Executive summary:

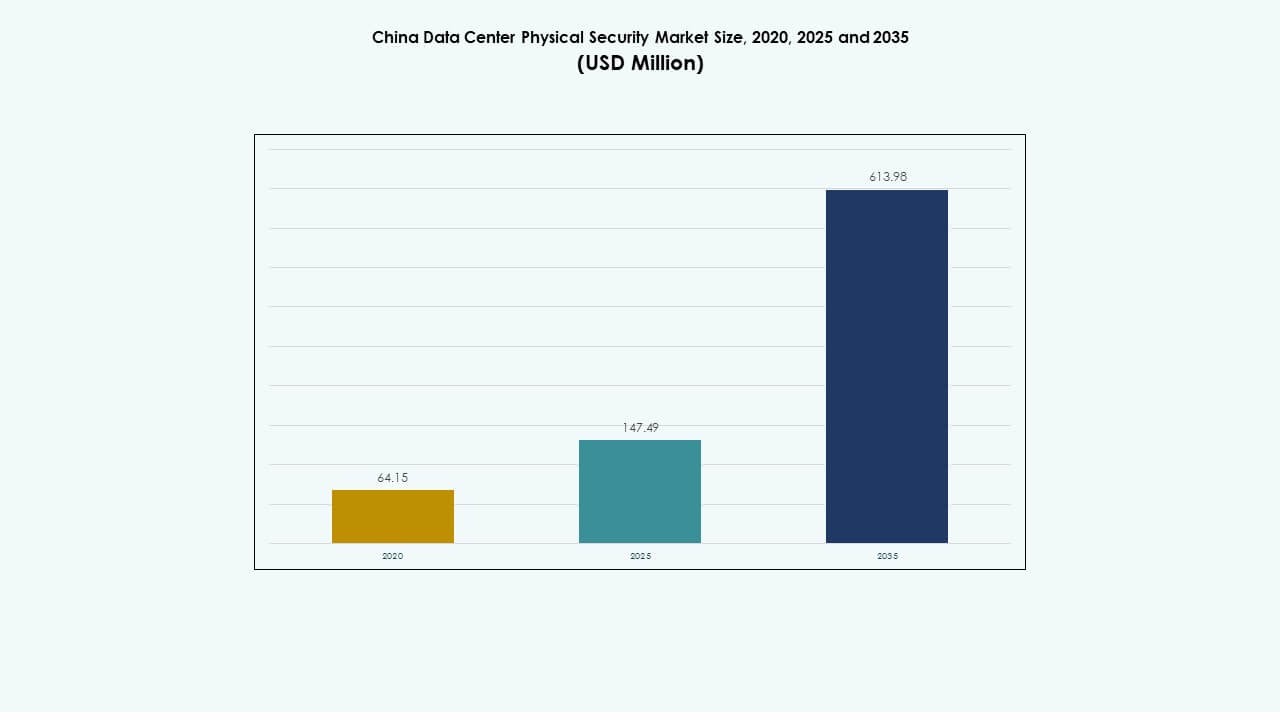

The China Data Center Physical Security Market size was valued at USD 64.15 million in 2020 and grew to USD 147.49 million in 2025. It is anticipated to reach USD 613.98 million by 2035, at a CAGR of 15.17% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2035 |

| China Data Center Physical Security Market Size 2025 |

USD 147.49 Million |

| China Data Center Physical Security Market, CAGR |

15.17% |

| China Data Center Physical Security Market Size 2035 |

USD 613.98 Million |

The China Data Center Physical Security Market expands with rapid adoption of AI-driven surveillance, biometric access control, and IoT-enabled monitoring. Rising hyperscale investments and government-led cybersecurity mandates drive system upgrades. Innovation in automation and analytics enhances protection and operational efficiency. The market holds strategic value for investors aiming to support secure digital infrastructure and long-term resilience.

Eastern China dominates the market due to high data center concentration and strong industrial digitization. Northern China follows, driven by government-backed projects and defense-grade security integration. Southern provinces emerge as fast-growing regions supported by cloud infrastructure and industrial expansion. Regional policies continue to strengthen adoption across all major economic zones.

Market Drivers

Market Drivers

Expanding Hyperscale Infrastructure and Rising Security Prioritization

The China Data Center Physical Security Market is driven by the expansion of hyperscale and colocation data centers across major cities like Beijing, Shanghai, and Shenzhen. Large operators invest in multi-layered security frameworks to protect growing digital assets and prevent operational disruption. Demand for surveillance, access control, and intrusion detection is growing with the rapid rise in data-intensive industries. Strong policy support under China’s digital economy roadmap strengthens adoption. It supports investors aiming to safeguard mission-critical facilities amid cloud migration and AI-driven workloads. Businesses prioritize compliance with national cybersecurity standards. The market gains importance due to its role in sustaining uninterrupted service.

- For instance, Alibaba Cloud Security Center uses machine learning and big data analytics to detect threats such as unusual login attempts and malicious processes. It provides multi-layered protection, compliance checks, and real-time monitoring across Alibaba Cloud’s data centers in China, including major hubs like Beijing and Shanghai.

Integration of Artificial Intelligence and IoT into Physical Security Systems

AI, machine learning, and IoT integration reshape physical security frameworks across China’s data centers. Smart cameras, biometric readers, and automated monitoring tools detect abnormal activity and minimize human errors. The market benefits from real-time analytics for threat anticipation and response optimization. IoT-based environmental sensors enhance perimeter and server room safety. It aligns with the broader trend of intelligent facility management. Vendors leverage predictive maintenance and unified dashboards to streamline control. The integration of edge analytics allows faster local decision-making. Businesses adopt these solutions to improve efficiency and resilience.

Regulatory Compliance and Government-led Infrastructure Protection Policies

Stringent national regulations under China’s Cybersecurity Law and Data Security Law boost investments in certified security systems. Operators focus on building government-compliant data centers with advanced access authentication. The market benefits from coordinated public-private security programs that encourage secure facility construction. Local manufacturing of surveillance hardware ensures cost-efficient scaling. It supports China’s goal of achieving technological self-reliance in critical infrastructure protection. Multinational firms adapt their strategies to meet localization rules. Businesses enhance on-site verification protocols to maintain regulatory transparency. The emphasis on compliance accelerates secure facility deployment.

- For instance, Tencent Cloud complies with China’s Cybersecurity Law and Data Security Law, holding certifications such as ISO 27001 and China Classified Protection (三级等保). It uses multi-factor biometric authentication and hardware security modules (HSM) to strengthen secure access and meet national compliance standards for data protection.

Strategic Investments and Partnerships Driving Infrastructure Modernization

Major technology and telecom companies form partnerships with security integrators to upgrade existing facilities. Investments target unified platforms that connect multiple layers of physical and digital security. The market advances through ecosystem collaboration involving AI firms and industrial automation providers. It helps enterprises adopt standardized safety protocols for high-traffic data centers. Global vendors entering China partner with local integrators for regulatory alignment. It boosts technology transfer and improves end-user trust. Continuous funding in infrastructure modernization supports job creation and economic resilience.

Market Trends

Market Trends

Shift Toward AI-driven Predictive Surveillance Systems

The China Data Center Physical Security Market experiences a strong shift toward AI-based predictive surveillance. Advanced analytics enable automated incident forecasting and instant alerts. Facial recognition and behavioral mapping tools improve perimeter defense accuracy. The adoption of AI reduces dependency on manual oversight. Vendors integrate machine learning to adapt to dynamic environments. Smart video management platforms link with building automation systems. It allows data-driven decision-making in control rooms. The use of predictive insights supports proactive security maintenance.

Emergence of Integrated Security Management Platforms

Data center operators prefer integrated platforms that unify video, access, and intrusion systems into one dashboard. These platforms improve operational visibility and reduce maintenance costs. They allow real-time synchronization between IT and physical infrastructure layers. Vendors focus on cloud-based deployment models for scalability and flexibility. Integration enhances cross-system communication and shortens response time during critical events. It empowers facilities to align security with business continuity plans. Operators gain analytical insights into system performance. The growing shift toward convergence accelerates adoption.

Increased Focus on Green and Energy-efficient Security Solutions

Sustainability goals influence the development of next-generation physical security systems. Manufacturers design low-power surveillance cameras and smart sensors to cut energy use. The market aligns with China’s broader carbon neutrality targets. Operators deploy renewable-powered access control units to reduce operational footprints. It improves energy performance while maintaining reliability. Data centers emphasize eco-certification of security equipment. Suppliers introduce recyclable materials in system enclosures. The trend attracts eco-conscious investors seeking sustainable infrastructure growth.

Rise of Edge and Modular Data Center Security Deployments

Edge computing expansion leads to modular security installations in distributed environments. Small and medium data centers deploy scalable access and monitoring systems tailored to compact layouts. Edge facilities demand autonomous surveillance units capable of remote diagnostics. The market grows as service providers secure edge nodes supporting AI and IoT traffic. It reflects a transition toward decentralized protection models. Vendors develop plug-and-play systems for rapid deployment. The modular approach ensures flexibility in fast-evolving infrastructure networks.

Market Challenges

Market Challenges

High Deployment Costs and Integration Complexity Across Legacy Systems

The China Data Center Physical Security Market faces cost pressure from advanced equipment and integration challenges. Many facilities still rely on outdated control systems, making modernization difficult. Integrating AI-based analytics with older frameworks requires technical expertise. Procurement costs for high-end biometric and sensor systems strain smaller operators. The shortage of skilled personnel limits seamless adoption. It raises project timelines and total cost of ownership. Enterprises hesitate to invest without measurable ROI. Vendors must simplify deployment processes to expand market reach.

Regulatory Barriers and Data Localization Constraints on Global Vendors

Regulatory uncertainty and localization requirements challenge international solution providers. Vendors must store sensitive security data within China’s borders. It restricts cross-border collaboration and delays new technology rollouts. Domestic certifications are mandatory for hardware and software approval. The limited interoperability between domestic and foreign systems complicates partnerships. Businesses find compliance management resource-intensive. It slows down project execution in multi-region operations. Maintaining balance between compliance and innovation remains a key barrier to market acceleration.

Market Opportunities

Expansion of Cloud and AI-driven Security Infrastructure

The China Data Center Physical Security Market offers growth potential through AI-enhanced and cloud-based systems. Rising cloud service adoption fuels new installations in hyperscale campuses. Vendors gain opportunities in deploying automated surveillance and smart alarm networks. It encourages partnerships between local manufacturers and software firms. Enterprises leverage intelligent monitoring for predictive analytics. This transformation supports smarter, more adaptive security models. Long-term prospects favor domestic innovation and export potential in advanced surveillance.

Government-led Smart City and Digital Silk Road Initiatives

China’s smart city programs expand the scope for secure data infrastructure development. These projects link data centers with urban surveillance and critical communication grids. The market benefits from government-backed investments in secure connectivity networks. It supports global data exchange within Belt and Road economies. Businesses targeting these projects gain early access to infrastructure contracts. It reinforces national resilience and strengthens industrial competitiveness. The focus on strategic digital expansion enhances multi-sector collaboration.

Market Segmentation

By Data Center Size

Small and medium data centers account for steady adoption of modular security systems, while large facilities dominate revenue due to broader infrastructure scope. The China Data Center Physical Security Market sees large data centers deploying advanced multi-layer protection, including AI-enabled monitoring. Growth in smaller sites arises from regional expansion and localized cloud nodes. Both segments benefit from scalable and energy-efficient designs enhancing compliance and reliability.

By Component

Solutions lead the market as data centers prioritize hardware and software integration for unified control. Services gain traction due to the demand for ongoing monitoring and technical support. The China Data Center Physical Security Market expands through combined offerings that balance product capability with managed services. Continuous maintenance ensures system reliability and uptime in high-volume operations. Service providers differentiate through remote diagnostics and customization features.

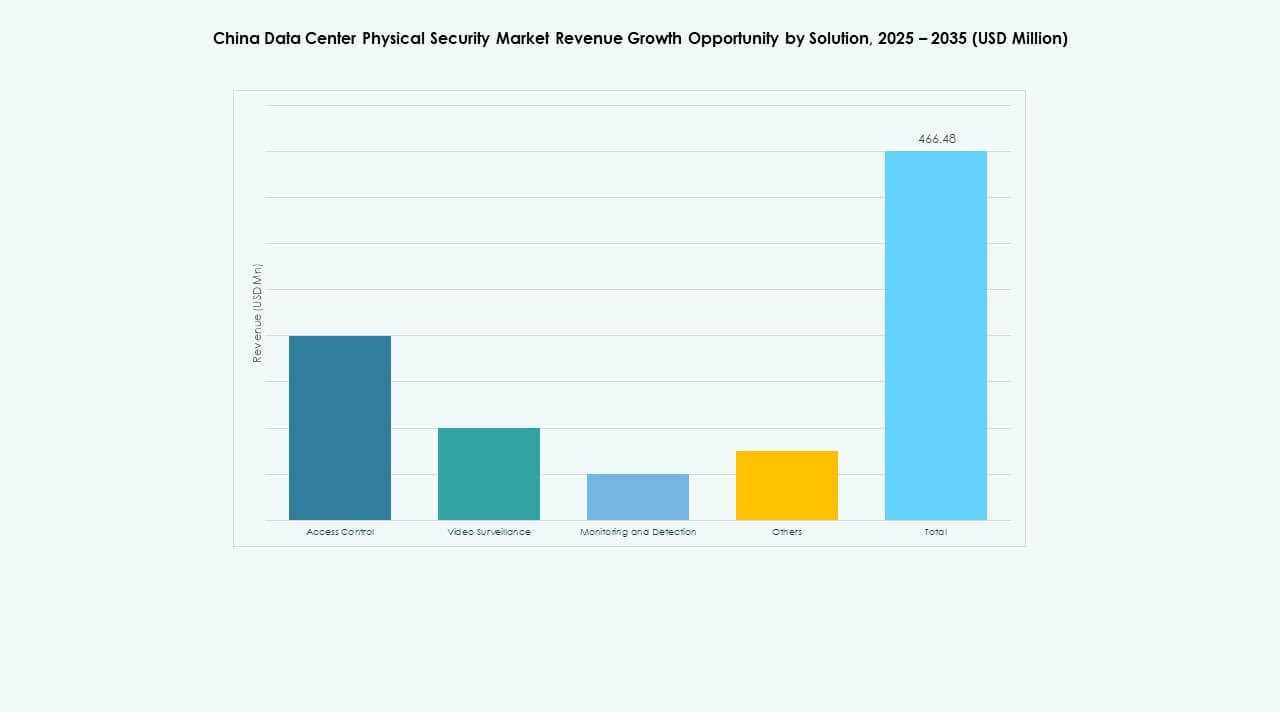

By Solution

Video surveillance remains dominant, supported by AI-powered analytics and real-time threat detection. Access control systems with biometric validation and keycard protocols reinforce perimeter protection. The China Data Center Physical Security Market embraces monitoring and detection solutions integrating fire, smoke, and temperature alerts. Vendors innovate in edge-based video storage and smart response algorithms. These technologies increase operational transparency and safeguard critical assets.

By Services

System integration holds the largest share due to complex infrastructure setups across multiple layers. Consulting services expand with new regulatory and compliance requirements. Maintenance and support grow as data centers adopt 24/7 operation models. The China Data Center Physical Security Market values reliable technical partnerships for lifecycle management. Firms offering end-to-end integration and real-time system health checks gain higher market credibility.

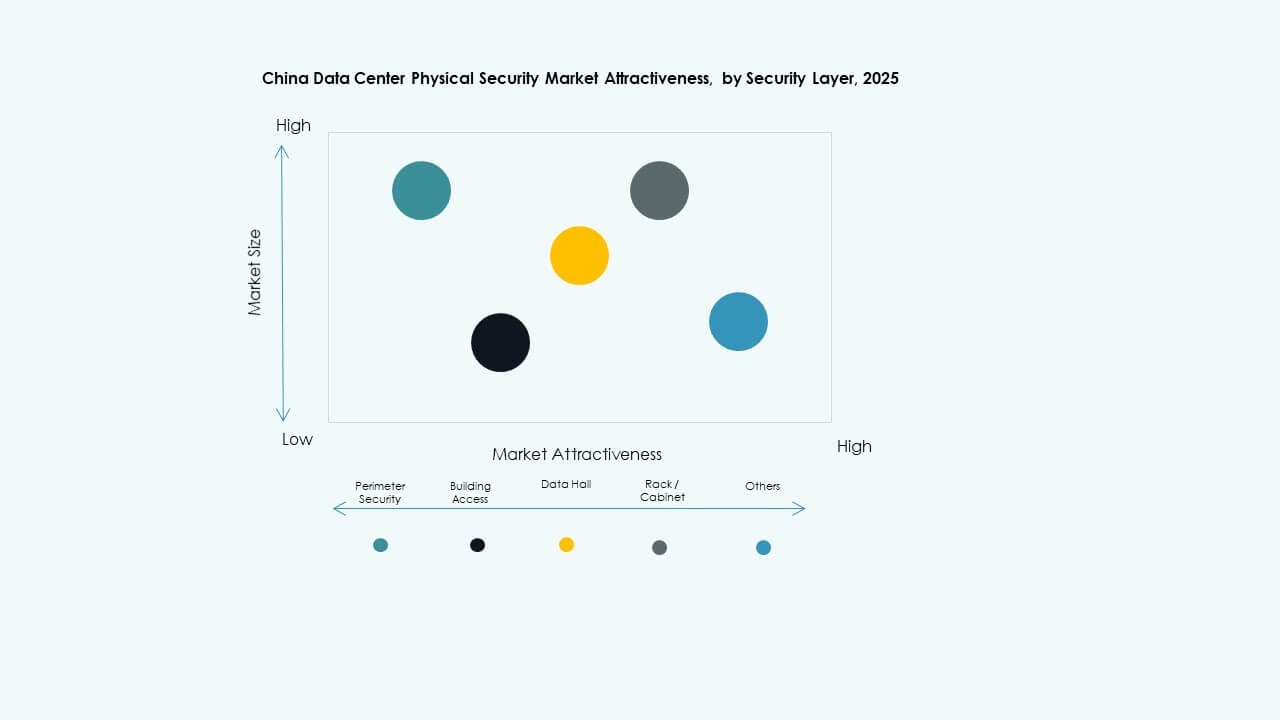

By Security Layer

Perimeter security leads with widespread deployment of sensors, fencing, and surveillance cameras. Building access systems follow with smart biometric entry points. The China Data Center Physical Security Market benefits from multi-zone defense extending to racks and cabinets. Data halls demand stricter access protocols to protect critical processing zones. Comprehensive integration across layers enhances response speed and data integrity.

By Data Center Type

Hyperscale facilities dominate the segment with continuous investments in large-scale security infrastructure. Colocation centers follow, driven by tenant diversification and shared security standards. Enterprise and edge data centers show high adaptability to modular systems. The China Data Center Physical Security Market gains momentum as operators align system designs with performance and compliance needs. Hybrid deployments link centralized and distributed architectures efficiently.

By End-user

IT and telecom sectors lead adoption due to critical infrastructure protection needs. BFSI and government agencies follow with strict security policies. Healthcare and manufacturing sectors show rising investment in secured storage. The China Data Center Physical Security Market grows as e-commerce and retail players strengthen access control. Multi-sector collaboration fosters steady technological adoption across regions.

Regional Insights

Regional Insights

Eastern China Dominating with 45% Market Share

Eastern China, led by Shanghai and Jiangsu, accounts for about 45% of the China Data Center Physical Security Market. Strong cloud infrastructure and financial hubs accelerate deployment. High-density industrial clusters demand advanced perimeter and building security systems. The concentration of hyperscale projects increases technology innovation. It remains a focal area for international partnerships and local manufacturing expansion. Investors prioritize this region for high-return opportunities.

- For instance, China Telecom is building a large hyperscale data center in Shanghai’s Lingang area with plans for about 40,000 high-power racks. The facility incorporates advanced liquid-cooling technology and targets a power usage effectiveness (PUE) of around 1.3, aligning with China’s efficiency standards for next-generation data centers.

Northern China Capturing 30% with Government-backed Projects

Northern China, including Beijing and Tianjin, holds around 30% share supported by state-owned digital infrastructure. Government data centers and research facilities integrate AI-driven surveillance frameworks. The region benefits from policy-driven funding for defense-grade security technologies. It plays a strategic role in cybersecurity and cloud sovereignty initiatives. The local ecosystem encourages R&D in smart access control. It maintains consistent growth driven by national security demand.

Southern and Western China Emerging with 25% Market Share

Southern and Western provinces, including Guangdong and Sichuan, contribute nearly 25% of total market value. Expansion of industrial parks and digital manufacturing zones fuels growth. Regional governments encourage secure digital transformation through special incentives. It supports adoption of modular and energy-efficient surveillance systems. The market benefits from the growing presence of edge and colocation facilities. These regions attract emerging vendors focusing on regional service delivery.

- For instance, Guangdong province plans to deploy about 1 million server racks by 2025 within clustered industrial parks. These upcoming facilities focus on energy efficiency with power usage effectiveness (PUE) targets below 1.3 and use modular, liquid-cooled designs to improve performance and reduce costs.

Competitive Insights:

- Bosch Sicherheitssysteme GmbH

- Honeywell International Inc.

- Johnson Controls

- Schneider Electric SE

- Axis Communications AB

- Dahua Technology Co. Ltd.

- Siemens AG

- Fortinet

- Genetec

- Securitas AB

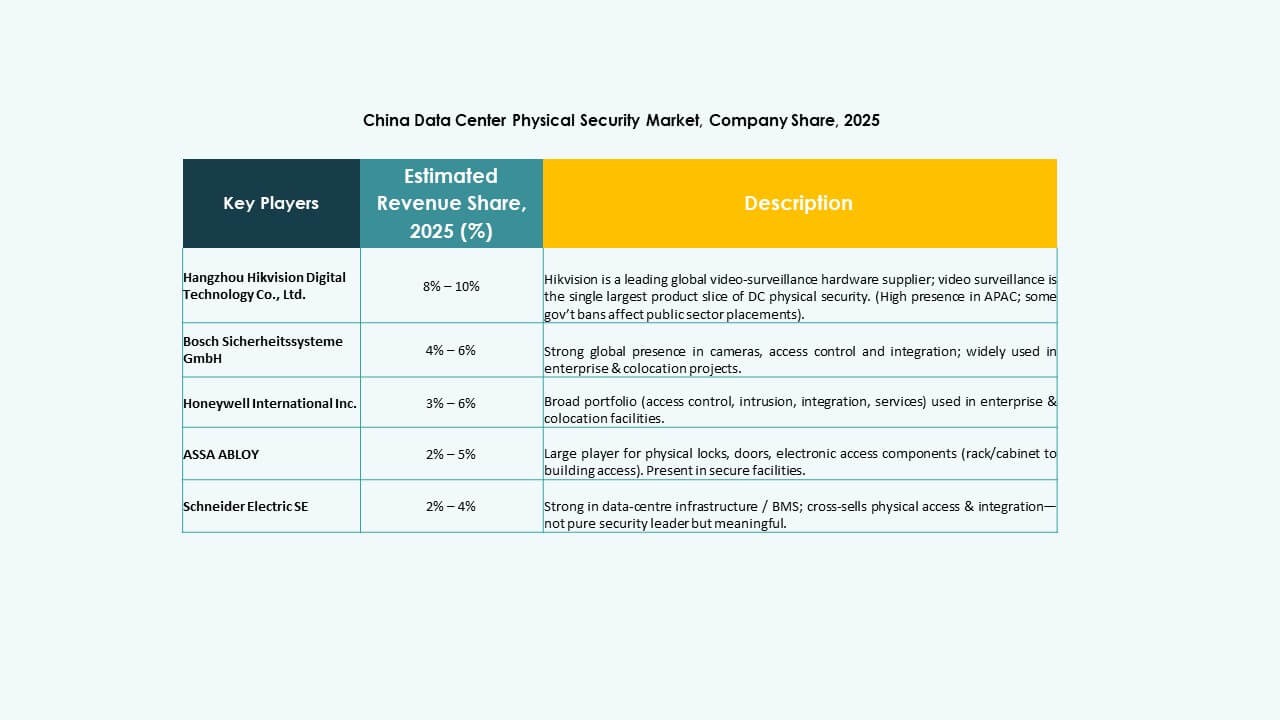

The China Data Center Physical Security Market features strong competition among global and domestic players focused on integrated surveillance, access control, and AI-driven monitoring systems. It is shaped by technology convergence and regulatory compliance influencing vendor positioning. Bosch, Honeywell, and Schneider Electric lead with comprehensive end-to-end security portfolios, while Dahua and Axis strengthen regional dominance through camera and analytics solutions. Johnson Controls and Siemens expand through automation and smart infrastructure integration. Fortinet and Genetec focus on cyber-physical convergence to enhance system resilience. Strategic collaborations, local manufacturing, and compliance alignment define success in this growing market.

Recent Developments:

- In October 2025, ASSA ABLOY acquired Kentix GmbH, a German company specializing in monitoring and access control products designed for data centers, enhancing their capabilities in physical security for this sector.

- In January 2025, ASSA ABLOY also acquired InVue, a Charlotte-based provider of asset protection and access control solutions, aligning with their strategy to expand globally in access control and asset protection.

- In June 2024, Honeywell International Inc. completed the acquisition of Carrier Global Corporation’s Global Access Solutions business for $4.95 billion, enhancing its building automation portfolio with advanced access control solutions like LenelS2, Onity, and Supra, which support security needs in data centers including those in Spain.

- In December 2024, Bosch Sicherheitssysteme GmbH sold its security and communications technology product business to the European investment firm Triton. The transaction included three business units Video, Access and Intrusion, and Communication as Bosch aims to focus more on systems integration business.