Executive summary:

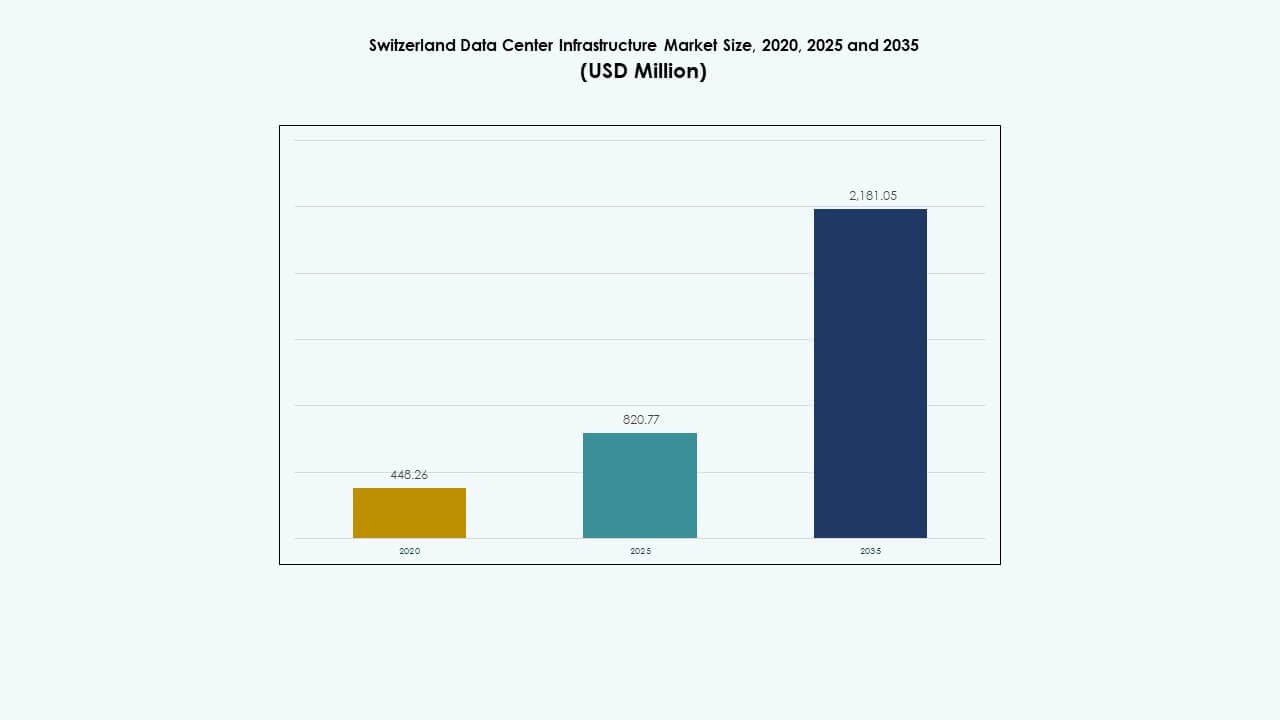

The Switzerland Data Center Infrastructure Market size was valued at USD 448.26 million in 2020, increased to USD 820.77 million in 2025, and is anticipated to reach USD 2,181.05 million by 2035, at a CAGR of 10.20% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2035 |

| Switzerland Data Center Infrastructure Market Size 2025 |

USD 820.77 Million |

| Switzerland Data Center Infrastructure Market, CAGR |

10.20% |

| Switzerland Data Center Infrastructure Market Size 2035 |

USD 2,181.05 Million |

The market is driven by rising demand for cloud and hybrid infrastructure, advanced computing workloads, and sustainable power solutions. Operators focus on AI, automation, and liquid cooling to manage growing density and improve energy performance. Strong compliance with privacy regulations attracts enterprise and financial clients. The Switzerland Data Center Infrastructure Market remains strategically important for investors seeking stable, high-return assets within Europe’s digital transformation landscape.

Zurich and Geneva lead market activity due to their high network density, renewable power access, and presence of hyperscale operators. These regions form the country’s primary data exchange hubs supporting financial services, AI, and research sectors. Emerging zones in Central and Western Switzerland attract edge deployments and modular data centers. Strong connectivity with Germany, France, and Italy enhances cross-border cloud operations, reinforcing Switzerland’s role as a secure European digital hub.

Market Drivers

Rising Investments in Sustainable and Energy-Efficient Data Centers

The Switzerland Data Center Infrastructure Market expands through high investment in low-carbon infrastructure and renewable power. Operators use hydroelectric and solar energy to achieve strict sustainability goals. Enterprises move workloads to facilities with low Power Usage Effectiveness (PUE) levels. The shift supports green data policies aligned with EU standards. Investors view renewable-powered centers as low-risk, long-term assets. Energy-efficient hardware, cooling, and UPS systems gain strong traction. The focus on decarbonization raises foreign investor confidence. It benefits both domestic and international operators planning long-term digital expansion.

- For example, CERN’s Prévessin data center targets a PUE of 1.1, below the global average of 1.6, via water recycling and advanced cooling across its 6,000 sqm facility with 12 MW total capacity and 2 MW cooling per room.

Adoption of Cloud, AI, and HPC Workloads Driving Infrastructure Upgrades

The market benefits from strong demand for hybrid cloud, artificial intelligence (AI), and high-performance computing (HPC). Enterprises modernize IT infrastructure to handle growing data volumes. AI and financial analytics workloads push operators to expand GPU clusters and edge computing. Colocation providers deploy new fiber routes to handle latency-sensitive workloads. AI training clusters drive liquid cooling adoption. It strengthens Switzerland’s role as a regional data hub. Demand from fintech and life sciences drives strong connectivity needs. The market’s maturity attracts global hyperscalers seeking reliable power and governance.

- For instance, Microsoft announced a USD 400 million investment in June 2025 to expand its Swiss data center footprint across Zurich and Geneva, aimed at strengthening AI and cloud infrastructure. The initiative focuses on supporting regulated industries and sustainability goals, reinforcing Switzerland’s position as a key European digital and innovation hub.

Government Policies and Data Privacy Framework Enhancing Market Confidence

Strict national privacy laws strengthen confidence among foreign and local clients. The Swiss Federal Act on Data Protection (FADP) ensures compliance with international standards. Global enterprises choose Swiss facilities for handling sensitive data. It builds the country’s reputation as a secure hosting environment. Cross-border data exchange is supported by clear regulatory rules. Businesses in banking, biotech, and logistics trust Swiss locations for mission-critical storage. Stable governance and favorable tax policies sustain investor interest. The focus on transparency and accountability supports ongoing infrastructure modernization.

Strong Connectivity Ecosystem and Strategic European Position

Switzerland benefits from a robust fiber and subsea network linking it with Germany, France, and Italy. Its geographic position supports regional cloud interconnection and disaster recovery. It strengthens international enterprise access to low-latency routes. Major telecoms invest in 400G backbone networks across Zurich and Geneva. The infrastructure supports consistent service-level reliability. Data centers near border zones benefit from renewable energy corridors. The market’s geographic neutrality attracts cross-border digital trade. It remains a gateway for both Western and Central European digital operations.

Market Trends

Market Trends

Rapid Growth in Hyperscale and Edge Deployments Across Major Hubs

The Switzerland Data Center Infrastructure Market witnesses expansion in hyperscale and edge deployments. Zurich and Geneva dominate with hyperscale clusters catering to cloud and AI firms. Edge data centers emerge near industrial corridors to serve latency-sensitive workloads. It ensures smoother digital services for real-time applications. Telecom operators enhance 5G and edge interconnectivity zones. Hyperscale facilities use modular designs for scalability. Enterprises invest in distributed nodes to optimize workload distribution. The trend supports flexible hybrid and multi-cloud models.

Integration of Liquid Cooling and AI-Based Thermal Optimization Systems

Operators deploy liquid cooling and AI-driven management systems to maintain optimal energy performance. Facilities adopt immersion cooling for GPU clusters and dense rack environments. AI analytics help track thermal efficiency and predict maintenance schedules. It improves energy utilization and lowers total cost of ownership. Colocation facilities use predictive cooling models for workload balancing. The transition to smarter systems enhances operational uptime. Adoption of digital twin technology helps simulate infrastructure performance. This trend strengthens innovation leadership within Swiss data operations.

Growing Demand for Modular and Prefabricated Construction Models

Demand for modular data center construction rises due to time and cost efficiency. The Switzerland Data Center Infrastructure Market shifts toward factory-built modules for faster deployment. Modular systems allow scalability based on client demand. Construction firms collaborate with IT integrators to deliver preassembled solutions. Prefabricated units reduce land use and enhance sustainability. The approach suits remote or restricted locations with power constraints. It simplifies permitting and speeds up project execution. The strategy aligns with investor preferences for lower-risk, scalable assets.

Expansion of Renewable Energy Integration in Facility Design

Operators focus on integrating on-site renewable generation into new campuses. Hydropower and solar contribute significantly to total capacity. Smart microgrids stabilize power and reduce emissions. It aligns with corporate sustainability reporting frameworks. Data centers design energy storage systems to manage power peaks. Partnerships with local utilities strengthen green infrastructure development. Power purchase agreements (PPAs) ensure predictable long-term supply. The trend enhances Switzerland’s leadership in sustainable digital infrastructure.

Market Challenges

Market Challenges

High Construction Costs and Limited Land Availability in Urban Hubs

The Switzerland Data Center Infrastructure Market faces constraints from high real estate costs in Zurich and Geneva. Limited land availability slows hyperscale expansion. Construction materials and labor costs remain among the highest in Europe. Operators compete for industrial plots with access to cooling water and grid connections. It increases barriers for new entrants and smaller providers. The reliance on local permitting frameworks delays timelines. Investors face higher capital intensity compared to neighboring markets. Balancing sustainability and cost efficiency becomes a key challenge.

Energy Supply Constraints and Cooling Efficiency Pressure

Energy-intensive workloads strain regional power grids. Cooling systems require optimization to maintain low PUE values during high-density operations. Seasonal temperature variations affect energy performance. It drives demand for advanced heat reuse and free-air cooling solutions. Regulatory pressure to maintain carbon neutrality adds cost challenges. Operators must integrate battery storage and renewable sources to stabilize loads. Power redundancy requirements increase investment burden. Grid congestion risks affect new build feasibility. The industry must balance sustainability with operational reliability.

Market Opportunities

Rising Investments in AI Infrastructure and GPU Data Clusters

The Switzerland Data Center Infrastructure Market offers strong growth potential through AI and HPC deployments. AI training and simulation workloads drive GPU cluster installations. It attracts hyperscalers expanding AI-focused capacity across major hubs. Partnerships between telecoms and IT integrators create new colocation models. Financial services, healthcare, and research sectors boost high-performance computing use. Low-latency fiber routes support AI model training pipelines. Investors prioritize AI-ready campuses with renewable power availability.

Expansion of Cross-Border Connectivity and Digital Sovereignty Projects

Strong opportunities emerge through cross-border interconnectivity projects linking Switzerland with EU nations. Data centers form part of regional digital sovereignty networks. It supports compliance with both EU and Swiss data frameworks. Telecom firms expand 400G backbone capacity to meet traffic growth. Edge data centers near borders handle real-time industrial workloads. Regional collaborations strengthen redundancy and load balancing. The focus on sovereign data hosting positions Switzerland as a trusted European digital hub.

Market Segmentation

By Infrastructure Type

Electrical infrastructure dominates due to strong focus on reliable power systems and renewable integration. Mechanical infrastructure grows through advanced cooling and modular system demand. IT and network infrastructure gain traction with AI and cloud expansion. Civil and structural investments ensure seismic and climate resilience. The Switzerland Data Center Infrastructure Market sees high modernization spending across all segments, with IT infrastructure leading in revenue share due to fast technology refresh cycles.

By Electrical Infrastructure

UPS systems and power distribution units form the largest share. Operators focus on redundancy and energy efficiency. Battery Energy Storage Systems (BESS) adoption rises for peak load management. Transfer switches and switchgears enhance stability during grid interruptions. It ensures 24/7 reliability for mission-critical applications. Renewable grid connections gain momentum in major cities. Electrical upgrades remain central to sustainable growth plans.

By Mechanical Infrastructure

Cooling units and chillers dominate due to high-density workloads. Containment systems reduce heat leakage and improve airflow. Pumps and piping upgrades optimize water use in closed-loop systems. It strengthens operational reliability during power peaks. Operators deploy liquid and immersion cooling for AI and HPC workloads. Smart thermal control enhances uptime. Mechanical infrastructure modernization stays essential for long-term efficiency.

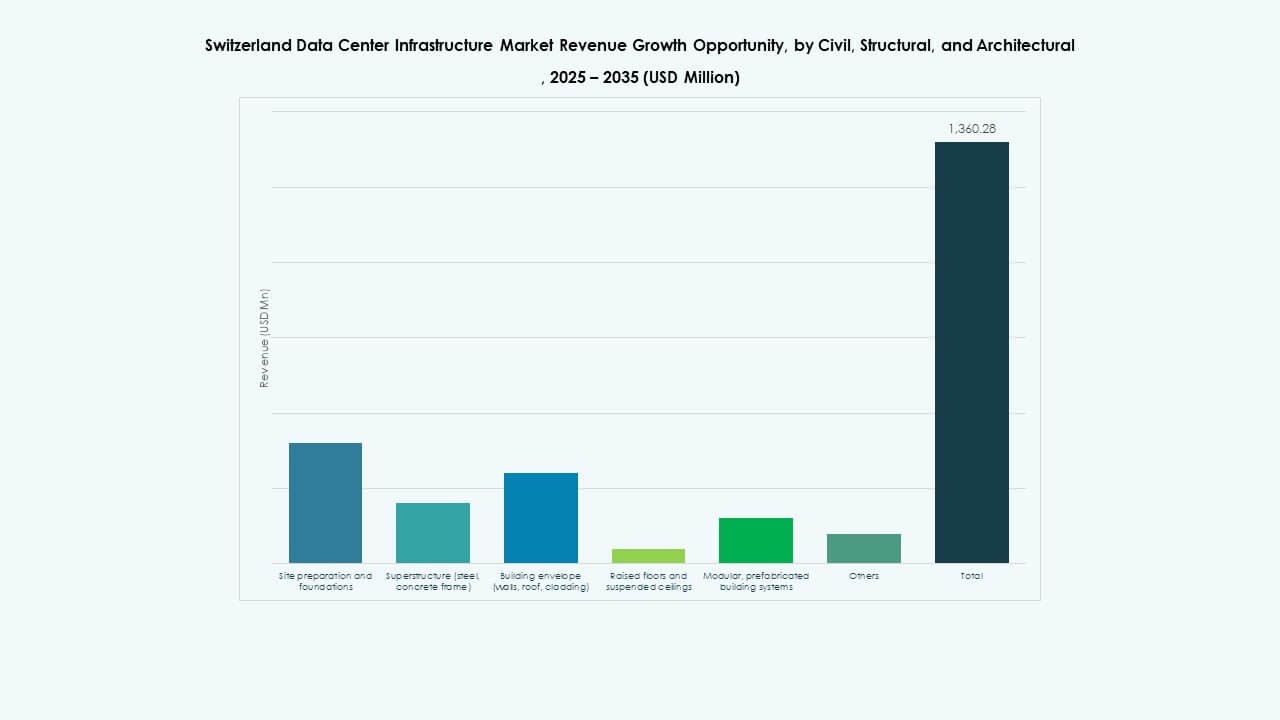

By Civil / Structural & Architectural

Civil and structural components ensure facility durability. Modular and prefabricated designs speed up construction timelines. Strong building envelopes reduce temperature variation and improve energy use. Raised floors support airflow management in dense racks. Seismic safety compliance remains a priority. It boosts investor confidence in long-term asset integrity. The market focuses on durable, adaptable structures for sustainability.

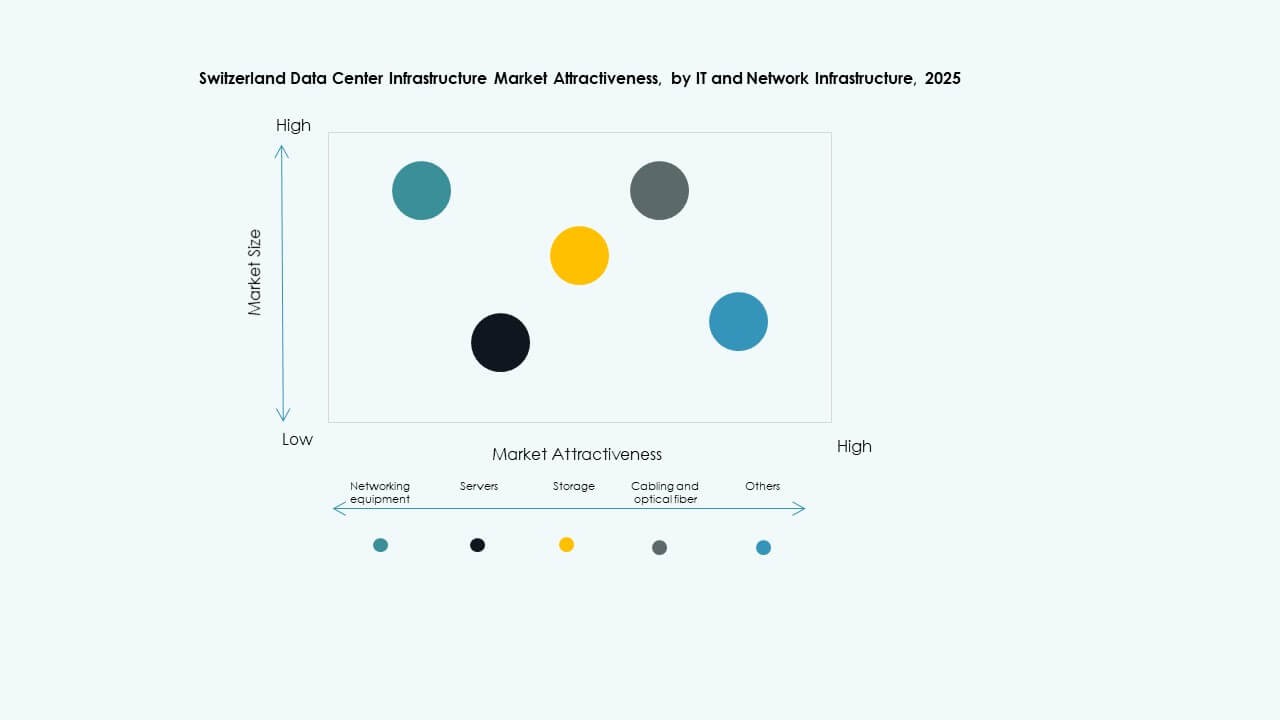

By IT & Network Infrastructure

Servers, networking gear, and storage systems form the foundation of digital operations. Cabling and optical fiber upgrades support multi-terabit speeds. Racks and enclosures adapt to high-density layouts. It drives modernization in existing data centers. Demand for next-generation servers supporting AI acceleration rises. Network automation strengthens interconnection reliability. IT and network upgrades remain the most dynamic segment by spending.

By Data Center Type

Hyperscale centers dominate due to high demand from cloud and AI providers. Colocation facilities expand for enterprise and hybrid deployments. Edge data centers grow near telecom and industrial corridors. Enterprise centers remain vital for secure, in-country operations. The Switzerland Data Center Infrastructure Market benefits from balance between hyperscale innovation and localized edge growth.

By Delivery Model

Design-build and turnkey projects dominate due to time-sensitive deployment needs. Retrofit and modular factory-built models gain pace for flexible upgrades. Construction management ensures quality control for complex multi-phase builds. It strengthens collaboration between operators and EPC contractors. The delivery model landscape supports scalability and faster project execution.

By Tier Type

Tier 3 facilities lead due to balance between reliability and cost efficiency. Tier 4 expansion grows among hyperscale providers requiring maximum uptime. Tier 1 and 2 sites serve regional or edge applications. The market aligns with global Uptime Institute standards. It emphasizes redundancy and energy efficiency to meet enterprise expectations.

Regional Insights

Regional Insights

Zurich and Geneva – Core High-Density Hubs with 58% Market Share

Zurich and Geneva dominate the Switzerland Data Center Infrastructure Market with combined 58% share. Both cities host hyperscale and colocation campuses. Strong grid reliability and connectivity make them preferred by international firms. Financial institutions drive high-density data requirements. It benefits from redundant power networks and renewable access. These regions remain central to cross-border digital and cloud services.

- For instance, Green, a leading Swiss data center operator, began construction on its fourth facility at the Metro-Campus Zurich West in Lupfig near Zurich. The site spans about 5,525 m² with a planned IT capacity of 12 MW and is scheduled to open in 2026, supporting Switzerland’s growing demand for high-efficiency and sustainable digital infrastructure.

Central and Western Switzerland – Emerging Zones with 27% Market Share

Central and Western regions attract mid-size colocation and enterprise projects. Lower land costs support edge and modular builds. Energy availability from hydro sources supports expansion. It experiences investment in data exchange points for regional firms. Proximity to logistics corridors enhances infrastructure reliability. These areas contribute 27% of the total share.

- For instance, NorthC Group plans a new data center at the uptownBasel campus in Arlesheim, offering 2,500 m² of space and 5.5 MW usable capacity, powered entirely by renewable energy and designed for AI, med-tech, and future-oriented workloads.

Eastern and Southern Switzerland – Growing Edge and Regional Networks with 15% Share

Eastern and Southern areas, including Ticino and Graubünden, expand edge and disaster recovery sites. Lower costs and renewable access attract smaller operators. It supports digital manufacturing and AI research workloads. Telecoms strengthen cross-border fiber into Italy and Austria. The zones contribute nearly 15% of the market share. Growth focuses on regional interconnection and hybrid deployments.

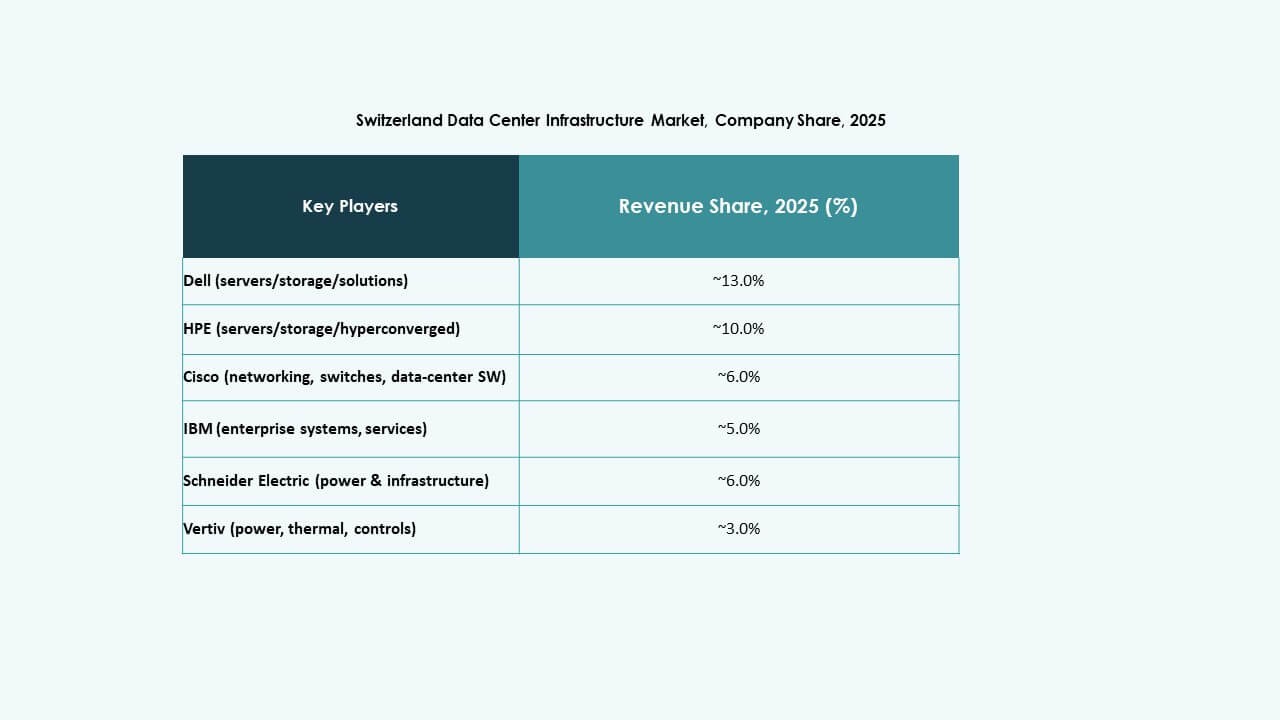

Competitive Insights:

- ABB Ltd.

- Schneider Electric SE

- Dell, Inc.

- Vertiv Group Corp.

- Cisco Systems, Inc.

- Fujitsu Ltd.

- Huawei Technologies Co., Ltd.

- Digital Realty Trust, Inc.

- Equinix, Inc.

- IBM Corp.

The Switzerland Data Center Infrastructure Market draws competition among global leaders with diverse strengths. ABB and Schneider Electric lead in power distribution, UPS, and electrification solutions. Dell, Vertiv, Cisco and Fujitsu focus on modular infrastructure, servers, cooling and network equipment. Huawei delivers integrated ICT and power solutions that appeal to large-scale operators. Digital Realty and Equinix drive demand via colocation and hyperscale data-center development. IBM supports enterprise clients with IT and storage systems. Market players compete on reliability, energy efficiency, scalability and regulatory compliance. Firms that combine strong power infrastructure, modular build-out, and scalable IT stacks hold a strategic edge. Investors view these firms as stable supply partners for long-term data center growth.

Recent Developments:

- In October 2025, IFM Investors acquired Swiss digital infrastructure firm Green Group AG from French private equity firm InfraVia, marking a significant expansion in Europe’s data center investments through the IFM Global Infrastructure Fund, with the deal expected to close later that year.

- In January 2025, Infomaniak achieved a milestone at its Geneva data center by recovering 100% of electricity for district heating, serving 6,000 households at just 25% server capacity, underscoring sustainability efforts in Switzerland’s data center infrastructure.