Executive summary:

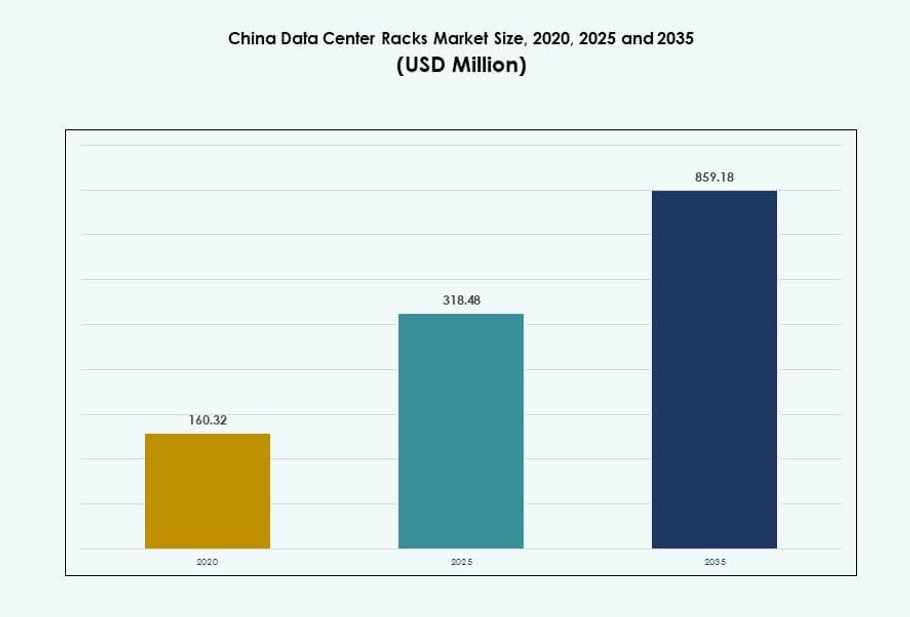

The China Data Center Racks Market size was valued at USD 160.32 million in 2020 to USD 318.48 million in 2025 and is anticipated to reach USD 859.18 million by 2035, at a CAGR of 10.29% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2035 |

| China Data Center Racks Market Size 2025 |

USD 318.48 Million |

| China Data Center Racks Market, CAGR |

10.29% |

| China Data Center Racks Market Size 2035 |

USD 859.18 Million |

Rising AI workloads, 5G deployments, and the government’s push for data localization are driving strong demand for advanced rack systems. Enterprises and cloud service providers are investing in modular, scalable racks to handle high-density computing. Technology shifts toward liquid cooling, smart monitoring, and integrated power solutions are changing rack configurations. Innovation is focused on thermal management, real-time analytics, and workload optimization. The market holds strategic importance for investors targeting digital infrastructure, especially in hyperscale and AI-centric facilities.

North and East China lead the market due to dense enterprise clusters and hyperscale development in cities like Beijing and Shanghai. South China is emerging with growing e-commerce and AI investment, especially around Guangdong and Shenzhen. Western and Central China are gaining traction from national data migration programs and lower power costs. These regions offer large land banks and policy incentives that support rack deployment in newly built hyperscale zones.

Market Dynamics:

Market Drivers

Rapid Digital Transformation Across Industries Is Creating Strong Rack Demand Across China

The surge in digital platforms across finance, healthcare, and retail has sharply raised infrastructure needs. Enterprises demand scalable rack systems to support growing data volumes, real-time analytics, and hybrid cloud strategies. The China Data Center Racks Market benefits from this shift, with buyers prioritizing space efficiency, airflow optimization, and power load balancing. Telecom firms are modernizing network backbones, driving upgrades in rack architecture. Cloud providers are also rolling out new zones requiring denser, modular racks. E-commerce and video streaming services need racks with better cable management and cooling integration. This creates a large addressable market across public and private operators. The market supports critical backend functions for national digitization goals. It remains essential for businesses scaling infrastructure without compromising energy efficiency.

Strong AI and HPC Adoption Is Accelerating the Shift Toward High-Density Rack Designs

China’s focus on AI and high-performance computing is transforming rack infrastructure standards. New GPU clusters and AI training environments demand racks that support 40–100 kW densities. Liquid cooling integration is increasing, requiring custom-designed enclosures and high-load-bearing racks. The China Data Center Racks Market has seen demand shift toward prefabricated, high-resilience formats. Leading cloud players have redesigned core facilities to prioritize vertical growth and server density per footprint. Rack-level cooling and power delivery systems have become critical design parameters. Businesses investing in AI need reliable rack ecosystems to handle thermal and electrical loads. Government policies backing AI compute zones support long-term infrastructure investments. This evolution has made racks a strategic purchase in performance-driven deployments.

Government Policies and Infrastructure Initiatives Are Stimulating Large-Scale Rack Deployments

Policies like “Eastern Data, Western Computing” are shifting workloads to inland regions, creating demand for rack capacity across provinces. Investments in national computing hubs are accelerating rack installations in both hyperscale and edge sites. Energy-efficiency standards and modular buildouts influence rack configurations to support low PUE targets. The China Data Center Racks Market benefits from strong regulatory support for domestic manufacturing and sustainable IT infrastructure. Operators must deploy rack systems that comply with fire safety, grounding, and airflow standards. Local vendors are increasing innovation to meet these evolving compliance requirements. Enterprises working with state-backed cloud platforms are scaling infrastructure aligned with digital public services. The regulatory framework continues to shape design preferences across tier-1 and tier-2 cities.

- For instance, Gansu’s State Grid cloud center installed 3,000 racks at an initial cost of RMB 1 billion as part of national computing hub build-outs under the policy.

Enterprise Cloud Shift and Modular Data Center Adoption Are Reshaping Procurement Needs

Private enterprises are modernizing their IT with cloud-first architectures that depend on flexible and secure rack environments. Modular and prefabricated data centers drive demand for plug-and-play rack solutions. The China Data Center Racks Market supports scalable deployments for customers managing hybrid and multi-cloud strategies. Racks that enable easy installation of smart PDUs, sensors, and thermal controls are now favored. Growing edge computing projects in manufacturing and logistics also require compact and ruggedized racks. Enterprises want rapid deployment with built-in power and network management integration. These preferences drive innovation among domestic suppliers, increasing market competitiveness. Rack systems are now seen not just as hardware, but as part of overall IT optimization strategies.

- For example, Huawei’s CloudMatrix 384 system, unveiled at the 2025 World AI Conference, is a rack‑scale AI computing architecture using 384 Ascend 910C NPUs across multiple racks to support high‑density AI workloads with unified, high‑bandwidth interconnects.

Market Trends

Shift Toward Liquid-Cooled and Rear-Door Heat Exchanger Rack Systems for AI Workloads

High-density workloads from AI and machine learning require rack systems capable of advanced cooling. Rack manufacturers in China are integrating support for liquid cooling and rear-door heat exchangers. These solutions help achieve thermal efficiency while maintaining rack space availability. The China Data Center Racks Market is seeing hyperscalers adopt direct-to-chip and immersion-cooled systems within standard 42U and above racks. Equipment standardization ensures compatibility with evolving data center form factors. Vendors are releasing pre-certified liquid cooling-compatible racks to match power-intensive rack unit densities. Market buyers demand future-proof systems to reduce retrofit costs. These developments reflect a broader trend toward thermal-aware rack procurement.

Deployment of Edge Data Centers Is Driving Demand for Compact, Ruggedized Rack Units

Edge computing is rising across transportation, energy, and retail sectors in China, creating new rack demand outside core zones. Compact, shock-resistant, and temperature-resilient racks are required for these environments. The China Data Center Racks Market is adjusting to this trend with localized manufacturing of edge-compatible units. Buyers in logistics and industrial automation need enclosures that secure data at the source. IP-rated racks and outdoor cabinets are in higher demand. Form factor adaptation supports unmanned sites with remote monitoring needs. Businesses increasingly seek enclosures that integrate UPS, switches, and compute into a single rack footprint. Edge-ready solutions drive value in bandwidth-sensitive use cases.

Integration of Smart Power and Environmental Monitoring Capabilities Within Racks

Data centers now require racks with built-in intelligence for power, temperature, and humidity control. Rack systems are being integrated with advanced sensors and smart PDUs to optimize uptime. The China Data Center Racks Market has shifted toward intelligent enclosures capable of edge analytics. Operators need real-time alerts on thermal loads, airflow imbalances, and unauthorized access. This drives demand for software-defined rack environments and centralized DCIM compatibility. Racks function as infrastructure endpoints rather than passive steel frames. Enhanced rack telemetry supports predictive maintenance and automation in large-scale deployments. Integration improves operational control and supports compliance tracking across multiple sites.

Vendor-Led Standardization and Modular Rack Configurations Are Improving Deployment Speed

Domestic and international vendors are driving a shift toward pre-engineered and standardized rack formats. Modular configurations enable fast deployment across diverse facility types. The China Data Center Racks Market supports rack-and-stack models using pre-tested components. This approach improves speed-to-market while reducing custom engineering costs. Facility owners prefer uniformity for rack heights, rail compatibility, and airflow design. Vendors are launching tool-less installation systems and cable management accessories as standard offerings. Pre-assembled kits improve efficiency across hyperscale, colocation, and private builds. Standardization helps reduce lead times and accelerates project execution in high-growth clusters.

Market Challenges

Heat Management and Power Delivery Constraints Limit Ultra-Dense Rack Deployments in Legacy Sites

High-density racks generate significant heat, often beyond the cooling limits of older data centers. Many facilities still rely on raised-floor designs not optimized for liquid or rear-door cooling. The China Data Center Racks Market faces deployment hurdles in retrofitting legacy infrastructure with modern rack technologies. Operators struggle to meet thermal thresholds when deploying racks above 30 kW without major upgrades. Power delivery systems also need rewiring to support higher load racks, which adds capital costs. Constraints around floor loading and ceiling height affect rack configuration. These factors slow down modernization and limit adoption of advanced rack systems in traditional enterprise environments.

Supply Chain Volatility and Component Sourcing Delays Impact Rack Availability and Customization

Global metal supply fluctuations and regional manufacturing restrictions affect rack pricing and production timelines. Buyers face delays for custom enclosures, rail kits, and accessories needed for unique workloads. The China Data Center Racks Market must navigate logistics bottlenecks for cable trays, lock systems, and brushed panels. Cross-border shipping of certain components remains slow due to inspection and customs delays. Domestic manufacturing helps ease pressure but cannot always meet high-spec or fast-turnaround demands. Smaller players struggle to scale without assured access to parts and raw materials. This adds risk for buyers planning large data center rollouts across multiple cities.

Market Opportunities

Growth of Tier-2 and Tier-3 Cities Opens New Avenues for Scalable Rack Deployments

Government incentives are pushing digital infrastructure into inland cities like Chengdu, Guiyang, and Xi’an. These regions offer low energy costs and abundant land for hyperscale sites. The China Data Center Racks Market can expand by supplying modular racks for prefabricated builds. Operators target scalable rack designs that meet green building standards and optimize airflow. Rack manufacturers can benefit by localizing production near inland clusters and supporting emerging data zones.

Rising Global Interest in Chinese Rack Manufacturing Boosts Export Potential

China’s rack manufacturers have strengthened design quality, thermal engineering, and power integration capabilities. Global markets are sourcing cost-efficient, high-performance racks for AI and cloud builds. The China Data Center Racks Market gains export potential by meeting international standards like RoHS, CE, and UL. Suppliers offering ODM/OEM services have new opportunities in Southeast Asia, Africa, and Latin America. Export-ready product lines enable global expansion.

Market Segmentation

By Rack Type

Cabinet racks dominate the China Data Center Racks Market due to their enclosed structure, which offers better security, airflow control, and cable management. They are widely adopted in hyperscale, colocation, and enterprise environments, accounting for the largest market share. Open frame racks, while cost-effective and easier to install, are preferred in test labs or controlled environments. The “others” category, including wall-mount and micro racks, sees rising demand from edge deployments.

By Rack Height

42U racks hold the largest share in the China Data Center Racks Market, as they offer an ideal balance between space, airflow, and ease of maintenance. This height is considered a global standard and fits well with modular designs. Below 42U racks are used in compact or edge data centers, while above 42U configurations support high-density workloads in AI and HPC environments. The shift toward taller racks is increasing due to growing floor space constraints.

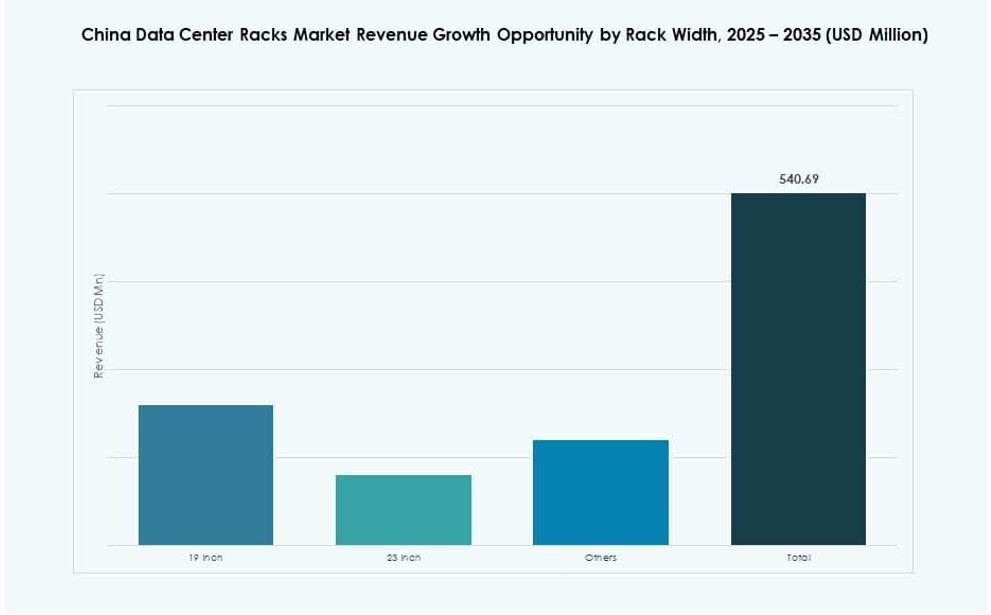

By Width

19-inch racks are the industry standard in China and dominate the China Data Center Racks Market. They are compatible with most server and network equipment. 23-inch racks have gained limited traction for telecom and custom applications that require broader cable spacing. “Others” include proprietary and customized widths for niche use cases like industrial or rugged edge deployments, which remain a small but emerging segment.

By Application

Server racks lead the China Data Center Racks Market in terms of volume and revenue, driven by demand from cloud service providers and large enterprises. These racks house critical compute infrastructure and must support high weight and airflow needs. Network racks are essential for backbone connectivity, usually deployed in parallel with server racks, and hold switches, routers, and patch panels. Both segments require structured layouts and power provisioning.

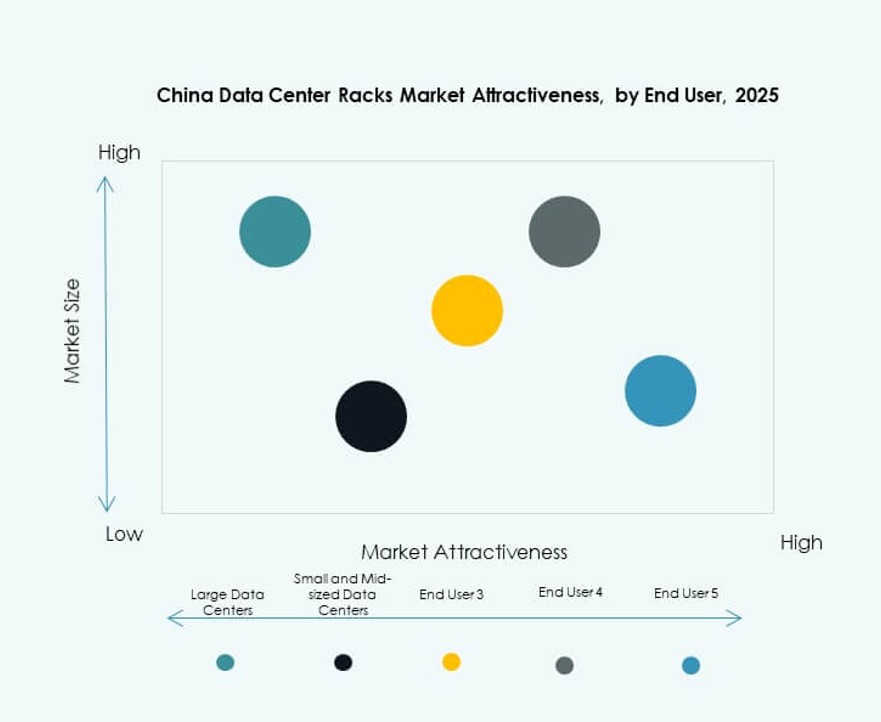

By End-user

Large data centers contribute the majority share in the China Data Center Racks Market. These include hyperscale and colocation facilities with high-density rack needs and complex power-cooling integration. Small and mid-sized data centers serve localized and edge workloads, preferring pre-assembled racks for faster deployment. Both segments show rising interest in smart racks with integrated power and monitoring capabilities.

By Vertical

IT & telecom dominates the China Data Center Racks Market due to its vast network infrastructure and cloud buildouts. BFSI and government & defense sectors follow, requiring highly secure, monitored rack setups. Healthcare and retail are adopting modular racks for digitized patient records and e-commerce operations. Energy companies use ruggedized racks in field and offshore applications. The “others” segment includes education, manufacturing, and logistics industries with growing digitization needs.

Regional Insights

North and East China Lead Rack Demand with Strong Enterprise and Hyperscale Growth

North China, led by Beijing and Tianjin, holds around 35% market share in the China Data Center Racks Market. These areas host major government cloud infrastructure and telecom hubs. East China, including Shanghai, Jiangsu, and Zhejiang, contributes about 32%, driven by finance, manufacturing, and enterprise IT needs. Both regions benefit from dense fiber connectivity, advanced facilities, and established data center ecosystems. They remain the core zones for high-end rack deployments.

- For example, in January 2024, Alibaba Group announced the development of three new data centers across China, including Shanghai, with a combined planned expansion totaling 2 million square meters to support national cloud and AI workloads.

South China Emerges as a Fast-Growing Zone Due to E-Commerce and AI Expansion

South China holds approximately 18% of the market, with Guangdong and Shenzhen at the forefront of cloud, AI, and fintech growth. New data centers are being built with high rack densities and smart power integration. Demand stems from local tech giants, export-focused firms, and digital startups. The region’s industrial transformation supports deployment of customized rack systems for AI, retail, and video processing workloads. It continues to gain momentum due to its commercial dynamism.

- For example, Tencent, Alibaba, and Baidu have collaborated under the Open Data Center Committee (ODCC) to co‑develop Scorpio rack specifications that support hyperscale deployments and high‑density AI workloads with power levels above 30 kW per rack.

West and Central China Witness Accelerated Rack Growth from National Infrastructure Programs

Western and Central China regions account for roughly 15% market share in the China Data Center Racks Market. These areas are vital to national projects like “Eastern Data, Western Computing,” which shifts workloads to areas like Guizhou and Inner Mongolia. Lower land and energy costs enable hyperscale investments with high-rack capacity. Policy incentives attract data center operators who seek to expand into cost-efficient zones. The rack market in these regions is expected to grow at a double-digit rate.

Competitive Insights:

- Schneider Electric

- Vertiv Group

- Rittal

- Huawei (Zhongxing Cabinets)

- Kstar Cabinets

- Cisco Systems, Inc.

- Dell Inc.

- Hewlett Packard Enterprise (HPE)

- Legrand

- Panduit Corp.

The China Data Center Racks Market is highly competitive, with global OEMs and domestic manufacturers competing across design, density, and customization. It is led by Vertiv, Schneider Electric, and Rittal, who offer integrated rack solutions for hyperscale and modular deployments. Local players like Kstar and Zhongxing Cabinets gain traction through cost-effective, prefabricated options tailored for regional workloads. Companies compete on innovation, including rack-based cooling, power integration, and smart monitoring. Strategic partnerships with cloud providers and colocation firms support market expansion. Players investing in liquid cooling compatibility, faster deployments, and edge-ready formats are outperforming. Custom rack design and value-added services differentiate vendors in high-growth regions like South and Western China.

Recent Developments:

- In November 2025, Foxconn entered a partnership with OpenAI to co‑design and engineer AI data center racks and related infrastructure components. The collaboration focuses on rack design, cabling, power systems, and cooling tailored to advanced AI workloads.

- In August 2025, Vertiv completed the acquisition of Great Lakes Data Racks & Cabinets, strengthening its infrastructure solutions portfolio. Great Lakes adds custom rack enclosures, cable management systems, and seismic cabinet capabilities to Vertiv’s offerings.