Executive summary:

The South Korea Data Center Market size was valued at USD 3,209.24 million in 2020 to USD 5,499.43 million in 2025 and is anticipated to reach USD 14,487.07 million by 2035, at a CAGR of 10.10% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2035 |

| South Korea Data Center Market Size 2025 |

USD 5,499.43 Million |

| South Korea Data Center Market, CAGR |

10.10% |

| South Korea Data Center Market Size 2035 |

USD 14,487.07 Million |

Market growth in South Korea is driven by rapid cloud adoption, widespread 5G integration, and rising demand for AI-powered infrastructure. Enterprises across finance, healthcare, telecom, and retail are investing in scalable data solutions to manage growing workloads. Innovation in automation, virtualization, and energy-efficient systems enhances operational performance. The market plays a strategic role by enabling digital-first business models and attracting strong investment from both domestic and global players.

Regionally, Seoul dominates the market due to its position as the country’s financial and technology hub, supported by hyperscale deployments and enterprise clusters. Busan is emerging as a key secondary hub, leveraging coastal connectivity and subsea cable infrastructure. Central and other smaller regions are also gaining importance with government-backed digital initiatives and lower land costs, ensuring balanced development and wider access to infrastructure.

Market Drivers

Rising Demand for Digital Transformation Across Enterprises

The South Korea Data Center Market benefits from accelerated digital transformation in finance, healthcare, telecom, and retail. Enterprises expand IT infrastructure to handle growing volumes of unstructured and structured data. The integration of advanced analytics, AI, and IoT fuels demand for reliable storage and computing. It strengthens resilience by enabling real-time insights and faster decision-making. Investors view the sector as a critical growth enabler for smart industries. Rapid adoption of advanced business models ensures long-term competitiveness. This transformation makes data centers indispensable for digital-first enterprises.

- For instance, SK Telecom, in partnership with global tech firms, is building Korea’s largest AI-dedicated data center with 60,000 GPUs and 100 megawatts of power capacity, backed by a 7 trillion-won investment with AWS. This project positions SK Telecom as a key leader in AI data center infrastructure in the Asia-Pacific region.

Expansion of Cloud Adoption and Hybrid Infrastructure Models

Cloud adoption continues to shape demand across industries, supported by hybrid infrastructure that balances scalability with control. Large enterprises shift workloads to cloud platforms while retaining critical data on-premises. It enables businesses to align operations with compliance standards and optimize costs. The South Korea Data Center Market attracts hyperscale providers due to this hybrid preference. Integration of private and public environments strengthens enterprise flexibility. Telecom firms and global providers invest heavily in advanced cloud infrastructure. Businesses see cloud-enabled ecosystems as essential to digital innovation. This dynamic accelerates long-term investment flows.

- For instance, KT Cloud inaugurated a new high-tech data center in Yecheon-gun in June 2025, equipped with a power capacity of 10MW (6MW dedicated to IT operations), supporting cloud-native services such as OpenStack and Kubernetes. KT Cloud has publicly confirmed plans to expand overall data center capacity to 320MW by 2030, illustrating robust hybrid infrastructure and cloud expansion.

Adoption of Artificial Intelligence and High-Performance Computing

Artificial intelligence and high-performance computing are reshaping infrastructure requirements. Businesses adopt GPU-based servers and advanced processors to support complex workloads. It drives demand for low-latency, high-capacity facilities capable of handling AI-driven tasks. The South Korea Data Center Market attracts global AI firms seeking advanced deployment capabilities. Healthcare, finance, and automotive industries leverage AI for diagnostics, trading, and autonomous systems. High computing power enhances predictive analytics and innovation pipelines. Enterprises prioritize AI-ready environments to gain competitive advantage. This adoption aligns the market with global innovation priorities.

Strategic Role in Regional Connectivity and Digital Economy Growth

South Korea holds a strong position as a regional digital hub. Advanced 5G networks and global subsea cables support its expanding connectivity. It attracts multinational enterprises establishing regional headquarters. The South Korea Data Center Market provides critical infrastructure for Asia-Pacific cloud and content delivery networks. Government initiatives drive public cloud and digital economy adoption. Strong investment from domestic conglomerates reinforces national competitiveness. Businesses see South Korea as a gateway to regional innovation. This strategic importance sustains high investor confidence.

Market Trends

Integration of Renewable Energy for Sustainable Operations

Sustainability is emerging as a defining trend in the South Korea Data Center Market. Operators implement renewable energy solutions including wind, solar, and hydropower integration. It reduces reliance on fossil fuels and aligns with climate commitments. Enterprises emphasize energy efficiency with advanced cooling and power management systems. Green certifications strengthen brand value and investor appeal. Carbon-neutral initiatives set new operational benchmarks. It positions South Korea as a responsible infrastructure hub. The focus on sustainability increases long-term competitiveness for both local and global operators.

Growth of Edge Data Centers to Support Low-Latency Applications

Edge computing gains traction with growing demand for real-time applications. Industries including automotive, gaming, and healthcare require faster data processing closer to end-users. The South Korea Data Center Market supports edge facilities to minimize latency. It ensures enhanced user experience and operational agility. 5G rollouts accelerate edge adoption across metropolitan and secondary cities. Enterprises benefit from distributed infrastructure with scalable capacity. Regional hubs invest in edge integration for advanced services. This shift highlights the growing role of modular and micro data centers.

Deployment of Advanced Security and Compliance Infrastructure

Cybersecurity investments dominate strategic plans for enterprises and providers. Operators integrate AI-based threat detection and zero-trust frameworks. The South Korea Data Center Market evolves with strict compliance to local and global data protection rules. It ensures trust among enterprises and customers handling sensitive workloads. Security upgrades extend from physical access to multi-layered digital safeguards. Financial services, defense, and healthcare prioritize such secure environments. It builds resilience against ransomware and cyberattacks. Regulatory alignment enhances long-term sustainability and operational trust.

Increased Investment in Automation and Software-Defined Data Centers

Automation transforms data center operations with predictive maintenance, orchestration, and AI-driven monitoring. Software-defined infrastructure reduces manual interventions and optimizes resource allocation. The South Korea Data Center Market embraces virtualization to manage complex workloads. It improves cost efficiency and enhances scalability for diverse industries. Enterprises prioritize orchestration platforms for seamless hybrid deployment. AI-enabled monitoring strengthens uptime and performance. It reshapes operational standards and reduces downtime risks. Automation becomes a critical trend ensuring competitive efficiency.

Market Challenges

High Energy Consumption and Rising Operational Costs

Energy remains one of the largest expenses for operators. Advanced cooling, power distribution, and server upgrades increase overall consumption. The South Korea Data Center Market faces challenges in maintaining profitability while managing rising energy prices. It drives pressure to adopt renewable solutions and efficient equipment. However, integration costs remain significant. Balancing sustainability goals with financial viability proves difficult. Larger facilities struggle to maintain low PUE ratios at scale. These challenges slow expansion in cost-sensitive segments.

Regulatory Pressure and Land Availability Constraints

Strict regulations on data sovereignty, cybersecurity, and environmental impact challenge market expansion. Enterprises must comply with evolving policies on sensitive data storage. The South Korea Data Center Market also faces land scarcity in metropolitan hubs. It limits the ability to build large-scale facilities near Seoul. Operators explore secondary cities, but infrastructure readiness varies. Compliance costs increase capital requirements for new entrants. It places smaller players at a competitive disadvantage. Market growth requires balancing regulation with strategic investments.

Market Opportunities

Expansion of Hyperscale and AI-Optimized Facilities

Hyperscale growth creates significant opportunities in the South Korea Data Center Market. Global providers expand capacity to meet demand for AI, big data, and cloud. It attracts partnerships between telecoms and multinational enterprises. Emerging AI ecosystems require GPU-intensive infrastructure, creating space for innovation. Operators gain revenue from hosting advanced applications. Businesses leverage hyperscale facilities for agility and scalability. The trend opens long-term opportunities for investors targeting next-generation workloads.

Rising Demand for Colocation and Hybrid Cloud Services

Colocation growth reflects strong demand among SMEs and large enterprises. The South Korea Data Center Market benefits from firms shifting workloads to hybrid environments. It provides secure, scalable solutions without high upfront investment. Colocation enhances access to regional and global networks. Cloud-linked colocation creates new service models for enterprises. It strengthens partnerships between global and domestic operators. Businesses use these services to support expansion strategies. Opportunities increase with continued enterprise digitalization.

Market Segmentation

By Component

Hardware dominates the South Korea Data Center Market, led by servers, cooling, and power infrastructure. Growing demand for high-performance computing drives investments in storage and networking. Software solutions such as DCIM and virtualization gain momentum but remain secondary to physical assets. Services including consulting and managed solutions expand as enterprises seek expert integration. Hardware maintains the largest share, reflecting its role as the backbone of advanced facilities.

By Data Center Type

Hyperscale facilities hold the largest share, supported by investments from global cloud providers. Colocation follows, driven by SMEs seeking cost-effective infrastructure. Enterprise data centers remain relevant but face pressure from hybrid models. Edge facilities grow steadily with IoT and 5G applications. Mega data centers attract investment for large-scale demand. Cloud and Internet Data Centers (IDC) expand rapidly, strengthening South Korea’s position as a digital hub.

By Deployment Model

Hybrid models dominate, combining on-premises control with cloud scalability. Enterprises adopt hybrid to balance compliance with flexibility. Cloud-based models grow fastest, supported by hyperscale provider investments. On-premises remain important for sensitive industries like government and defense. The South Korea Data Center Market reflects a clear preference for hybrid ecosystems. It enables businesses to adapt quickly to changing requirements. Growth favors models integrating agility with security.

By Enterprise Size

Large enterprises account for the majority share, reflecting strong digital infrastructure budgets. SMEs show rising adoption of colocation and cloud-linked solutions. It allows smaller firms to scale without heavy investment. The South Korea Data Center Market supports enterprise needs across industries. Large enterprises demand advanced compliance, while SMEs prioritize agility. Both segments contribute to overall diversification.

By Application / Use Case

IT and telecom lead with significant market share, supported by 5G and digital services. BFSI follows, requiring high-security data management. Healthcare and retail expand their demand with AI-driven tools and online platforms. Manufacturing strengthens its adoption through IoT integration. Government and defense ensure critical workloads remain secure. Media and entertainment benefit from streaming and gaming demand. Education and energy remain smaller but growing sectors.

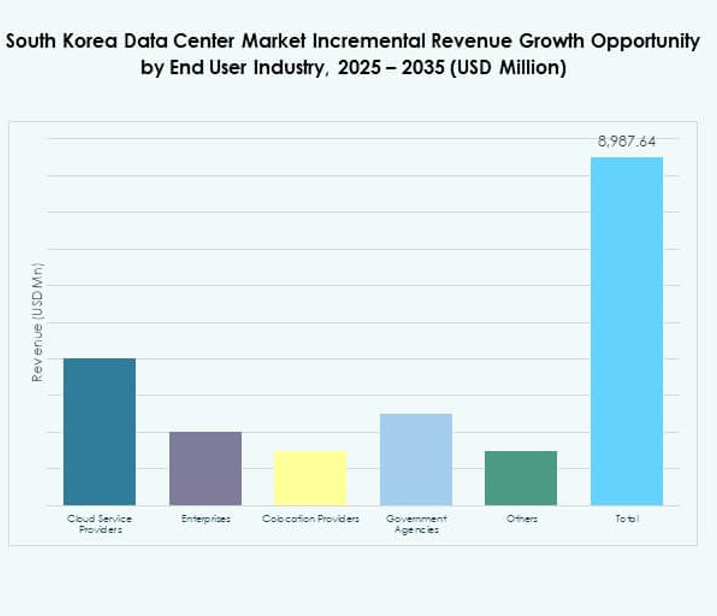

By End User Industry

Cloud service providers dominate, supported by hyperscale expansion. Enterprises represent strong demand across industries. Colocation providers play a critical role for SMEs. Government agencies enforce compliance and rely on domestic facilities. The South Korea Data Center Market reflects a diverse end-user landscape. Each segment supports the country’s role as a digital hub.

Regional Insights

Seoul Metropolitan Region Holding 62% Market Share

The Seoul metropolitan region dominates the South Korea Data Center Market with 62% share. Its role as the financial and business hub attracts major hyperscale and colocation investments. Dense enterprise clusters increase demand for high-capacity facilities. It benefits from strong connectivity, advanced infrastructure, and large customer bases. Global and domestic operators concentrate expansion in this region. It remains the epicenter for digital services and innovation in South Korea.

- For instance, in June 2025, Naver Cloud signed an eight-year contract to lease space at the LG CNS-operated Jukjeon Data Center in Seoul, a facility spanning 99,070 sqm and designed for large-scale enterprise and cloud workloads.

Busan and Southern Region Capturing 23% Market Share

Busan and southern cities account for 23% of the market. Coastal proximity supports subsea cable connectivity and international traffic. It enhances South Korea’s position as a global internet gateway. Investments focus on modular and edge facilities to serve logistics and manufacturing sectors. The region diversifies market presence beyond Seoul. It emerges as a critical secondary hub for resilience and scalability.

- For instance, Digital Edge launched the PUS1 facility in Centum City, Busan, integrated with a Cable Landing Station to enable direct international network interconnection for businesses seeking geographical redundancy to Seoul, and its SEL2 36MW facility—launched in July 2025 in Incheon—supports power densities up to 130kW per cabinet.

Central and Emerging Regions Accounting for 15% Market Share

Central and emerging regions represent 15% share of the South Korea Data Center Market. Smaller cities attract investment due to lower land costs and renewable integration potential. Government initiatives promote digital infrastructure expansion across underserved areas. It creates opportunities for SMEs and public services adoption. These regions support balanced national growth in digital infrastructure. Long-term development ensures broader access to advanced data services.

Competitive Insights:

- KT Corporation

- SK Telecom

- LG CNS

- Naver Cloud

- Digital Realty Trust, Inc.

- NTT Communications Corporation

- Microsoft Corporation

- Amazon Web Services, Inc. (AWS)

- Google LLC (Alphabet Inc.)

The South Korea Data Center Market is defined by strong competition among domestic telecom giants and global hyperscale providers. KT Corporation, SK Telecom, and LG CNS dominate with extensive infrastructure, leveraging nationwide networks to serve enterprises and government clients. Naver Cloud strengthens its presence through cloud-native solutions tailored to domestic businesses. Global players such as AWS, Microsoft, and Google expand with hyperscale facilities, targeting high-capacity workloads and hybrid cloud adoption. Digital Realty and NTT Communications enhance competitiveness by providing colocation and cross-border connectivity. It evolves with rising demand for AI-ready infrastructure, low-latency services, and sustainable operations. Collaboration between local operators and international cloud firms continues to reshape the ecosystem, driving innovation and positioning South Korea as a strategic digital hub in the Asia-Pacific region.

Recent Developments:

- In September 2025, the South Korean government and BlackRock signed a memorandum of understanding to cooperate on establishing hyperscale AI data centers powered by renewable energy. The initiative, announced after a meeting in New York, aims to meet both domestic and Asia-Pacific region AI infrastructure demand over the next decade.

- In September 2025, Warburg Pincus, in partnership with Wide Creek Asset Management and DC Connects, acquired a greenfield site in Yongin City, Gyeonggi Province, to develop an 80MW hyperscale data center specifically focused on AI and cloud workloads.

- In August 2025, SK Telecom partnered with Schneider Electric to integrate digital twin technology into the SK AIDC in Ulsan, deploying advanced mechanical, electrical, and plumbing equipment to realize sustainable and highly efficient data center management.

- In August 2025, DCI Data Centers and Koramco Asset Management announced the development of a new 40MW hyperscale data center in Seonggok-dong, Ansan. DCI will lead the project with Koramco managing development, with construction planned for Q4 2025 and operations commencing in 2028.