Executive summary:

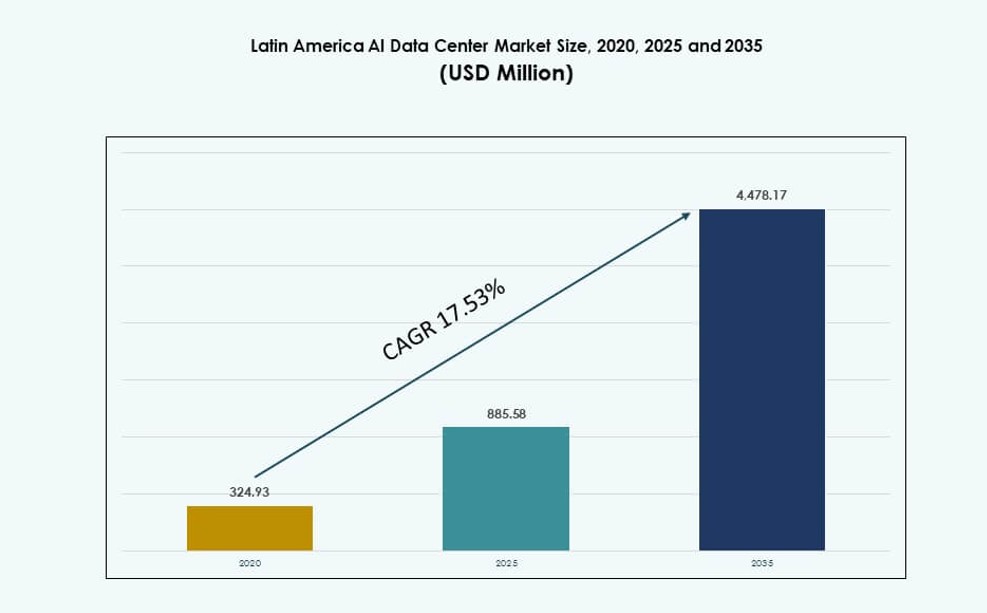

The Latin America AI Data Center Market size was valued at USD 324.93 million in 2020 to USD 885.58 million in 2025 and is anticipated to reach USD 4,478.17 million by 2035, at a CAGR of 17.53% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2035 |

| Latin America AI Data Center Market Size 2025 |

USD 885.58 Million |

| Latin America AI Data Center Market, CAGR |

17.53% |

| Latin America AI Data Center Market Size 2035 |

USD 4,478.17 Million |

Rising enterprise adoption of AI across sectors such as finance, telecom, and public services is driving demand for compute-intensive infrastructure. Regional cloud expansions, GPU-enabled facilities, and edge deployments are accelerating. Governments are also supporting AI strategies with local hosting mandates and tech investments. The Latin America AI Data Center Market is becoming vital for companies seeking low-latency processing, regulatory compliance, and digital innovation at scale.

Brazil leads the regional market due to strong cloud infrastructure, hyperscale investments, and policy alignment. Mexico is also expanding with AI-ready campuses and cross-border cloud zones. Chile, Colombia, and Argentina are emerging markets with local demand, green energy integration, and connectivity through new subsea cables. These trends reflect the growing strategic footprint of AI infrastructure across Latin America.

Market Dynamics:

Market Drivers

Accelerated Digital Transformation Across Enterprises and Public Sector Institutions

The Latin America AI Data Center Market is expanding due to the region’s digital transformation push across industries. Governments and private enterprises are adopting AI to streamline operations and improve citizen and customer services. AI-driven automation in banking, healthcare, and logistics is increasing demand for high-performance computing infrastructure. Governments are investing in smart cities and public digital ID systems that rely on real-time data. These developments require scalable data center environments capable of handling AI workloads. Organizations need fast deployment, which colocation and modular facilities enable. Businesses also seek low-latency solutions to support local AI applications. Public cloud adoption is growing but hybrid setups dominate due to data residency laws. The market is becoming central to Latin America’s digital competitiveness.

Wider Cloud Availability Zones and Regional Infrastructure Expansion

The growing footprint of global cloud providers is reshaping the Latin America AI Data Center Market. AWS, Google Cloud, Microsoft Azure, and Oracle have opened or announced new regions in Brazil, Chile, and Mexico. These developments reduce latency and drive enterprise confidence in deploying AI locally. Enhanced connectivity and backbone networks allow for large-scale model training and inference at regional hubs. Infrastructure providers are also improving power and cooling design to meet the AI load density needs. Strategic location planning considers subsea cable landing stations and access to renewable energy. This is attracting new AI workload migration from the U.S. and Europe to the region. It enables local content generation, localized AI language models, and improved user experience. Enterprises are building latency-sensitive AI services closer to users.

Edge and Micro Data Centers Supporting AI at the Network Edge

Edge AI applications like computer vision for traffic monitoring, industrial automation, and smart agriculture are growing fast. This shift requires small-scale, distributed AI data centers near users, often in tier-2 or rural cities. Energy-efficient micro data centers are enabling regional use cases with limited connectivity. Telecom firms are deploying AI at cell tower edge nodes for real-time optimization and traffic analytics. Cloud-edge hybrid models allow central training and decentralized inference. These deployments improve data privacy and responsiveness. Countries like Colombia and Peru are showing early adoption in transport, mining, and logistics sectors. AI-ready edge facilities are opening opportunities in remote and underserved areas. The Latin America AI Data Center Market is aligning with distributed AI trends.

- For instance, Cirion Technologies operates carrier-neutral data centers in Bogotá and launched its Bare Metal Cloud service in 2024, offering dedicated infrastructure with low-latency connectivity for high-performance workloads. This supports enterprise applications across Colombia with flexible deployment options.

Growing Private and Public Investments in AI Infrastructure and Talent

Latin American governments are funding AI research and infrastructure through national digital strategies. Brazil’s AI strategy includes development of innovation hubs supported by cloud and compute facilities. Private investors and venture capitalists are backing AI-native startups in fintech, healthtech, and agritech. These startups require affordable access to training compute environments and scalable storage. Data center providers are integrating GPU clusters and high-density racks for such use cases. Talent development through university-industry partnerships is also contributing to AI adoption. AI labs hosted within data centers promote co-location and collaboration. The Latin America AI Data Center Market is benefiting from this ecosystem convergence. Stakeholders view it as a foundation for regional tech innovation and economic growth.

- For instance, Scala Data Centers received approval in 2024 to build “Scala AI City” in Eldorado do Sul, Brazil, with energy access of up to 5 GW to support high-performance AI and hyperscale workloads. This project marks one of the largest AI-aligned infrastructure initiatives in Latin America.

Market Trends

High-Density Rack Designs and Liquid Cooling Integration for AI Workloads

AI workloads require high power density, prompting the adoption of advanced rack-level infrastructure. Liquid cooling systems are being integrated to manage the heat from GPUs and accelerators. Providers are shifting from traditional 8–10 kW racks to configurations exceeding 50 kW. This change drives updates in facility design and power distribution strategies. Liquid cooling adoption is rising in Brazil and Chile where energy availability supports it. Vendors are partnering with chipmakers to optimize thermal performance. Facilities are evolving into AI-optimized zones rather than uniform white spaces. The Latin America AI Data Center Market is witnessing a steady rise in high-density deployments.

Green Data Centers and Renewable Energy Sourcing for AI Sustainability

Sustainability targets are influencing how AI data centers operate in Latin America. Providers are investing in renewable power purchase agreements (PPAs), particularly in solar-rich regions. Chile and Brazil lead in this trend due to strong solar and hydro capacity. AI workloads consume significant energy, making efficiency measures essential. Green building certifications like LEED and Energy Star are gaining traction in facility design. Providers are also exploring battery energy storage systems (BESS) and onsite renewables. Carbon neutrality is becoming a differentiator in AI facility marketing. The Latin America AI Data Center Market is aligning with global green computing goals.

AI-Specific Zoning and AI Parks Emerging in Urban and Semi-Urban Areas

New infrastructure developments are being marketed specifically for AI-intensive tenants. Developers are creating “AI-ready” campuses with dedicated zones for GPU clusters and ML model training. Urban and semi-urban sites are preferred for better connectivity and access to talent. Some facilities include coworking spaces, AI incubators, and demo labs for enterprise trials. AI parks are emerging in tech hubs like São Paulo, Santiago, and Mexico City. These sites offer integrated orchestration platforms and plug-and-play AI stacks. Customers gain faster onboarding and reduced CAPEX. The Latin America AI Data Center Market is shifting toward application-specific facility planning.

Private AI Cloud Offerings and Regional Sovereign AI Platforms

Data localization and regulatory concerns are driving demand for sovereign AI platforms. Enterprises and governments want control over sensitive data and AI model training. Regional cloud providers are developing private AI clouds with GPU-accelerated infrastructure. These platforms support local AI frameworks, LLM training, and inferencing. Countries like Argentina and Colombia are creating national AI strategies tied to infrastructure. Managed AI services and platform-as-a-service (PaaS) are gaining traction. Enterprises prefer regional vendors for sector-specific customization. The Latin America AI Data Center Market is growing its AI-as-a-service ecosystem.

Market Challenges

Power Infrastructure Constraints and Regional Grid Reliability Concerns

One of the primary challenges in the Latin America AI Data Center Market is power infrastructure limitations. Several regions face unstable grid supply and aging transmission networks. High-density AI racks require consistent power delivery that many urban grids struggle to provide. Backup generation and on-site substations add cost and complexity to deployments. Grid outages increase operational risk and reduce reliability for mission-critical AI applications. Countries without regulatory clarity for power provisioning face longer facility development cycles. Data center providers must balance energy availability with cost and sustainability. These challenges restrict expansion in high-potential but underpowered markets.

Regulatory Fragmentation, Data Sovereignty Laws, and Talent Gaps

Latin America’s regulatory environment varies widely by country, impacting data center project planning. Some jurisdictions lack clear rules around AI data hosting, cross-border transfer, and public sector workloads. Data sovereignty laws require local storage, increasing infrastructure duplication costs. Compliance with evolving privacy regulations adds to legal uncertainty. The region also faces a shortage of AI-literate workforce for operating complex facilities. Skilled personnel for managing GPU clusters and orchestrating AI models remain scarce. This talent gap increases dependence on foreign experts and inflates operating costs. The Latin America AI Data Center Market must address these policy and workforce gaps to scale efficiently.

Market Opportunities

Rising AI Adoption in Financial Services, Agriculture, and Public Sector

Growing use of AI in sectors like banking, agriculture, and public services is creating infrastructure demand. Financial institutions are deploying AI for fraud detection and risk scoring. Smart agriculture uses computer vision and edge AI for crop monitoring. Governments adopt AI for citizen services, smart mobility, and emergency response. These sectors require localized AI inference with secure, high-throughput data centers. The Latin America AI Data Center Market stands to gain from such domain-specific expansion.

Expansion into Underserved Secondary Cities and AI-Edge Corridors

Secondary cities with industrial hubs are emerging as targets for edge and micro data center rollouts. Infrastructure development in cities like Campinas, Monterrey, and Medellín is gaining momentum. These areas offer proximity to AI use cases in manufacturing, logistics, and energy. Edge AI use aligns with latency reduction and localized model execution. The Latin America AI Data Center Market can scale by tapping into these emerging urban corridors.

Market Segmentation

By Type

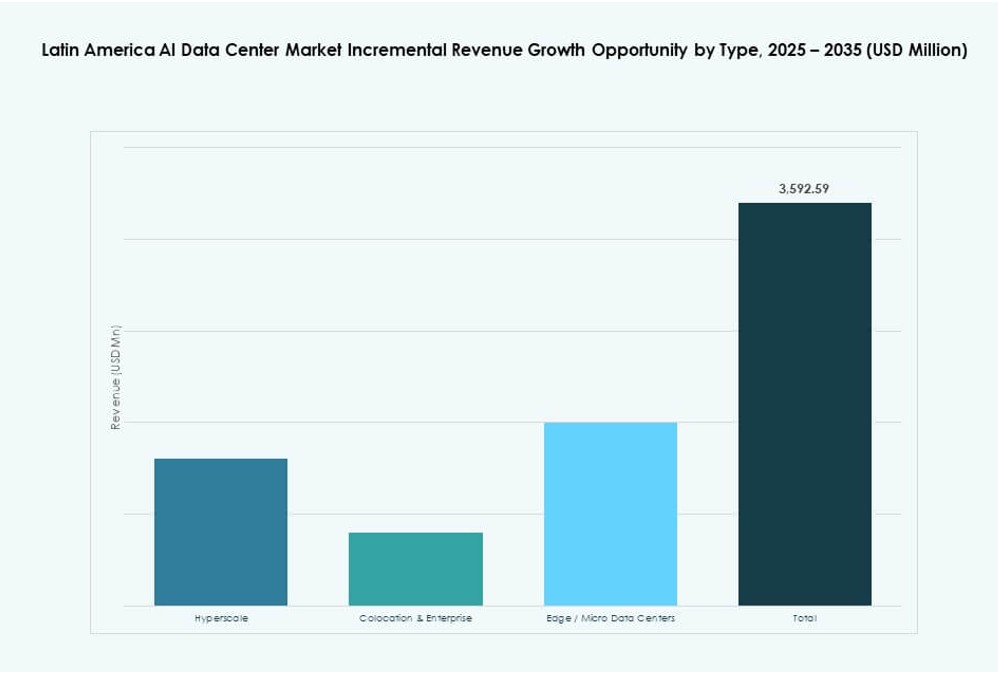

The Latin America AI Data Center Market is dominated by the Hyperscale segment due to major cloud provider investments in the region. Hyperscale facilities support large-scale model training, data storage, and real-time inference. Colocation & Enterprise centers are also gaining traction as businesses seek AI-ready hosting with cost efficiency. Edge/Micro Data Centers are emerging fast, especially in underserved regions requiring low-latency processing and real-time insights.

By Component

Hardware remains the largest revenue contributor in the Latin America AI Data Center Market due to rising demand for GPU clusters, high-density servers, and advanced cooling systems. Software & Orchestration is growing rapidly as enterprises require scalable and automated AI workload management. Services are increasingly bundled with infrastructure, including AI consulting, deployment, and monitoring for new users entering the AI space.

By Deployment

Hybrid deployment leads the Latin America AI Data Center Market as organizations balance local data processing needs with scalable cloud training environments. On-premise deployments remain important for highly regulated industries such as BFSI and public sector. Cloud deployment is rising steadily, supported by regional cloud zones and the increasing popularity of AI-as-a-service offerings.

By Application

Machine Learning (ML) is the leading application in the Latin America AI Data Center Market, used across fintech, retail, and industrial sectors. Generative AI (GenAI) is seeing rapid adoption with the rise of enterprise LLM use cases. Natural Language Processing (NLP) supports language translation, call center automation, and chatbots. Computer Vision (CV) finds use in public safety, transport, and logistics.

By Vertical

IT and Telecom dominate the Latin America AI Data Center Market due to heavy investments in AI-driven service delivery and network optimization. BFSI is a key vertical, using AI for customer service automation and risk analytics. Healthcare is growing steadily with diagnostic AI applications. Retail, Manufacturing, and Automotive are leveraging AI for supply chain optimization and predictive maintenance. Media & Entertainment is exploring GenAI for content creation.

Regional Insights

Brazil accounts for over 45% of the Latin America AI Data Center Market, driven by its advanced cloud regions, government support, and enterprise-scale AI adoption. São Paulo is the regional AI infrastructure hub, with high-density campuses, sovereign AI cloud offerings, and strong power access. Brazil’s regulatory environment and AI national strategy make it attractive to hyperscalers and local investors.

- For instance, São Paulo’s total occupied data center capacity reached 446 MW in Q1 2025, up from 374.8 MW in Q1 2024, reflecting continued demand growth. This trend highlights Brazil’s position as a core hub for digital and AI infrastructure in Latin America.

Mexico holds around 20% market share and acts as a strategic AI corridor for North America–Latin America integration. Cloud availability zones in Querétaro and emerging data center clusters in Monterrey support AI expansion. Mexico’s manufacturing, retail, and telecom sectors are deploying edge AI and hybrid AI-cloud systems. Strong trade links with the U.S. also attract nearshoring and cross-border AI workload flows.

- For instance, Equinix operates the MX2 facility in Querétaro as a major carrier-neutral hub. Cloud availability zones in Querétaro and emerging data center clusters in Monterrey support AI expansion across northern Mexico.

Chile, Colombia, and Argentina collectively hold about 25% market share, with each country contributing unique strengths. Chile offers renewable energy-driven infrastructure, while Colombia focuses on public sector AI and data localization. Argentina is advancing national AI policy and expanding enterprise AI usage. These subregions support future growth of the Latin America AI Data Center Market through innovation, connectivity, and emerging demand.

Competitive Insights:

- Ascenty

- Scala Data Centers

- Odata

- Cirion Technologies

- Microsoft (Azure)

- Amazon Web Services (AWS)

- Google Cloud / Alphabet

- NVIDIA

- Equinix

- Digital Realty Trust

The Latin America AI Data Center Market features strong competition between regional operators and global hyperscalers. Ascenty, Scala Data Centers, and Odata lead the regional buildout with high-density, AI-ready facilities in Brazil, Chile, and Colombia. Global cloud firms like AWS, Microsoft, and Google Cloud are expanding regional zones to serve enterprise AI workloads. NVIDIA and other hardware vendors are enabling the GPU backbone powering AI clusters across facilities. Interconnection specialists like Equinix and Digital Realty support cloud-to-edge integration, enhancing latency-sensitive AI applications. It reflects a shift toward AI-optimized design, liquid cooling, and hybrid deployment support. Strategic partnerships, sustainable infrastructure, and proximity to undersea cables are shaping site selection and investment patterns across key metro regions.

Recent Developments:

- In January 2026, RT‑One partnered with Hitachi Energy to develop electrification infrastructure for what is planned to be the largest AI data center platform in Latin America. This collaboration focuses on high‑voltage electrical systems and grid connections for mega campuses in Uberlândia and Maringá, Brazil, aiming to support high‑density AI computing with reliable, efficient power solutions.

- In October 2025, OpenAI signed a letter of intent with Sur Energy for a potential Argentina AI data center project with investments up to $25 billion. The plan could deliver up to 500 megawatts of compute capacity, making it one of Latin America’s largest AI infrastructure developments aimed at supporting advanced compute needs.