilities in regions such as Edinburgh and Inverness utilize low-carbon energy and adopt advanced environmental and security standards to improve efficiency and resilience. These projects align with Scotland’s national sustainability and data localization goals.

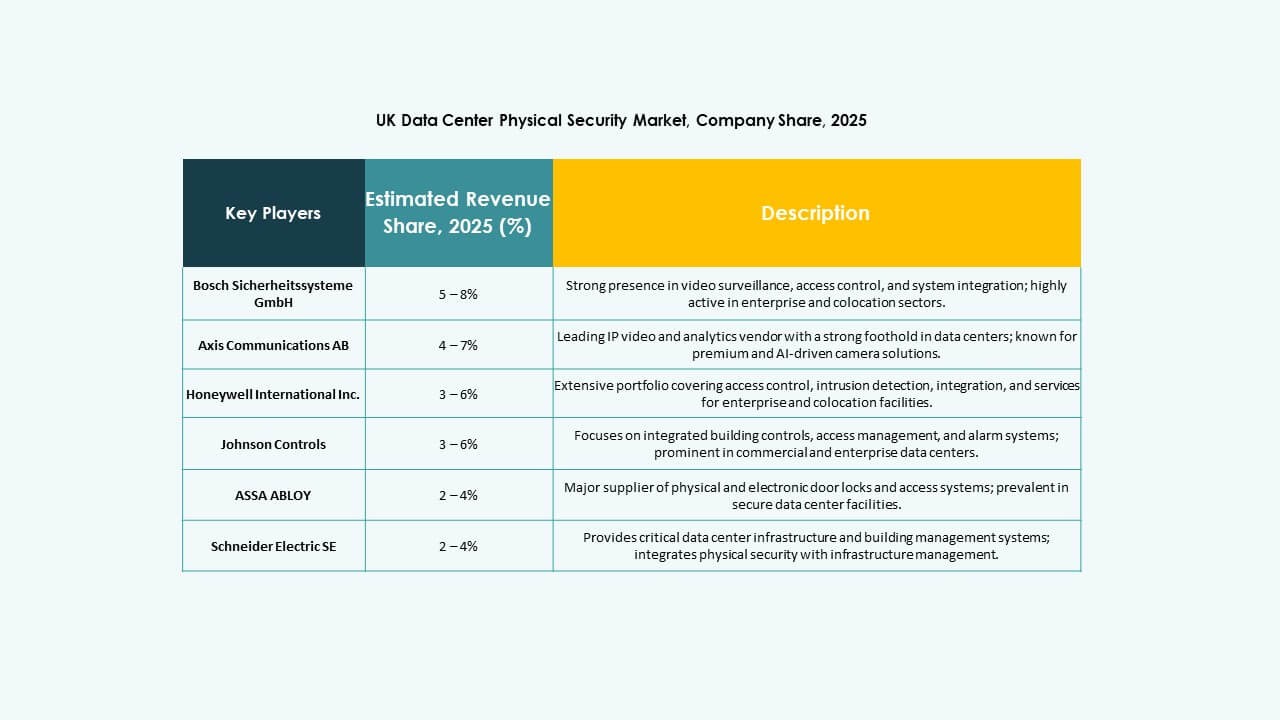

Competitive Insights:

- Bosch Sicherheitssysteme GmbH

- Securitas AB

- Axis Communications AB

- Honeywell International Inc.

- Johnson Controls

- Schneider Electric SE

- ABB Ltd

- Siemens AG

- Cisco Systems, Inc.

- Genetec

- Fortinet

- Palo Alto Networks

- Dahua Technology Co. Ltd.

- Hanwha Vision Co. Ltd.

- Secom Co. Ltd.

The UK Data Center Physical Security Market features strong competition among established global and regional players offering integrated safety solutions. It focuses on comprehensive systems that merge access control, video surveillance, and intrusion detection under centralized management. Leading firms expand through mergers, advanced analytics integration, and AI-enabled monitoring solutions. Vendors emphasize modular designs and compliance-based frameworks to attract hyperscale and colocation operators. Partnerships between technology developers and managed service providers drive faster market penetration. The competition favors companies capable of delivering scalable, energy-efficient, and interoperable systems. Product differentiation depends on reliability, cybersecurity alignment, and support service depth. Continuous innovation in automation and real-time intelligence defines leadership within this evolving security ecosystem.

Recent Developments:

- In June 2025, Vantage Data Centers secured EUR 720 million through Europe’s inaugural data-center asset-backed securitization to refinance four sites in Germany, underscoring rising investments in secure physical infrastructure within the Europe data center physical security market.

- In December 2024, Bosch Sicherheitssysteme GmbH sold its security and communications technology product business to the European investment firm Triton. The transaction included three business units Video, Access and Intrusion, and Communication as Bosch aims to focus more on systems integration business.

- In February 2024, Axis Communications AB confirmed that more than 200 of its network products, including cameras, intercoms, and audio devices, now support the IEEE 802.1AE (MACsec) security standard. This enhancement strengthens data integrity and device authentication at the Ethernet layer, reducing the risk of unauthorized access. The update underscores Axis Communications’ commitment to advancing secure networked physical security solutions for data-intensive environments such as data centers.