Executive summary:

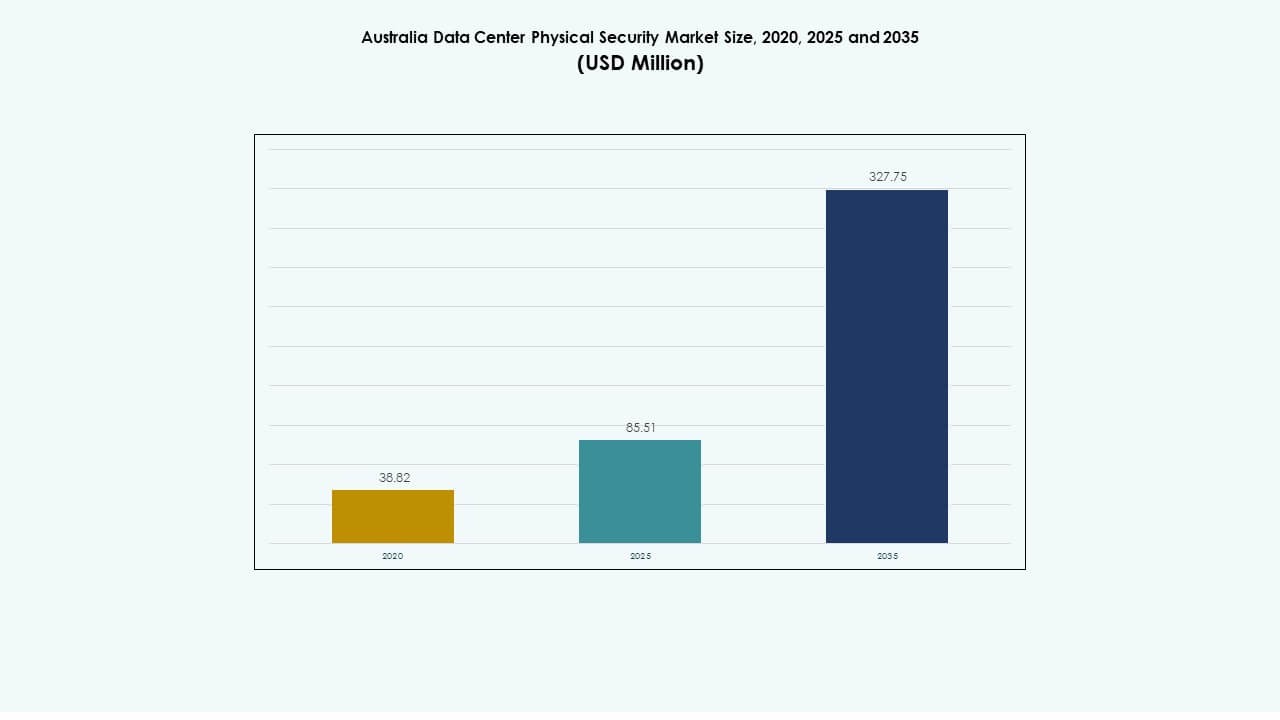

The Australia Data Center Physical Security Market size was valued at USD 38.82 million in 2020, reaching USD 85.51 million in 2025, and is anticipated to achieve USD 327.75 million by 2035, registering a CAGR of 14.29% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2035 |

| Australia Data Center Physical Security Market Size 2025 |

USD 85.51 Million |

| Australia Data Center Physical Security Market, CAGR |

14.29% |

| Australia Data Center Physical Security Market Size 2035 |

USD 327.75 Million |

Strong demand for advanced access control, surveillance, and monitoring technologies is driving growth in the Australia Data Center Physical Security Market. Rising investments in hyperscale and colocation facilities have accelerated the adoption of AI-enabled surveillance, biometric verification, and IoT-based control systems. It plays a crucial role in securing high-value digital infrastructure and ensuring regulatory compliance, making it strategically important for both domestic and international investors in the digital economy.

Geographically, New South Wales and Victoria lead the market due to concentrated data center ecosystems in Sydney and Melbourne. Western Australia and Queensland are emerging regions driven by renewable-powered data centers and cloud adoption. These areas benefit from rising infrastructure investments, strong connectivity, and growing interest from hyperscalers seeking sustainable and secure facilities to expand their Australian operations.

Market Drivers

Market Drivers

Growing Digital Transformation and Cloud Expansion

The Australia Data Center Physical Security Market is driven by rapid cloud adoption and digitalization across industries. Businesses rely on secure infrastructure to handle sensitive data, increasing the need for multi-layered protection. It benefits from strong demand for advanced surveillance and biometric systems to prevent breaches. Government and corporate compliance standards push organizations toward higher security benchmarks. Rising data center investments by hyperscalers reinforce the importance of robust physical security. Integration of AI and IoT devices improves threat detection and incident response. The market reflects a strong alignment between digital trust and infrastructure reliability. Investors see long-term value in expanding Australia’s secure data ecosystem.

Rising Implementation of Advanced Security Technologies

Technology integration drives the evolution of physical security systems in modern data centers. AI-based facial recognition, video analytics, and automated access control improve efficiency and accuracy. The Australia Data Center Physical Security Market benefits from real-time monitoring enabled by edge computing. Cloud-based command centers enhance decision-making and reduce operational risk. It supports seamless coordination between hardware and software security tools. Businesses adopt predictive maintenance and sensor analytics to prevent downtime. Security management platforms now unify various systems for greater visibility. The market’s innovation pace reflects Australia’s readiness for smart and self-regulating facilities.

Regulatory Push and Cyber-Physical Convergence

Strict compliance with national cybersecurity and data protection laws shapes market direction. Operators must ensure that physical and digital systems work together for seamless protection. The Australia Data Center Physical Security Market sees growth from increased government monitoring of data infrastructure. Integration of physical security with cybersecurity frameworks creates unified resilience strategies. It encourages investments in certified and compliant technologies. Vendors focus on providing end-to-end solutions meeting ISO 27001 and ASD standards. This convergence helps address complex threats while ensuring operational continuity. Businesses find these systems vital for regulatory alignment and investor trust.

- For example, Equinix in Australia holds ISO/IEC 27001 certification and has achieved Certified Strategic status under the Australian Government Hosting Certification Framework (HCF). Its data centers implement integrated cyber and physical security controls to meet national compliance and data sovereignty requirements.

Rising Investments from Global and Local Players

Global data center operators expand Australian facilities to meet rising cloud service demand. Companies such as Equinix, NEXTDC, and Digital Realty invest heavily in secure data hubs. The Australia Data Center Physical Security Market gains momentum from these expansions. It stimulates demand for smart access systems, motion sensors, and AI-enabled cameras. Investors prioritize physical security as a core requirement for asset protection. Partnerships between local security firms and global technology providers strengthen supply chains. Market players emphasize innovation through integrated and automated defense mechanisms. These initiatives position Australia as a regional benchmark in secure digital infrastructure.

- For example, NEXTDC operates over 12 data centers across Australia, featuring biometric access controls, high-definition CCTV surveillance, and 24/7 Security Operations Centers. The company partners with Gunnebo for secure man-trap entry systems and Genetec for integrated security management platforms to ensure multi-layered protection across its facilities.

Market Trends

Market Trends

AI-Enabled Surveillance and Automation Rise

Artificial intelligence transforms traditional security models through predictive surveillance and smart analytics. The Australia Data Center Physical Security Market experiences increased adoption of AI-based tools for incident prevention. Machine learning helps identify anomalies in real time, improving situational awareness. Automated control systems minimize manual intervention and operational delays. Edge analytics enhance local decision-making near data sources. Businesses implement intelligent video analytics for crowd management and perimeter protection. It reflects a shift toward self-learning systems capable of adapting to evolving threats. The trend promotes data-driven security across hyperscale and colocation centers.

Growing Preference for Integrated Security Platforms

Operators prefer unified security systems that connect cameras, sensors, and access points under one interface. The Australia Data Center Physical Security Market benefits from seamless management offered by integrated control solutions. These platforms reduce complexity and improve response coordination. Real-time dashboards enable instant alerts and predictive analysis. Organizations deploy centralized monitoring to oversee multi-location operations efficiently. Integration reduces hardware dependency and simplifies compliance management. It also strengthens collaboration between IT and facility teams. The shift ensures continuous visibility and enhances data center uptime.

Sustainability and Green Security Infrastructure

Sustainability goals drive design choices across modern facilities. The Australia Data Center Physical Security Market adopts energy-efficient hardware and low-emission systems. Green-certified buildings integrate solar-powered surveillance and smart cooling. Eco-friendly security systems reduce energy usage without compromising reliability. Vendors develop recyclable and modular solutions that support carbon neutrality. It aligns physical security with broader ESG strategies. Data center operators invest in digital twins to optimize power management. These developments showcase security innovation compatible with environmental priorities.

Adoption of Edge and Remote Management Technologies

Decentralized data infrastructure increases demand for edge security management. The Australia Data Center Physical Security Market witnesses rising deployment of remote-controlled systems. Edge computing allows local processing of surveillance data with reduced latency. Remote control rooms manage dispersed facilities using cloud-based networks. It enhances reliability across secondary cities like Perth and Brisbane. Organizations adopt 5G-enabled devices to support real-time video transmission. This distributed model reduces risks from centralized failures. The shift signifies a scalable approach to securing Australia’s expanding digital landscape.

Market Challenges

Market Challenges

High Implementation and Maintenance Costs

The Australia Data Center Physical Security Market faces cost barriers linked to advanced technology deployment. Installation of AI-based surveillance and biometric systems requires significant investment. Small and mid-tier operators struggle with capital-intensive infrastructure upgrades. Maintenance of integrated networks adds recurring expenses. It also demands skilled professionals for real-time monitoring and repair. Supply chain delays in specialized hardware increase operational risks. Market fragmentation leads to inconsistent system interoperability. Cost concerns limit adoption among smaller enterprises and regional players.

Complex Threat Landscape and Compliance Burdens

Evolving security risks challenge data center operators in maintaining constant protection. The Australia Data Center Physical Security Market encounters issues balancing innovation with compliance. Frequent changes in data protection laws create administrative strain. Integrating physical and cyber controls under one framework remains difficult. It requires continuous software updates and multi-layer testing. Dependence on legacy systems slows migration to modern security platforms. Cyber-physical attacks exploit weak points between access and network systems. These factors elevate operational pressure and slow long-term implementation cycles.

Market Opportunities

Expansion of Hyperscale and Colocation Facilities

New hyperscale developments create vast demand for multi-layered protection solutions. The Australia Data Center Physical Security Market benefits from the growth of large-scale facilities across major cities. It opens opportunities for security vendors specializing in integrated access and surveillance. Government initiatives encouraging digital infrastructure investments further expand adoption. Partnerships with global tech firms enhance solution availability. Operators seek predictive and automated protection tools for enhanced safety. Increasing need for modular security systems supports market scalability. These conditions enable consistent revenue growth and innovation.

Emergence of Smart Data Centers and AI Adoption

Smart facilities utilize AI and IoT to monitor threats with precision and speed. The Australia Data Center Physical Security Market experiences rising interest in intelligent, self-adaptive systems. Integration of predictive analytics with biometric access tools improves performance. It creates new business avenues for software developers and integrators. Growth in 5G and edge computing supports remote and automated surveillance. Investors prioritize vendors offering flexible, scalable systems. These opportunities strengthen Australia’s role as a secure digital hub. Market players leveraging AI-driven solutions will gain a strong competitive advantage.

Market Segmentation

By Data Center Size

Large data centers dominate due to heavy investment from hyperscalers and colocation providers. The Australia Data Center Physical Security Market sees medium and small centers expanding for edge applications. Large centers adopt layered systems integrating perimeter, building, and rack-level protection. High demand for redundancy drives adoption of advanced monitoring tools. Smaller facilities focus on modular solutions for cost efficiency. The segment’s scalability ensures wider accessibility. Increasing capacity in metro regions boosts growth for all facility sizes. Data center scale strongly influences solution complexity and vendor partnerships.

By Component

Solutions hold the largest market share, driven by demand for surveillance and access technologies. The Australia Data Center Physical Security Market sees rising service adoption for integration and support. Solutions include video monitoring, biometric systems, and alarm control. Service providers enhance reliability through continuous updates and risk audits. Enterprises prefer hybrid models combining on-premise and cloud solutions. Integration of AI software improves device interoperability. Service partnerships with OEMs ensure system optimization. This balanced component mix strengthens operational performance and uptime.

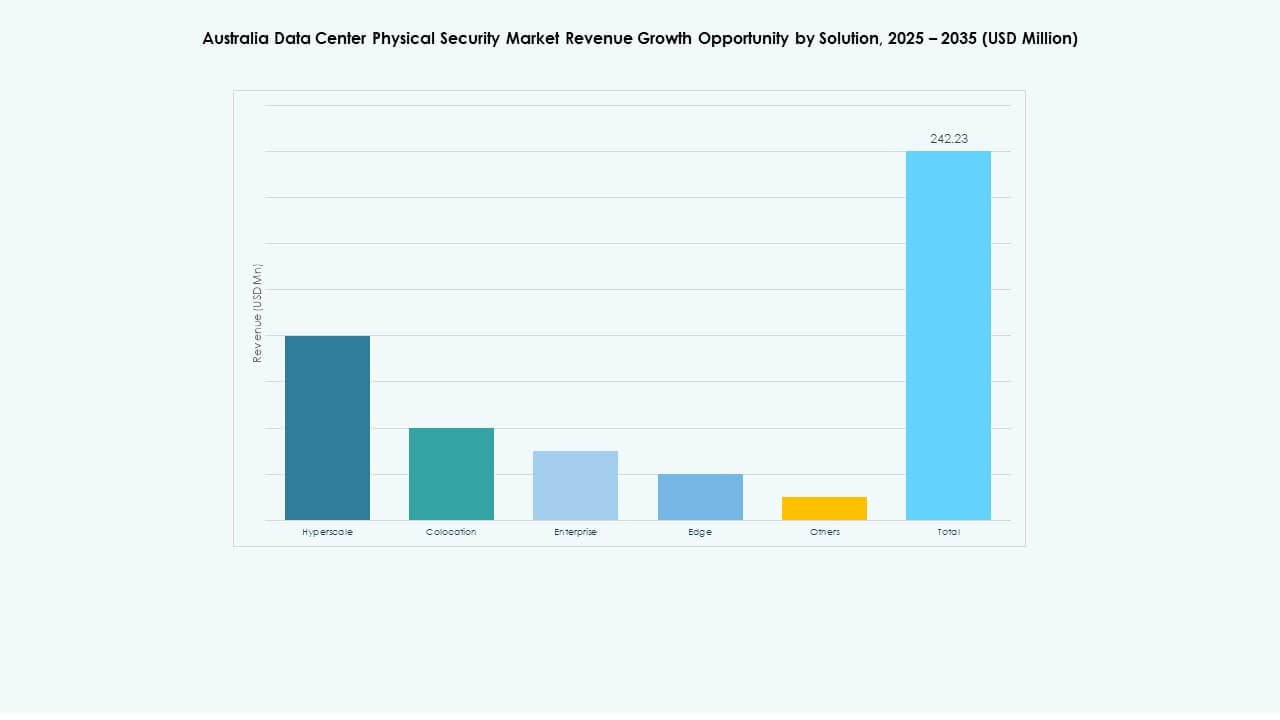

By Solution

Access control leads the solution category due to the need for regulated facility entry. The Australia Data Center Physical Security Market also records strong use of video surveillance and monitoring systems. AI analytics strengthen these solutions by improving identification accuracy. Real-time alerts prevent unauthorized access and equipment tampering. Advanced sensors and motion detectors secure critical areas. Enterprises invest in unified software dashboards for system oversight. Demand for cloud-based platforms improves scalability. These solutions collectively enhance end-to-end infrastructure defense.

By Services

System integration dominates due to complex multi-vendor environments. The Australia Data Center Physical Security Market shows increasing demand for consulting and maintenance support. Integration ensures seamless functioning of diverse devices and software. Consulting services help align strategies with compliance standards. Maintenance contracts sustain performance and reduce downtime. End-users prioritize vendors offering full-lifecycle management. Service quality becomes a competitive differentiator in high-availability facilities. These services ensure consistent reliability in rapidly expanding infrastructures.

By Security Layer

Perimeter security forms the foundation for all protection systems. The Australia Data Center Physical Security Market emphasizes layered defense extending to building and rack levels. Access control at each layer ensures comprehensive coverage. Data halls use biometric locks and surveillance cameras for constant monitoring. Rack-level sensors prevent tampering or theft of hardware. Integration between layers enhances situational awareness. Facility operators deploy automated systems for faster response. This multi-layer approach underpins long-term resilience and compliance.

By Data Center Type

Hyperscale data centers dominate with significant investment in high-density infrastructure. The Australia Data Center Physical Security Market sees growth in colocation and enterprise facilities. Edge data centers expand with rising IoT and AI workloads. It benefits from scalable and decentralized security solutions. Colocation sites demand strict access policies due to shared environments. Enterprise facilities focus on integrated systems for internal compliance. These varied types support a balanced market ecosystem. Ongoing expansion ensures sustained opportunities across all categories.

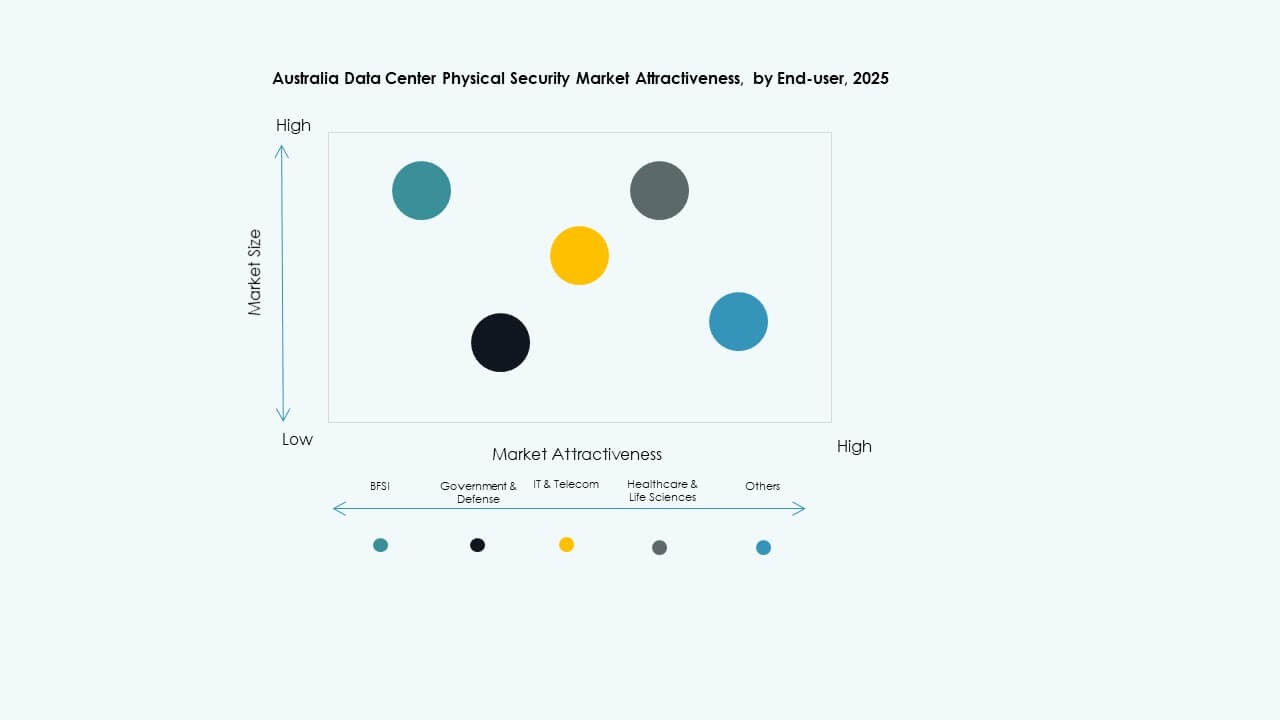

By End-User

IT and telecom lead due to their dependence on secure digital environments. The Australia Data Center Physical Security Market also finds strong participation from BFSI and government sectors. Healthcare and retail sectors adopt these solutions to meet regulatory standards. Manufacturing facilities integrate systems for equipment and data protection. E-commerce platforms demand 24/7 surveillance for logistics centers. End-users value AI automation for operational control. Each sector aligns with customized security needs. Broader adoption across industries ensures diversified market growth.

Regional Insights

New South Wales and Victoria: Core Data Center Hubs

New South Wales holds about 45% of the Australia Data Center Physical Security Market, led by Sydney’s hyperscale dominance. Victoria follows with nearly 30%, driven by major developments in Melbourne. These states attract top-tier investments from global players. Their advanced connectivity and regulatory frameworks support robust security integration. It benefits from government-backed sustainability initiatives. Strong cloud adoption across enterprises accelerates facility expansion. Both regions represent the strategic heart of Australia’s secure data infrastructure.

- For example, NEXTDC operates the S2 Sydney data center, which holds Uptime Institute Tier IV certification for both design and constructed facility. The site features fault-tolerant power and cooling infrastructure with biometric access controls and advanced surveillance, ensuring high operational reliability and secure performance.

Western Australia and Queensland: Emerging Growth Corridors

Western Australia captures roughly 15% market share, supported by new energy-efficient centers. Queensland holds close to 7%, expanding with regional digital hubs. The Australia Data Center Physical Security Market grows here through edge computing and renewable projects. Investments target coastal and mining-linked locations for resilience. Smart monitoring tools improve safety across distributed operations. Local governments promote data infrastructure for regional economic development. These areas show rising importance in national data security networks.

- For instance, CDC Data Centres has announced the development of a 200MW data center campus near Perth, Western Australia, utilizing advanced closed-loop liquid cooling systems that consume zero water in the cooling process. This is considered one of the largest AI and technology campuses in the region, aligning with energy-efficiency and environmental sustainability goals.

South Australia and Tasmania: Niche but Strategic Regions

South Australia and Tasmania together account for about 3% of the market. The Australia Data Center Physical Security Market sees gradual expansion driven by green and modular facility projects. Both regions host specialized centers for defense and research data. Operators invest in renewable-backed systems with minimal emissions. It benefits from collaborations with universities and technology institutes. Secure infrastructure enhances local digital ecosystems. Their niche positioning supports future diversification and redundancy for national data infrastructure.

Competitive Insights:

Competitive Insights:

- Wilson Security

- SIS Australia Holdings Pty Ltd

- MSS Security

- API Access & Security

- ISCS (International Security Control Solutions Pty Ltd)

- ABB Ltd

- Siemens AG

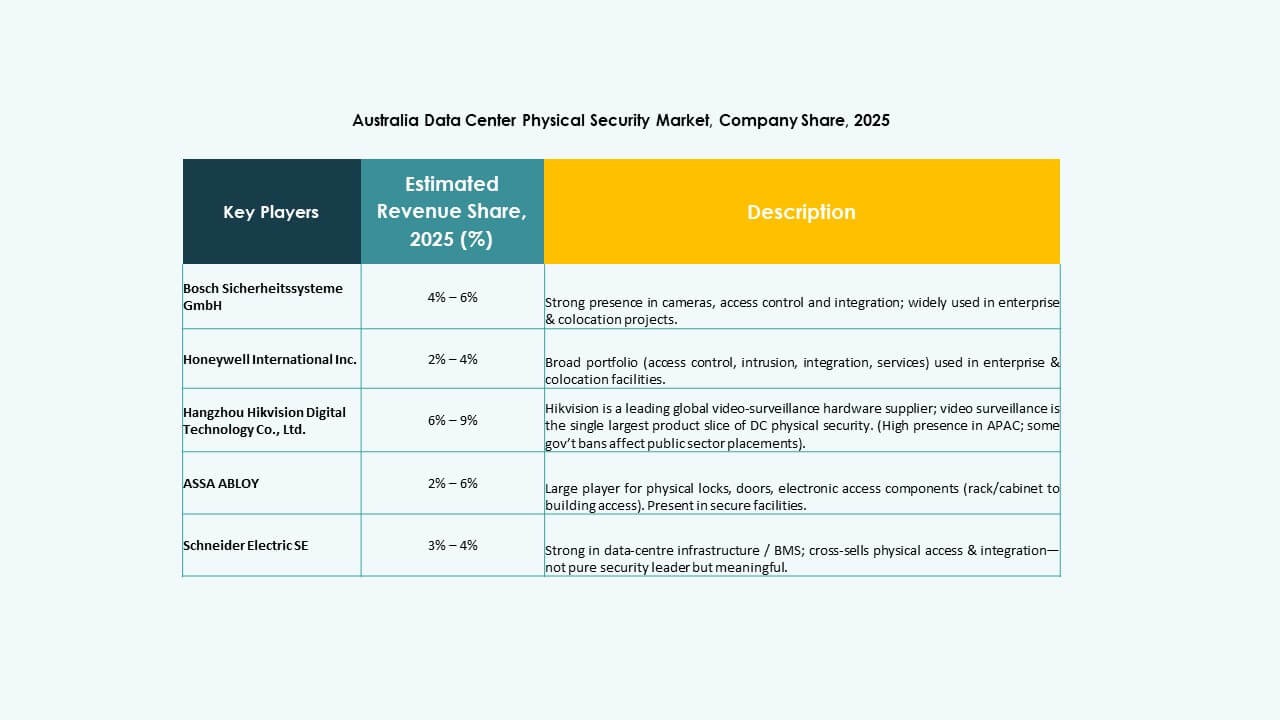

- Bosch Sicherheitssysteme GmbH

- Honeywell International Inc.

- Johnson Controls

The Australia Data Center Physical Security Market features strong competition between global technology vendors and domestic service providers. It is shaped by companies offering integrated access control, video surveillance, and monitoring solutions tailored to large-scale data centers. Global players such as Siemens, Bosch, and Honeywell dominate through advanced AI-enabled systems, while local firms like Wilson Security and MSS Security excel in on-ground operations and managed services. ABB and Johnson Controls focus on energy-efficient and automated security systems. Service integration, compliance with government cybersecurity mandates, and scalability define competitive success. Vendors emphasize partnerships and digital innovation to enhance performance, reduce downtime, and meet sustainability goals, strengthening their foothold across hyperscale and enterprise facilities in Australia.

Recent Developments:

- In October 2025, ASSA ABLOY acquired Kentix GmbH, a German company specializing in monitoring and access control products designed for data centers, enhancing their capabilities in physical security for this sector.

- In January 2025, ASSA ABLOY also acquired InVue, a Charlotte-based provider of asset protection and access control solutions, aligning with their strategy to expand globally in access control and asset protection.

- In June 2024, Honeywell International Inc. completed the acquisition of Carrier Global Corporation’s Global Access Solutions business for $4.95 billion, enhancing its building automation portfolio with advanced access control solutions like LenelS2, Onity, and Supra, which support security needs in data centers including those in Spain.

- In December 2024, Bosch Sicherheitssysteme GmbH sold its security and communications technology product business to the European investment firm Triton. The transaction included three business units Video, Access and Intrusion, and Communication as Bosch aims to focus more on systems integration business.