Executive summary:

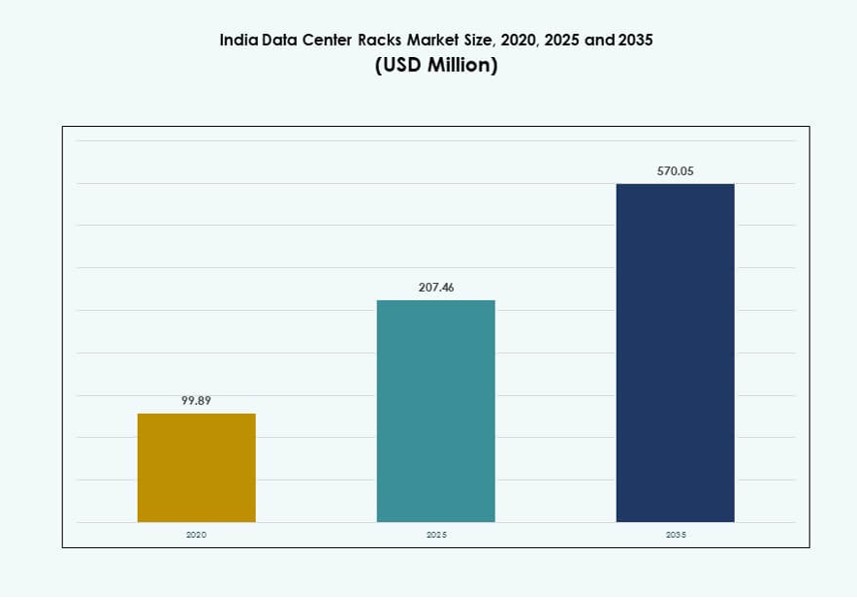

The India Data Center Racks Market size was valued at USD 99.89 million in 2020 to USD 207.46 million in 2025 and is anticipated to reach USD 570.05 million by 2035, at a CAGR of 10.61% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2035 |

| India Data Center Racks Market Size 2025 |

USD 207.46 Million |

| India Data Center Racks Market, CAGR |

10.61% |

| India Data Center Racks Market Size 2035 |

USD 570.05 Million |

Rising demand for cloud services, AI workloads, and edge computing is driving rapid adoption of advanced rack systems. Organizations seek modular, scalable racks that support high-density deployments and integrated cooling. Adoption of prefabricated and intelligent rack solutions is expanding, particularly in colocation and hyperscale environments. Policy-driven digital infrastructure and data localization initiatives further strengthen market demand. Investors focus on energy-efficient rack systems with reduced total cost of ownership. These shifts reinforce the strategic relevance of rack infrastructure for hyperscale scalability, resilience, and regulatory compliance across India’s digital economy.

Western India leads the market with strong presence in Mumbai and Pune, supported by submarine cables, cloud zones, and financial sector needs. Southern cities such as Chennai and Hyderabad are rising hubs due to hyperscaler expansions and favorable infrastructure. Northern India is growing steadily, led by Delhi NCR’s enterprise ecosystem. Eastern and Tier-2 cities are emerging regions, driven by edge deployments and state-level digitalization projects. This geographic spread reflects a nationwide acceleration in data center rack adoption.

Market Dynamics:

Market Drivers

Growing Demand for High-Density Racks Driven by Cloud and AI Workloads

The India Data Center Racks Market is witnessing strong demand for high-density racks as enterprises adopt AI, machine learning, and big data analytics. These workloads need higher power, optimized airflow, and efficient rack-level designs. Organizations are integrating GPUs and accelerators, which raise thermal output and space utilization. High-density racks support more servers per square foot, cutting floor space and energy costs. It enables hyperscale providers to scale quickly while maintaining operational efficiency. Cloud service providers and colocation operators lead this transition to higher-density configurations. Rack vendors are innovating with modular and prefabricated systems for faster deployment. Strategic investments in AI-ready racks are rising. It positions India as a vital growth zone for rack infrastructure.

- For instance, CtrlS Datacenters operates Tier IV-certified data center facilities in Mumbai designed for high-density workloads with N+1 redundancy. These facilities support GPU-based compute environments and advanced cooling architectures required for AI and cloud-driven applications.

Digital Transformation and Edge Deployments Reshaping Rack Design Preferences

Digital transformation across public and private sectors continues to push rack-level infrastructure upgrades. Edge computing adoption is expanding rack demand in Tier-2 and Tier-3 cities, where latency-sensitive applications need localized compute. These deployments often use compact, modular racks for fast setup and remote manageability. Organizations in retail, manufacturing, and telecom sectors prioritize space-efficient racks with built-in cooling and power distribution. Prefabricated micro data centers further drive demand for 19-inch and 23-inch racks. IT teams now prefer smart racks that support asset tracking and environmental monitoring. Rack systems with inbuilt DCIM compatibility are gaining traction. It reflects how India Data Center Racks Market is adapting to distributed architectures.

Policy Push, Data Sovereignty, and Localization Fuel Domestic Infrastructure Growth

The India Data Center Racks Market benefits from strong regulatory and policy support. Government schemes promoting data localization, digital governance, and sovereign cloud drive new rack infrastructure projects. Key policies such as the Digital India initiative and National Data Centre policy are catalyzing investment. Telecom and banking firms face compliance mandates to store and process data locally. This increases demand for secure and scalable rack systems within domestic facilities. Colocation firms are expanding rack footprints to meet rising enterprise requirements. State governments are offering land, power subsidies, and single-window clearances. It creates a favorable business case for investors and operators building rack-ready facilities.

- For instance, Yotta Infrastructure’s NM1 facility in Navi Mumbai is Tier IV certified, supporting 7,200 racks with 50 MW capacity. It caters to data sovereignty needs across BFSI, government, and enterprise sectors in India.

Investor Interest in Modular, Scalable, and Energy-Efficient Rack Solutions

Investors and data center developers prioritize rack solutions that lower deployment time and improve space utilization. Scalable racks support phased capacity addition while reducing upfront costs. Modular systems enable flexible configurations based on power, cooling, and compute needs. This approach suits hyperscalers, BFSI, and e-commerce players scaling compute infrastructure across regions. Energy-efficient racks integrated with thermal containment and airflow optimization are in demand. These racks reduce total cost of ownership while meeting ESG targets. Suppliers offering quick-to-deploy, pre-engineered rack systems attract more partnerships. The India Data Center Racks Market is now central to strategic infrastructure portfolios for both domestic and foreign investors.

Market Trends

Rising Adoption of Smart Racks with Integrated Monitoring and Remote Management

Organizations across sectors are adopting smart racks equipped with sensors and remote management modules. These racks support real-time tracking of temperature, humidity, power usage, and server activity. Facility operators use integrated dashboards for predictive maintenance and capacity planning. Adoption of DCIM and AI-based optimization is increasing. This allows proactive fault detection and thermal management. Smart racks also help reduce operational downtime. Remote management tools gain traction in edge locations with limited on-site staff. The India Data Center Racks Market is moving toward intelligent infrastructure that supports real-time visibility and control.

Shift Toward Custom Rack Designs for Hyperscale and AI-Specific Deployments

Hyperscalers are designing custom racks tailored for GPU clusters, liquid cooling, and AI workloads. These racks often exceed 42U in height and support power densities beyond 30 kW. Customization includes enhanced airflow, cable routing, and immersion-ready features. Design flexibility helps operators balance compute needs with energy constraints. AI models require dense compute and memory, driving specialized rack formats. Cloud providers and ODMs collaborate on rack design standardization. The India Data Center Racks Market is seeing strong uptake of these non-standard, high-performance racks across key metros.

Rack Infrastructure Expansion in Tier-2 Cities to Support Edge and Regulatory Compliance

Infrastructure growth is moving beyond major metros into Tier-2 and Tier-3 cities. Enterprise demand, edge nodes, and sovereign cloud needs fuel localized rack deployment. Compact modular racks are used in retail banking, logistics, and telecom sectors for low-latency operations. Regional governments promote data center ecosystems with policy incentives. Power and fiber availability are improving in secondary cities. This decentralization increases rack demand in places like Kochi, Nagpur, and Bhubaneswar. The India Data Center Racks Market reflects this geographic dispersion of rack deployment.

Growing Preference for Sustainable Racks and Circular Infrastructure Models

Sustainability goals are reshaping how racks are designed and deployed. Operators are choosing recyclable materials, modular designs, and longer lifecycle components. Sustainable racks reduce e-waste and offer better airflow for energy savings. Circular infrastructure strategies include refurbishing and reusing older racks. Certification standards now include environmental impact benchmarks. Rack vendors with green certifications gain preference in RFPs. It helps clients meet ESG reporting goals. The India Data Center Racks Market is aligning with global sustainability mandates through design innovation.

Market Challenges

Inconsistent Power and Infrastructure in Emerging Zones Slows Rack Expansion

Power quality, cooling infrastructure, and fiber availability remain weak in several Tier-2 and Tier-3 locations. Edge deployments need consistent uptime, but voltage fluctuations and outages pose a risk. Limited access to reliable backup systems affects rack utilization efficiency. Land acquisition delays and fragmented regulatory clearances extend setup timelines. High costs of high-density thermal containment limit small players. These infrastructure gaps impact the pace of rack installation and scalability. The India Data Center Racks Market needs stronger policy coordination and utilities modernization to meet growing demand in emerging zones.

High Initial Investment and Skill Shortage Limit Smart Rack Adoption at Scale

Advanced racks with integrated DCIM, sensors, and modular cooling carry a high upfront cost. Small and mid-sized data centers hesitate to invest in premium rack systems. Budget constraints lead to extended use of legacy open-frame racks. Skilled professionals for thermal planning, power provisioning, and smart rack deployment are in short supply. Training programs for data center infrastructure roles remain limited. Slow integration with BMS and network systems adds complexity. The India Data Center Racks Market must overcome financial and human capital constraints to support widespread intelligent rack adoption.

Market Opportunities

Edge and AI Workloads Open New Rack Deployment Frontiers in Regional Markets

Edge computing for low-latency use cases creates strong demand for compact, modular, and prefabricated racks. These deployments in BFSI, manufacturing, and retail support localized processing and reduce data transmission costs. AI training clusters need racks supporting high thermal loads, liquid cooling, and flexible form factors. Investments in 5G, IoT, and regional cloud nodes drive this trend. The India Data Center Racks Market is well-positioned to meet these evolving architecture needs.

Make-in-India Initiatives and Vendor Localization Improve Rack Supply Ecosystem

Policies promoting local manufacturing and value addition enable rack OEMs to set up domestic production. This reduces lead time, lowers costs, and creates export opportunities. Government incentives for electronics and hardware manufacturing help domestic rack vendors scale operations. It supports job creation and strengthens India’s strategic tech supply chain. The India Data Center Racks Market benefits from this growing localization wave.

Market Segmentation

By Rack Type

The cabinet segment dominates the India Data Center Racks Market due to rising use in hyperscale and colocation environments. Cabinets provide better airflow control, physical security, and structured cabling options compared to open-frame racks. Open-frame racks are still used in small data rooms for their cost-effectiveness and accessibility. However, demand for enclosed cabinet racks is growing due to heat management needs, especially in high-density server rooms.

By Rack Height

The 42U segment leads the India Data Center Racks Market, driven by its industry-standard compatibility and flexibility across applications. It balances capacity, ergonomics, and manageability for most enterprise and colocation setups. The above 42U segment is gaining traction with hyperscale deployments where compute density and vertical space utilization are critical. Below 42U racks are preferred in edge and retail use cases where space is constrained.

By Width

The 19-inch width segment holds the highest market share due to global standardization and compatibility with most IT equipment. These racks are widely adopted across industries and provide easy integration with servers, switches, and power units. The 23-inch segment is used in telecom and networking setups where wider equipment is deployed. Demand for wider racks may grow with increased GPU and AI deployments in the India Data Center Racks Market.

By Application

Server racks dominate the India Data Center Racks Market, supported by rising cloud, AI, and virtualization workloads. These racks host blade and rack servers in both enterprise and hyperscale environments. Network racks hold a smaller share but remain essential for switchgear, routers, and telecom cabinets. Demand for network racks will grow as edge and 5G deployments expand across regions.

By End-User

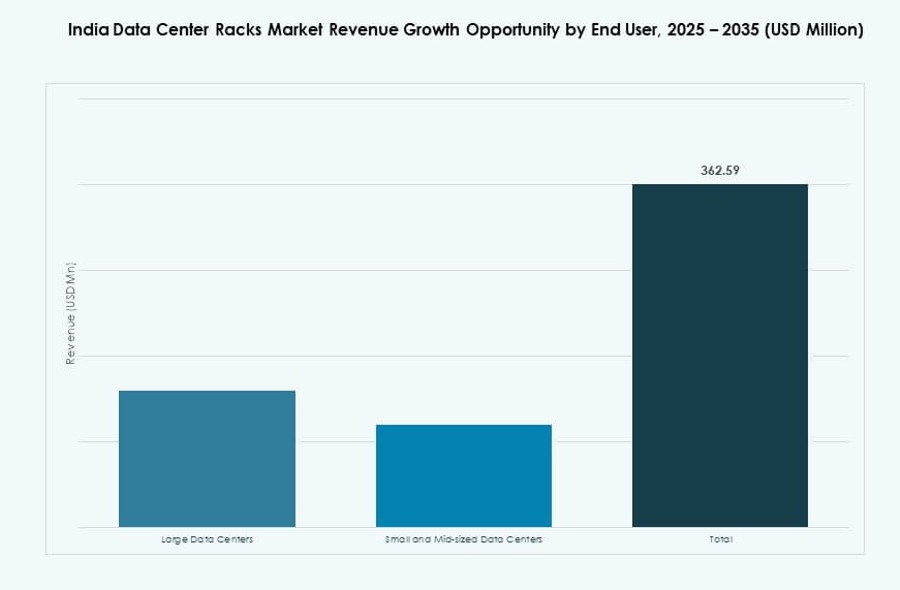

Large data centers are the leading end-users due to high-volume procurement, complex workloads, and multi-rack configurations. Colocation, hyperscale, and telecom facilities prefer modular, scalable rack systems with high density. Small and mid-sized data centers are adopting standard cabinet racks with basic thermal and power integration. Growth in this segment is driven by enterprise digitization and edge infrastructure in non-metro cities.

By Vertical

The IT & telecom segment leads the India Data Center Racks Market due to large-scale investments in cloud, edge, and connectivity infrastructure. BFSI follows closely, with strong demand for secure, high-availability rack systems supporting regulatory compliance. Healthcare and government are emerging verticals as digital records, telemedicine, and governance platforms expand. Energy and retail segments are also adopting compact and smart racks for distributed sites.

Regional Insights

Western India Leads with 38% Share, Driven by Hyperscaler Presence and Connectivity

Western India, led by Mumbai and Pune, dominates the India Data Center Racks Market with around 38% share. Mumbai hosts major hyperscaler zones, subsea cable landings, and financial services data infrastructure. The presence of reliable power, skilled labor, and carrier-neutral facilities attracts global investments. Pune supports backup and edge sites for metro regions. It benefits from lower real estate costs and growing demand for disaster recovery.

Southern Region Holds 29% Share with Rising Activity in Chennai, Hyderabad, and Bengaluru

Southern India accounts for approximately 29% market share, supported by strong IT presence and connectivity. Chennai is a key landing point for international cables, making it ideal for hyperscale builds. Hyderabad is gaining traction due to its pro-investment policies and growing cloud zones. Bengaluru supports enterprise and cloud-native workloads, with demand rising for smart racks. The region benefits from favorable power tariffs and infrastructure readiness.

- For instance, AWS held discussions in 2024 to expand its Hyderabad data center region with an additional $2 billion investment, strengthening infrastructure for high-density rack deployments and AI-driven workloads.

Northern and Eastern Zones Are Emerging, Contributing 33% Combined Share

Northern and Eastern India together contribute around 33% to the India Data Center Racks Market. Delhi NCR leads in the north with colocation and enterprise data center growth. Eastern zones like Kolkata are expanding slowly, driven by BFSI and government projects. These areas face infrastructure gaps but attract new investments due to untapped market potential. Rack deployments are rising in urban clusters and logistics hubs. Rack vendors focus on pre-configured modular systems to address varied regional requirements.

- For instance, AdaniConneX advanced Phase 1 of its 1 GW hyperscale data center campus in Noida during 2024, targeting AI-ready infrastructure and high-density rack deployments for hyperscaler demand.

Competitive Insights:

- AMCO Enclosures

- Dell Inc.

- Hewlett Packard Enterprise Development LP

- NetRack Enclosures

- Rittal

- Schneider Electric

- Valrack

- Vertiv Group

- Cisco Systems, Inc.

- Legrand

The India Data Center Racks Market is highly competitive, with both global manufacturers and local specialists offering a broad range of rack solutions. Global firms such as Schneider Electric, Vertiv, Rittal, and Dell compete on innovation, energy efficiency, and scalability. Local players like Valrack and NetRack Enclosures focus on custom designs, cost efficiency, and quicker deployments tailored for Indian environments. Hyperscale demand is shifting vendor preferences toward high-density, prefabricated, and smart rack systems. Sustainability, thermal performance, and remote monitoring capabilities are now key differentiators. It fosters intense product development, while partnerships with cloud providers and colocation firms drive volume contracts. The India Data Center Racks Market is evolving into a performance-driven ecosystem with rising investments in domestic manufacturing, design flexibility, and modularity.

Recent Developments:

- In August 2025, Google confirmed a USD 6 billion investment for a 1 GW data center campus in Visakhapatnam, Andhra Pradesh, allocating USD 2 billion for renewable energy integration. The project drives demand for high-density, energy-efficient data center racks suited to AI workloads and sustainable designs in the Indian market.

- In July 2025, AWS reiterated its USD 12.7 billion commitment through 2030 for AI-centric data center infrastructure in multiple Indian regions. This expansion supports hyperscale facilities requiring advanced racks for 80-100 kW loads and liquid cooling compatibility.

- In May 2025, Vertiv announced a strategic partnership with RAH Infotech to expand its critical digital infrastructure solutions, including power, thermal, and intelligent management systems for data centers across India. This collaboration targets enterprises, government projects, and data centers, enhancing availability of Vertiv’s rack-integrated technologies through RAH’s distribution network.