Executive summary:

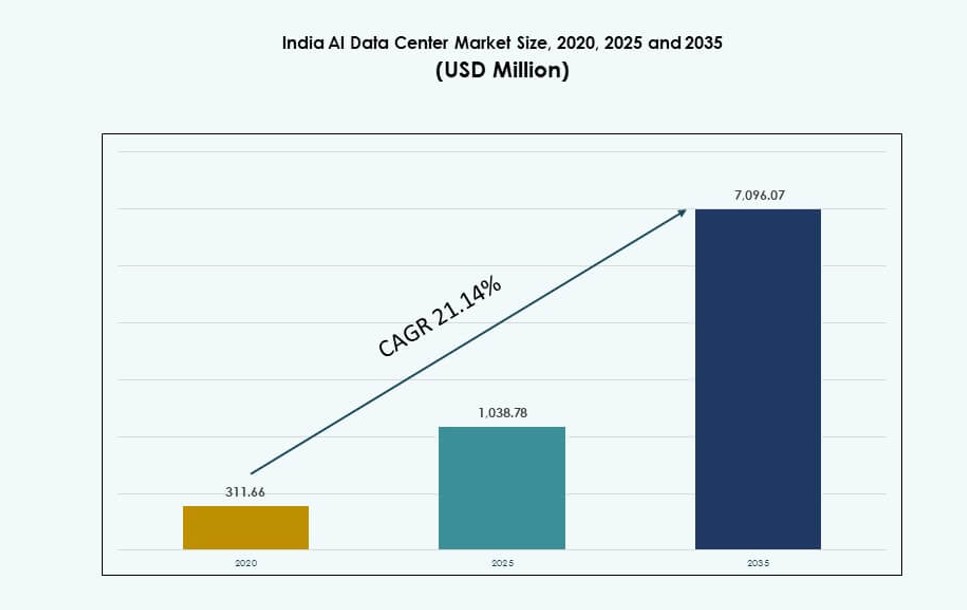

The India AI Data Center Market size was valued at USD 311.66 million in 2020 to USD 1,038.78 million in 2025 and is anticipated to reach USD 7,096.07 million by 2035, at a CAGR of 21.14% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2035 |

| India AI Data Center Market Size 2025 |

USD 1,038.78 Million |

| India AI Data Center Market, CAGR |

21.14% |

| India AI Data Center Market Size 2035 |

USD 7,096.07 Million |

Rising demand for GPU infrastructure, AI model training, and sovereign cloud services is reshaping digital infrastructure strategies. Businesses are shifting to hybrid AI-native environments to support real-time analytics and generative AI. Government-backed initiatives like Digital India and AI Mission India are fostering rapid compute capacity growth. Enterprises across banking, telecom, and healthcare are deploying AI-driven applications. This demand has made India a high-priority AI data center investment destination for both domestic and global operators. Strategic investors recognize the market’s scale, energy advantage, and growing regulatory clarity.

Western India leads the India AI Data Center Market, with Mumbai and Pune accounting for the largest hyperscale capacity due to subsea cable landings and enterprise density. Southern India, led by Bengaluru, Chennai, and Hyderabad, follows closely, backed by strong talent availability and cloud availability zones. Northern India is emerging with government-backed parks in Noida and Lucknow. Central and Eastern regions show rising interest through greenfield deployments and smart city rollouts.

Market Dynamics:

Market Drivers

Rapid Growth of Domestic AI Workloads Across Key Economic Sectors

India’s AI landscape is expanding due to sector-wide digitization and deep learning adoption. Financial services, healthcare, and manufacturing are investing in AI for automation and analytics. This shift is generating strong demand for local compute power. Public cloud providers and private enterprises are turning to domestic AI data centers to reduce latency. Deployment of large language models, recommendation systems, and AI inference tools is rising. The India AI Data Center Market supports these dynamic needs with scalable, GPU-enabled environments. Government-led data localization policies further strengthen onshore demand. Investors see high-value infrastructure returns from supporting India’s AI transformation.

Digital Public Infrastructure and AI-First Policy Interventions

India Stack, Aadhaar, and UPI have built digital rails supporting large-scale AI applications. National platforms for education, health, and governance use data-intensive models. The India AI Data Center Market supports sovereign infrastructure aligned with AI-specific compute requirements. Strategic initiatives like the India AI Mission and Digital India push compute decentralization. These interventions incentivize new zones and promote private partnerships. It enables regional innovation and builds long-term data center demand. AI-first policy design ensures strong institutional compute needs. Investors benefit from regulatory clarity, national focus, and ecosystem maturity.

- For instance, in October 2025, AdaniConneX and Google announced plans for India’s largest AI data center campus, integrating fiber optic networks and green power to support public and sovereign AI infrastructure.

Enterprise Cloud Migration with AI-Native Architecture Requirements

Indian enterprises are upgrading legacy systems to AI-ready digital cores. This trend fuels demand for hybrid and cloud-native infrastructure optimized for AI training and inference. The India AI Data Center Market addresses these performance needs with purpose-built facilities. Support for high-density GPU clusters, liquid cooling, and AI-specific workload scheduling is key. SaaS platforms, fintechs, and media firms need low-latency, high-throughput environments. Colocation and hyperscale models offer flexibility and efficiency. Businesses are adopting zero-trust frameworks and sovereign data zones. These trends lock in long-term enterprise demand for AI infrastructure.

AI Ecosystem Expansion through Startups, Academia, and Public Cloud Providers

India’s AI ecosystem includes over 3,000 startups, many working on vertical-specific models. Universities and research institutes develop homegrown AI stacks. Public cloud players invest in regional AI zones to serve this ecosystem. The India AI Data Center Market enables GPU access, elastic scale, and secure hosting for such users. Incubators and accelerators require flexible capacity at lower cost. AI-focused platforms integrate infrastructure-as-a-service models to scale innovation. India’s talent pool and developer community further boost usage intensity. This cycle of innovation and infrastructure demand creates strong market fundamentals.

- For instance, RackBank began construction of India’s first AI Data Center Park in Nava Raipur in 2025, offering GPU-as-a-service infrastructure for startups and academic research clusters working on deep learning and NLP models.

Market Trends

Widespread Shift Toward Liquid Cooling and High-Density Rack Deployments

Operators in the India AI Data Center Market are deploying liquid cooling to handle thermal loads from GPU-intensive racks. Traditional air cooling fails at densities beyond 40 kW per rack. New builds are adopting direct-to-chip and rear-door heat exchanger systems. These solutions improve energy efficiency and rack consolidation. The shift enables support for advanced model training workloads. Data centers can now deliver up to 100 kW per rack, reducing space and improving performance. This trend aligns with global AI data center design evolution. It gives India’s operators a competitive infrastructure edge.

Integration of AI Infrastructure with Green Power and Sustainability Goals

AI compute needs raise energy demand, pushing operators to prioritize renewable sourcing. The India AI Data Center Market is seeing strong traction in power purchase agreements (PPAs) with solar and wind developers. Facilities in Tamil Nadu, Gujarat, and Karnataka are leveraging regional RE capacity. Green building certifications and water-saving cooling systems are becoming common. Power usage effectiveness (PUE) targets are set below 1.3 for new AI centers. ESG-driven investors and hyperscale clients favor sustainable builds. This trend aligns performance with environmental compliance and long-term operating cost savings.

Localization of AI Zones Near Strategic Cloud and Connectivity Hubs

Data center operators are clustering AI capacity near undersea cable landing stations and cloud availability zones. Mumbai, Chennai, and Hyderabad lead with access to global connectivity and cloud infrastructure. The India AI Data Center Market benefits from proximity to hyperscale regions operated by AWS, Azure, and Google Cloud. This localization reduces latency and ensures direct access to AI services. Enterprises use these zones for hybrid deployments with public cloud peering. AI model training, inferencing, and edge AI workloads benefit from proximity and integration.

Specialized AI Infrastructure-as-a-Service Offerings by Indian Providers

Indian cloud and colocation providers are launching infrastructure offerings tailored for AI developers and enterprises. These platforms include pre-configured NVIDIA DGX nodes, GPU bare-metal access, and AI workload orchestration tools. The India AI Data Center Market is diversifying its service portfolio beyond general compute. Providers now offer elastic scaling for AI jobs, deep integration with MLOps platforms, and custom tuning environments. This shift addresses demand from startups, research institutions, and enterprises. It reflects a maturing AI stack supported by robust backend infrastructure.

Market Challenges

Power Availability, Grid Reliability, and High Energy Costs in Urban Zones

AI data centers require continuous, high-density power, which stresses India’s urban grid infrastructure. Mumbai and Bengaluru face transmission constraints and voltage fluctuations. The India AI Data Center Market must navigate these challenges with onsite generation and storage. Backup systems, diesel fuel dependency, and limited RE access inflate costs. Operators must secure long-term power contracts to avoid disruptions. High capex on electrical infrastructure adds financial burden. Policies for grid modernization and energy trading remain complex. These factors limit rapid scale-up in high-demand areas.

Talent Shortages in AI Infrastructure Operations and Engineering Roles

India produces strong software and AI talent but lacks experienced professionals in data center operations. Managing AI-specific facilities requires advanced electrical, thermal, and workload orchestration skills. The India AI Data Center Market faces hiring gaps in design engineers, DCIM professionals, and thermal system specialists. Training programs and certifications are limited to metro cities. Retaining skilled staff is costly due to global demand. This shortage slows operational readiness and scalability. Bridging this gap is critical to ensuring performance and uptime for AI infrastructure.

Market Opportunities

Emergence of Edge AI and 5G-Driven Regional Compute Demand

India’s 5G rollout is pushing AI inference to the edge. Use cases in smart cities, retail, and logistics need real-time AI processing. The India AI Data Center Market can benefit by deploying micro and modular AI nodes across Tier II and Tier III cities. These edge units support low-latency workloads, reducing dependence on central hubs. Telecom operators and smart infrastructure firms are key customers.

Strategic Opportunity for Sovereign AI Cloud and Model Hosting

Policy momentum around data sovereignty is creating space for India-based AI cloud stacks. Enterprises and government bodies want localized model training and inferencing. The India AI Data Center Market supports sovereign GPU clusters and compliance-ready environments. Indian cloud firms can host foundational models aligned with national policy frameworks. This opportunity attracts enterprise AI buyers seeking secure, local infrastructure.

Market Segmentation

By Type

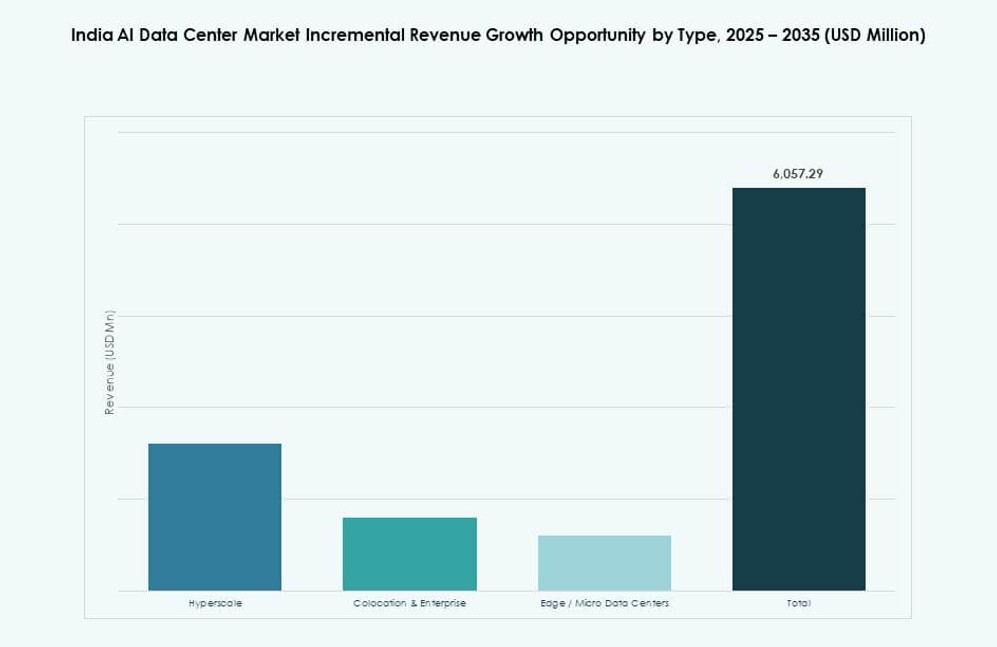

Hyperscale is the dominant segment in the India AI Data Center Market, driven by demand from global cloud service providers and large enterprises. These facilities offer the scale, power, and redundancy needed for AI training. Colocation & Enterprise models are growing, serving banking, retail, and SaaS providers with tailored deployments. Edge/Micro Data Centers are emerging to support low-latency inference in remote or urban nodes.

By Component

Hardware holds the largest share due to investment in high-density servers, GPUs, and power infrastructure. AI workloads demand specialized components like NVIDIA H100s, direct liquid cooling, and advanced switching fabrics. Software & Orchestration is rising with MLOps integration and AI workload management tools. Services are key for deployment, tuning, and operations support, especially for mid-sized firms.

By Deployment

Hybrid deployment is most preferred in the India AI Data Center Market, balancing cloud scale and data control. Large firms integrate on-premise infrastructure with cloud AI platforms for flexibility. Cloud-only deployments are strong in tech and startup segments. On-premise remains relevant in government and regulated industries that require full data control and compliance.

By Application

Machine Learning dominates due to widespread adoption in customer analytics, fraud detection, and automation. Generative AI is growing fast, fueled by demand for LLMs, copilots, and creative tools. NLP sees strong uptake in contact centers, search, and chatbots. Computer Vision supports manufacturing, logistics, and retail. Others include graph learning and time-series forecasting.

By Vertical

IT and Telecom lead the India AI Data Center Market, driven by hyperscalers, SaaS firms, and telcos adopting AI. BFSI follows, using AI for risk scoring, customer analytics, and automation. Healthcare uses AI for imaging, diagnostics, and population health models. Retail, Manufacturing, and Media use AI for personalization and production optimization. Government and automotive segments show emerging demand.

Regional Insights

Western India – Leading with Hyperscale Clusters and Connectivity Infrastructure

Western India dominates with a 43% share of the India AI Data Center Market. Mumbai and Pune lead due to undersea cable landing stations, data localization demand, and strong industrial ecosystems. Gujarat is attracting hyperscale investments with renewable power and industrial land. The region’s edge lies in global connectivity, established cloud zones, and financial services demand.

- For instance, Yotta Infrastructure’s NM1 facility in Navi Mumbai, operational since 2020, supports 7,200 racks across 820,000 sq. ft. with 50 MW IT power capacity.

Southern India – Growth Driven by Talent, Cloud Zones, and Policy Support

Southern India holds around 32% share, with Bengaluru, Chennai, and Hyderabad as major hubs. Bengaluru offers deep talent pools and R&D ecosystems, while Chennai supports power-intensive AI centers with access to renewable energy and port infrastructure. Telangana’s proactive policy and data center incentives attract major operators. Strong IT exports and startup ecosystems drive sustained demand.

- For instance, the Chandanvelly campus is engineered for ultra‑high density racks (up to ~135 kW per rack) and advanced cooling technologies to handle AI and cloud compute demands.

Northern and Eastern India – Emerging Zones with Targeted State Incentives

Northern and Eastern India together contribute roughly 25% of the India AI Data Center Market. Noida and Gurugram are growing with government support and proximity to the national capital. Kolkata and Bhubaneswar offer affordable land and state incentives for new facilities. Regional diversity in demand, availability of Tier II/III cities, and 5G rollout present long-term opportunities for AI-specific infrastructure.

Competitive Insights:

- Yotta Infrastructure

- CtrlS Datacenters

- STT GDC India

- AdaniConneX

- Amazon Web Services (AWS)

- Microsoft (Azure)

- Google Cloud

- Equinix

- Digital Realty Trust

- NVIDIA

The India AI Data Center Market features a mix of domestic infrastructure leaders and global hyperscale cloud providers. Yotta, CtrlS, and STT GDC India dominate with expansive campuses tailored for high-density AI workloads. AdaniConneX is scaling aggressively through renewable-backed data parks. AWS, Microsoft, and Google Cloud maintain strong regional presence with hyperscale availability zones. Global colocation firms like Equinix and Digital Realty bring modular capacity and international connectivity. Technology enablers such as NVIDIA play a critical role by supplying AI-optimized GPUs and system architectures. The competitive focus is shifting toward liquid cooling, green energy integration, and AI-specific infrastructure services. It reflects a landscape driven by sovereign hosting needs, cloud demand, and scalable GPU availability.

Recent Developments:

- In May 2025, RackBank Datacenters Pvt Ltd broke ground on India’s first AI data center park in Sector-22, Nava Raipur, spanning 5.5 hectares with GPU-based computing. The ₹2,000 crore project starts at 5 MW capacity, scalable to 150 MW, and expects to create 500 direct jobs.

- In January 2025, Microsoft announced a $3 billion investment in cloud and AI infrastructure, including new data centers across India over two years. Partnerships with RailTel, Apollo Hospitals, Bajaj Finserv, and others target AI adoption in sectors like railways and healthcare.

- In January 2025, CtrlS Datacenters announced plans to develop a 40-acre data center campus in Chandanvelly Industrial Park near Hyderabad, aligning with its AI-driven capacity expansion.