Executive summary:

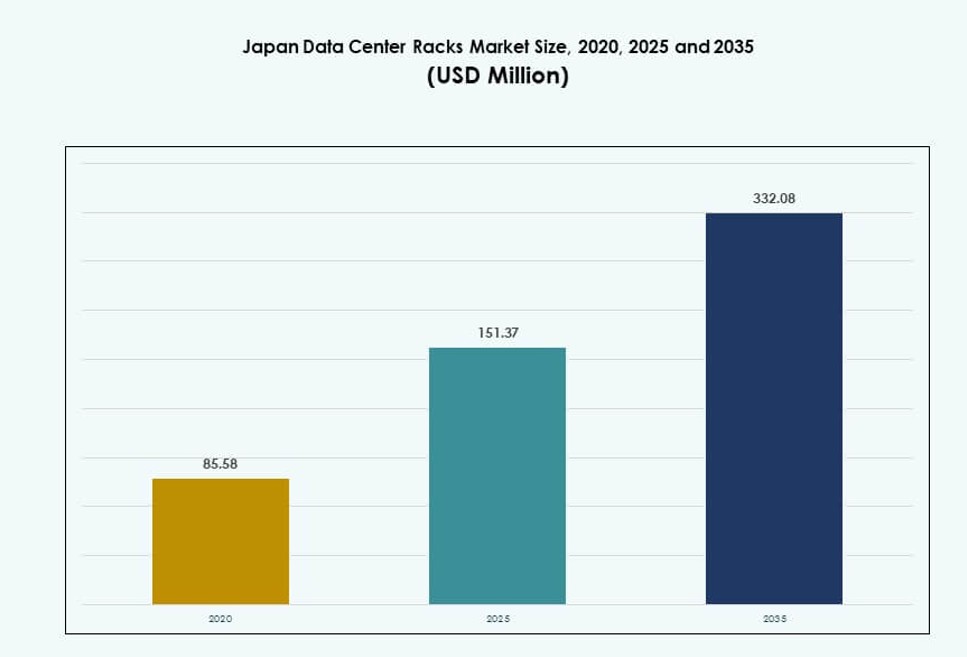

The Japan Data Center Racks Market size was valued at USD 85.58 million in 2020 to USD 151.37 million in 2025 and is anticipated to reach USD 332.08 million by 2035, at a CAGR of 8.11% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2035 |

| Japan Data Center Racks Market Size 2025 |

USD 151.37 Million |

| Japan Data Center Racks Market, CAGR |

8.11% |

| Japan Data Center Racks Market Size 2035 |

USD 332.08 Million |

High-density computing, AI workload growth, and modular infrastructure are driving the market forward. Enterprises are adopting liquid-cooled and smart racks to handle rising power loads and energy goals. Rack designs are evolving to support flexible configurations, software-defined operations, and platform-layer integration. Telecom and IT providers are upgrading racks for edge, 5G, and AI-ready deployments. Government digital policies and sustainability mandates further accelerate infrastructure spending. Investors see long-term value in scalable, resilient rack infrastructure aligned with Japan’s national digital priorities. The market reflects a critical layer in enabling hyperscale, enterprise, and hybrid cloud infrastructure. Its strategic role supports compute efficiency and national competitiveness.

Tokyo leads the market due to dense cloud zones, government-backed cloud adoption, and hyperscaler investments. Osaka serves as a secondary hub for disaster recovery and hybrid workloads with mirrored rack infrastructure. Cities like Fukuoka, Nagoya, and Sapporo are emerging with edge data center expansion and telecom rollouts. Strong fiber connectivity and regional 5G projects support rack deployments beyond major metros. These regions offer space, lower cost, and policy incentives for decentralized infrastructure. The market continues expanding geographically as demand for localized compute and edge storage rises. Japan’s rack demand now reflects a multi-regional data infrastructure evolution.

Market Dynamics:

Market Drivers

Rise in Hyperscale and AI Workloads Demands High-Density Rack Designs

The Japan Data Center Racks Market is driven by rising demand for AI, ML, and HPC applications. These workloads need high-density, scalable racks supporting liquid cooling and 50 kW+ power thresholds. Hyperscalers are expanding in Tokyo and Osaka with modular designs for rapid deployment. Rack infrastructure has evolved with built-in cable management and cooling integration. Domestic and global players are aligning with ODCC and OCP standards for rack interoperability. Japan’s hyperscale boom is backed by digital government initiatives and sovereign cloud policies. AI-focused enterprises require low-latency environments with dynamic rack configurations. These needs push demand for advanced rack setups. It plays a central role in modern compute and data delivery infrastructure.

- For instance, NTT Communications’ Osaka No. 7 data center achieved NVIDIA DGX-Ready certification in 2024, supporting high-density racks for generative AI with liquid cooling readiness across its 4,600 m² server room, expandable to 9,500 m².

Shift Toward Energy-Efficient and Sustainable Infrastructure Investments

Energy use optimization is a critical driver for new rack adoption in Japan’s energy-constrained environment. Operators prefer racks that support cold aisle containment, airflow control, and integrated power monitoring. Liquid cooling-compatible racks are gaining traction to reduce PUE and manage GPU heat loads. Companies also focus on carbon reduction, prompting eco-designs across the facility level. Rack infrastructure with in-rack cooling and high-efficiency PDUs contributes to ESG targets. Data center owners favor racks that align with long-term sustainability plans. Japan’s push for greener IT infrastructure intensifies demand for efficient rack hardware. It supports both energy savings and regulatory compliance. This alignment strengthens investor confidence in facility upgrades.

Digital Infrastructure Modernization Backed by Policy and Telecom Expansion

Japan’s digital economy strategies are directly boosting rack deployments across legacy and greenfield facilities. The Digital Agency’s reforms are pushing cloud-first and edge-ready architectures. Telecom players are upgrading racks across 5G edge sites and regional nodes. Government cloud zones require secure, modular rack designs integrated with monitoring. Infrastructure investment in edge computing zones brings higher demand for flexible rack deployments. Hybrid setups across cloud, colocation, and edge are shaping procurement cycles. Japan’s focus on digital transformation accelerates the need for agile, resilient rack formats. It is now a strategic enabler for reliable digital operations. Public and private initiatives align to scale modular rack infrastructure.

- For instance, NTT’s Tokyo No. 11 data center supports high rack densities with 2,000 kg/m² floor loads, N+1 UPS redundancy, and 48+ hours of emergency generator runtime, enabling reliable edge and cloud upgrades.

Rack Standardization and Automation Adoption in Managed Services Models

Standardization in rack formats has improved time-to-deploy, asset lifecycle, and automation integration. Managed hosting providers are offering pre-configured racks with integrated power, cooling, and security sensors. These automated racks reduce human error and improve service SLA metrics. Support for remote diagnostics and software-defined infrastructure is built into newer racks. Customers seek racks that align with containerized, virtualized, and disaggregated storage formats. Smart rack adoption is expanding across Tokyo, with support from local integrators. Japan Data Center Racks Market benefits from cloud-native growth and orchestration-ready environments. It supports dynamic, software-controlled infrastructure scaling. This trend attracts both enterprise and hyperscale customers.

Market Trends

Integration of Direct-to-Chip and Rear Door Liquid Cooling in Rack Systems

Rising rack power density in Japan is leading to widespread adoption of liquid-based cooling systems. Direct-to-chip and rear door heat exchangers are being integrated into high-performance racks. Operators prefer modular liquid-cooled racks that support GPUs, AI accelerators, and dense compute nodes. Compatibility with standard rack dimensions supports easier upgrades. Vendors are developing ready-to-deploy liquid cooling racks with monitoring sensors and thermal alerts. Thermal efficiency improvements of 30–40% are prompting shift away from traditional airflow methods. Rack-level liquid systems are favored in Tokyo hyperscale zones. Japan Data Center Racks Market benefits from this transition in power-dense deployments. It aligns with the global move to liquid cooling for compute-intensive workloads.

Growth of Edge-Centric Rack Deployments Across Regional Nodes

Edge computing growth is driving new rack installations across suburban and rural locations. Operators deploy compact, pre-configured racks with integrated power and cooling at telecom edge sites. Regional edge facilities use ruggedized and modular rack enclosures for outdoor and low-footprint sites. Demand for 5G backhaul, latency-sensitive applications, and smart city infrastructure supports this shift. Telecom players and CDN providers install edge racks across Fukuoka, Sapporo, and Nagoya. Edge racks are often pre-integrated with switchgear, micro DCIM, and redundant systems. Japan Data Center Racks Market sees growth through distributed architecture designs. It responds to demand for faster data processing near end-users.

Adoption of AI-Powered DCIM for Rack-Level Performance Optimization

Data centers in Japan are deploying AI-integrated data center infrastructure management (DCIM) tools at rack level. These tools optimize airflow, temperature, power load, and device utilization in real time. Rack enclosures now integrate sensors for predictive analytics and failure prevention. AI-based monitoring supports remote diagnostics and automated response protocols. Operators use digital twins and simulation for optimizing rack layouts. This trend supports operational resilience and sustainability tracking. Facilities running high-density racks benefit from granular telemetry and alert systems. Japan Data Center Racks Market aligns with this AI adoption in infrastructure management. It improves uptime, efficiency, and cost savings.

Growing Investments in Seismic-Resistant and Prefabricated Rack Systems

Japan’s seismic risk profile has led to increased demand for earthquake-resistant rack frames. Vendors now offer racks tested for vibration, tilt, and anchoring strength for high-risk zones. Prefabricated rack systems are gaining adoption in modular data center rollouts. Seismic-rated racks are widely used in government, banking, and telecom facilities. Certification standards influence rack procurement, especially in Tokyo and Sendai regions. Rack structures with adjustable stabilizers and reinforced frames ensure asset safety. Prefabrication also enables faster deployment cycles for urban expansions. Japan Data Center Racks Market reflects this focus on structural safety and speed. It supports national infrastructure reliability goals.

Market Challenges

Space Constraints and High Real Estate Costs Limit Expansion Potential

Japan’s urban centers face limited land availability, restricting greenfield facility development. Data centers in Tokyo and Osaka operate in high-cost zones, creating pressure on rack density. Operators must optimize vertical rack space and power usage in compact layouts. These constraints often increase reliance on high-density or liquid-cooled racks, raising upfront investment. Expansion requires creative solutions like underground or multi-level data floors. Retrofitting older sites to meet new rack formats also remains complex. Japan Data Center Racks Market struggles with balancing scale and efficiency in constrained spaces. It slows deployment cycles and complicates long-term rack planning. Cost-intensive real estate adds further pressure on margins.

Supply Chain Disruptions and Customization Needs Hinder Procurement Speed

Rack procurement cycles face delays due to complex customization and sourcing limitations. Many data centers in Japan prefer specific design configurations based on workload, compliance, and vendor standards. Custom racks with specialized cooling, power, or seismic features require longer lead times. Global supply chain disruptions have caused delivery delays and increased component prices. Local manufacturing capacity remains limited for advanced modular rack systems. Import regulations and component availability add to project risk. Japan Data Center Racks Market encounters bottlenecks during high-demand phases. It slows adoption of advanced rack types and reduces agility in hyperscale expansions. Operators seek local alternatives to reduce sourcing risk.

Market Opportunities

AI Workload Expansion Creates Demand for 50 kW+ High-Density Rack Deployments

The rise in AI training workloads from enterprises and hyperscalers presents strong demand for next-gen rack solutions. GPU-intensive environments require high power density racks that support liquid cooling and integrated PDUs. Japan Data Center Racks Market can scale rapidly by aligning with AI-driven capacity needs. It opens opportunities for modular, scalable, and smart racks supporting AI clusters. Providers offering fast-deploy rack systems will gain competitive edge. Tokyo and Osaka AI zones will remain top targets. Smart city initiatives will further drive AI-ready rack procurement.

Regional Edge Expansion Unlocks New Markets for Compact and Prefabricated Racks

Edge infrastructure growth across regional cities opens doors for compact rack vendors. Prefabricated racks with integrated cooling, power, and security are ideal for telecom and smart infrastructure deployments. Japan Data Center Racks Market benefits from regional policy support and decentralization goals. Rack vendors can enter tier-2 city markets with containerized or all-in-one rack solutions. These smaller deployments will enable distributed cloud growth in less saturated zones. Expansion potential remains strong across northern and western prefectures.

Market Segmentation

By Rack Type

Cabinet racks hold the dominant share in the Japan Data Center Racks Market due to widespread use in hyperscale and enterprise settings. They offer enhanced cable management, airflow control, and physical security. Open frame racks are used primarily in secure environments where airflow and accessibility are prioritized. Others include wall-mount and portable configurations suited for smaller deployments. Cabinet racks are favored for flexibility and power integration. They support dense configurations and thermal containment needs. Market preference continues shifting toward closed cabinets for high-density workloads.

By Rack Height

42U racks dominate the Japan Data Center Racks Market, balancing space efficiency and hardware capacity. These standard-height racks support most IT, networking, and power equipment, fitting seamlessly into modular layouts. Below 42U racks are used in edge sites and constrained server rooms. Above 42U racks are gaining interest from hyperscalers due to rising demand for scalable AI and storage capacity. 42U remains ideal for hybrid deployments across colocation and enterprise facilities. It enables easier maintenance and compatibility with global OEM designs.

By Width

The 19-inch segment leads in the Japan Data Center Racks Market as the global standard for most IT equipment. It ensures compatibility across OEMs and simplifies inventory management. 23-inch racks are used for telecom and specialized deployments requiring larger cable trays or airflow. Others include non-standard custom widths used in niche or legacy environments. The 19-inch racks continue dominating because of design consistency, lower cost, and interoperability. It allows easier scaling and service integration across multiple data center zones.

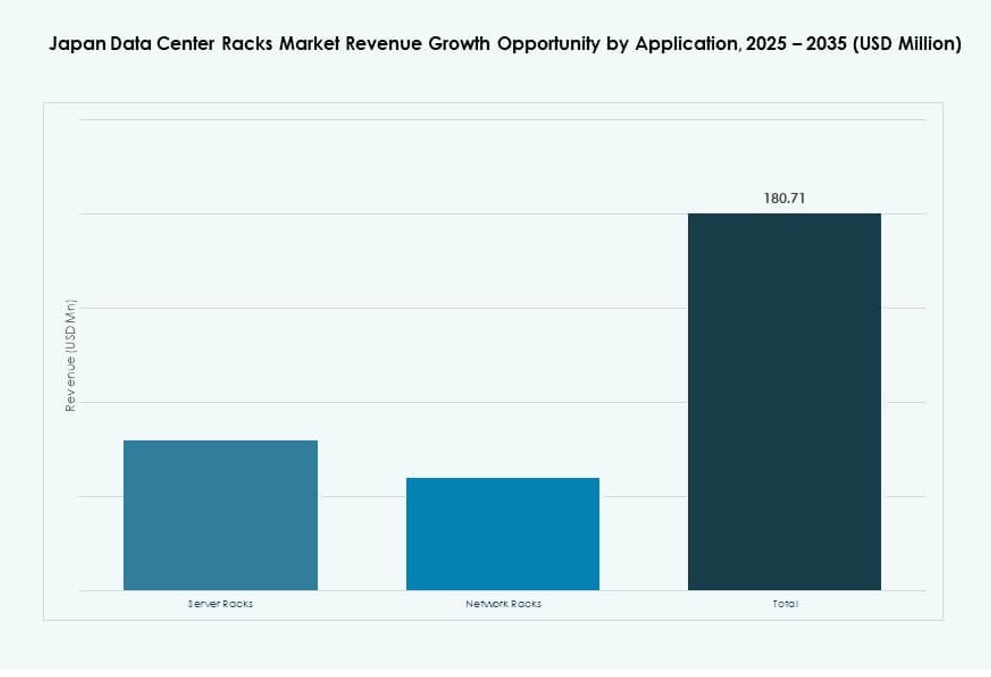

By Application

Server racks account for the largest share in the Japan Data Center Racks Market due to the growing demand for compute-intensive tasks and virtualization. These racks support critical workloads in hyperscale and private cloud environments. Network racks serve routing, switching, and security equipment in telecom and interconnect zones. The need for high IOPS and AI processing keeps server rack deployment strong. Innovations in rack power and thermal management also favor server rack sales. Network racks grow steadily through telco expansion and 5G rollouts.

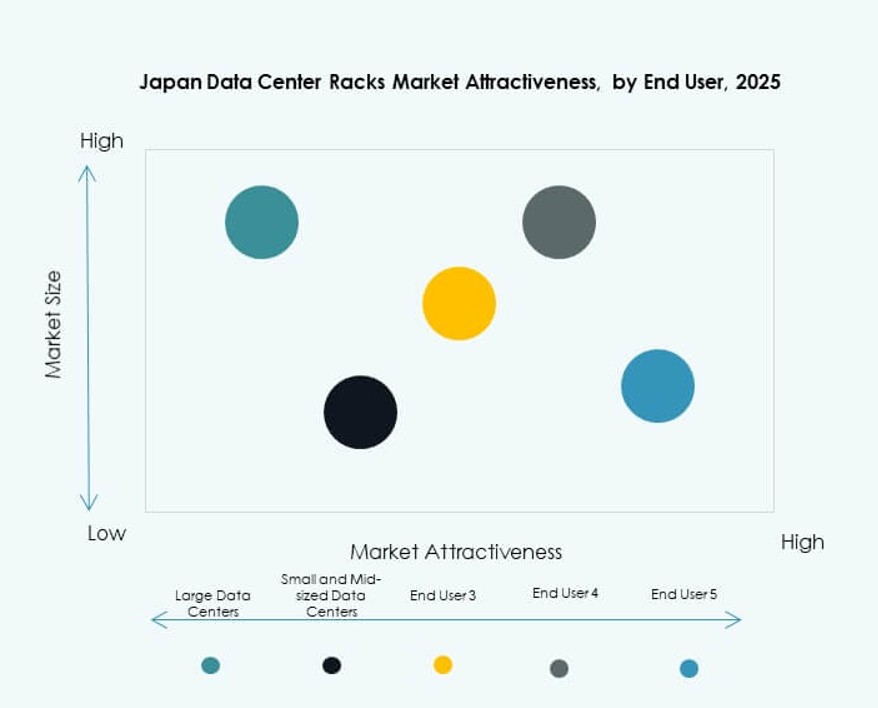

By End-user

Large data centers dominate the Japan Data Center Racks Market with higher deployment volumes and larger infrastructure investments. These facilities require scalable, high-density rack systems to support AI, cloud, and hybrid models. Small and mid-sized data centers adopt more standardized racks for general-purpose IT needs. Enterprises transitioning to hybrid cloud also drive demand across both categories. Large data centers invest in smart racks with monitoring and modularity. They push procurement cycles for advanced power and cooling solutions.

By Vertical

IT & Telecom remains the leading vertical in the Japan Data Center Racks Market, driven by hyperscaler, cloud, and mobile expansion. BFSI follows, focusing on secure, redundant infrastructure for financial services and core banking. Government and defense segments demand secure and resilient racks aligned with sovereign data policies. Healthcare, energy, and retail show steady growth through digital transformation. Retail racks are expanding with rising online commerce and analytics. Each vertical adopts rack formats aligned with workload, compliance, and resiliency priorities.

Regional Insights

Tokyo Region Leads with 44% Market Share Driven by Hyperscale and Public Sector Cloud

Tokyo dominates the Japan Data Center Racks Market with around 44% share, driven by hyperscale deployments and cloud region clustering. Public sector cloud programs and financial services infrastructure add strong demand for high-density racks. Most international hyperscalers and domestic operators base their largest facilities in Tokyo. The region’s strong fiber network, policy support, and skilled workforce attract continued investment. Tokyo racks often support AI clusters and sovereign cloud nodes. It remains the core market for high-spec rack designs.

- For instance, AWS’s Asia Pacific (Tokyo) region launched in 2011 and operated 4 Availability Zones as of 2024, enabling redundant networking across data centers for services including AI workloads.

Osaka Holds 31% Share Due to Disaster Recovery, Redundancy, and Telecom Infrastructure

Osaka contributes about 31% of the market share, acting as Japan’s secondary hub for disaster recovery and mirrored data center operations. Many enterprises use Osaka to ensure redundancy and regulatory compliance. Rack installations in Osaka often support hybrid cloud, telco infrastructure, and resilient design architectures. The region’s lower risk profile and fiber connectivity make it ideal for backup and latency-sensitive operations. Japan Data Center Racks Market benefits from strong rack demand in mirrored deployments. It supports national infrastructure continuity goals.

- For instance, KDDI signed an agreement with Sharp in 2024 to develop a data center at the Sharp Sakai Plant in Osaka, planning to host at least 1,000 servers including Nvidia GB200 NVL72 configurations for resilient AI workloads.

Regional Cities Hold 25% Market Share with Emerging Edge, Telecom, and Industry Clusters

The remaining 25% of Japan’s rack demand comes from emerging zones like Fukuoka, Sapporo, Nagoya, and Hiroshima. These cities are witnessing growth in telecom edge facilities, smart city projects, and AI research clusters. Prefabricated and compact racks see higher deployment across edge locations and university campuses. Operators target these areas for distributed compute, content delivery, and regional cloud services. Japan Data Center Racks Market sees new rack opportunities in these expanding zones. It supports decentralized, scalable infrastructure growth aligned with regional needs.

Competitive Insights:

- Schneider Electric

- Vertiv Group

- Rittal

- Fujitsu

- Hewlett Packard Enterprise

- Cisco Systems, Inc.

- Dell Inc.

- Nitto Kogyo

- Takachi Electronics Enclosure

- Chatsworth Products

The Japan Data Center Racks Market features a mix of global giants and domestic specialists offering a wide range of rack systems. Schneider Electric, Vertiv, and Rittal lead in high-density and modular rack deployments for hyperscale environments. Fujitsu and HPE focus on enterprise-grade integrated racks with power and cooling features. Local firms like Nitto Kogyo and Takachi provide tailored solutions that meet seismic and compact footprint requirements. The competitive environment is shaped by innovation in liquid cooling, smart racks, and energy-efficient designs. It is further defined by partnerships with hyperscalers and telecom operators. Companies gain advantage by offering fast-deploy, compliant, and high-reliability rack systems aligned with Japan’s infrastructure and digital goals.

Recent Developments:

- In November 2025, Schneider Electric introduced a new line of data center infrastructure solutions designed for high‑density AI and accelerated compute workloads. The launch includes integrated white space solutions that support extreme rack power densities beyond 1 MW, improved power distribution schemes, and enhanced thermal management capabilities to support modern rack designs.

- In October 2025, Schneider Electric announced collaboration with NVIDIA to develop an 800 VDC power sidecar system supporting future racks up to 1.2 MW. This innovation focuses on high‑capacity rack power delivery and energy efficiency for next‑generation AI infrastructure.

- In August 2025, Vertiv Holdings Co. completed its acquisition of Great Lakes Data Racks & Cabinets, valued at approximately $200 million. This strategic move expanded Vertiv’s rack, cabinet, and integrated infrastructure portfolio with custom rack solutions, seismic cabinets, and advanced cable management systems.