Executive summary:

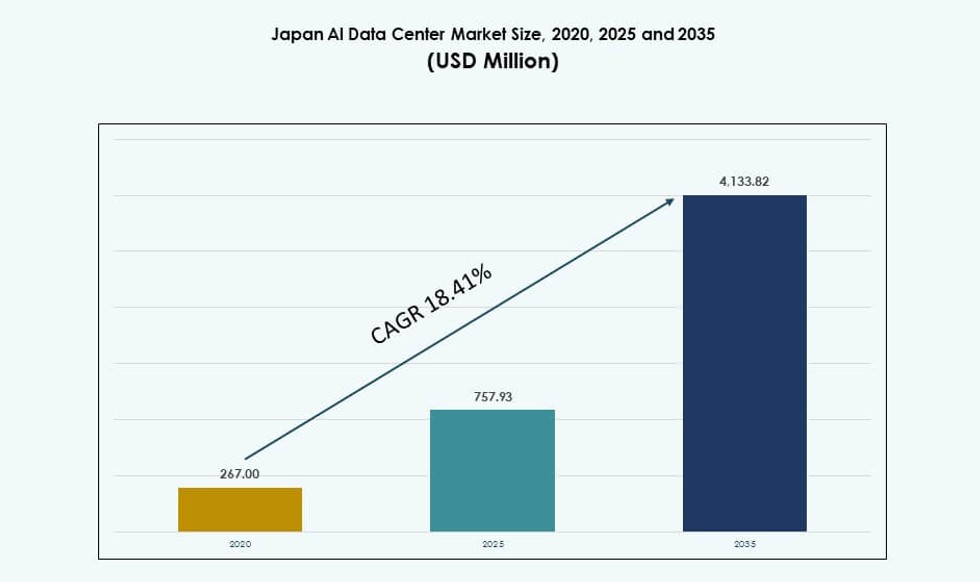

The Japan AI Data Center Market size was valued at USD 267.00 million in 2020 to USD 757.93 million in 2025 and is anticipated to reach USD 4,133.82 million by 2035, at a CAGR of 18.41% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2035 |

| Japan AI Data Center Market Size 2025 |

USD 757.93 Million |

| Japan AI Data Center Market, CAGR |

18.41% |

| Japan AI Data Center Market Size 2035 |

USD 4,133.82 Million |

The market is growing due to rapid digital transformation, strong cloud penetration, and rising AI workload demands. Enterprises are deploying high-density GPU clusters to train and run AI models at scale. Government-led initiatives to promote sovereign AI infrastructure are accelerating localized data center deployments. Investors are drawn to Japan’s stable regulatory environment, high connectivity, and skilled workforce. Innovations in liquid cooling and orchestration software are shaping next-gen infrastructure. Telecom operators and hyperscalers are building scalable facilities with integrated AI tools. Demand for low-latency AI inference and GenAI training is driving capital toward advanced data environments.

Tokyo leads the market with the highest share due to enterprise demand, hyperscaler presence, and connectivity density. Osaka is growing as a secondary AI hub with robust industrial demand and disaster recovery zones. Emerging cities like Fukuoka and Sendai are capturing attention through edge deployments, local incentives, and land availability. These regions offer scalable power and support real-time AI applications closer to end users. The geographic distribution helps balance load, mitigate risk, and extend infrastructure reach. The Japan AI Data Center Market benefits from a multi-region strategy that aligns with both enterprise goals and national digital policies.

Market Dynamics:

Rapid Expansion of AI Workloads Driving Demand for High-Density, AI-Optimized Infrastructure

The Japan AI Data Center Market is experiencing strong demand due to the rapid expansion of AI workloads across sectors. Enterprises are deploying deep learning models for automation, medical diagnostics, smart robotics, and digital twins. These applications require GPU-dense clusters, low-latency interconnects, and scalable compute. Local firms are shifting from legacy cloud to AI-native infrastructure for better performance and control. High memory bandwidth, AI-specific silicon, and energy-efficient cooling are becoming standard deployment criteria. Data centers are being redesigned to support model training at scale. Japan’s technology ecosystem is pushing toward sovereign AI compute capacity. For investors, the combination of demand certainty and capital intensity makes it a long-term strategic opportunity. The Japan AI Data Center Market is becoming essential for firms building advanced AI services and applications.

Government and Industry Initiatives Enhancing AI Infrastructure and National AI Capabilities

The national government is actively promoting digital transformation and AI readiness through dedicated initiatives and subsidies. Programs like the Digital Garden City Nation initiative are creating high-performance regional data infrastructure. Public-private partnerships are funding AI testbeds and industrial AI clouds. Incentives are driving deployment of AI-ready capacity across power-rich zones and tech hubs. Japan’s policy shift toward digital sovereignty and cybersecurity compliance is shaping data center investments. Strategic partnerships with chipmakers, universities, and telecom players are accelerating innovation and deployment. It also aligns with Japan’s ambition to lead in robotics and manufacturing automation powered by AI. The government’s long-term view de-risks private investment into hyperscale and edge AI infrastructure. The Japan AI Data Center Market benefits from these national goals and planning mechanisms.

- For instance, Fugaku, developed by RIKEN and Fujitsu, achieved 442 petaFLOPS on the TOP500 LINPACK benchmark, ranking among the world’s fastest supercomputers. It has been used in various scientific and AI research projects, including drug discovery simulations.

Strategic Investments from Global and Domestic Players Creating a Competitive Infrastructure Landscape

Multinational cloud and colocation providers are expanding aggressively into Japan to meet growing AI infrastructure needs. Major players are investing in AI-optimized facilities with direct liquid cooling, 100 Gbps networks, and modular rack designs. Domestic telecom firms are upgrading legacy data centers into AI-enabled hubs. Strategic land acquisition, zoning approvals, and renewable energy access are shaping location choices. Facilities in Tokyo and Osaka are being built for 30–100 MW of AI-dedicated capacity. Collaboration with semiconductor companies and system integrators is enhancing AI training efficiency. These developments are creating a dense ecosystem of interoperable AI infrastructure. The Japan AI Data Center Market stands out in Asia for its ability to deliver resilient, scalable, and high-throughput environments. It is attracting both hyperscalers and enterprise users.

- For instance, in April 2025, NTT Global Data Centers Japan and TEPCO Power Grid broke ground on a 50 MW data center campus in the Inzai‑Shiroi area near Tokyo. The development is part of NTT’s strategy to expand capacity for future AI and cloud infrastructure, with the first facility scheduled to be operational by 2027.

Rise in Industry-Specific AI Use Cases Driving Tailored Infrastructure Deployments

AI use cases in Japan are expanding beyond tech and finance to manufacturing, automotive, healthcare, and entertainment. These verticals are deploying custom models that demand unique training and inference environments. Factories need edge AI nodes, hospitals require real-time diagnostics, and retail demands fast personalization. This diversity of use cases is encouraging modular, sector-specific data center configurations. Providers are offering optimized platforms that blend AI chips, orchestration tools, and secure connectivity. Vertical alignment is also driving demand for hybrid and on-premise AI compute. The growing AI adoption at scale across sectors creates a sticky demand base for specialized infrastructure. The Japan AI Data Center Market is evolving into a hub for industry-specific AI architecture. It plays a critical role in supporting Japan’s economic digitization goals.

Market Trends

Shift Toward Direct Liquid Cooling and High-Density Racks for AI Training Efficiency

Operators in the Japan AI Data Center Market are moving toward direct liquid cooling to handle high thermal loads. New facilities are being designed to support racks over 50 kW, with customized airflow and coolant loops. Rear door heat exchangers and cold plate liquid cooling are becoming standard in AI deployments. Integration with DCIM platforms allows for real-time thermal monitoring and optimization. This shift improves energy efficiency and reduces space requirements. It supports GPU clusters running large transformer-based models. Facilities in Tokyo and Kansai are already offering high-density colocation for AI startups. The trend reduces operating cost while enabling complex AI training at scale. It signals Japan’s move toward next-gen data center architecture.

Hybrid and Edge Deployments Emerging to Support Low-Latency AI Applications Nationwide

There is rising demand for AI infrastructure at the edge to enable real-time processing in logistics, retail, and smart cities. Telecom firms and edge providers are deploying micro data centers closer to end users. These edge nodes support AI inference for use cases such as surveillance, traffic optimization, and predictive maintenance. Hybrid cloud platforms are gaining popularity to orchestrate workloads across edge and core facilities. Tokyo acts as a central AI hub, while edge sites in Fukuoka, Sapporo, and Nagoya expand national reach. Enterprises are investing in distributed AI infrastructure for latency-sensitive workloads. Standardization and interoperability of edge platforms are improving integration with hyperscale clouds. The Japan AI Data Center Market is supporting a nationwide AI fabric through this trend.

Integration of Renewable Energy and Carbon-Free Goals into AI Data Center Design

Sustainability is becoming a core requirement for AI data center investments in Japan. Operators are integrating onsite solar, grid-sourced renewables, and energy storage systems to meet carbon neutrality goals. AI workloads have high power demands, pushing for green power procurement and PPA contracts. Several hyperscale sites now operate with over 60% renewable energy penetration. Power usage effectiveness (PUE) metrics are optimized through liquid cooling and intelligent power distribution. Companies are publishing sustainability KPIs to meet ESG mandates and attract funding. Smart grids and virtual power plants are also being integrated to stabilize load. The Japan AI Data Center Market is aligning itself with both national energy policy and global sustainability targets. It offers a long-term green growth path.

AI-Native Data Center Software Stack Becoming a Differentiator in Infrastructure Offerings

Operators are embedding AI-native orchestration software into their offerings to handle diverse model workflows. GPU allocation, workload migration, and thermal tuning are increasingly automated using AI-based tools. Container-based platforms with support for Kubernetes CSI plugins are gaining traction. AI fabric managers enable workload-aware scheduling and power optimization across clusters. Observability tools provide real-time insights into latency, performance, and utilization. These platforms reduce cost and complexity for enterprises running large-scale AI operations. Japan-based providers are also localizing stack layers to align with regional compliance standards. The Japan AI Data Center Market is seeing increased value creation through software-driven differentiation. It helps providers deliver more efficient and responsive AI environments.

Market Challenges

Limited Availability of Power, Land, and Grid-Ready Zones for High-Density AI Infrastructure

One of the major challenges in the Japan AI Data Center Market is securing adequate land and power supply. Urban zones like Tokyo and Osaka have limited real estate for large-scale builds. Grid constraints and zoning issues restrict the development of new AI-ready campuses. AI infrastructure demands stable, high-voltage electricity and advanced cooling systems, which are not available in many regions. Energy regulators are cautious about capacity additions, slowing project timelines. Operators face long lead times for substation upgrades and transmission integration. The fragmented energy market adds complexity to power sourcing and pricing. These constraints limit hyperscaler expansion and delay capacity rollouts. The Japan AI Data Center Market must overcome these hurdles to scale efficiently.

Rising Costs, Supply Chain Disruptions, and Talent Shortages Affecting Deployment Timelines

The cost of building and operating AI-ready facilities is rising due to inflation, equipment delays, and global supply issues. High-end GPUs, power modules, and liquid cooling parts face procurement delays. Construction labor shortages and rising wages stretch project budgets and extend build timelines. Skilled AI infrastructure engineers, especially with thermal, network, and orchestration expertise, are in short supply. Regulatory approval processes are also lengthy, especially for large megawatt facilities. Import restrictions and compliance rules for sensitive components increase planning complexity. These risks make it harder for smaller firms to compete or expand rapidly. The Japan AI Data Center Market faces execution barriers that require better coordination and resource planning.

Market Opportunities

Surge in Generative AI Startups and Enterprise Adoption Creating Multi-Tenant Infrastructure Demand

Japan is seeing a sharp increase in GenAI startups, language model developers, and enterprise AI projects. These players prefer renting high-performance infrastructure with low capital investment. This shift favors colocation and cloud providers offering scalable AI environments. Flexible consumption models and GPU-as-a-Service platforms are gaining adoption. The Japan AI Data Center Market is well-positioned to serve this demand with localized, low-latency facilities.

International Partnerships and Sovereign Compute Requirements Opening New Market Segments

Japan’s alignment with data sovereignty and digital trade standards is pushing demand for sovereign AI compute. Partnerships with U.S. and EU tech firms aim to build privacy-compliant, AI-ready capacity. These alliances create growth potential for facilities offering local control, secure routing, and regulatory compliance. The Japan AI Data Center Market can capture value by offering trusted, regulated AI environments.

Market Segmentation

By Type

Hyperscale data centers dominate the Japan AI Data Center Market, driven by demand from cloud giants and national AI platforms. These facilities offer 20 MW to 100 MW of scalable capacity with advanced cooling and interconnects. Colocation and enterprise deployments are growing across sectors needing private AI compute. Edge and micro data centers are emerging to serve retail, mobility, and industrial AI use cases. The hyperscale segment holds the largest share due to centralized AI training needs.

By Component

Hardware forms the largest share of the Japan AI Data Center Market due to the high cost of GPUs, storage, and networking. AI clusters require NVIDIA H100s, InfiniBand networks, and advanced thermal systems. Software and orchestration tools are gaining share as automation and container-based deployment increase. Services such as managed hosting, GPU-as-a-Service, and optimization consulting are growing among mid-market firms. Hardware remains dominant due to upfront capital intensity and compute density.

By Deployment

Cloud deployment leads the Japan AI Data Center Market due to flexibility and scalability offered to GenAI and ML users. Enterprises use hybrid models for regulatory compliance and latency-sensitive inference. On-premise AI deployments are still relevant in manufacturing, defense, and healthcare sectors with strict data privacy norms. Hybrid solutions are increasing in popularity due to their control and portability. Cloud holds the highest market share supported by hyperscaler investments and national cloud strategies.

By Application

Machine Learning and Generative AI are the top applications in the Japan AI Data Center Market, driving demand for GPU-heavy infrastructure. NLP and computer vision also show high adoption in finance, retail, and automotive sectors. GenAI workloads are pushing infrastructure needs for fine-tuning and large-scale inference. Enterprises are deploying AI models across customer service, process automation, and product design. Machine learning holds the largest share, while GenAI grows fastest in volume and intensity.

By Vertical

The IT and Telecom vertical leads the Japan AI Data Center Market due to early adoption of AI in services and operations. BFSI and Manufacturing follow closely, leveraging AI for fraud detection and predictive maintenance. Healthcare is growing rapidly due to AI-led diagnostics and imaging. Media and automotive sectors are investing in GenAI and simulation-based AI. IT and Telecom hold the largest share, driven by hyperscaler cloud platforms and telecom AI workloads.

Regional Insights

Tokyo Metropolitan Region Commands Over 45% Market Share Due to Infrastructure Density and Enterprise Demand

The Tokyo subregion leads the Japan AI Data Center Market with over 45% share due to dense connectivity, financial institutions, and availability of high-quality power. It hosts most hyperscaler campuses and AI-ready zones. Operators are upgrading legacy sites into high-density GPU clusters for large enterprise workloads. The concentration of R&D, AI startups, and regulatory bodies supports a robust ecosystem. It continues to attract new builds for sovereign AI compute and GenAI training hubs.

Kansai Region, Including Osaka, Holds Nearly 30% Share Backed by Redundancy and Industrial AI Use Cases

The Kansai region, led by Osaka, accounts for around 30% of the Japan AI Data Center Market. It is preferred for disaster recovery, energy access, and lower land cost compared to Tokyo. Industrial firms in the region deploy AI for robotics, production control, and logistics. The region supports regional AI cloud infrastructure with 10–30 MW data centers. Osaka is also a strategic location for AI inference nodes serving western Japan. It is becoming a parallel hub to Tokyo.

- For instance, in June 2025, KDDI and HPE announced the launch of an AI-focused data center in Sakai, Osaka, scheduled to begin operations by early 2026. The facility will feature NVIDIA Blackwell GPU systems with direct liquid cooling to support high-performance industrial AI workloads.

Emerging Regional Zones Like Fukuoka and Sendai Capture 15–20% Market Share with Edge and Localized AI Infrastructure

Regional areas such as Fukuoka, Sendai, and Hokkaido make up 15–20% of the market, growing through local government incentives and edge deployments. These zones support AI for smart cities, agriculture, and decentralized healthcare. Edge facilities in these regions handle real-time AI workloads near end users. Power availability and lower real estate costs make them attractive for future AI expansion. The Japan AI Data Center Market benefits from this geographic diversification to balance capacity and resilience.

- For instance, Internet Initiative Japan (IIJ) operates data center facilities in locations including Fukuoka, Tokyo, and Osaka as part of its nationwide infrastructure portfolio. These facilities support cloud and enterprise hosting requirements and contribute to IIJ’s broader strategy in digital infrastructure services.

Competitive Insights:

- NTT Global Data Centers

- MC Digital Realty

- Amazon Web Services (AWS)

- Microsoft (Azure)

- Google Cloud / Alphabet

- Equinix

- Digital Realty Trust

- Colt Data Centre Services

- CoreWeave

- NVIDIA

The Japan AI Data Center Market is highly competitive, led by global hyperscalers, telecom-backed operators, and specialized GPU infrastructure providers. NTT Global Data Centers and MC Digital Realty dominate due to their extensive presence and domestic partnerships. AWS, Microsoft, and Google Cloud continue scaling GPU-rich infrastructure for GenAI and ML workloads. Equinix and Colt offer high-density colocation in Tokyo and Osaka for enterprise AI. New entrants like CoreWeave are expanding to offer AI-specific cloud services. Hardware and systems vendors like NVIDIA and HPE collaborate closely with data center operators to optimize GPU deployments. It remains a capital-intensive market where efficiency, scalability, and regulatory alignment determine leadership. The Japan AI Data Center Market favors players with deep technical expertise, reliable energy access, and sector-specific service portfolios.

Recent Developments:

- In October 2025, Hitachi Ltd. and OpenAI formed a strategic partnership focused on expanding AI data center infrastructure and sustainable operations. The companies signed a Memorandum of Understanding on October 2, 2025, to jointly develop next‑generation AI infrastructure and streamline deployment of advanced AI technologies.

- In August 2025, EdgeConneX expanded its presence with a second data center site acquisition in Japan’s Greater Osaka and Yawata areas. The company announced this landbank expansion to accelerate development of hyperscale data centers supporting cloud and AI workloads. These facilities aim to leverage renewable energy and modern infrastructure to meet growing digital demands.

- In May 2025, Hitachi Systems released three standardized containerized data center models in Japan including high-load, server room, and edge computing options designed for fast deployment of generative AI and cloud workloads.

- On November 2024, Keppel announced that its private fund, Keppel Data Centre Fund II (KDCF II), entered into a sale and purchase agreement with Mitsui Fudosan for the forward purchase of Keppel DC Tokyo 2.