Executive summary:

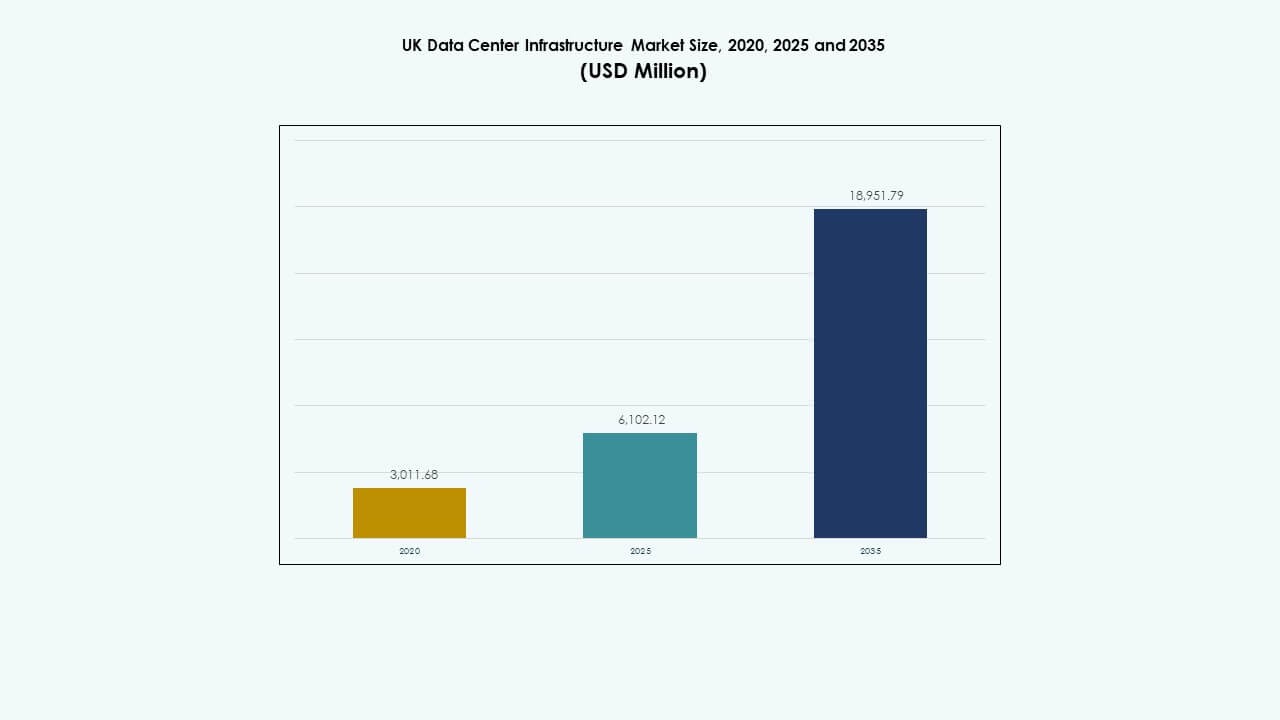

The UK Data Center Infrastructure Market size was valued at USD 3,011.68 million in 2020, rising to USD 6,102.12 million in 2025, and is anticipated to reach USD 18,951.79 million by 2035, growing at a CAGR of 11.91% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2035 |

| UK Data Center Infrastructure Market Size 2025 |

USD 6,102.12 Million |

| UK Data Center Infrastructure Market, CAGR |

11.91% |

| UK Data Center Infrastructure Market Size 2035 |

USD 18,951.79 Million |

Rising demand for cloud computing, AI workloads, and edge deployments drives infrastructure modernization. Companies invest in advanced power, cooling, and network systems to enhance scalability and sustainability. The UK Data Center Infrastructure Market benefits from increased enterprise digital transformation and regulatory support for data localization. It serves as a strategic hub for investors seeking stable returns from digital infrastructure, powered by the rapid growth of connected services and automation technologies.

London and the South East remain dominant due to robust connectivity and enterprise concentration. Northern England shows rapid expansion through new hyperscale and colocation projects supported by lower land costs. Scotland and Wales attract attention for renewable energy availability and government-backed green incentives. The UK Data Center Infrastructure Market gains balanced growth across regions, enhancing national resilience and diversifying data capacity distribution beyond traditional metropolitan hubs.

Market Drivers

Market Drivers

Rapid Growth in Digital Transformation and Cloud Infrastructure Expansion

The UK Data Center Infrastructure Market experiences strong momentum from widespread digital transformation. Businesses across industries migrate workloads to the cloud to improve flexibility and cost efficiency. The adoption of hybrid and multi-cloud strategies increases infrastructure demand. Cloud providers invest in large campuses near London to meet service requirements. The market also benefits from national digital policies supporting secure cloud expansion. It continues to attract hyperscale investment from global players. The rapid rise of AI workloads further accelerates infrastructure upgrades. Organizations pursue resilient architecture to support round-the-clock operations. Strong government backing ensures long-term digital readiness.

- For example, Latos Data Centres, a UK-based operator, is authentically expanding its footprint with plans to build 40 AI-ready data centers across the UK by 2030, starting with a large hyperscale facility near Cardiff delivering 90MVA across 50,400 square meters of floor space. This expansion reflects strong momentum driven by AI workloads and cloud adoption.

Rising Adoption of Edge Computing and Data Localization Requirements

Edge computing plays a critical role in shaping the UK Data Center Infrastructure Market. Businesses demand low-latency computing for real-time applications in logistics, finance, and retail. Distributed edge sites reduce congestion at core facilities and improve response times. Telecom operators deploy micro data centers integrated with 5G networks. These edge deployments improve consumer experiences and operational performance. Strict data localization rules under UK law push companies to host data domestically. It promotes new regional facilities outside London. Enterprises emphasize secure and compliant local storage solutions. Such shifts strengthen distributed infrastructure and national resilience.

Innovation in Energy Efficiency and Sustainability Practices

The growing focus on sustainable operations drives infrastructure innovation in the UK Data Center Infrastructure Market. Operators adopt advanced cooling technologies and renewable energy integration to reduce emissions. Many facilities use liquid cooling and AI-based optimization for energy use. New builds target PUE levels near 1.2 or lower, aligning with global green standards. Solar and wind power supply a large share of operational energy. Investors prioritize ESG-aligned portfolios in digital infrastructure. Energy reuse and waste-heat recovery projects enhance efficiency. The shift toward sustainability attracts long-term institutional funding. It transforms data centers into low-carbon digital utilities.

- For example, Equinix has been expanding liquid-cooling and AI-driven efficiency measures across its global data centers, including facilities in London. The company targets PUE levels near 1.2 in new builds and continues investing in sustainable operations through advanced cooling and optimized power management systems.

Integration of Artificial Intelligence and Automation in Data Center Operations

Automation reshapes operations across the UK Data Center Infrastructure Market. AI tools enhance predictive maintenance, workload management, and security monitoring. Data centers use autonomous systems to detect faults before failure. Automation helps reduce human error and operational downtime. AI-driven cooling systems optimize airflow and power distribution in real time. Robotic inspection and maintenance support 24/7 reliability. The push for intelligent infrastructure boosts productivity and resource efficiency. It reduces maintenance costs and improves uptime performance. Such transformation makes UK facilities globally competitive in smart operations.

Market Trends

Market Trends

Shift Toward Modular and Prefabricated Data Center Construction

A major trend in the UK Data Center Infrastructure Market is modular construction. Developers favor prefabricated modules for faster delivery and reduced cost. These modules allow flexible scaling based on workload growth. Prefabrication supports energy-efficient designs and simplified maintenance. Hyperscalers deploy such systems to accelerate new builds. Shorter deployment cycles strengthen time-to-market advantage. It enables data centers to align capacity with evolving AI and cloud needs. The shift boosts standardization and cross-site uniformity. Modular systems also meet sustainability goals by minimizing waste.

Growing Role of Renewable Energy and Power Purchase Agreements (PPAs)

Energy sustainability emerges as a key trend within the UK Data Center Infrastructure Market. Operators secure long-term renewable PPAs to stabilize power costs. Many facilities rely on wind farms and solar arrays to reach carbon neutrality. Power reliability becomes essential as grid congestion increases. Energy storage integration supports stable supply during peak demand. Data center operators invest in battery systems for resilience. Green energy credentials attract environmentally conscious clients. This trend aligns with national net-zero emission targets. It strengthens investor confidence in sustainable infrastructure models.

Adoption of High-Density Computing and Liquid Cooling Systems

High-density computing shapes the technical evolution of the UK Data Center Infrastructure Market. AI workloads, GPU clusters, and analytics drive higher rack power density. Traditional air cooling struggles to manage heat loads effectively. Operators turn to liquid and immersion cooling for better thermal control. These systems cut energy use and extend equipment life. Facility designs evolve to accommodate liquid circulation systems. The trend supports advanced hardware performance and reduced floor space use. Data centers adopting this technology see better efficiency and reliability. It positions the UK as a leading hub for high-performance computing infrastructure.

Increasing Investments in Colocation and Interconnection Ecosystems

Colocation remains a strong trend within the UK Data Center Infrastructure Market. Enterprises prefer third-party facilities for cost and scalability benefits. London’s connectivity density attracts global carriers and cloud exchanges. Interconnection hubs improve data exchange speed between networks. Operators expand regional facilities to reduce dependency on the capital. Hybrid models combining private and shared infrastructure gain traction. The expansion of internet exchanges boosts data flow efficiency. Growing enterprise demand for secure connectivity supports colocation investment. It helps the market maintain long-term competitiveness.

Market Challenges

Market Challenges

Escalating Energy Costs and Limited Power Availability in Key Regions

Energy cost volatility creates pressure in the UK Data Center Infrastructure Market. Rising electricity prices increase operational expenses for large facilities. London and surrounding regions face grid congestion and power constraints. Projects face delays due to connection approvals. Operators struggle to balance capacity expansion with sustainable power sourcing. Limited renewable energy access further complicates planning. Energy efficiency upgrades become vital for maintaining margins. It compels operators to innovate with advanced cooling and microgrid systems. Long-term power strategies define future competitiveness in this market.

Stringent Regulatory Compliance and Land Availability Constraints

Regulatory complexity challenges the UK Data Center Infrastructure Market. Environmental, construction, and cybersecurity standards impose long approval timelines. Urban land scarcity limits hyperscale development near London. Developers must find suitable secondary sites without compromising connectivity. Compliance with energy-efficiency regulations adds design and cost hurdles. Operators must also meet evolving data protection requirements under UK law. These conditions slow project execution and raise overall costs. It pressures firms to balance compliance, performance, and expansion goals. Local partnerships become critical to overcoming approval barriers.

Market Opportunities

Emergence of AI and Edge-Ready Infrastructure for Next-Generation Workloads

AI and edge computing open strong opportunities for the UK Data Center Infrastructure Market. Businesses seek low-latency nodes for real-time analytics and automation. Telecom firms integrate edge micro data centers into 5G rollouts. AI-ready infrastructure supports faster model training and inference. Localized compute reduces data transport costs and delays. Operators offering AI-optimized facilities gain premium demand. It positions the UK as a strategic hub for intelligent digital services.

Growing Investments in Green Data Centers and Circular Energy Systems

Sustainability presents long-term opportunities for the UK Data Center Infrastructure Market. Investors fund renewable-powered and carbon-neutral facilities. Operators implement waste-heat recovery and closed-loop cooling systems. Cities adopt data centers as part of urban sustainability plans. Green certifications improve brand reputation and attract global clients. Integration with district heating networks enhances energy reuse. It drives eco-efficient expansion aligned with national climate goals.

Market Segmentation

By Infrastructure Type

Electrical infrastructure dominates the UK Data Center Infrastructure Market due to continuous demand for reliable power systems. Mechanical components like cooling and containment follow closely in share. Civil and architectural upgrades support large-scale expansions. IT and network infrastructure witness fast upgrades driven by AI and cloud integration. Advanced cabling and racks enable higher density deployments. Growth remains steady across modular and traditional setups supporting multi-tenant facilities.

By Electrical Infrastructure

Uninterruptible Power Supply (UPS) holds the largest share in the UK Data Center Infrastructure Market. Reliable UPS systems ensure uninterrupted service during grid fluctuations. Battery Energy Storage Systems (BESS) gain popularity for renewable integration. PDUs and transfer switches support efficient power distribution. Utility grid connections improve redundancy and scalability. Demand rises for advanced power electronics that reduce downtime risks.

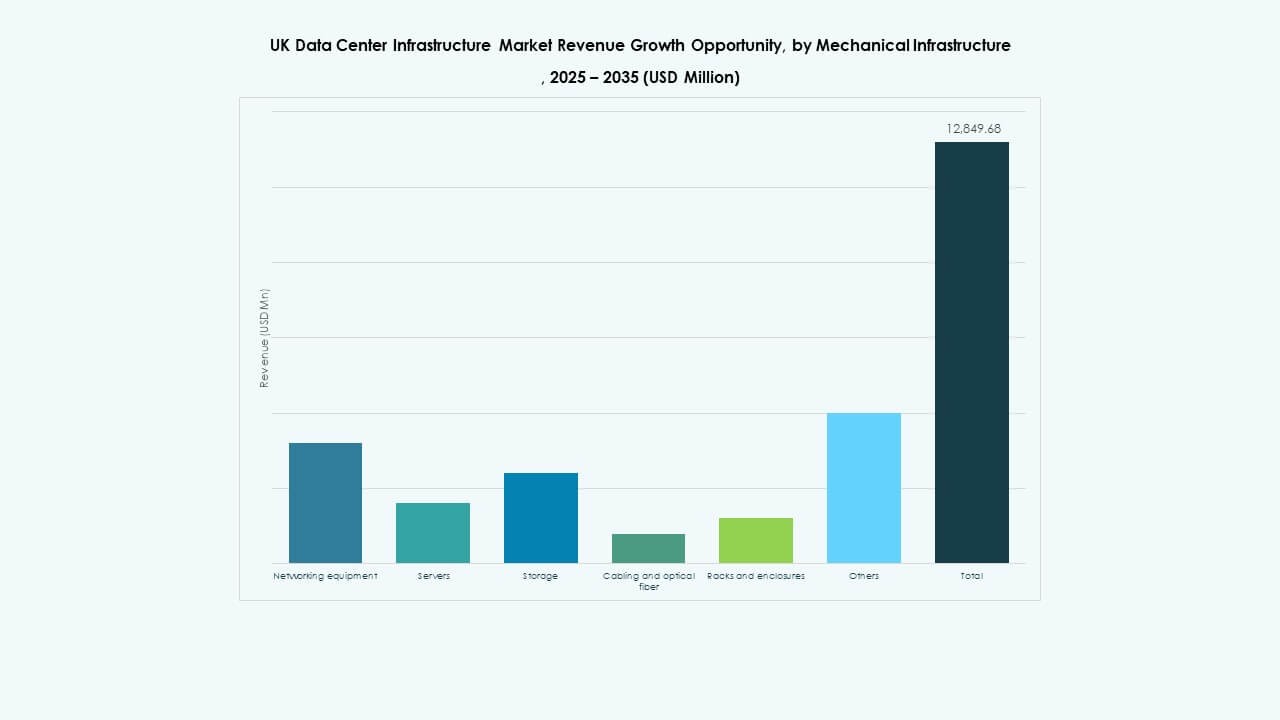

By Mechanical Infrastructure

Cooling units such as CRAC and CRAH dominate the mechanical segment of the UK Data Center Infrastructure Market. Operators invest in air and liquid chillers to maintain server reliability. Containment systems improve thermal isolation and energy efficiency. Pumps and piping systems ensure continuous coolant flow. Sustainable design adoption reduces carbon output. Facilities deploy hybrid systems combining air and water solutions.

By Civil / Structural & Architectural

Superstructure and building envelope systems lead this segment in the UK Data Center Infrastructure Market. Modular building designs improve deployment speed. Steel and concrete frames support high-load installations. Raised floors and suspended ceilings enhance airflow efficiency. Prefabricated modules minimize construction waste. Strong foundations ensure seismic and vibration resistance for stable operation.

By IT & Network Infrastructure

Servers and storage units form the core of the IT infrastructure segment in the UK Data Center Infrastructure Market. Networking equipment and optical cabling support high-speed data transfer. Racks and enclosures optimize spatial organization. Growing AI and analytics workloads demand scalable compute capacity. Upgraded systems reduce latency and enhance digital service performance.

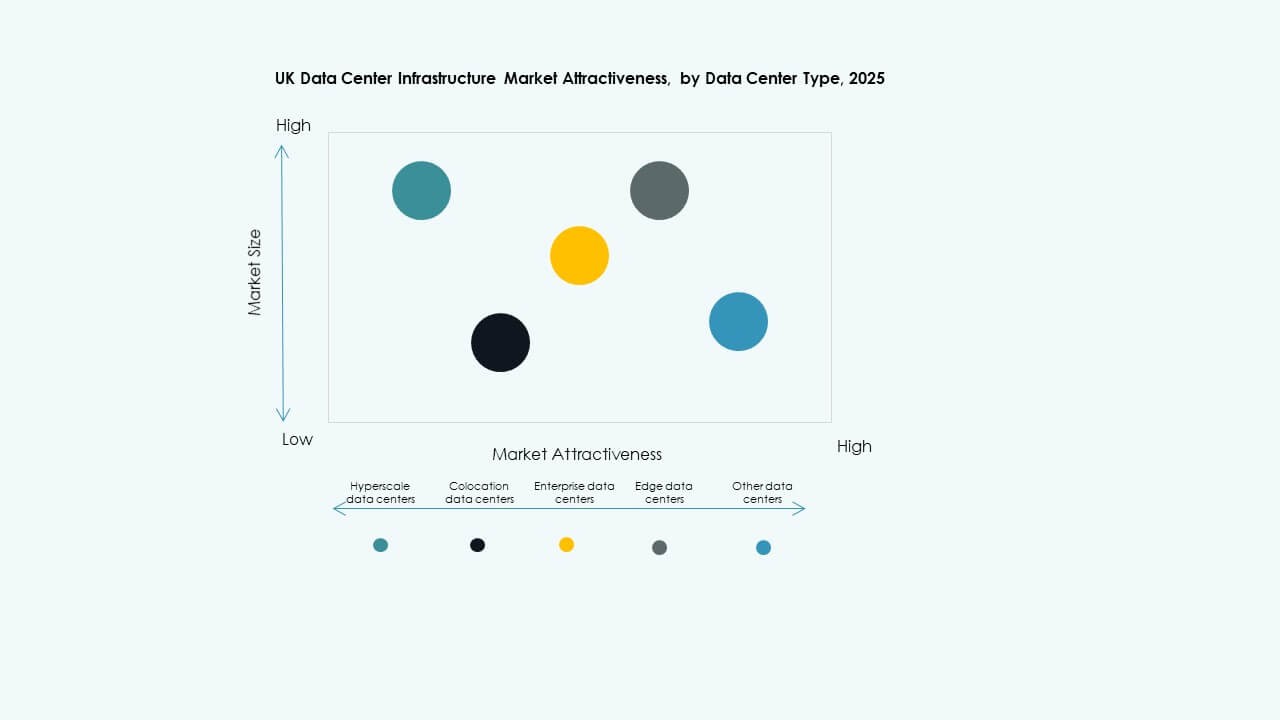

By Data Center Type

Hyperscale data centers lead the UK Data Center Infrastructure Market with dominant capacity share. Colocation facilities expand rapidly to serve enterprise clients. Edge centers emerge to support distributed computing needs. Enterprise data centers maintain stable demand for in-house applications. Modular facilities gain traction for quick deployment.

By Delivery Model

Turnkey and design-build models dominate the UK Data Center Infrastructure Market due to cost and time efficiency. Retrofit and modular factory-built systems follow with flexible customization. Construction management services cater to large-scale corporate projects. EPC models gain preference for complex multi-phase developments.

By Tier Type

Tier 3 facilities hold the largest share in the UK Data Center Infrastructure Market, offering balanced redundancy and cost. Tier 4 centers rise in adoption for mission-critical applications. Tier 1 and 2 facilities serve small-scale enterprises. Continuous uptime expectations drive upgrades to higher-tier designs.

Regional Insights

London and South East – Core Hub with 65% Market Share

London dominates the UK Data Center Infrastructure Market with nearly 65% share. It hosts major hyperscale and colocation hubs due to network density and connectivity. Enterprises favor this region for low latency and financial sector proximity. The South East complements London with strong infrastructure and available land. The region benefits from reliable grid access and strong renewable adoption. It remains the central node for international cloud operators.

- For example, in September 2025, Google opened its new Waltham Cross data center in Hertfordshire as part of a £5 billion UK investment plan. The facility supports AI and cloud services while emphasizing sustainability and renewable energy integration, contributing to Google’s goal of achieving near-carbon-free operations in the UK by 2026.

Northern England – Emerging Growth Corridor with 20% Market Share

Northern England accounts for about 20% of the UK Data Center Infrastructure Market. The region gains traction due to lower costs and new renewable energy zones. Manchester and Leeds attract hyperscale and colocation projects. Regional authorities promote data investment to balance economic distribution. Improved fiber routes and power supply strengthen site attractiveness. It becomes a preferred destination for expansion outside the congested South.

Scotland, Wales, and Others – Sustainable Expansion with 15% Market Share

Scotland and Wales collectively represent around 15% share of the UK Data Center Infrastructure Market. These areas attract investors with cool climates and green power sources. Edinburgh and Cardiff show increasing data infrastructure deployments. Rural zones offer space for low-impact modular centers. Government incentives support regional digital growth. It contributes to nationwide capacity diversification and sustainability alignment.

- For example, Verne Global operates a 100% renewable-powered data center campus in Keflavík, Iceland, utilizing hydroelectric and geothermal energy. The facility leverages the cool Nordic climate for ultra-efficient cooling and supports high-performance computing and AI workloads with minimal environmental impact.

Competitive Insights:

Competitive Insights:

- ABB Ltd.

- Cisco Systems, Inc.

- Dell Inc.

- Equinix, Inc.

- Hewlett Packard Enterprise Development LP

- Schneider Electric SE

- Vertiv Group Corp.

- Huawei Technologies Co., Ltd.

- IBM Corporation

- Fujitsu Limited

The UK Data Center Infrastructure Market remains highly competitive with strong participation from global and regional players. It is defined by continuous investment in power, cooling, and IT system innovation. ABB, Schneider Electric, and Vertiv lead in electrical and mechanical systems supporting energy efficiency. HPE, Dell, and IBM dominate IT and networking infrastructure. Equinix and Fujitsu strengthen the colocation and managed service space. Huawei expands presence through modular and prefabricated facility solutions. Companies focus on AI-driven management platforms, sustainable operations, and scalable architectures. Mergers, technology partnerships, and regional capacity expansions enhance competitive positioning and market influence.

Recent Developments:

- In November 2025, ABB Ltd. expanded its partnership with Applied Digital to supply power infrastructure for Applied Digital’s second AI factory campus in North Dakota, supporting the rapidly growing power needs of AI workloads with advanced medium voltage electrical infrastructure. This long-term partnership enables ABB to deliver low and medium voltage electrical architecture for large-scale data centers aimed at high performance and energy efficiency.

- In November 2025, Schneider Electric secured roughly USD 2.3 billion in new U.S. data-center contracts. The deals include major supply agreements with a hyperscale operator and a leading colocation provider to supply power modules, cooling systems, UPS units and switchgear over 2025–2026.

- In October 2025, Hitachi signed a strategic partnership with OpenAI to expand global AI data-center infrastructure. Under this agreement, the companies will co-develop modular and prefabricated data-center designs, energy-efficient cooling and storage infrastructures, and plan supply-chain strategies for reliable deployment. The deal targets sustainable data-center operations and rapid global expansion of AI infrastructure

- In September 2025, Schneider Electric launched its AI-ready liquid-cooled EcoStruxure solutions designed for high-density servers supporting NVIDIA GPU-based workloads, marking a significant product launch in data center infrastructure.

- In September 2025, ABB announced a $110 million investment in the US to support growth in data centers and power grids, including doubling the size of its Richmond, Virginia facility to meet increasing demand from North American customers, creating new production and engineering roles