Executive summary:

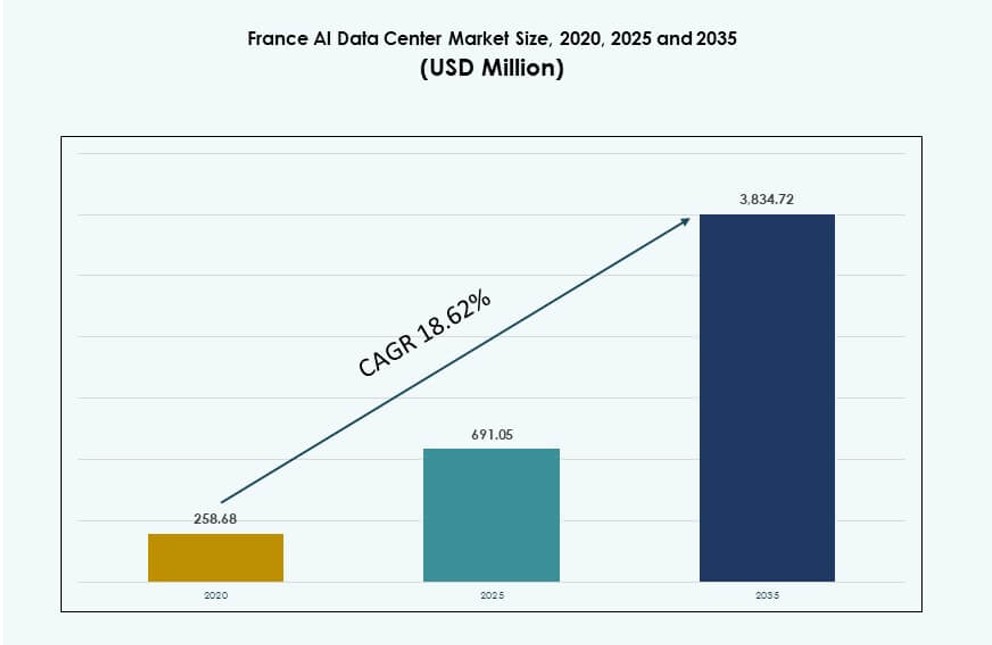

The France AI Data Center Market size was valued at USD 258.68 million in 2020 to USD 691.05 million in 2025 and is anticipated to reach USD 3,834.72 million by 2035, at a CAGR of 18.62% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2035 |

| France AI Data Center Market Size 2025 |

USD 691.05 Million |

| France AI Data Center Market, CAGR |

18.62% |

| France AI Data Center Market Size 2035 |

USD 3,834.72 Million |

The market is gaining momentum due to rapid advancements in generative AI, sovereign cloud initiatives, and hyperscale infrastructure. Enterprises and cloud providers are investing in high-density, liquid-cooled data centers to meet the rising demand for AI training and inference. Government support for digital sovereignty and data localization strengthens market confidence. AI workloads across sectors like healthcare, BFSI, and manufacturing continue to grow. Businesses seek scalable, compliant infrastructure to support mission-critical AI deployments. Innovation in cooling, orchestration, and GPU architecture reshapes operational benchmarks.

Paris leads the market due to its dense enterprise cluster, government-backed cloud zones, and strong network backbone. It hosts the largest concentration of hyperscale and sovereign AI facilities. Marseille is growing rapidly with strategic cable landing points that support international AI traffic and cross-border workloads. Lyon, Bordeaux, and Lille are emerging markets driven by land availability, government incentives, and proximity to research hubs. These regional expansions support edge deployments and localized AI applications across industrial zones. The geographic spread ensures infrastructure redundancy, data compliance, and broader AI service reach.

Market Dynamics:

Market Drivers

Surging Demand for AI Compute Power Accelerates Hyperscale and Enterprise Infrastructure Investments

France is witnessing rising AI workloads across sectors such as BFSI, healthcare, and manufacturing. Enterprises are scaling compute capacity to support large language models and AI-driven automation. Hyperscale providers are deploying high-density infrastructure optimized for GPU clusters. The France AI Data Center Market benefits from strong demand for liquid-cooled racks and modular power systems. Government-backed digital transformation plans further accelerate infrastructure rollout. AI model training and inference need low-latency, high-performance environments. Public and private sectors prioritize AI-ready capacity for data-intensive applications. Investors focus on long-term ROI through scalable, sustainable infrastructure models. It offers strategic positioning for pan-European AI service delivery.

Strategic Government Support Through Sovereign AI and Cloud Initiatives Fuels Infrastructure Growth

France’s government policies support digital sovereignty and national AI leadership through public funding and regulatory alignment. The national cloud strategy incentivizes domestic data center development for critical AI services. Sovereign cloud projects attract private players aiming to meet GDPR, HDS, and SecNumCloud standards. Public sector clients increasingly rely on in-country facilities to process AI workloads. Strategic initiatives strengthen trust in French infrastructure providers. AI-focused startups and enterprises gain compute access through localized services. The France AI Data Center Market benefits from the alignment of regulatory compliance with compute infrastructure growth. Energy-efficient and AI-specific configurations gain priority in funding. It supports geopolitical data localization efforts.

- For instance, a Bpifrance, MGX, Mistral AI, and NVIDIA joint venture plans a 1,400 MW AI-ready data center campus starting construction in Q2 2026.

Shift Toward High-Density Liquid Cooling Systems to Handle AI Workload Heat and Energy Demands

Rising deployment of AI chips and accelerators increases power density and thermal challenges. Liquid cooling adoption rises as enterprises shift from air-based systems to advanced thermal solutions. Rack-level designs now support over 30 kW for deep learning clusters. Direct-to-chip and immersion cooling solutions gain traction in AI-centric deployments. Infrastructure operators integrate heat reuse and closed-loop liquid systems. The France AI Data Center Market sees strong momentum in high-density facilities backed by R&D investment. Power and cooling efficiency becomes a differentiator among colocation providers. Equipment vendors prioritize modular, AI-ready systems. It drives convergence of cooling design and compute innovation.

- For instance, in February 2025, Equinix inaugurated its PA13x data center in Paris with a €350 million investment to support AI workloads and high-performance infrastructure across the Île-de-France region. The facility expands Equinix’s footprint to meet growing demand for digital and AI-ready capacity in France.

Edge AI Expansion in Urban and Industrial Hubs for Real-Time Decision-Making and Data Localization

Edge data centers support latency-sensitive AI use cases such as autonomous vehicles, industrial IoT, and smart cities. France’s major metros deploy AI edge infrastructure for real-time processing. Demand rises for micro data centers embedded in telecom and urban networks. Enterprises adopt edge nodes to comply with data localization and reduce cloud latency. Use cases expand across transportation, healthcare diagnostics, and predictive maintenance. The France AI Data Center Market benefits from AI-adapted edge solutions integrated with 5G and fiber networks. Regional data hubs reduce backhaul and enable distributed inference. It enables decentralized AI applications in dynamic environments. Operators target 10–15 kW per rack in edge formats.

Market Trends

Rising AI Cluster Deployments in Tier III and Tier IV Facilities with Enhanced Interconnectivity

Operators are deploying AI compute zones within certified Tier III and Tier IV facilities to ensure uninterrupted services. These zones host dense clusters of GPUs, TPUs, and AI accelerators for model training. Inter-rack interconnects and low-latency fabrics are essential for distributed training performance. Network optimization through NVLink and 800G Ethernet links becomes standard. Interoperability between clusters and cloud enhances flexibility in resource allocation. The France AI Data Center Market sees rapid design changes to accommodate AI clusters. Enhanced security and data integrity frameworks are layered onto compute nodes. DCIM platforms are evolving to monitor high-performance AI zones. It makes advanced infrastructure accessible across AI stages.

Convergence of AI and Green Energy Goals to Drive Renewable-Powered AI Data Centers

AI infrastructure growth aligns with France’s renewable energy transition roadmap. Operators adopt wind and hydroelectric power purchasing agreements to supply AI clusters. Liquid cooling and energy reuse systems help reduce carbon footprints. AI optimization also improves workload scheduling and resource efficiency. Colocation providers are targeting PUE values below 1.2 in new builds. The France AI Data Center Market is aligning AI growth with ESG mandates. Hybrid cooling and AI workload orchestration reduce excess heat waste. Providers integrate AI-driven control systems to manage facility-level energy. It promotes AI deployment without exceeding sustainability thresholds.

Increased Integration of AI-Ready Racks with Modular and Scalable Architectures

Modular architecture adoption is rising across hyperscale and enterprise builds. Rack-level designs now integrate AI acceleration, liquid cooling, and orchestration software. AI-ready modules allow flexible scaling by power, compute, and thermal density. Enterprises demand rack formats that support future AI chip upgrades. Containerized data centers gain traction in research and edge AI deployments. The France AI Data Center Market supports AI-integrated modular solutions across urban and campus sites. Suppliers bundle GPUs, NVMe storage, and orchestration in plug-and-play formats. Rapid deployment supports AI project agility. It allows operators to meet shifting AI demands with minimal disruption.

Growing Presence of Cloud-to-Edge AI Platforms and Federated Learning Workflows

AI infrastructure expands beyond centralized data centers into edge nodes and federated environments. Federated learning enables model training on distributed datasets across hospitals, banks, and retail chains. France’s telecom providers support edge AI rollouts with dense fiber backbones. AI model deployment becomes location-sensitive, supporting real-time response. Cloud providers now offer hybrid AI environments with local inferencing. The France AI Data Center Market evolves toward integrated cloud-to-edge frameworks. AI containers operate across clusters, private clouds, and mobile nodes. Data gravity and privacy concerns drive local processing of AI pipelines. It brings compute closer to data sources across industries.

Market Challenges

Escalating Energy Constraints and Grid Pressure from High-Density AI Workloads Across Facilities

AI workloads require significant power draw, creating pressure on regional energy infrastructure. Dense GPU racks often exceed 30–50 kW per rack, demanding robust grid interconnects. Some regions face power allocation delays and capacity bottlenecks. High energy demand competes with industrial and residential priorities. Infrastructure upgrades lag behind hyperscale build timelines. The France AI Data Center Market faces difficulty balancing AI growth and grid resilience. Energy pricing volatility also affects long-term TCO planning. Renewable energy adoption helps, but availability remains uneven. It slows time-to-market for large-scale AI deployments.

Rising Regulatory Complexity Around Data Sovereignty and Cross-Border AI Workflows

Strict data protection laws and sovereignty frameworks add legal and operational complexity. AI models require access to large, often international, datasets. French laws limit cross-border processing of health and financial data. Compliance with SecNumCloud, GDPR, and HDS increases costs and infrastructure requirements. Vendors must isolate data zones and maintain audit-ready controls. The France AI Data Center Market must navigate evolving cybersecurity regulations. AI deployments in sensitive verticals face slow approvals. Regulatory overhead delays hyperscale cloud onboarding. It increases localization pressure on multinational AI providers.

Market Opportunities

Emergence of Sovereign AI Cloud Offerings for Regulated and Public Sector Clients in France

France’s focus on AI sovereignty opens opportunities for trusted cloud infrastructure. Operators offering certified environments for public workloads see long-term demand. Projects like Bleu and trusted zones create secure AI model deployment paths. The France AI Data Center Market benefits from growing demand for compliant, in-country compute. It drives innovation in secure hardware, orchestration, and policy-ready AI architectures.

AI-Driven Industry 4.0 and Smart City Programs to Boost Edge and Micro Data Center Deployments

Edge AI demand grows across logistics, automotive, healthcare, and city planning. Operators deploy micro data centers in smart grids and manufacturing hubs. New 5G zones support AI inferencing at the edge. The France AI Data Center Market captures growth from AI-integrated industrial sites. It positions edge providers to serve decentralized AI workloads.

Market Segmentation

By Type

Hyperscale facilities dominate the France AI Data Center Market due to their role in training large-scale AI models. Major cloud providers and tech firms invest in GPU-heavy campuses designed for scalability. These facilities account for the largest market share due to compute density and power availability. Colocation and enterprise data centers serve compliance-focused industries such as healthcare and finance. Edge and micro data centers are emerging across smart city and industrial deployments. Each segment addresses specific latency, security, or scalability needs.

By Component

Hardware holds the highest share of the France AI Data Center Market due to demand for AI chips, high-speed interconnects, and liquid-cooled racks. Enterprises and hyperscalers invest in custom infrastructure optimized for inferencing and model training. Software and orchestration tools enable efficient AI workload scheduling and DCIM integration. Services, including facility management, AI consulting, and maintenance, support long-term infrastructure use. The rise of AI workloads increases demand across all three components.

By Deployment

Hybrid deployment leads the France AI Data Center Market, offering flexibility between on-premise control and cloud scalability. Enterprises blend private AI clusters with public cloud training zones. On-premise deployment supports sensitive workloads requiring strict access controls and data locality. Cloud deployments grow fast for scalable AI development. Vendors offer sovereign cloud zones to meet regulatory needs. Each model aligns with unique risk, performance, and governance goals.

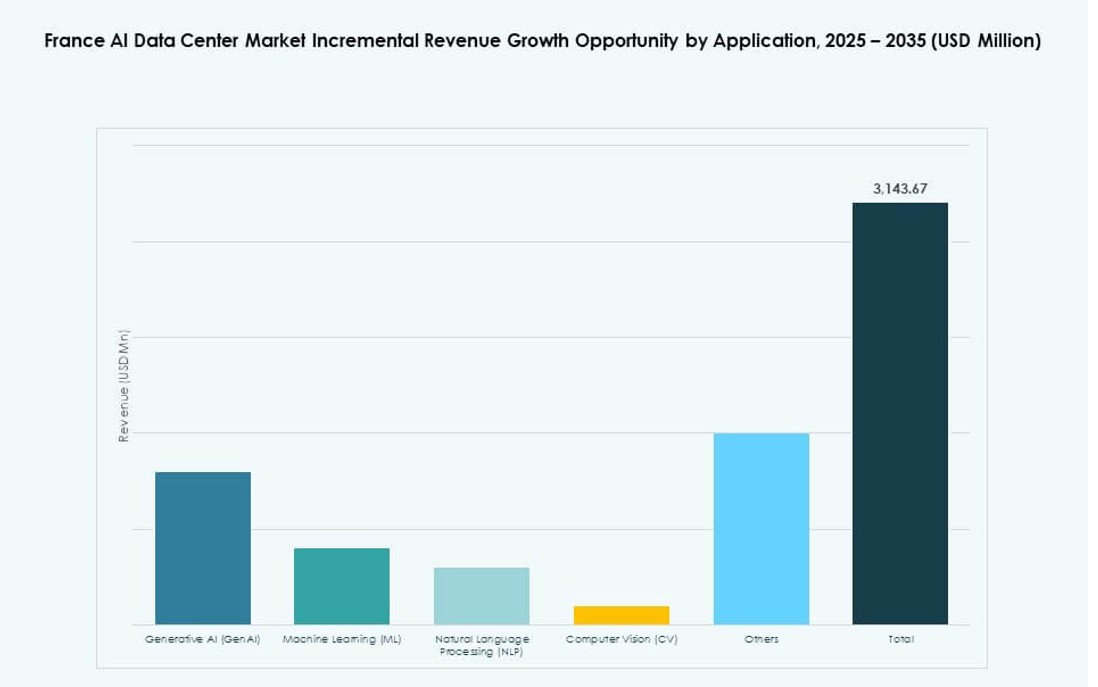

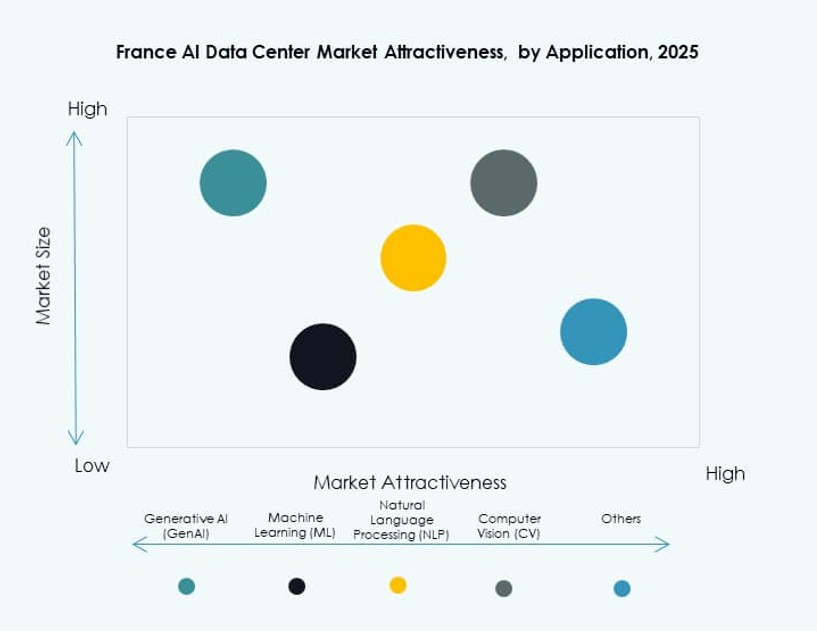

By Application

Machine Learning (ML) holds the largest application share in the France AI Data Center Market due to enterprise analytics and automation use cases. Generative AI (GenAI) adoption rises across media, legal, and customer service applications. Natural Language Processing (NLP) supports government translation, sentiment analysis, and voice recognition tools. Computer Vision (CV) gains traction in security, manufacturing, and medical diagnostics. Diverse use cases drive broad infrastructure adoption across verticals.

By Vertical

BFSI and Healthcare dominate vertical demand in the France AI Data Center Market due to high-security, high-performance AI needs. BFSI uses AI for fraud detection, customer segmentation, and risk scoring. Healthcare adopts AI for imaging, diagnostics, and patient management. Retail and IT sectors also scale AI workloads through edge and cloud nodes. Automotive and manufacturing see growth from Industry 4.0 and autonomous systems. Media, entertainment, and public services also expand AI use.

Regional Insights

Paris commands over 42% share of the France AI Data Center Market, led by dense enterprise clusters, government cloud zones, and R&D institutions. The region hosts major AI deployments from hyperscalers, sovereign cloud providers, and public sector IT departments. Its strong fiber backbone and access to skilled talent reinforce its position as the central hub. Paris data centers support AI training and inference workloads across multiple verticals. It remains the strategic core for investment and innovation.

- For instance, Microsoft invested €4 billion to expand Paris-area data centers, deploying 25,000 advanced GPUs by end of 2025 for AI training workloads.

Marseille holds around 26% of the France AI Data Center Market, acting as a key landing zone for submarine cables. Its international connectivity supports cross-border AI workflows and model deployment across Europe and North Africa. AI infrastructure here benefits from integration with energy grids and favorable power availability. The region is also growing in edge deployments targeting southern France and Mediterranean logistics corridors. It plays a vital role in decentralized and global AI pipelines.

- For instance, Orange landed the Medusa submarine cable system in Marseille, integrating with all city data centers across 17 cables for cross-border AI data flows.

Emerging cities such as Lyon, Bordeaux, and Lille account for nearly 32% share and are rapidly gaining traction for AI infrastructure. These regions offer lower land costs, expanding industrial zones, and targeted incentives for digital investment. Local governments support AI data center zones tied to universities and manufacturing hubs. They also attract edge providers seeking geographic diversity. The France AI Data Center Market benefits from this balanced expansion across core and regional markets. It ensures capacity distribution and resilience.

Competitive Insights:

- OVHcloud

- Iliad Data Centers

- DATA4

- Scaleway

- Microsoft (Azure)

- Amazon Web Services (AWS)

- Google Cloud (Alphabet)

- Meta Platforms

- Equinix

- Digital Realty Trust

The France AI Data Center Market is shaped by a mix of domestic and global players, each targeting high-density infrastructure for AI model workloads. OVHcloud and Iliad Data Centers lead in sovereign cloud offerings tailored for compliance-heavy sectors. DATA4 and Scaleway expand their AI-ready capacity across Paris and emerging metros. Hyperscalers like AWS, Azure, and Google Cloud invest in large-scale AI clusters with liquid cooling and high-power racks. Meta strengthens its presence with AI training campuses optimized for in-house models. Global colocation providers such as Equinix and Digital Realty Trust support hybrid deployments with scalable, network-rich facilities. It remains highly competitive with strong vertical alignment, sustainability focus, and modular infrastructure adoption.

Recent Developments:

- In September 2025, Mistral AI raised €1.7 billion in a major funding round led by ASML, with participation from existing investors including Bpifrance and NVIDIA. This capital infusion positions the company to scale its AI model and infrastructure capabilities, supporting broader AI compute workloads likely hosted on high‑performance data centers within France and Europe.

- In May 2025, MGX (UAE), Bpifrance (France), Mistral AI (France), and NVIDIA (USA) announced a joint venture to develop the Paris AI Campus, a 1.4 GW facility aimed at becoming Europe’s largest AI data center in the Paris region, with construction starting in 2026 and operations by 2028.