Executive summary:

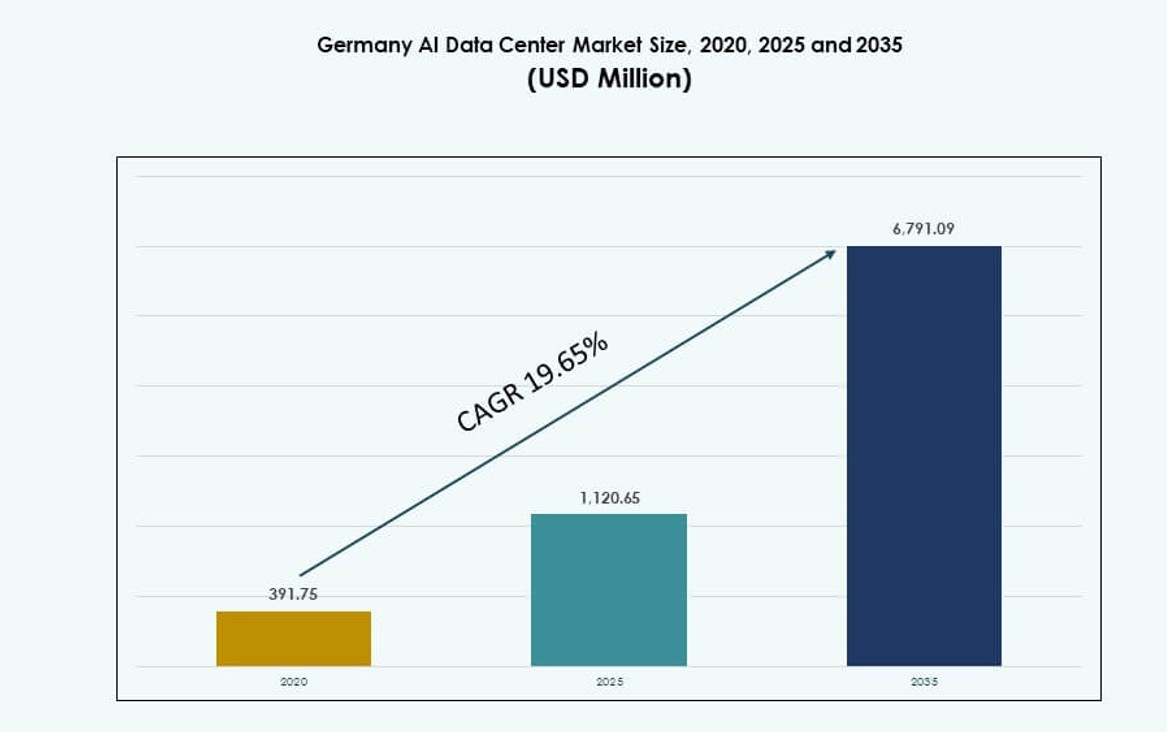

The Germany AI Data Center Market size was valued at USD 391.75 million in 2020 to USD 1,120.65 million in 2025 and is anticipated to reach USD 6,791.09 million by 2035, at a CAGR of 19.65% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2035 |

| Germany AI Data Center Market Size 2025 |

USD 1,120.65 Million |

| Germany AI Data Center Market, CAGR |

19.65% |

| Germany AI Data Center Market Size 2035 |

USD 6,791.09 Million |

The market is being driven by rising demand for high-performance AI compute infrastructure across sectors such as manufacturing, automotive, and finance. Adoption of generative AI, sovereign cloud frameworks, and energy-efficient liquid cooling is shaping infrastructure strategies. Businesses are investing in high-density GPU clusters and digital twin platforms to gain a competitive edge. AI data centers now support mission-critical workloads, requiring strong reliability and regulatory compliance. Germany’s push for data sovereignty aligns with local deployment models. These shifts create long-term value for investors focused on enterprise AI acceleration and digital transformation.

Frankfurt continues to lead due to its dense connectivity, hyperscale cloud zones, and enterprise customer base. Berlin and Munich are gaining traction, supported by AI research ecosystems and startup growth. Hamburg, Stuttgart, and Düsseldorf show steady adoption due to industrial AI applications and access to regional power grids. Distributed edge expansion is also supporting AI inference across multiple urban and industrial zones, strengthening Germany’s national AI infrastructure network.

Market Dynamics:

Market Drivers

Surging Demand for High-Density Compute in AI Training and Inference Workloads

The Germany AI Data Center Market is driven by the sharp rise in demand for AI training and inference infrastructure. Enterprises, research institutions, and startups require high-density racks and specialized GPU clusters to process large AI models. Data centers are evolving to handle these workloads by adopting direct-to-chip liquid cooling and power-efficient designs. AI-based applications across sectors demand lower latency and higher compute throughput. Facility operators are redesigning layouts for thermal efficiency and workload prioritization. Innovation in chip architecture further increases computational requirements. AI-native applications like autonomous driving, generative content, and fraud detection require dense inference models. Businesses are aligning their data strategies to extract more value from internal and external data streams. These shifts elevate the need for purpose-built AI-ready data center ecosystems.

- For instance, NVIDIA’s DGX H100 systems deliver 32 petaFLOPS of FP8 AI performance per rack with 8 H100 GPUs and 640 GB total GPU memory.

Accelerating Adoption of Sovereign Cloud and AI Infrastructure Due to Compliance Mandates

Compliance with national and EU data protection laws influences infrastructure decisions across industries. Sovereign cloud models are expanding, requiring local AI infrastructure that meets security and jurisdiction standards. Germany’s emphasis on digital sovereignty, especially in healthcare, finance, and public sectors, drives private and hybrid data center investments. Operators deploy AI-optimized hardware inside national borders to meet audit and data residency requirements. Government-backed programs further stimulate local AI compute infrastructure. These dynamics are creating an AI-ready ecosystem tailored to GDPR, BSI, and ISO standards. It supports private-sector innovation within regulated frameworks. The Germany AI Data Center Market benefits from this structured push for regulated compute expansion. Operators gain from stronger demand visibility and long-term service contracts.

Rising Integration of AI in Industrial and Automotive Applications Across Core Sectors

Germany’s industrial base increasingly integrates AI into robotics, predictive maintenance, supply chain automation, and autonomous mobility systems. These use cases generate massive volumes of sensor data and require real-time inference capabilities. AI-enabled quality control, computer vision inspection, and smart production lines create demand for low-latency edge-to-core data handling. AI data centers support these applications with specialized clusters, smart storage, and orchestration platforms. Automotive OEMs and suppliers deploy digital twins and reinforcement learning models across product development. The manufacturing sector requires scalable infrastructure to simulate and optimize complex systems. These trends highlight the AI data center’s role in Germany’s industrial digitalization roadmap. Investors view these developments as structurally supportive of long-term compute demand.

- For instance, Siemens’ Amberg Electronics Factory processes 1 billion data points daily across 75,000 sensors for AI-driven predictive maintenance and quality control.

Strategic Investments by Hyperscalers and Operators in AI-Ready Infrastructure

Major hyperscale players, including AWS, Google, and Microsoft, are expanding their AI-optimized data centers across Germany. Their infrastructure strategies focus on energy efficiency, green power sourcing, and high-density capacity. These facilities feature liquid cooling, high-performance fabric, and dedicated zones for large model training. The ecosystem is also supported by colocation and enterprise data centers upgrading to AI specifications. Investment volumes continue to grow due to demand for foundation model development, multilingual NLP, and secure AI hosting. Investors recognize long-term returns from AI infrastructure due to its stickiness and technical barriers. The Germany AI Data Center Market reflects a maturing opportunity driven by strategic deployment of intelligent, scalable infrastructure.

Market Trends

Expansion of Liquid-Cooled Racks and Rear-Door Heat Exchangers for Thermal Efficiency

AI workloads in Germany are pushing thermal output beyond traditional air-cooling thresholds. Liquid-cooled systems and rear-door heat exchangers are gaining traction in new and retrofit data centers. Operators invest in direct-to-chip liquid cooling for racks exceeding 40 kW, reducing energy waste. These systems help maintain uptime for GPU clusters and foundation model training nodes. Cooling innovation is now integral to facility differentiation. Vendors offer modular, closed-loop solutions compatible with existing layouts. Operators reduce PUE while supporting sustained peak performance. Environmental regulations and ESG targets drive accelerated adoption. The Germany AI Data Center Market incorporates thermal innovation to support sustainable AI compute growth.

AI Data Centers Leveraging Green Energy Procurement and Sustainable Design Standards

Carbon-neutral infrastructure is becoming standard in Germany’s AI data center roadmap. Operators are securing long-term green PPAs, especially from wind and hydro assets in Bavaria and Brandenburg. New facilities follow LEED and BREEAM standards, integrating passive cooling, waste heat reuse, and water-free systems. AI clusters operate at higher densities, making power sourcing and cooling critical to ESG compliance. Hyperscalers now co-locate AI deployments near renewable grids. Investors evaluate site plans based on emissions metrics and regulatory alignment. Germany’s energy transition aligns with AI infrastructure needs, creating competitive advantage for green sites. The Germany AI Data Center Market now prioritizes sustainable performance and low-carbon delivery.

Rising Use of AI-Specific Interconnects and Memory Architectures for Performance Gains

AI workloads in Germany increasingly rely on high-throughput interconnects like NVLink, InfiniBand, and PCIe 5.0. These architectures reduce bottlenecks in multi-GPU training and inference pipelines. Memory-bound models benefit from shared HBM stacks and fabric-based memory pooling. Data centers deploy rack-scale systems optimized for model parallelism and distributed inference. Operators select GPUs and accelerators based on AI use case, not just compute density. Infrastructure is tuned to support frameworks like PyTorch, JAX, and ONNX Runtime. Performance-per-watt and memory bandwidth are key KPIs. Germany’s AI infrastructure reflects these micro-architecture shifts. The Germany AI Data Center Market now emphasizes stack-level optimization for workload-specific gains.

Integration of AI-Oriented DCIM and Orchestration for Workload-Aware Operations

AI-specific workload orchestration is reshaping data center management practices. Germany’s facilities integrate DCIM tools with workload-aware insights, thermal maps, and power balancing algorithms. GPU clusters require dynamic scheduling based on model type, latency budget, and power headroom. Orchestration platforms now include ML-based forecasting and AI failure prediction. Operators deploy predictive maintenance modules tied to workload telemetry. Smart racks with node-level management allow granular oversight. These platforms help reduce TCO while maintaining peak compute availability. It also improves SLA adherence across AI deployments. The Germany AI Data Center Market benefits from these advances in autonomous infrastructure control.

Market Challenges

Grid Limitations, Permitting Delays, and Location Constraints for High-Density AI Facilities

Germany’s AI data centers face challenges in accessing high-capacity grid power and securing land near metro zones. Many legacy substations lack the capacity to support 100+ MW campuses. Long permitting timelines delay time-to-market for AI projects, especially in urban areas like Frankfurt and Berlin. Environmental reviews, building codes, and zoning approvals often stall hyperscale developments. Competing land use and ESG rules limit site options. Upgrading transmission infrastructure is capital-intensive and time-bound. The Germany AI Data Center Market must navigate these structural bottlenecks to meet compute demand. Operators mitigate risk through phased builds and regional diversification.

Talent Shortage, Security Concerns, and Ecosystem Fragmentation in AI Infrastructure Deployment

The market also faces shortages of skilled professionals in AI infrastructure, GPU tuning, and data center automation. Talent gaps slow onboarding of AI-ready environments and affect system optimization. Concerns around AI data breaches and unauthorized access grow with model sensitivity. Operators must enforce strict access controls and zero-trust security postures. Fragmentation in platform standards leads to integration issues between AI frameworks and infrastructure stacks. Organizations struggle with siloed data pipelines and lack of unified orchestration. Vendor lock-in risks reduce flexibility in long-term infrastructure planning. The Germany AI Data Center Market must address these technical and operational hurdles to sustain momentum.

Market Opportunities

Emergence of AI Zones and Research-Backed Compute Clusters Across Key Innovation Hubs

Innovation districts in Berlin, Munich, and Stuttgart are building AI zones featuring university-backed compute clusters and private infrastructure. These zones attract startups, industry partnerships, and cross-border AI research projects. The Germany AI Data Center Market benefits from localized compute aligned with public and academic goals. Operators can co-locate with talent and innovation hubs to build specialized, low-latency AI infrastructure.

Rise of Industry-Specific AI Infrastructure Demand in Regulated and Critical Sectors

Sectors like automotive, healthcare, and financial services are investing in dedicated AI infrastructure to comply with security and latency needs. This creates demand for smaller, purpose-built data centers or private AI modules in regulated environments. The Germany AI Data Center Market supports this diversification with tailored offerings and modular deployments.

Market Segmentation

By Type

Hyperscale facilities dominate the Germany AI Data Center Market, accounting for the largest share due to demand from global cloud providers and AI model training. These facilities support multi-megawatt loads, high GPU density, and advanced cooling systems. Colocation and enterprise data centers are expanding AI capacity to serve regulated workloads. Edge and micro data centers are emerging to support inference at local endpoints and industrial zones.

By Component

Hardware leads the component segment in the Germany AI Data Center Market, driven by the deployment of AI accelerators, smart storage systems, and high-density racks. Software and orchestration platforms are growing as operators adopt AI-specific workload management tools. Services including system integration, design, and lifecycle support are rising in importance for scaling AI infrastructure efficiently.

By Deployment

Cloud deployment holds the highest share due to hyperscale cloud region expansion and AI-as-a-service offerings. Hybrid models are gaining adoption among financial institutions and industrial players requiring flexibility and control. On-premise deployments remain relevant in highly regulated sectors needing sovereign compute and data control. The Germany AI Data Center Market reflects this shift toward flexible AI deployment architectures.

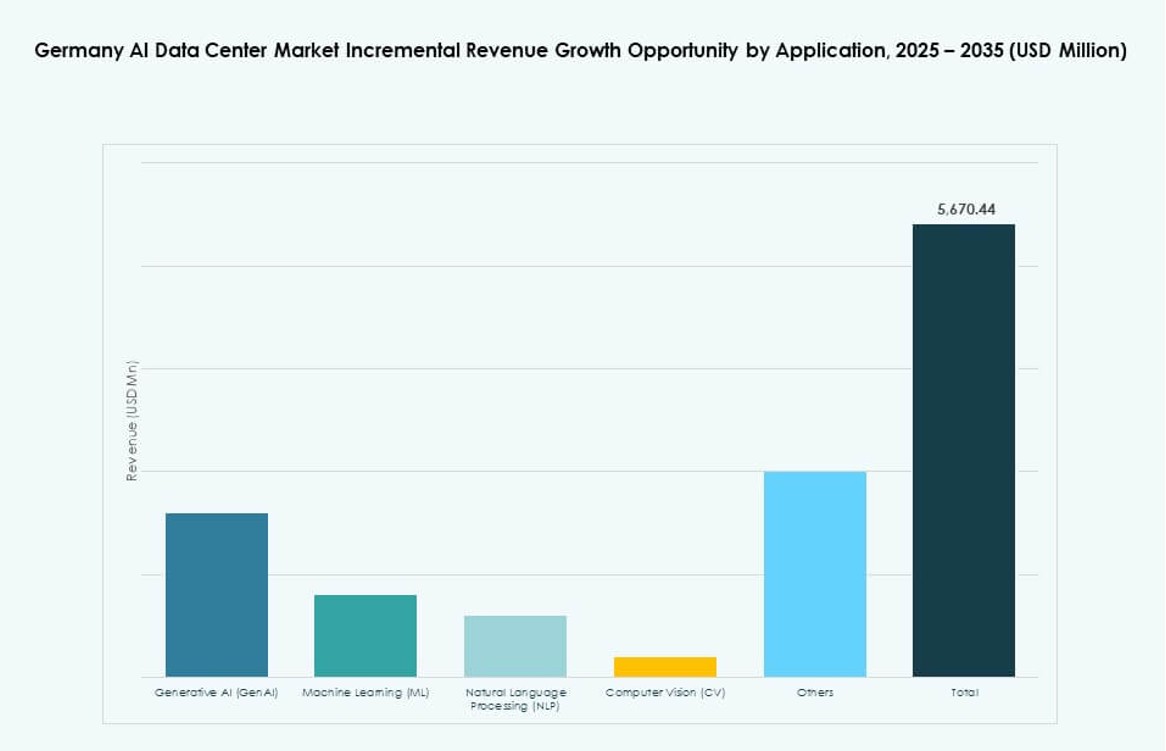

By Application

Machine Learning (ML) is the dominant application in the Germany AI Data Center Market due to widespread use in analytics, recommendation engines, and automation. Generative AI is growing rapidly across creative and enterprise content use cases. Natural Language Processing (NLP) supports multilingual AI models tailored for European markets. Computer Vision (CV) enables industrial and healthcare use cases requiring real-time inference.

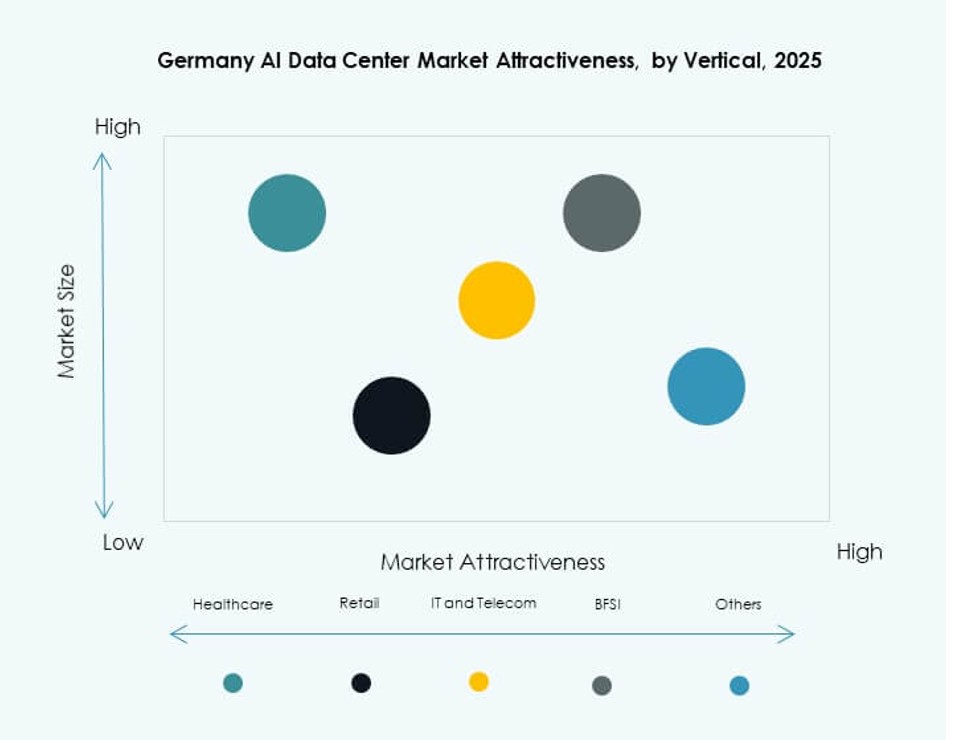

By Vertical

The IT and Telecom segment leads the Germany AI Data Center Market due to cloud service demand and AI-native workloads. BFSI and healthcare sectors adopt AI for fraud detection, diagnostics, and compliance. Automotive and manufacturing segments drive compute demand for simulation and autonomy. Media & entertainment also contributes, particularly in rendering, content personalization, and synthetic generation workflows.

Regional Insights

Frankfurt Metropolitan Region Dominates with Over 40% Share Due to Connectivity and Cloud Zones

Frankfurt remains the core of the Germany AI Data Center Market, accounting for over 40% share. It hosts major cloud regions, fiber interconnection points, and financial AI use cases. The city supports dense data center clusters with reliable grid access. Operators favor Frankfurt due to its ecosystem depth and access to enterprise clients. High availability and low-latency zones make it ideal for AI model training and inference. Power constraints are a concern but managed through phased expansions.

Berlin and Munich Emerging as High-Growth Hubs Driven by Startups and Research Centers

Berlin and Munich jointly contribute over 25% of the Germany AI Data Center Market. Berlin benefits from AI startup growth, digital public services, and tech ecosystem maturity. Munich supports automotive and industrial AI research with university and corporate collaboration. Both cities receive public support for AI innovation zones. The regions attract modular data center deployments and sovereign AI compute clusters. Their position strengthens due to talent availability and high-speed network access.

- For instance, T-Systems partnered with NVIDIA in 2025 to launch a sovereign AI cloud designed for EU-compliant industrial workloads, with deployment planned across German facilities starting in 2026.

Stuttgart, Düsseldorf, and Hamburg Showing Steady Adoption Backed by Industrial AI Applications

Secondary cities like Stuttgart, Düsseldorf, and Hamburg hold over 20% combined share in the Germany AI Data Center Market. These regions benefit from strong industrial bases and emerging AI demand in logistics, manufacturing, and mobility. Data center expansion is supported by lower land costs and proximity to enterprises. Operators target AI-specific use cases such as predictive maintenance and digital twins. Steady adoption across these cities expands Germany’s distributed AI infrastructure footprint.

- For instance, Vantage Data Centers secured €720 million financing in 2025 for expansions across German sites including Stuttgart-area facilities supporting 50 MW AI workloads.

Competitive Insights:

- maincubes

- NORIS Network

- e-shelter

- Microsoft (Azure)

- Amazon Web Services (AWS)

- Google Cloud

- Meta Platforms

- Equinix

- Digital Realty Trust

- NVIDIA

The Germany AI Data Center Market features a dynamic competitive environment shaped by both global hyperscalers and regional operators. AWS, Google, and Microsoft are scaling AI-ready zones with massive GPU clusters, liquid cooling, and sovereign cloud controls. Regional players like maincubes, NORIS Network, and e-shelter target localized demand through colocation and edge-ready infrastructure. Equinix and Digital Realty offer hybrid AI deployments with strong interconnection services. NVIDIA powers the compute layer with accelerators critical for GenAI and HPC. The market benefits from strategic partnerships, data sovereignty compliance, and high-density infrastructure. It remains competitive through energy-efficient design, regulatory alignment, and edge AI expansion across metro zones.

Recent Developments:

- In January 2026, Siemens and NVIDIA expanded their strategic partnership to advance AI-driven industrial automation. The initiative centers on Siemens’ Electronics Factory in Erlangen, Germany, which is now being equipped with NVIDIA’s AI infrastructure and Omniverse platform.

- In November 2025, Google announced a €5.5 billion investment plan through 2029, including a new AI-ready data center in Dietzenbach and upgrades to its Hanau facility to support Vertex AI and Gemini models for German businesses like Mercedes-Benz.

- In November 2025, Deutsche Telekom partnered with Nvidia on a €1 billion AI cloud for industrial applications, launching in Q1 2026 to provide sovereign GPU access via T-Systems’ facilities.