Executive summary:

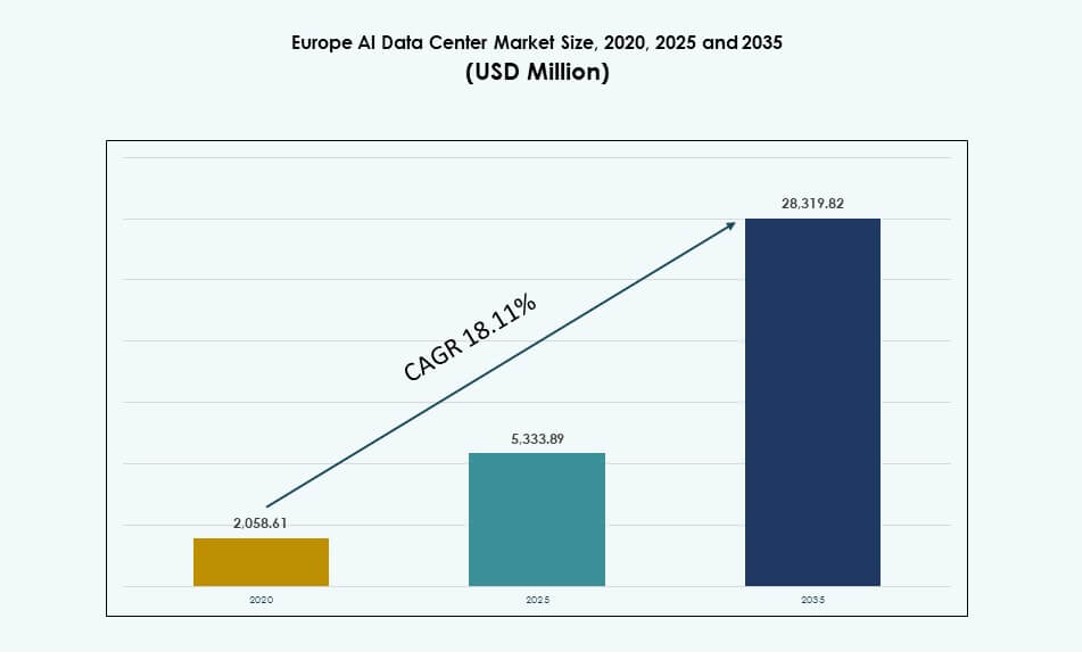

The Europe AI Data Center Market size was valued at USD 2,058.61 million in 2020 to USD 5,333.89 million in 2025 and is anticipated to reach USD 28,319.82 million by 2035, at a CAGR of 18.11% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2035 |

| Europe AI Data Center Market Size 2025 |

USD 5,333.89 Million |

| Europe AI Data Center Market, CAGR |

18.11% |

| Europe AI Data Center Market Size 2035 |

USD 28,319.82 Million |

The market is driven by increasing AI workload demand across sectors like finance, healthcare, manufacturing, and telecom. Enterprises invest in high-density infrastructure with liquid cooling, modular racks, and advanced orchestration tools. Hyperscalers expand GPU clusters to support model training and inferencing at scale. Cloud-native services and sovereign AI zones are accelerating deployments. Organizations prioritize low latency, sustainability, and compliance. Green energy integration and automation enhance cost-efficiency. The market supports innovation across AI lifecycle needs, making it strategic for investors focused on digital infrastructure and enterprise transformation.

Western Europe leads the market with strong digital maturity, data regulations, and cloud infrastructure in countries like Germany, France, Ireland, and the UK. Northern Europe is emerging due to green energy availability and government-backed AI zones in Sweden and Finland. Southern and Eastern Europe show growth through public-sector projects and telecom-led edge deployments. Tier-2 cities see rising demand driven by latency-sensitive workloads and regional data processing needs.

Market Dynamics:

Market Drivers

Rapid Expansion of AI-Driven Workloads Across Core Industry Verticals and Enterprise Functions

Enterprise adoption of artificial intelligence across Europe is rising in banking, healthcare, manufacturing, and telecom. Organizations deploy AI models for fraud analytics, patient diagnostics, customer insights, and smart factory operations. The surge in AI workloads creates strong demand for compute-intensive infrastructure. The Europe AI Data Center Market supports growing needs for GPU-based acceleration and data storage at scale. AI training clusters now require high-density rack systems with direct-to-chip cooling and resilient interconnects. IT decision-makers prioritize low-latency processing and real-time analytics. Increased model complexity also fuels infrastructure upgrades and cluster scaling. It presents a critical infrastructure backbone for digital competitiveness. Regional governments support the trend with AI ecosystem investments.

Widespread Integration of Advanced Cooling and Power Systems for High-Density AI Infrastructure

Thermal management innovation is a top driver for AI data center upgrades across Europe. Liquid cooling adoption is growing in both hyperscale and enterprise environments. Operators integrate rear door heat exchangers, direct-to-chip systems, and immersion cooling setups. These technologies support workloads with 30 kW to 100 kW per rack density. The Europe AI Data Center Market sees rising installation of modular UPS and high-efficiency power systems. Integration of renewable sources into grid and backup architecture is increasing. Data center operators optimize energy use to meet ESG requirements. High-density compute loads require efficient airflow and thermal design. AI applications push facilities toward intelligent infrastructure and smart power routing.

- For instance, Vertiv provides rear-door heat exchanger systems across European data centers, supporting AI workloads with rack densities approaching 50 kW, helping operators improve thermal efficiency without large-scale retrofits.

Surging Cloud Investments from U.S. and Regional Hyperscale Players Across Key European Zones

Microsoft, AWS, Google, and Oracle are expanding their AI-ready cloud regions across Western and Northern Europe. These deployments include high-density racks, liquid cooling systems, and GPU clusters for foundation model workloads. The Europe AI Data Center Market benefits from hyperscale activity in Dublin, Frankfurt, Madrid, and Paris. Cloud-native AI tools drive consumption growth among enterprises and developers. National digital strategies in countries like France and Germany reinforce data sovereignty and regional AI leadership. Interoperability with edge zones enables hybrid deployment flexibility. Investors view the region as a secure and growth-aligned AI infrastructure market. It drives large-scale construction, supplier engagement, and cross-border connectivity upgrades.

Focus on Sovereign AI Infrastructure and Policy-Driven Demand from Public Institutions

European governments prioritize sovereign infrastructure to support sensitive AI use cases in defense, healthcare, and education. AI regulations such as the EU AI Act guide infrastructure requirements and data handling. This creates structured demand for secure and compliant AI compute zones. The Europe AI Data Center Market gains from initiatives like Gaia-X, EuroHPC, and national AI centers. Public-private partnerships fuel high-density buildouts with GPU clusters, liquid-cooled racks, and integrated DCIM. Policy clarity ensures predictable investment environments for operators and hyperscale firms. Sovereign clouds and classified data mandates require localized facilities. It strengthens infrastructure alignment with digital ethics, privacy, and security goals.

- For instance, the EuroHPC-backed LUMI supercomputer in Finland delivers up to 2.35 exaflops in mixed-precision AI performance (HPL-MxP) using AMD EPYC CPUs and MI250X GPUs. Designated as one of the EU’s sovereign AI Factories, LUMI supports large-scale AI and HPC workloads for public institutions across Europe.

Market Trends

Rising Adoption of Rack-Level Liquid Cooling Systems Across AI-Optimized Colocation Facilities

Data center operators across Europe are rapidly adopting liquid cooling technologies to support AI loads. Rack-level designs support direct-to-chip cooling, immersion tanks, and rear-door heat exchangers. New colocation builds offer pre-fitted systems for AI tenants deploying 30–50 kW racks. The Europe AI Data Center Market reflects this shift in both hyperscale and regional markets. Operators reduce PUE and thermal hotspots through advanced CFD modeling. Liquid cooling supports predictable thermal profiles for dense GPU clusters. Facilities improve uptime and reduce cooling-related power use. Adoption accelerates in AI zones like Frankfurt, Amsterdam, and Zurich. It redefines thermal planning and hardware lifecycle.

AI-Specific Rack Designs and Power Delivery Models Enabling Modular Deployment at Scale

Modular rack configurations are gaining traction across AI deployments. Operators use standardized 42U and 48U racks with power densities above 30 kW. Pre-assembled systems with integrated PDUs, busways, and liquid-cooling loops reduce deployment time. The Europe AI Data Center Market shows increasing demand for flexible rack power provisioning. Dual-feed configurations, battery backup zones, and edge-aligned cabinets are becoming common. Operators tailor power delivery for ML, GenAI, and NLP applications. AI labs and cloud regions adopt scalable, high-resilience designs. Rack-level optimization supports phase-wise deployment and cost predictability. It reflects the market’s move toward modular, scalable AI infrastructure.

Integration of Renewable Energy Sources in AI Data Centers to Support Sustainability Targets

Data center operators are aligning with regional sustainability mandates by integrating wind, hydro, and solar energy sources. Operators in Norway, Sweden, and Finland use grid-based renewables to power AI racks. The Europe AI Data Center Market reflects ESG-driven demand among enterprise customers. On-site solar arrays and hydrogen-based UPS pilots are emerging trends. Cloud players commit to carbon-neutral AI zones by 2030. AI workloads create high electricity draw, making energy mix optimization essential. Operators implement real-time energy usage dashboards with AI-based energy load balancing. Partnerships with utilities secure green energy contracts. It reinforces long-term energy resilience and policy alignment.

Emergence of Edge AI Zones in Secondary Cities to Support Latency-Sensitive and Federated Workloads

AI infrastructure is expanding into edge zones to support latency-sensitive use cases. Secondary cities across Spain, Poland, and the Nordics are deploying AI micro data centers. These support smart city, retail, and IoT applications needing fast inference. The Europe AI Data Center Market supports edge zones with 5G integration and localized compute. Federated learning models drive demand for regional data processing. Smaller racks with GPU nodes and liquid cooling are integrated into urban edge locations. Telecom firms invest in AI-ready metro cores. Hybrid architectures connect edge to core AI zones. It expands the addressable market for infrastructure providers.

Market Challenges

Energy Grid Constraints and Power Allocation Uncertainty Impacting High-Density AI Infrastructure Rollouts

The rapid growth of AI workloads increases electricity demand across European data centers. High-density racks supporting GPUs draw large power loads per cabinet. Grid capacity in metro zones is strained by rising compute needs and housing policies. The Europe AI Data Center Market faces bottlenecks in obtaining new power allocations. Delays in utility permitting and substation construction hinder facility buildouts. Grid stability requirements impact deployment of renewable-integrated power systems. Operators must balance AI compute expansion with energy availability. Governments push demand-response programs, but long-term solutions are uneven. Investment decisions face uncertainty around energy availability and regional planning.

Skill Gaps in AI Infrastructure Operations and Limited Availability of Specialized Workforce

AI data centers require specialized expertise in managing high-density racks, liquid cooling, and AI cluster orchestration. Operators face shortages of personnel with experience in GPU server maintenance and thermal management. The Europe AI Data Center Market struggles with workforce training at the same pace as demand. Educational institutions lag in providing AI infrastructure-focused programs. Hiring is competitive across Western and Northern Europe. Vendors and colocation providers launch workforce upskilling partnerships. AI deployment quality depends on skilled professionals in operations and maintenance. Without adequate talent, infrastructure uptime and efficiency face risks.

Market Opportunities

Development of Sovereign AI Zones Aligned with EU Regulations for National-Level AI Infrastructure Needs

EU-backed regulatory frameworks drive investment into sovereign AI data centers across member states. Countries seek AI facilities with full compliance to GDPR and AI Act standards. The Europe AI Data Center Market benefits from this push for regionalized and trusted compute zones. Government-backed GPU clusters and AI labs present large contracts. Opportunities grow for vendors offering policy-compliant hardware, software, and services.

AI Model Localization, Edge AI Training, and High-Density GPU Infrastructure for Vertical-Specific Demand

Sector-specific AI adoption in BFSI, healthcare, and manufacturing drives demand for customized infrastructure. AI models require localized inference zones with low latency and high throughput. The Europe AI Data Center Market sees opportunities in deploying 30–50 kW rack systems for such use cases. Edge AI data centers in tier-2 cities expand vendor footprints. Partnerships with vertical players unlock long-term infrastructure contracts.

Market Segmentation

By Type

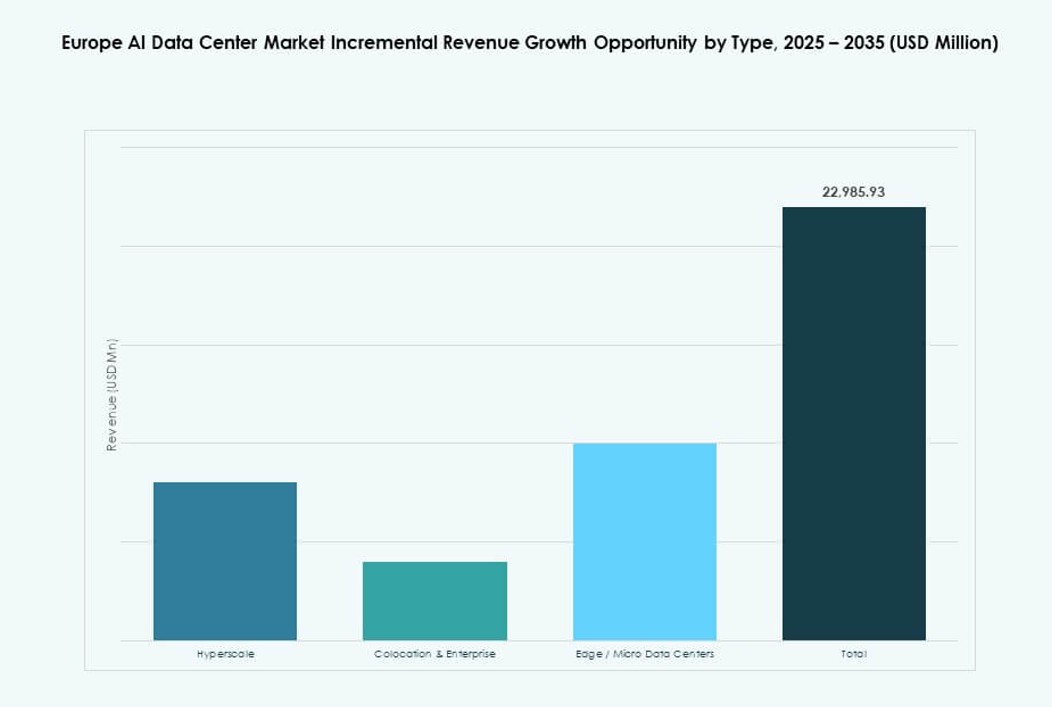

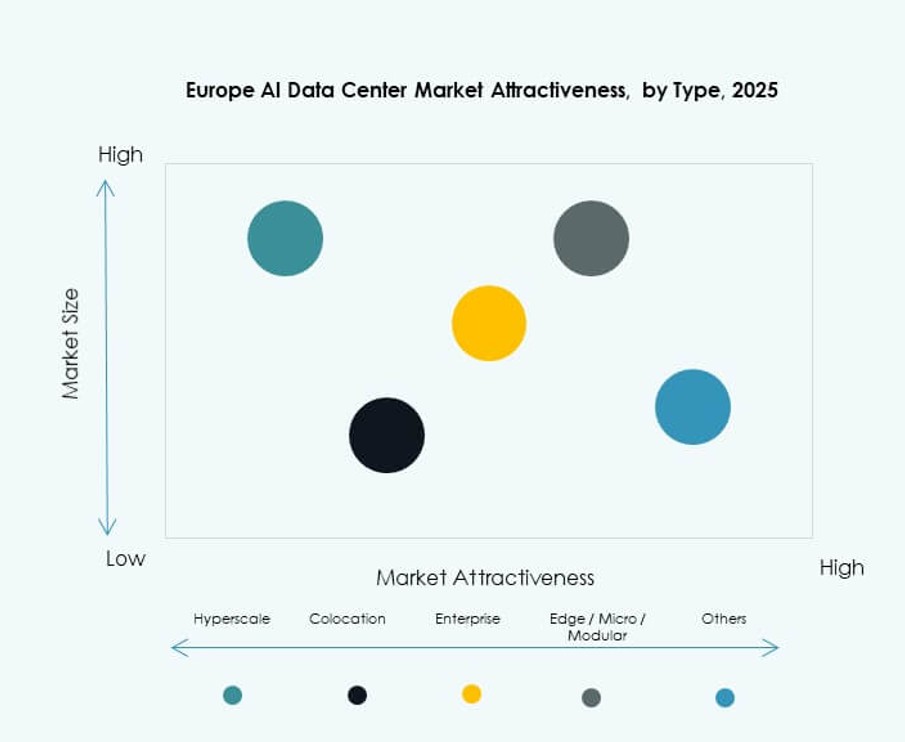

Hyperscale data centers dominate the Europe AI Data Center Market due to widespread deployment by AWS, Microsoft, Google, and Oracle. These facilities support large-scale GPU clusters for training foundational models. Colocation and enterprise segments are growing with demand from private AI workloads and sovereign deployments. Edge and micro data centers gain traction in latency-sensitive and federated AI use cases. Demand for micro AI zones in urban centers rises with 5G expansion.

By Component

Hardware leads the Europe AI Data Center Market due to high investment in GPU servers, AI racks, and liquid cooling systems. Software and orchestration tools grow as operators integrate DCIM, AI observability, and AI workload management platforms. Services segment includes infrastructure consulting, remote hands, and AI cluster support. Integration and optimization services see increased uptake across colocation and enterprise deployments.

By Deployment

Cloud deployment dominates with hyperscale firms building AI regions across Europe. Enterprises use cloud for training and hybrid for inference and compliance-sensitive AI workloads. Hybrid models grow with edge-core integration needs. On-premise deployment remains relevant for regulated verticals like BFSI, defense, and healthcare. Operators offer AI-specific deployment options with containerized racks and GPU blocks.

By Application

Machine Learning holds the largest share in the Europe AI Data Center Market. Generative AI is growing rapidly, driving GPU-intensive rack demand. NLP and computer vision use cases increase across telecom, manufacturing, and government. AI data centers support diverse applications from LLM training to federated learning. The “Others” category includes AI for cybersecurity, recommendation engines, and simulation workloads.

By Vertical

IT and Telecom leads the Europe AI Data Center Market with rising demand for AI-native services and cloud infrastructure. BFSI, healthcare, and retail sectors deploy AI for fraud detection, diagnostics, and consumer insights. Media & entertainment use AI for content generation and personalization. Manufacturing applies AI in predictive maintenance and automation. Each vertical has distinct compute and deployment preferences.

Regional Insights

Western Europe Dominates with Over 45% Market Share Led by Hyperscale Activity and Enterprise AI Demand

Western Europe remains the largest contributor to the Europe AI Data Center Market, holding over 45% market share. The UK, Germany, Ireland, and France host major hyperscale regions and enterprise AI deployments. Frankfurt, London, and Paris act as AI compute hubs with strong interconnectivity and policy alignment. Hyperscale players drive regional expansion with multi-zone infrastructure plans. Enterprise AI adoption is supported by mature data ecosystems and workforce availability. The region benefits from renewable integration and high compliance infrastructure.

- For instance, in November 2025, Google announced a €5.5 billion investment in Germany to expand AI infrastructure, including new data center construction in Dietzenbach and expansion at Hanau, optimized for large-scale model training.

Northern Europe Holds Around 25% Share with Focus on Green AI Infrastructure and Liquid Cooling

Northern Europe accounts for approximately 25% of the market, led by Sweden, Norway, Finland, and Denmark. These countries offer abundant renewable energy and natural cooling advantages. Operators deploy AI racks with high power densities supported by sustainable energy contracts. Stockholm and Oslo see increased GPU cluster deployment for AI workloads. Edge AI zones also emerge to support smart city and industrial use cases. Sustainability mandates drive liquid cooling pilots and carbon-neutral facility designs.

Southern and Eastern Europe Represent 30% Share with Strong Edge Growth and Government-Led Projects

Southern and Eastern Europe together hold nearly 30% market share in the Europe AI Data Center Market. Spain, Italy, Poland, and Romania see growing activity through government-backed AI zones and telecom-led expansions. Local cloud regions support compliance-sensitive AI applications. Edge AI deployments gain traction in tier-2 cities. Colocation providers invest in AI-ready micro facilities across metro zones. These subregions offer cost-effective expansion potential for new AI operators. Growth is driven by digitalization, 5G rollout, and EU infrastructure support.

- For instance, in July 2025, Khazna Data Centers and Eni signed an agreement to develop a 500 MW data center campus in Lombardy, Italy. The project is designed to support large‑scale AI and high‑performance computing workloads and strengthens Italy’s position in sovereign digital infrastructure.

Competitive Insights:

- Microsoft

- Amazon Web Services (AWS)

- Google Cloud

- OVHcloud

- Equinix

- Digital Realty

- IBM

- Meta Platforms

- Dell Technologies

- NVIDIA

The Europe AI Data Center Market features intense competition between hyperscale cloud providers, colocation operators, and infrastructure vendors. Microsoft, AWS, and Google Cloud drive hyperscale deployments across major metros like Frankfurt, Paris, and Dublin. OVHcloud and IBM support sovereign AI cloud services for compliance-focused sectors. Equinix and Digital Realty enable scalable, AI-ready colocation infrastructure with modular rack options. NVIDIA leads in AI accelerators, while Dell and HPE offer integrated GPU clusters and high-density server solutions. Meta expands its own AI infrastructure footprint for internal LLM workloads. It remains a dynamic landscape where players compete on sustainability, rack density, cooling innovation, and compliance capabilities to meet rising AI workload demands across enterprise and public sectors.

Recent Developments:

- In January 2026, Marvell Technology announced it will acquire XConn Technologies to expand its AI data center connectivity portfolio. The acquisition, finalized on January 2, 2026, aims to enhance Marvell’s PCIe and CXL switching silicon offerings critical for high‑bandwidth networking in AI data centers.

- In December 2025, HPE and NVIDIA launched a new AI Factory Lab in Grenoble, France, addressing EU sovereign AI infrastructure needs. The initiative introduces secure, scalable AI infrastructure solutions where enterprises can test and refine workload performance on region‑based systems, supporting data sovereignty and regulatory compliance within the European Union.

- In November 2025, Google announced a €5.5 billion investment in Germany for AI and cloud infrastructure buildouts. The plan covers new data center construction in Dietzenbach and expansion in the Hanau campus, strengthening AI‑optimized compute capacity and cloud services for enterprise and public sector customers across the region.