Executive summary:

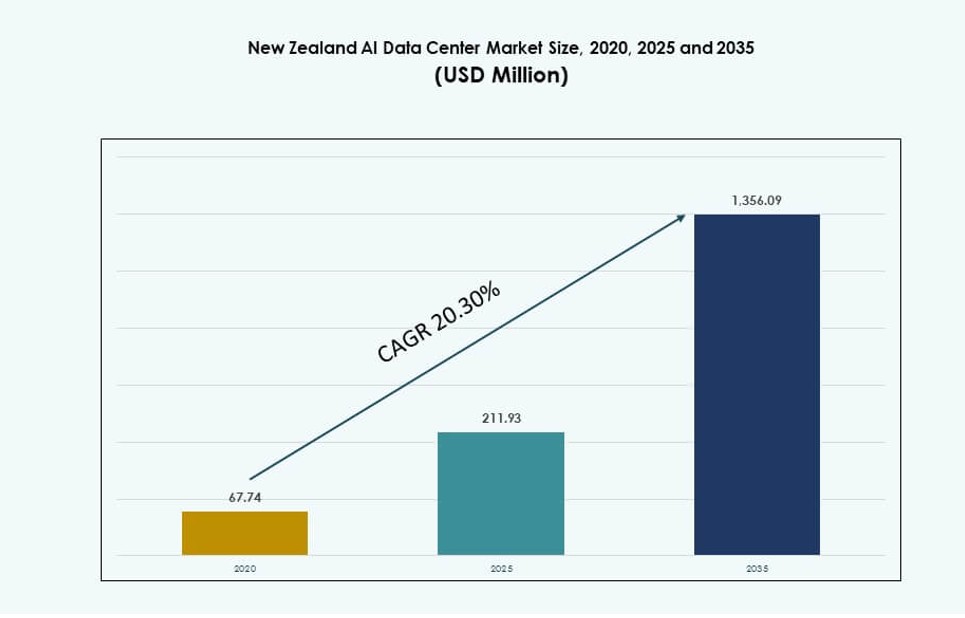

The New Zealand AI Data Center Market size was valued at USD 67.74 million in 2020 to USD 211.93 million in 2025 and is anticipated to reach USD 1,356.09 million by 2035, at a CAGR of 20.30% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2035 |

| New Zealand AI Data Center Market Size 2025 |

USD 211.93 Million |

| New Zealand AI Data Center Market, CAGR |

20.30% |

| New Zealand AI Data Center Market Size 2035 |

USD 1,356.09 Million |

The market is experiencing rapid growth driven by AI adoption across industries, cloud computing expansion, and strong demand for data sovereignty. Investments in GPU-optimized infrastructure, edge AI deployments, and energy-efficient design are reshaping the sector. Enterprises and governments increasingly rely on AI for automation, analytics, and predictive intelligence, making the market essential for digital competitiveness. It enables low-latency processing, supports high-density workloads, and aligns with sustainability targets. Businesses view it as a foundation for long-term innovation and economic productivity.

North Island leads the New Zealand AI Data Center Market due to its urban concentration, robust IT infrastructure, and cloud availability zones. Auckland and Wellington anchor most deployments, benefiting from high demand and network proximity. South Island is emerging with green-powered facilities and land availability supporting sustainable builds. Smaller regions are gaining traction for modular edge deployments in agriculture and logistics. This geographic distribution ensures redundancy, localized services, and broader national AI enablement.

Market Dynamics:

Market Drivers

Rising Demand for AI Workloads and Cloud-Based Data Services

The New Zealand AI Data Center Market is expanding due to surging enterprise demand for AI computing. Organizations across industries are deploying high-performance infrastructure to support generative AI and ML use cases. Local cloud providers and global hyperscalers are investing in compute-heavy facilities. These centers help process vast data volumes securely and efficiently. AI data centers now act as the foundation for digital transformation across business sectors. Private and public sector initiatives are fueling deployment of AI-ready hardware and orchestration software. Hybrid cloud adoption and AI-driven analytics tools increase workload complexity. Businesses view the market as strategic for scalability, resilience, and latency optimization. It plays a critical role in supporting innovation across industries.

- For instance, Datagrid developing a multi-building data center campus targeting over 100 MW capacity for high-density AI workloads. Local cloud providers and global hyperscalers are investing in compute-heavy facilities.

Integration of Advanced AI Technologies Into Core Business Models

Enterprises in New Zealand are embedding AI into their operations, driving demand for scalable infrastructure. NLP, computer vision, and neural network applications require specialized servers and low-latency architecture. Companies are aligning IT investments with AI strategies for automation, customer experience, and predictive insights. Local and regional firms see data center partnerships as essential to staying competitive. The New Zealand AI Data Center Market enables these players to process data closer to the source, improving performance and compliance. Industry-wide shift toward intelligent systems makes it vital for business continuity and digital growth. The rollout of AI-as-a-Service platforms fuels investment in dynamic data environments. Adoption of AI-optimized GPUs, liquid cooling, and orchestration tools shows a clear commitment to long-term tech readiness. It supports end-to-end data value chain execution.

Public Sector Digital Modernization and AI Policy Support

Government-led digital transformation agendas are promoting investment in AI infrastructure. National policies are encouraging localized processing, data sovereignty, and secure cloud access. Public cloud and on-premise AI infrastructure are being scaled for defense, healthcare, and education applications. New Zealand’s stable regulatory framework and strong sustainability goals attract global technology players. These players seek to leverage AI data centers to meet green compliance and workload efficiency. The New Zealand AI Data Center Market benefits from regional funding incentives and partnerships. Agencies are adopting AI to improve services like fraud detection, traffic management, and citizen engagement. It also supports collaborations in smart city projects and climate modeling. Such public-private partnerships give the market long-term momentum and stability.

- For instance, Microsoft partnering with Contact Energy for 51.4 MW renewable power supply from the Te Huka 3 station to support AI data center operations.

Edge Expansion and Support for Low-Latency AI Applications

AI workloads are increasingly being deployed at the edge, closer to the end user. This is driven by use cases like autonomous systems, real-time video analytics, and industrial automation. Edge and micro data centers reduce latency and enhance responsiveness for time-sensitive tasks. Telecom firms and infrastructure providers are integrating AI-ready edge solutions. The New Zealand AI Data Center Market sees growth in distributed, modular infrastructure tailored for low-latency processing. AI-specific edge deployments are enabling seamless operations in agriculture, energy, and logistics. Companies prioritize proximity-based computing for better customer experiences. High-speed connectivity and 5G rollouts amplify edge computing demand. It drives the need for agile, scalable, and localized AI infrastructure.

Market Trends

Green AI Infrastructure and Sustainability-Driven Data Center Development

Data centers are evolving toward energy-efficient, low-emission operations. Operators adopt liquid cooling, renewable energy sourcing, and carbon tracking to meet ESG goals. New Zealand’s clean energy mix supports green AI infrastructure development. Companies are using sustainability as a key differentiator when expanding or relocating data operations. The New Zealand AI Data Center Market integrates green building certifications and energy reuse systems. Industry leaders see net-zero targets as core to long-term competitiveness. AI workloads, being energy intensive, drive demand for efficient power and thermal management. Eco-friendly infrastructure attracts government incentives and international partnerships. It reinforces the country’s position in sustainable digital innovation.

AI-Optimized Hardware Integration Across Compute Infrastructure

AI model training and inference demand tailored compute infrastructure with high-throughput processing. Providers are deploying GPU clusters, ASICs, and high-bandwidth memory systems. This shift boosts workload density and throughput across AI environments. The New Zealand AI Data Center Market integrates NVIDIA H100s and similar accelerators for heavy AI workloads. Facilities now support rack densities above 50 kW and modular cooling. Vendors align hardware with AI training tools and orchestration stacks. Compatibility with major ML frameworks becomes critical for developers. Hardware innovation plays a central role in unlocking AI use cases. It shapes data center design, investment cycles, and workload optimization strategies.

Growth in AI-Driven Data Center Automation and Orchestration Tools

AI and machine learning are not just workloads—they also enhance how data centers operate. AI is now embedded into orchestration, thermal management, and fault detection. Providers use predictive analytics to reduce energy waste, schedule workloads, and avoid outages. The New Zealand AI Data Center Market sees growing adoption of autonomous DCIM tools. AI-based management improves uptime, enhances efficiency, and reduces operational overhead. It enables smarter capacity planning and dynamic resource scaling. Automation helps meet SLAs for demanding AI and enterprise clients. Integrated monitoring platforms reduce manual intervention across assets. These capabilities transform traditional facility operations into intelligent ecosystems.

AI-Centric Cloud Services and Ecosystem Expansion

Cloud platforms are tailoring services specifically for AI development and deployment. These include pre-trained models, low-code AI tools, and scalable GPU-based infrastructure. Enterprise clients prefer managed services that reduce development complexity. The New Zealand AI Data Center Market plays a key role in supporting AI-based cloud offerings. Global cloud vendors invest in local availability zones to improve latency and compliance. This fuels demand for edge zones and backup sites. AI services are bundled with analytics, IoT, and digital twin tools. Local firms benefit from seamless access to end-to-end AI stacks. This trend strengthens the data center’s strategic value in digital ecosystems.

Market Challenges

Infrastructure Constraints and Power Scalability Limitations

The New Zealand AI Data Center Market faces constraints in securing scalable power for AI-intensive workloads. Many regions lack high-density grid connectivity and substation readiness. Large-scale deployments demand resilient, multi-megawatt power systems. Land availability near renewable sources is also limited, slowing project timelines. Aging infrastructure in certain zones makes upgrades complex and cost-heavy. Providers struggle to align growth with sustainable energy sourcing. Equipment delivery timelines are impacted by global chip shortages and logistics lags. These infrastructure and supply hurdles restrict deployment speed. It reduces the market’s ability to support hyperscale demand efficiently.

Talent Shortage and Regulatory Complexity for AI Workloads

The pace of AI data center expansion is constrained by a limited skilled workforce. The market lacks sufficient professionals trained in AI infrastructure management, cooling optimization, and cybersecurity. Operators must invest heavily in training and certification programs. Regulatory policies on data localization and AI use are still evolving. This adds uncertainty to long-term planning for international players. The New Zealand AI Data Center Market must balance privacy, ethics, and performance in AI applications. Compliance overhead delays project approvals and increases costs. These talent and policy gaps slow down full-scale AI integration into digital infrastructure.

Market Opportunities

Emergence of AI Innovation Hubs and Start-up Ecosystems

The rise of AI startups and R&D centers fuels demand for agile, scalable infrastructure. Co-location services and modular deployments support rapid experimentation and prototyping. The New Zealand AI Data Center Market serves as an enabler for this innovation. It supports industry-academia collaborations and attracts global research partnerships. AI incubation centers seek compute access that balances speed, cost, and regulation.

Cross-Sector AI Adoption in Critical Economic Verticals

Healthcare, banking, and logistics sectors are scaling AI adoption rapidly. Demand for secure, compliant AI data processing fuels vertical-specific infrastructure. The New Zealand AI Data Center Market taps this cross-sector momentum. Sector-focused facilities enable tailored solutions, accelerating commercialization of AI use cases.

Market Segmentation

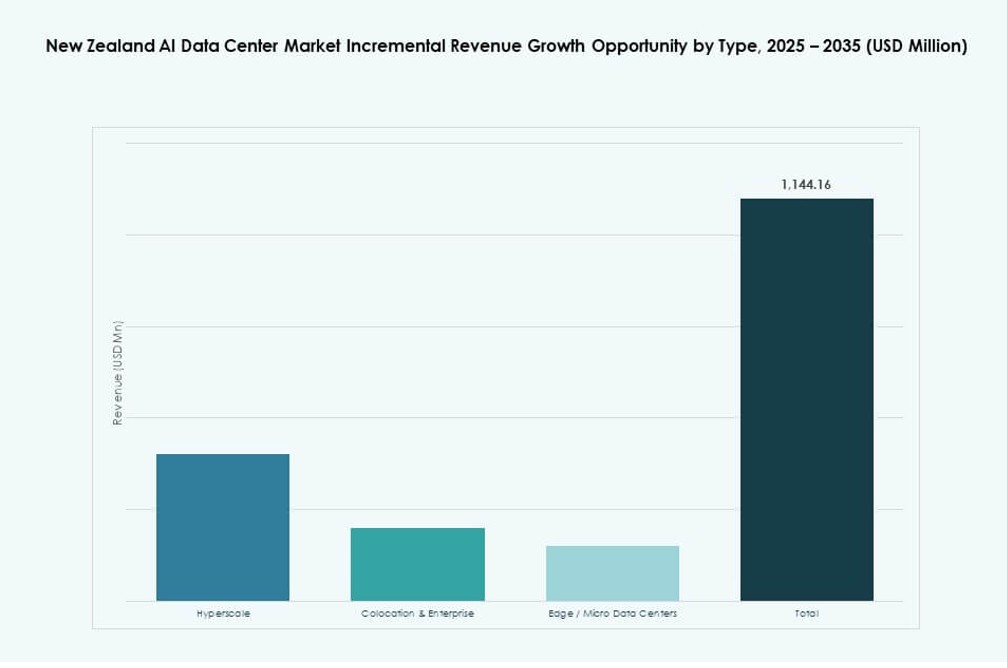

By Type

The hyperscale segment dominates the New Zealand AI Data Center Market, driven by global cloud providers and enterprise-scale workloads. Colocation & enterprise centers follow, supporting regional companies and AI start-ups. Edge/micro data centers are emerging, addressing low-latency needs in smart city and industrial projects.

By Component

Hardware is the leading component, with high demand for GPUs, ASICs, and power systems. Software & orchestration tools are gaining traction for managing complex AI workloads. Services are essential for deployment, maintenance, and continuous optimization of AI environments.

By Deployment

Hybrid deployment leads in the New Zealand AI Data Center Market, offering flexibility and control across public and private infrastructure. Cloud deployment follows, supported by hyperscaler investments. On-premise AI data centers are used in defense and financial sectors for compliance.

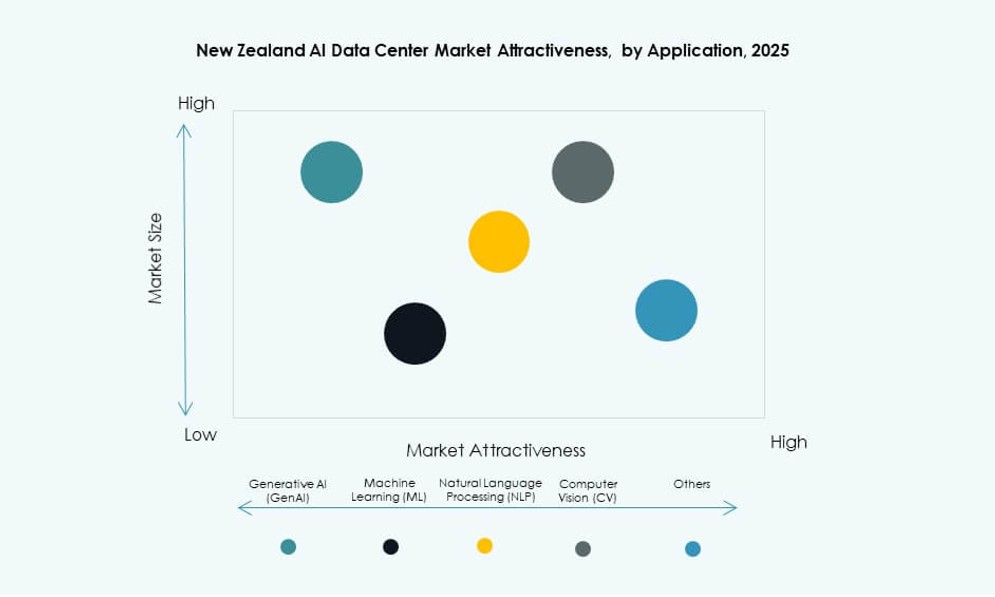

By Application

Machine learning holds the largest share, driven by its widespread use across sectors. Generative AI and NLP are rapidly growing due to creative and automation applications. Computer vision supports retail, manufacturing, and healthcare use cases. Other AI applications include robotics and predictive maintenance.

By Vertical

IT and telecom dominate the New Zealand AI Data Center Market due to their AI-first strategies. BFSI, healthcare, and retail sectors are expanding their AI footprint. Media, manufacturing, and automotive sectors follow, integrating AI to improve efficiency and customer outcomes.

Regional Insights

North Island: Leading With 62% Share Due to Urbanization and Infrastructure Readiness

North Island holds the largest market share in the New Zealand AI Data Center Market, accounting for nearly 62% of total deployments. Auckland and Wellington lead with strong telecom backbones, proximity to business hubs, and advanced IT infrastructure. These cities support major AI workloads in finance, government, and media. The region also attracts global cloud vendors due to favorable connectivity and talent availability. It anchors national digital transformation and AI growth initiatives.

- For instance, Spark New Zealand completed a 10MW expansion at its Takanini data center in Auckland, bringing total capacity to 12.3MW as of 2024.

South Island: Emerging Region With 24% Market Share Driven by Green Energy and Land Access

South Island represents around 24% of the market, growing steadily with its focus on sustainability. Christchurch and Dunedin are seeing increased data center activity, supported by clean energy access and regional grants. The cooler climate reduces cooling costs for AI workloads, while land availability supports hyperscale builds. The region is positioning itself as a low-carbon AI infrastructure hub. It draws attention from eco-focused tech companies.

Rest of the Regions: Account for 14% Share With Niche Applications and Edge Expansion

Other regions together account for 14% of the market, mainly in support of edge AI use cases. These include agricultural analytics, transport optimization, and distributed smart systems. Smaller cities are adopting modular micro data centers for real-time processing. These deployments are closer to AI-powered operations in forestry, dairy, and logistics. The New Zealand AI Data Center Market expands here via government and private sector co-investments. It adds resilience and geographic diversity to the country’s AI infrastructure landscape.

- For instance, Spark New Zealand operates 11 data centers nationwide with over 23MW total built capacity as of 2025, including regional sites in Waikato and Bay of Plenty for distributed operations

Competitive Insights:

- Datacom

- Spark Digital

- Revera

- Equinix

- Digital Realty Trust

- Microsoft (Azure)

- Amazon Web Services (AWS)

- Google Cloud

- Hewlett Packard Enterprise (HPE)

- NVIDIA

The New Zealand AI Data Center Market is shaped by both global cloud hyperscalers and local infrastructure providers. Datacom, Spark Digital, and Revera lead domestic operations with established enterprise partnerships. AWS, Microsoft, and Google Cloud continue expanding their cloud zones to support AI services locally. Equinix and Digital Realty provide scalable colocation environments for AI training and inference workloads. NVIDIA and HPE enable GPU-accelerated computing across deployments. It remains a competitive environment with differentiation based on sustainability, latency, and integration with AI frameworks. Players focus on modular builds, green compliance, and automation to capture AI workloads from healthcare, BFSI, and government clients.

Recent Developments:

- In September 2025, AWS launched its sovereign New Zealand cloud region featuring three availability zones and a long-term renewable-energy power purchase agreement with Mercury NZ. This initiative supports local AI processing for businesses like Vector and Datacom while enhancing data sovereignty through domestic storage options.

- In August 2025, Spark New Zealand agreed to sell a minority stake in its data center portfolio to reduce leverage and prioritize service expansion. The move aligns with surging AI infrastructure needs, freeing capital for higher-density racks suited to GPU training under the government’s AI strategy.