Executive summary:

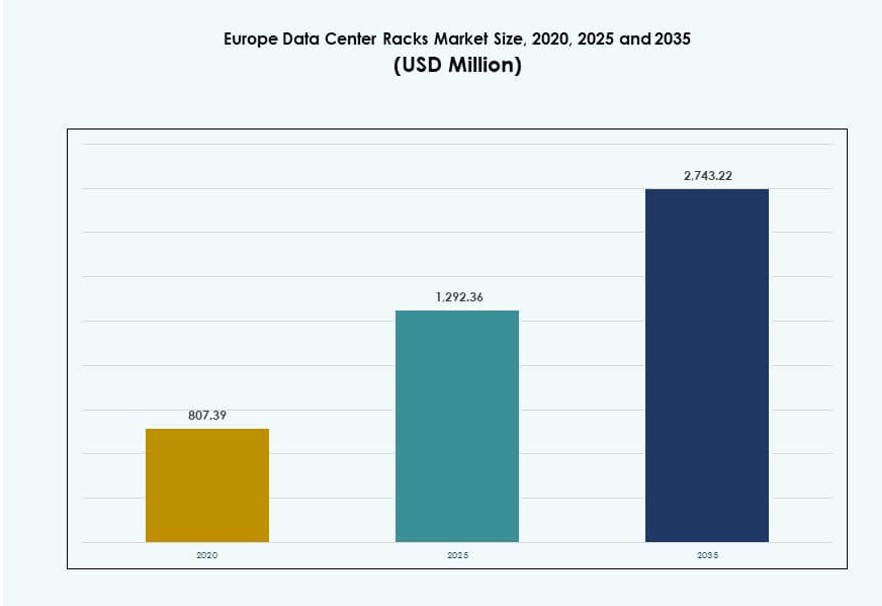

The Europe Data Center Racks Market size was valued at USD 807.39 million in 2020 to USD 1,292.36 million in 2025 and is anticipated to reach USD 2,743.22 million by 2035, at a CAGR of 7.77% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2035 |

| Europe Data Center Racks Market Size 2025 |

USD 1,292.36 Million |

| Europe Data Center Racks Market, CAGR |

7.77% |

| Europe Data Center Racks Market Size 2035 |

USD 2,743.22 Million |

The market is driven by the rise of AI-native data centers, increasing rack densities, and liquid-cooling integration. Hyperscale expansion across Western Europe and edge infrastructure in emerging zones fuel demand for scalable and intelligent racks. Enterprises are investing in software-defined infrastructure, with racks now integrating sensors, PDUs, and cooling enclosures. Sustainability and space optimization remain critical drivers. It plays a key role in supporting secure, high-performance, and future-ready infrastructure for cloud, colocation, and enterprise operators across the region.

Western Europe leads the market, supported by dense hyperscale deployments in Germany, the Netherlands, and the UK. The Nordic region is gaining traction due to its low power costs and green energy profile. Southern and Eastern Europe are emerging through government-backed digital infrastructure and compliance-led hosting demand. Each subregion contributes to the expansion of the Europe Data Center Racks Market by supporting local and cross-border data center growth.

Market Dynamics:

Market Drivers

Rising Adoption of High-Density Racks to Support AI and HPC Workloads

The shift toward high-performance computing is increasing rack densities across European facilities. Enterprises and hyperscale players are deploying racks with 30–50 kW capacity to support GPU clusters and AI training. These high-density configurations require advanced airflow, cable management, and thermal optimization. The Europe Data Center Racks Market benefits from this trend as AI-native workloads scale. Liquid cooling integration into rack units is expanding. Key markets like Germany and the Netherlands lead in adoption of AI-focused infrastructure. Government-backed digital transformation projects reinforce this trend. Edge data centers also deploy compact, high-density racks. Rack innovation is driving competitive positioning across core and edge locations.

Colocation and Cloud Expansion Fuel Rack Procurement Across Tier I and Tier II Markets

Growing demand for hybrid cloud and multi-tenant environments is spurring new data center builds. Colocation providers are deploying modular racks for faster scalability. The Europe Data Center Racks Market benefits from infrastructure growth in both established and emerging cities. Enterprises increasingly prefer colocation facilities with flexible rack footprints. Hyperscale cloud providers are expanding into secondary cities, creating fresh rack demand. Rack configurations now include integrated PDUs, airflow panels, and monitoring sensors. Operators seek faster deployments with pre-configured solutions. Standardization of rack dimensions ensures faster scale-up across distributed campuses. The need for physical security and airflow control remains critical in colocation settings.

- For instance, Digital Realty’s 2024 acquisition of a data center campus in Slough added 15 MW of capacity and over 2,000 cross-connects, enhancing colocation services in West London. The site supports scalable deployments for cloud and enterprise tenants within the company’s broader European platform.

Digital Sovereignty and Data Localization Regulations Encourage Regional Rack Deployments

Countries are enforcing regulations that require local data hosting for public and sensitive workloads. These rules prompt rack deployment across national facilities rather than central hubs. The Europe Data Center Racks Market benefits from this shift in infrastructure planning. Rack manufacturers support localized assembly and distribution to meet compliance. Public sector demand is growing for custom cabinets with enhanced security. Nations like France and Poland are strengthening domestic capacity. Rack shipments to government IT parks and municipal data centers are rising. Vendors offer secure, tamper-resistant rack enclosures. Compliance is shaping purchase preferences across verticals. Localization creates long-term contracts and recurring hardware upgrades.

Innovation in Rack-Level Monitoring, Automation, and Cooling Drives Strategic Importance

The need for real-time monitoring of temperature, airflow, and power usage is reshaping rack design. Intelligent racks with built-in sensors and telemetry are gaining traction. The Europe Data Center Racks Market sees rising integration of DCIM and thermal analytics software. Smart racks improve operational efficiency, especially in large-scale deployments. Edge sites also require automated health-checks due to limited on-site staff. Cooling-integrated racks are reducing PUE and improving energy sustainability. Investors favor infrastructure that delivers both scalability and efficiency. Rack-level intelligence enables predictive maintenance and uptime assurance. Strategic buyers prioritize future-proof designs supporting liquid cooling and AI-readiness.

- For instance, Microsoft’s data center region in Sweden operates on 100% renewable energy, primarily from hydroelectric sources, and supports efficient cloud operations through sustainable infrastructure and advanced cooling systems. This aligns with Microsoft’s commitment to carbon-free energy and high-efficiency performance in Europe.

Market Trends

Standardization of Rack Infrastructure to Enable Faster Cross-Border Data Center Expansions

Standard rack dimensions and component interfaces are enabling pan-European data center scaling. Operators replicate designs across regions for faster time to market. The Europe Data Center Racks Market benefits from modularity and interoperability across ecosystems. Enterprises prefer racks that support consistent workflows across sites. Component-level uniformity lowers installation errors and downtime. Global players like AWS, Azure, and Google favor standardized racks in European expansions. Open Compute Project (OCP) adoption also promotes design uniformity. Vendors are aligning offerings with hyperscale procurement models. Repeatable rack designs support rapid deployment across countries with minimal customization.

Integration of Liquid Cooling Solutions into Racks Becomes Essential for Thermal Efficiency

Data centers are reaching thermal limits with air cooling alone. Liquid cooling at the rack level enables support for high-wattage equipment. The Europe Data Center Racks Market is seeing strong uptake of direct-to-chip and rear-door liquid cooling. AI and HPC environments require cooling at rack densities over 40 kW. Liquid-ready racks are gaining demand from colocation and hyperscale providers. These racks include sealed containment, fluid connectors, and corrosion protection. Operators adopt liquid cooling to reduce energy use and meet green goals. Vendors develop compact rack-integrated cooling systems. Rack innovation is central to meeting upcoming ESG regulations.

Growth of Edge Computing Encourages Compact and Ruggedized Rack Deployments

Edge computing requires deployment of racks in harsh or space-constrained environments. The Europe Data Center Racks Market includes growth from smart cities, telecom towers, and remote industrial facilities. Edge racks are smaller, shock-resistant, and pre-integrated with cooling. They support low-latency processing near users or endpoints. Telecom providers and IoT platforms use edge racks to decentralize compute. Compact enclosures with remote management are essential for unmanned sites. Military, energy, and transport sectors deploy ruggedized racks. Rack vendors focus on mobility, cable optimization, and heat dissipation. Growth at the edge diversifies rack use cases across verticals.

Sustainable Rack Manufacturing and Materials Gain Momentum Across the Region

Sustainability goals influence the design and sourcing of data center racks. The Europe Data Center Racks Market reflects increased demand for recyclable materials and energy-efficient components. Manufacturers use steel and aluminum with low-carbon footprints. Some vendors integrate bamboo or recycled polymers for eco-friendly enclosures. Paints and finishes now meet RoHS and EU environmental norms. Buyers seek rack designs with minimal environmental impact across lifecycle. Governments push for local manufacturing to reduce transportation emissions. Circular economy principles guide product development. Sustainable racks are featured in tenders for public cloud and colocation builds. ESG-driven procurement is reshaping rack supply chains.

Market Challenges

Thermal Management Limitations and Space Constraints in Legacy Facilities

Older data centers across Europe often struggle to support high-density rack deployments. Their layouts lack adequate airflow and space for liquid cooling retrofits. The Europe Data Center Racks Market faces constraints when upgrading aging infrastructure. Air-cooled racks face efficiency losses at densities above 20–25 kW. Legacy halls with low ceilings and fixed cabling create design inflexibility. Operators must balance performance with safety and cooling capacity. Space optimization remains a bottleneck in Tier II cities. Rack upgrades often require full-room reengineering. These limitations hinder fast adoption of modern rack systems.

High Manufacturing and Shipping Costs Impact Procurement in Price-Sensitive Regions

Fluctuating raw material prices and high logistics costs raise rack prices across Europe. Some regions, particularly in Southern and Eastern Europe, face budget constraints. The Europe Data Center Racks Market sees procurement delays due to long lead times. Customized rack systems add cost layers and strain capital budgets. Import duties and regional compliance certifications raise costs further. Enterprises seek local manufacturing partners but face limited availability. Vendors must absorb currency volatility and trade disruptions. Price-sensitive verticals delay upgrades or opt for refurbished racks. Profit margins tighten for mid-sized suppliers lacking scale.

Market Opportunities

Strategic Investments in Modular Data Centers Create Demand for Pre-Assembled Rack Units

Modular data centers are gaining popularity for rapid deployment in greenfield and brownfield sites. These facilities rely on pre-assembled, tested rack systems for faster commissioning. The Europe Data Center Racks Market gains from demand for rack solutions pre-integrated with PDUs, cable trays, and sensors. Government cloud projects, digital campuses, and telecom networks favor modularization. This trend supports new entrants and smaller rack vendors offering rapid delivery.

Emergence of AI and GPU-Focused Facilities Encourages Adoption of Liquid-Cooled Rack Designs

AI infrastructure expansion across Europe is driving liquid-cooled rack adoption. Facilities focused on GPU clusters need rack systems that support 30–50 kW densities. The Europe Data Center Racks Market benefits as colocation and hyperscale players build AI-ready halls. Rack vendors with in-built cooling, leak detection, and safety compliance are gaining market share. Innovation in coolant compatibility and sensor integration boosts market opportunity.

Market Segmentation

By Rack Type

Cabinet racks dominate the Europe Data Center Racks Market due to their enclosed design, security features, and airflow control. Open frame racks see adoption in test labs and edge setups with space limitations. The “Others” segment includes wall-mount and portable rack types, catering to niche applications. Cabinet racks lead due to their compatibility with advanced cooling and cable management systems across colocation and enterprise environments.

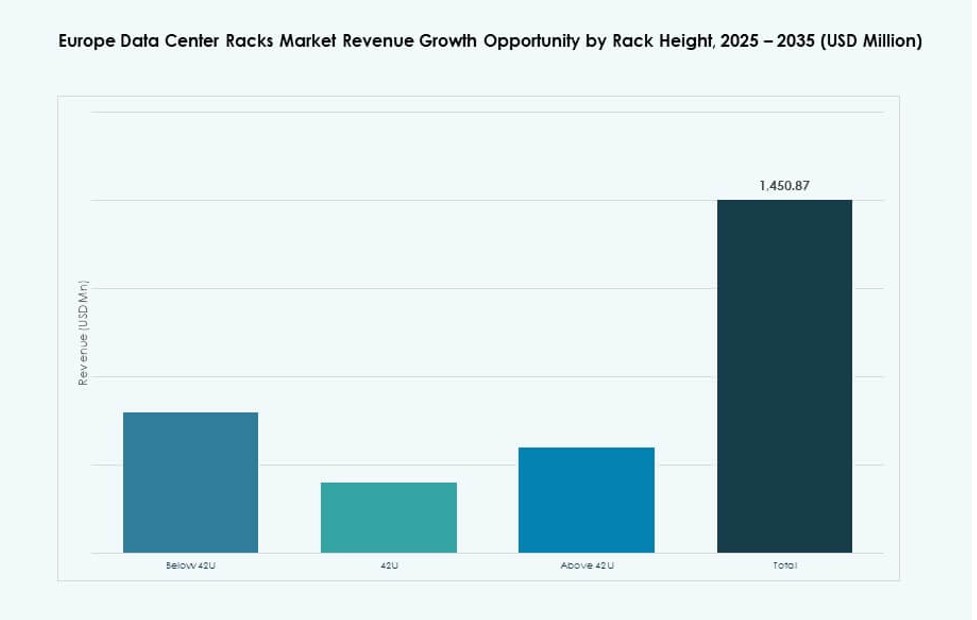

By Rack Height

42U racks are the most widely adopted size, offering the best balance between scalability and space usage. Below 42U racks serve edge and small setups with constrained height. Above 42U racks are gaining adoption in hyperscale environments to increase compute density per footprint. The Europe Data Center Racks Market is led by 42U racks due to their industry standardization and flexibility in deployment.

By Width

19-inch racks dominate due to their global standardization and compatibility with most IT hardware. 23-inch racks see limited usage in telecom-specific or legacy setups. The “Others” category includes custom or proprietary width designs. The 19-inch format continues to lead the Europe Data Center Racks Market for its universal fit and availability of accessories.

By Application

Server racks account for the largest share, driven by compute-heavy workloads in hyperscale and enterprise environments. Network racks support switching, routing, and security hardware, forming the second major application segment. The Europe Data Center Racks Market is dominated by server racks, which support mission-critical business and AI processing applications.

By End-user

Large data centers dominate the market due to their scale, need for modular systems, and ability to integrate high-density racks. Small and mid-sized data centers follow, often constrained by space and budget. The Europe Data Center Racks Market sees strong traction from large facilities undergoing constant rack refresh cycles to meet new workload demands.

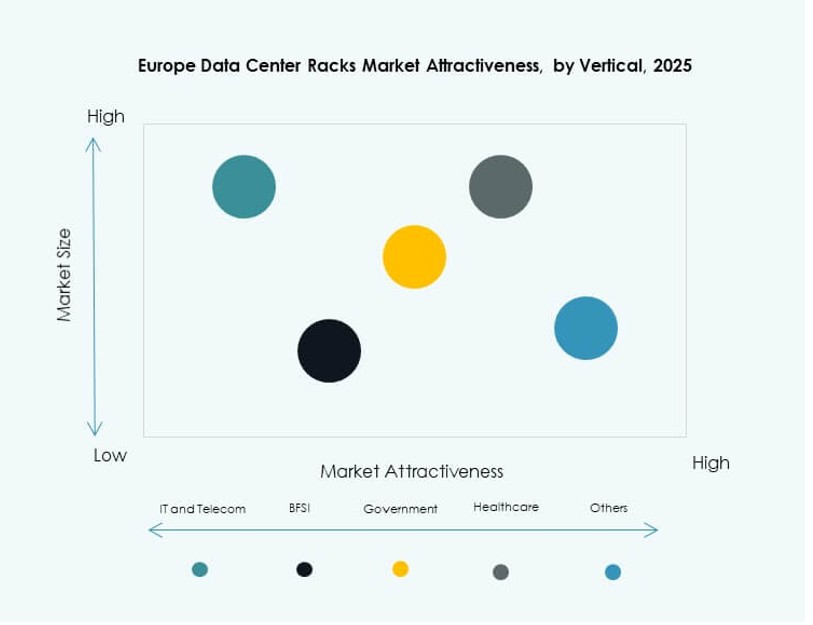

By Vertical

The IT & Telecom sector holds the largest market share due to continuous infrastructure upgrades and 5G rollout. BFSI and Government & Defense follow with strict security and compliance needs. Healthcare sees growing adoption from digital health initiatives. The Europe Data Center Racks Market benefits from vertical-specific needs, with IT & Telecom driving the highest rack density and turnover rates.

Regional Insights

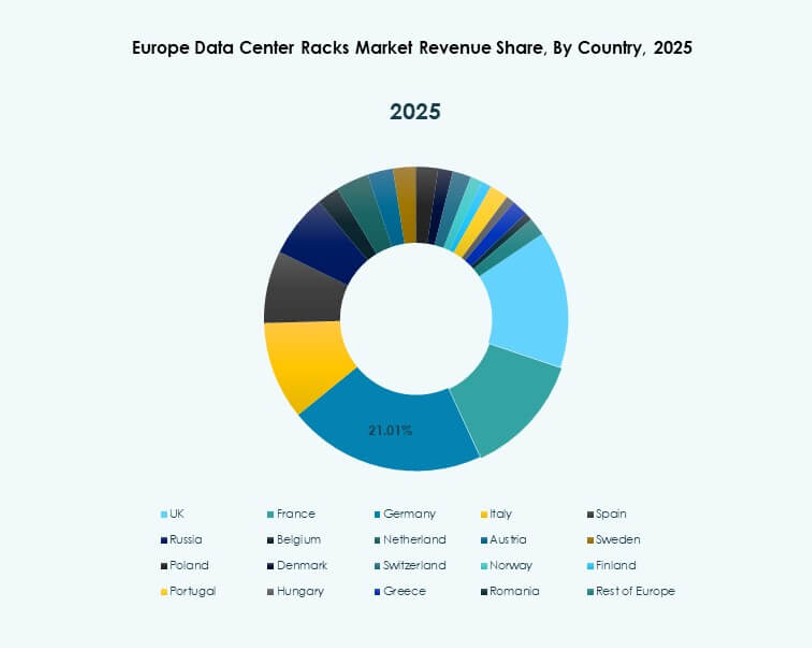

Western Europe Maintains Dominance with 48% Market Share Due to Hyperscale Presence

Western Europe leads due to advanced infrastructure and presence of global hyperscale firms. Countries like Germany, the UK, and the Netherlands host large colocation and cloud facilities. The Europe Data Center Racks Market sees consistent rack demand from Frankfurt, London, and Amsterdam hubs. Mature power and network infrastructure supports high-density deployments. Sustainability mandates further drive modernization in these regions. Rack innovation and liquid cooling solutions are deployed widely. Western Europe accounts for approximately 48% of the market.

- For instance, Equinix’s FR5 facility in Frankfurt offers colocation services with carrier-neutral connectivity and supports direct access to cloud on-ramps through the Equinix Fabric platform. It forms part of Equinix’s larger Frankfurt campus, one of the most interconnected data center hubs in Europe.

Nordic Region Accounts for 22% Market Share Due to Energy Efficiency and Green Power

Nordic countries offer low energy costs and abundant renewable power. Sweden, Norway, Finland, and Denmark attract data center investments focused on sustainability. The Europe Data Center Racks Market grows here through greenfield deployments with advanced thermal designs. Cold climate allows natural cooling benefits for rack setups. Government support and land availability encourage large-scale builds. The region holds nearly 22% of market share, supported by clean energy-based hyperscale campuses.

Southern and Eastern Europe Emerge with 30% Share from Localized Hosting and Compliance Needs

Southern and Eastern Europe are seeing a surge in colocation and edge data center growth. Countries like Spain, Poland, and Romania build capacity to meet local hosting and compliance mandates. The Europe Data Center Racks Market expands in these areas through enterprise, government, and telco demand. Rack vendors adapt designs for regional codes and space constraints. Regional players focus on low-cost, customizable rack offerings. This subregion holds an estimated 30% market share and continues to grow with digitization.

- For instance, Atman’s Warsaw‑3 campus near Warsaw launched its first building in September 2025, offering 14.4 MW of IT power and scalable colocation space designed for high‑performance infrastructure. The facility supports high‑density deployments and renewable‑powered operations, strengthening Poland’s role in Central and Eastern Europe’s data center ecosystem.

Competitive Insights:

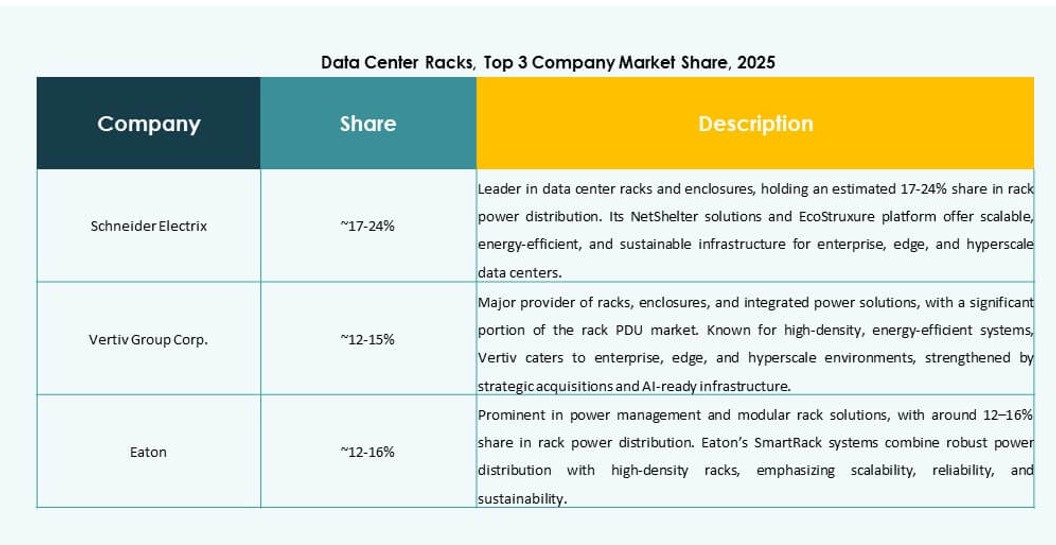

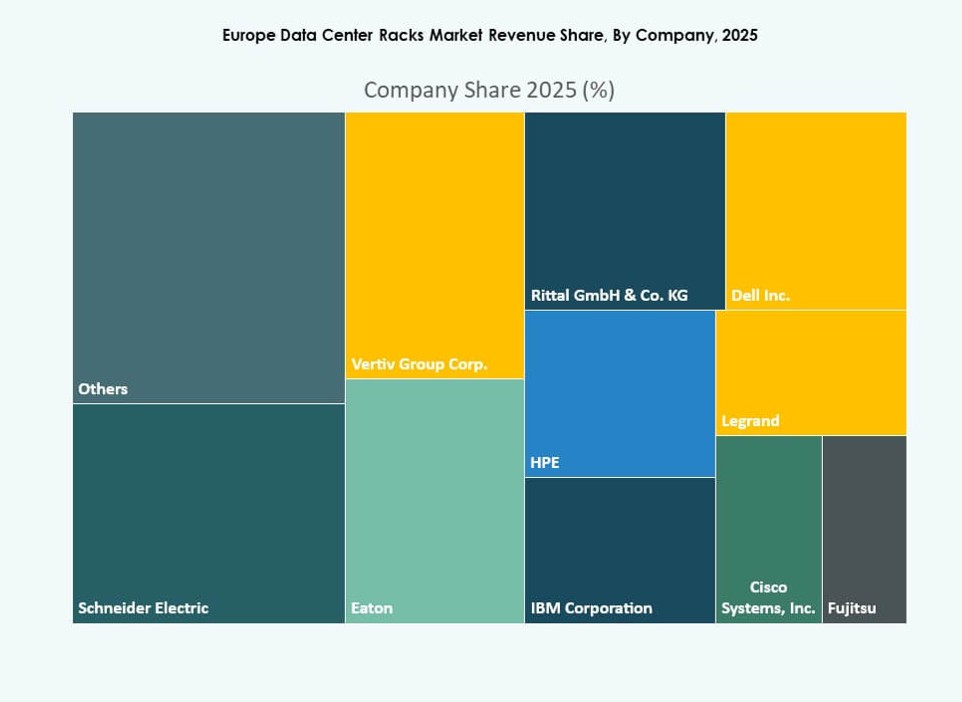

- Schneider Electric

- Vertiv Group

- Rittal

- Eaton

- Dell Inc.

- Hewlett Packard Enterprise (HPE)

- IBM (International Business Machines Corporation)

- Legrand

- Cisco Systems, Inc.

- Chatsworth Products

The Europe Data Center Racks Market features a mix of global powerhouses and specialized enclosure vendors competing on technology, customization, and deployment flexibility. It is led by Schneider Electric, Vertiv, and Rittal, known for full-stack infrastructure offerings integrated with cooling, power, and monitoring. HPE, Dell, and IBM leverage their compute portfolios to bundle rack systems for hyperscale and enterprise buyers. Companies like Eaton, Legrand, and Panduit focus on energy efficiency, modularity, and smart enclosures. Cisco and Chatsworth Products cater to high-density network and AI workloads. Players are focusing on liquid-cooling readiness, rack-level telemetry, and sustainability-driven designs. M&A and regional manufacturing partnerships are key strategies, while vendors tailor offerings for hyperscale, edge, and colocation clients across Western and Nordic Europe.

Recent Developments:

- In July 2025, Vertiv acquired Great Lakes Data Racks & Cabinets for approximately USD 200 million. The acquisition strengthens Vertiv’s integrated infrastructure offering by adding rack and cabinet expertise to its portfolio, which supports AI and high‑density computing environments.

- In April 2025, Apollo Funds finalized the purchase of Stack Infrastructure’s European colocation business, adding seven sites across Stockholm, Oslo, Copenhagen, Milan, and Geneva and standardizing cabinet models across the portfolio.

- In February 2025, CHINT strengthened its global collaboration with Rittal GmbH & Co. KG, focusing on innovations relevant to electrical enclosures and data center infrastructure solutions.