Executive summary:

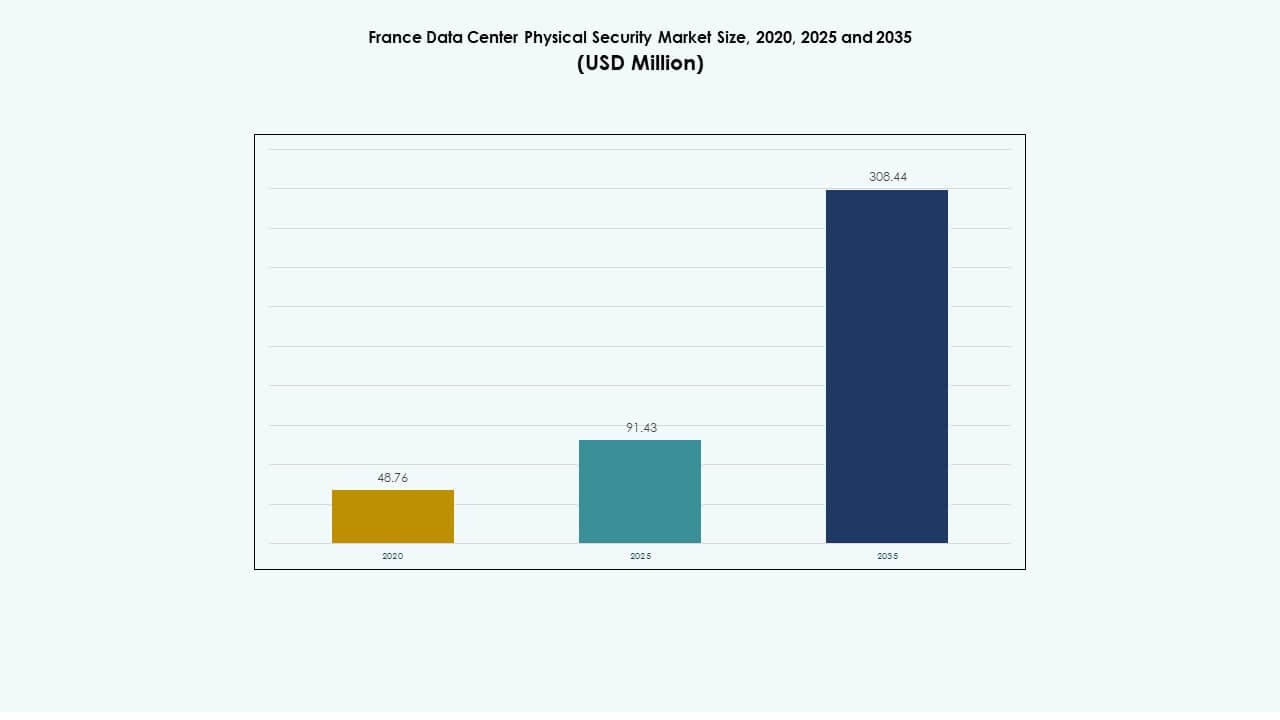

The France Data Center Physical Security Market size was valued at USD 48.76 million in 2020 to USD 91.43 million in 2025 and is anticipated to reach USD 308.44 million by 2035, at a CAGR of 12.87% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2035 |

| France Data Center Physical Security Market Size 2025 |

USD 91.43 Million |

| France Data Center Physical Security Market, CAGR |

12.87% |

| France Data Center Physical Security Market Size 2035 |

USD 308.44 Million |

Strong demand for advanced surveillance, access control, and AI-enabled monitoring drives market growth. Rising colocation and hyperscale data centers create greater focus on integrated security frameworks. Companies adopt biometric systems, smart sensors, and automation tools to enhance compliance and resilience. The market’s strategic importance lies in its role in safeguarding digital infrastructure, which attracts significant investor attention and technology innovation.

Île-de-France leads the market due to its dense concentration of enterprise and hyperscale data centers. Marseille follows with expanding edge and colocation developments linked to international connectivity. Northern and Western France emerge as new growth corridors supported by digital transformation initiatives and industrial expansion.

Market Drivers

Market Drivers

Rising Focus on Multi-Layered Data Center Security Infrastructure

The France Data Center Physical Security Market grows with the need for strong multi-layered protection across hyperscale and colocation facilities. Companies implement perimeter, access, and rack-level security to counter physical intrusion and data theft. Demand for AI-based video analytics rises to enhance real-time threat detection accuracy. Firms prioritize biometric access, integrated alarms, and remote monitoring to strengthen resilience. Government and industry compliance requirements drive continuous upgrades in physical infrastructure. It supports tighter operational control within critical environments. Strong security investments enhance investor confidence and reduce operational risk across key digital assets.

- For instance, Axis Communications’ ARTPEC-9 system-on-chip powers cameras with AI-based object analytics, 31× optical zoom, and OptimizedIR technology for high-precision night surveillance. These models enable real-time detection and classification directly on the edge, improving accuracy and reducing false alarms in secure data center environments.

Increasing Integration of AI and IoT in Physical Security Systems

Data centers in France rapidly adopt AI, IoT, and analytics-driven platforms to achieve predictive security. These systems analyze real-time patterns across sensors, access points, and video feeds to detect anomalies. Smart sensors support environmental control and unauthorized movement alerts. AI-based systems optimize manpower use and response timing. Firms deploy cloud-based control centers that manage distributed sites effectively. Integration between cyber and physical security platforms ensures unified monitoring. It creates new standards for compliance and operational transparency. Investors value this integration for ensuring long-term reliability and scalability.

- For instance, Johnson Controls delivers integrated security platforms that combine AI-enabled video analytics, access control, and intrusion detection. These systems provide centralized monitoring and automated threat recognition, enhancing protection and operational visibility across enterprise and data center environments.

Expansion of Colocation and Edge Facilities Creating Security Complexity

Rapid growth in colocation and edge deployments introduces security complexity in distributed infrastructure. Operators must coordinate layered controls across multiple access zones and remote nodes. The France Data Center Physical Security Market benefits from investments in advanced identity verification and video surveillance. Vendors focus on scalable systems that ensure uniform protection regardless of site size. Edge sites require compact yet efficient solutions for limited-space operations. Continuous innovation supports seamless integration between central hubs and remote centers. It strengthens the country’s network resilience and operational continuity. Data-driven solutions ensure consistent security oversight across expanding infrastructure.

Regulatory Alignment and Strategic Infrastructure Modernization

Strict compliance with EU and national data protection laws influences rapid modernization of security systems. Firms implement GDPR-aligned physical control measures across all operational zones. Government-led initiatives encourage adoption of high-availability and redundancy frameworks. The market evolves around certified solutions that satisfy ISO and Tier IV requirements. It highlights the strategic role of secure data hosting in France’s digital economy. Integration of sustainability and energy efficiency further increases capital inflow. Security providers collaborate with hyperscalers to build long-term risk mitigation strategies. Consistent upgrades ensure national data sovereignty and investor trust.

Market Trends

Market Trends

Adoption of AI-Powered Video Analytics for Predictive Security Monitoring

AI-based video surveillance becomes central to proactive protection strategies. Cameras powered by neural analytics detect suspicious patterns and automate incident reporting. The France Data Center Physical Security Market experiences a shift toward deep-learning models for anomaly detection. Firms replace traditional systems with intelligent software that reduces false alarms. Predictive maintenance models optimize equipment uptime and enhance threat readiness. AI-driven analytics also provide detailed audit trails for regulatory inspections. It enables continuous learning across vast data inputs. The approach reduces human dependency while ensuring faster response accuracy.

Integration of Cloud-Based Access Management Systems

Data centers increasingly use cloud-native platforms for centralized access control management. Operators deploy scalable authentication models linked to identity databases. These systems support hybrid access verification through biometrics and card-based entry. It allows faster updates across multiple sites while ensuring data consistency. Vendors introduce unified dashboards for real-time entry tracking and compliance reporting. Cloud integration improves efficiency, especially for colocation providers managing multiple clients. Firms gain improved visibility into physical operations. This trend drives adoption of flexible, software-defined control layers across large infrastructures.

Emergence of Modular Security Architecture for Edge Deployments

Edge data centers demand modular, adaptive security systems that fit smaller footprints. Vendors develop compact, plug-and-play units with automated perimeter detection. The France Data Center Physical Security Market benefits from flexible architectures supporting quick upgrades. These systems can scale with capacity expansion and remote operations. Operators prefer designs that reduce maintenance and installation time. Modular solutions help maintain uniformity across distributed sites. It ensures consistent security standards in rural and urban zones alike. The trend reflects growing interest in simplified yet effective infrastructure solutions.

Emphasis on Sustainability and Energy-Efficient Security Systems

Security equipment now integrates energy-saving modes and renewable power compatibility. Manufacturers design low-power surveillance cameras and smart lighting systems. Facilities implement sustainable cabling and energy recovery technologies. It reduces total cost of ownership for large data center operators. France’s green transition policies accelerate deployment of eco-certified systems. Vendors align product development with carbon-neutral goals. Intelligent control software optimizes equipment runtime without compromising performance. Sustainable innovation strengthens France’s position as a key hub for secure, eco-efficient data operations.

Market Challenges

High Implementation Costs and Complexity of System Integration

Integrating multi-vendor hardware and software across large-scale facilities creates cost and compatibility challenges. The France Data Center Physical Security Market faces pressure from rising installation expenses for AI-enabled systems. Many operators struggle to synchronize old and new infrastructure layers. Skilled workforce shortages delay project completion and increase operational risks. Maintaining uptime during upgrades requires redundant systems, which further elevate costs. It also demands regular software updates and certification renewals. Smaller facilities find such transitions financially difficult. Complex integration slows technology adoption among mid-tier providers.

Evolving Cyber-Physical Threat Landscape and Regulatory Pressure

Hybrid security risks now extend beyond physical intrusion to include coordinated cyberattacks. Operators must secure control systems and IoT sensors connected to corporate networks. The market faces growing pressure to meet evolving compliance standards under EU laws. Non-compliance can lead to penalties and customer loss. It also raises demand for continuous auditing and threat simulations. Companies must balance investment in security hardware with advanced analytics solutions. Rapid innovation outpaces regulation, creating uncertainty in planning cycles. Vendors and end-users must maintain alignment between technology evolution and legal frameworks.

Market Opportunities

Growing Investments in Hyperscale and Edge Infrastructure Development

Large-scale hyperscale expansions across Paris and Marseille create vast opportunities for security vendors. Firms require scalable access management, AI analytics, and redundancy frameworks. The France Data Center Physical Security Market benefits from modernization plans backed by European digital funding. Edge data centers in secondary regions also require affordable, automated monitoring systems. Vendors offering modular, interoperable products can capture strong market share. It positions France as a strategic security innovation hub for Western Europe. Partnerships with telecom operators and colocation providers will strengthen long-term adoption.

Advancement in Smart Sensor and Automation Technologies

Demand grows for intelligent sensors integrating motion detection, thermal imaging, and facial analytics. These innovations improve situational awareness and cut false alerts. AI-enabled control centers unify operations across multiple data halls. Security automation reduces manual intervention, enhancing reliability and cost efficiency. It allows faster decision-making and improves scalability. The rise of autonomous systems supports operational resilience and predictive maintenance. Vendors focusing on automation-centric offerings can gain a competitive edge. Long-term contracts with hyperscalers ensure stable revenue growth.

Market Segmentation

Market Segmentation

By Data Center Size

Large data centers dominate due to high density of hyperscale and colocation projects in Paris and Marseille. These facilities invest in multi-layered security frameworks with 24/7 surveillance and access control. Medium-sized data centers show steady demand driven by regional IT expansion. Small data centers adopt modular systems to balance cost and performance. The France Data Center Physical Security Market benefits from ongoing modernization of legacy infrastructure. Larger facilities lead market share due to extensive regulatory compliance and power capacity growth.

By Component

Solutions account for a major share, led by video surveillance, biometric access, and monitoring platforms. Organizations invest in integrated systems combining multiple technologies for holistic protection. Services grow steadily, especially in consulting and maintenance contracts. Managed services gain popularity among colocation and enterprise operators seeking scalability. The France Data Center Physical Security Market continues shifting toward full-service security packages. Vendors offering end-to-end integration solutions dominate the competitive landscape.

By Solution

Video surveillance remains the most deployed solution, followed by access control and monitoring systems. AI-driven cameras and facial recognition improve detection efficiency. Monitoring and detection tools ensure early risk identification through continuous analytics. Access control supports compliance with international data protection standards. Other solutions like intrusion alarms and anti-tailgating systems complement layered defense. The France Data Center Physical Security Market favors high-accuracy and low-latency systems for operational reliability.

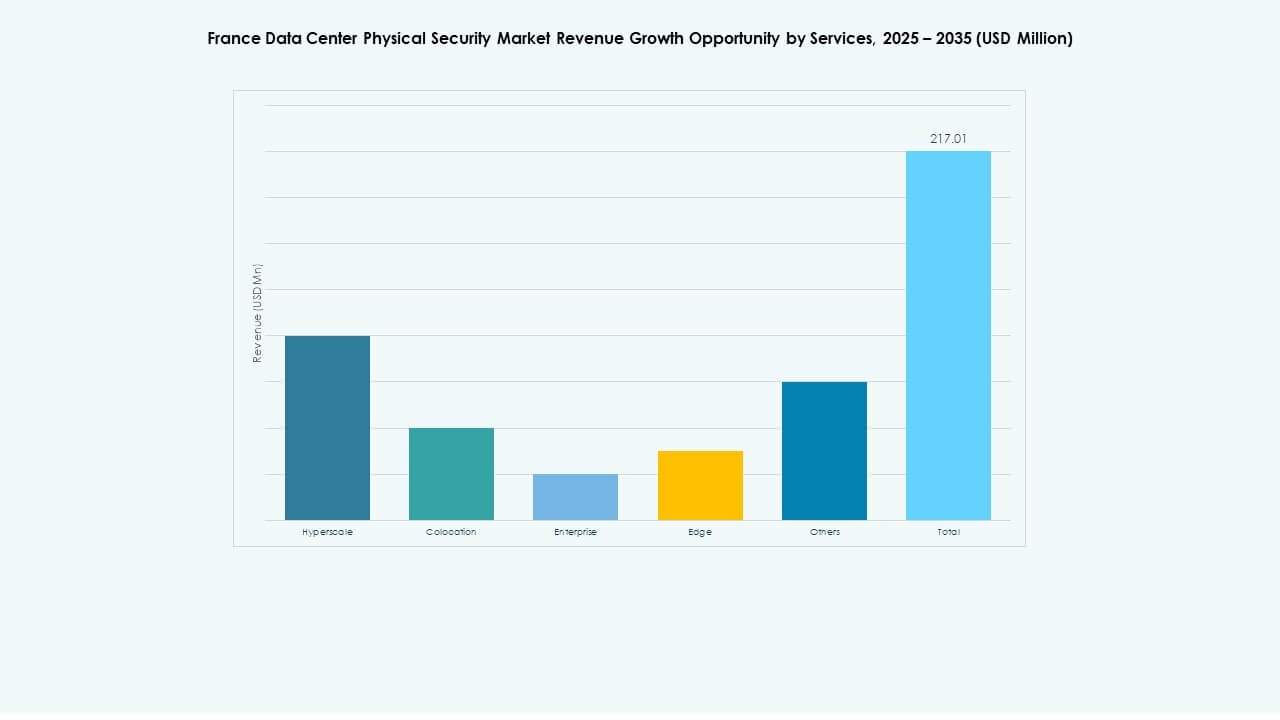

By Services

System integration holds the largest share due to demand for seamless connectivity across hardware and software. Consulting services expand with regulatory alignment and risk assessment projects. Maintenance and support remain essential for ensuring uptime and equipment calibration. Managed contracts increase due to labor shortages and complex architectures. The France Data Center Physical Security Market gains strength from vendor partnerships with hyperscale developers. Service providers focusing on lifecycle management and predictive maintenance gain steady traction.

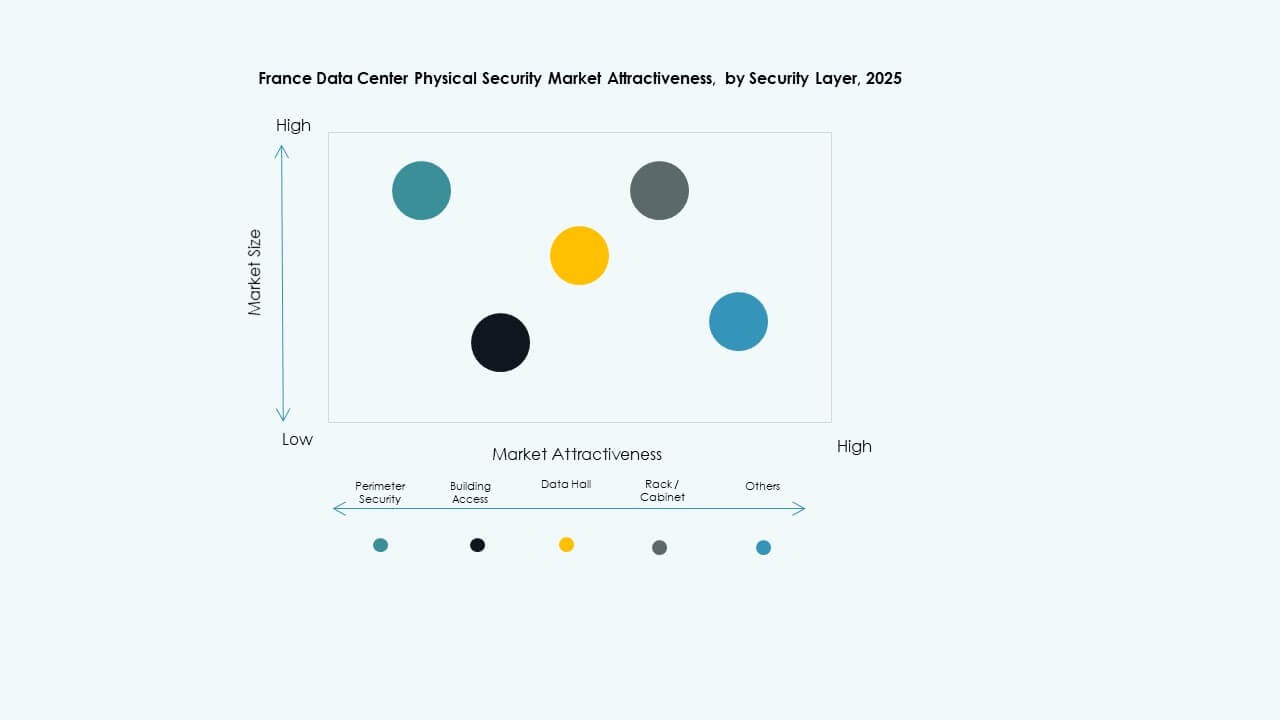

By Security Layer

Perimeter security and building access dominate due to strict entry protocols. Data hall and rack-level systems grow rapidly with AI surveillance and biometric access. Monitoring systems at each layer provide redundancy and audit control. The France Data Center Physical Security Market emphasizes comprehensive defense across layers. Operators integrate motion sensors, locking systems, and real-time analytics. This layered model improves visibility and reduces operational vulnerabilities across all zones.

By Data Center Type

Hyperscale data centers lead with major investments from global cloud providers. Colocation sites follow closely, supporting enterprise and SME demand. Edge facilities expand in emerging zones to improve latency and connectivity. Enterprise and government data centers adopt hybrid physical-cyber security models. The France Data Center Physical Security Market reflects strong synergy between infrastructure and automation. Hyperscale sites maintain the highest compliance and advanced access frameworks.

By End-User

IT and telecom remain dominant, followed by BFSI and government segments. High data sensitivity drives heavy investment in advanced access systems. Healthcare and life sciences adopt integrated surveillance for regulatory alignment. Retail and e-commerce deploy modular systems in distribution hubs. Manufacturing sites use perimeter protection and access monitoring. The France Data Center Physical Security Market supports broad adoption across industrial and public sectors.

Regional Insights

Île-de-France: Dominant Regional Hub

Île-de-France accounts for nearly 60% of the market share driven by hyperscale facilities in Paris. The region’s dense digital infrastructure and connectivity networks attract global investors. Large enterprises deploy AI-enabled systems and multi-layered protection frameworks. The France Data Center Physical Security Market benefits from strict regulatory compliance in this region. Strong government policies and infrastructure incentives sustain continued investment. It remains the core location for high-capacity data centers.

Southern France: Expanding Edge and Colocation Presence

Southern France, led by Marseille, holds around 25% market share with rapid edge and colocation expansion. Its strategic coastal position and submarine cable access support high data throughput. Operators enhance security against both physical and environmental threats. AI-based surveillance and modular control centers become more prevalent. It gains prominence as a backup and interconnection hub for global cloud networks. The area attracts increasing hyperscale partnerships and regional security deployments.

- For instance, Microsoft is expanding its Marseille data center as part of the same €4 billion investment, leveraging the site’s connectivity for AI infrastructure growth.

Western and Northern Regions: Emerging Growth Corridors

Western and Northern France collectively account for nearly 15% of the market share. These zones witness new investments in edge and enterprise-level data centers. Strong focus on industrial digitization drives new deployments. It strengthens France’s overall geographic diversity in secure hosting infrastructure. Government-led digital transformation initiatives enhance regional competitiveness. These emerging corridors promise balanced future growth across distributed physical security networks.

- For instance, Data4 Group operates large-scale data center campuses in Paris-Saclay and Marcoussis, offering over 250 MW of IT power capacity. These sites feature ISO-certified physical security, redundant power infrastructure, and modular design to support enterprise and hyperscale deployments across France.

Competitive Insights:

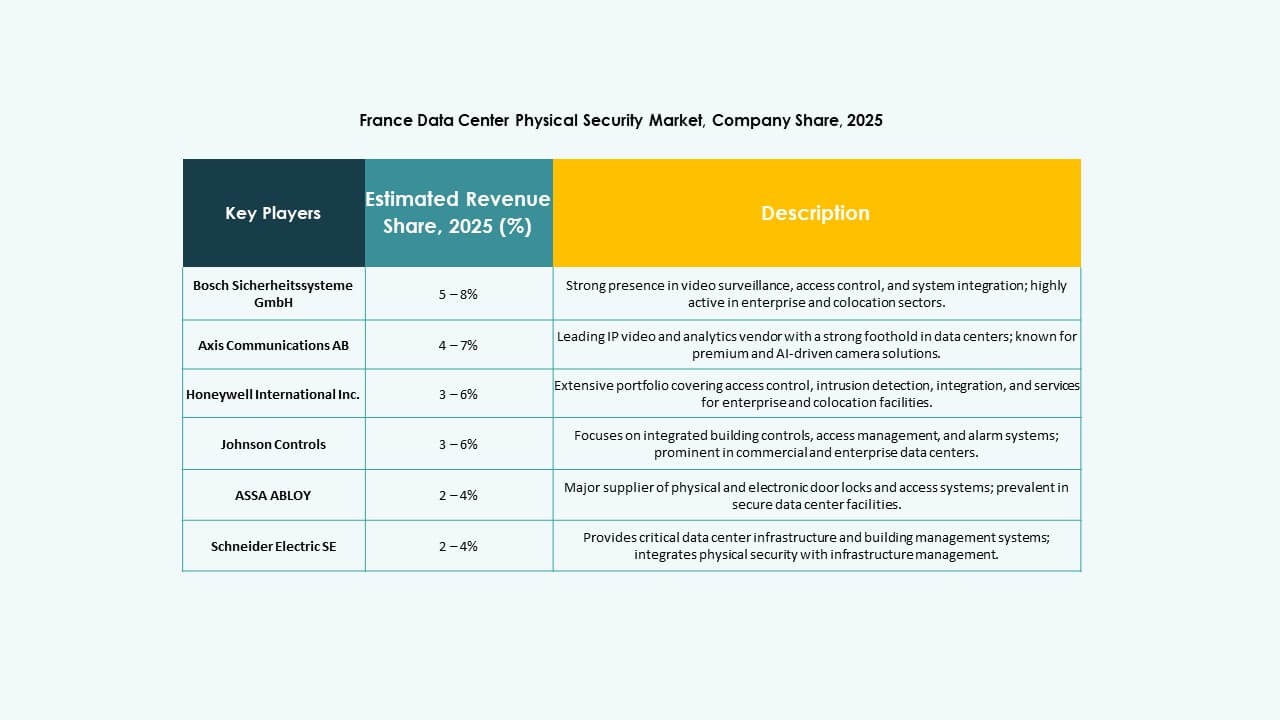

- Bosch Sicherheitssysteme GmbH

- Securitas AB

- Axis Communications AB

- Honeywell International Inc.

- Johnson Controls

- Schneider Electric SE

- ABB Ltd

- Siemens AG

- Cisco Systems, Inc.

- Genetec

The competitive landscape in the [ France Data Center Physical Security Market] features a mix of legacy security titans and agile technology-oriented vendors. Leading firms maintain dominance through broad portfolios covering surveillance, access control, and integrated security services. Vendors such as Bosch, Honeywell and Siemens leverage global operations and strong brand trust to serve hyperscale and enterprise data centers. Meanwhile, technology-driven providers like Axis and Cisco push edge-ready, IP-based security solutions. Service-focused companies such as Securitas and Johnson Controls deliver managed security and compliance support, which appeals to colocation and mid-tier data center operators. Intense competition accelerates innovation cycles and forces firms to differentiate via scalability, integration capabilities, and compliance readiness to secure long-term contracts.

Recent Developments:

Recent Developments:

- In October 2025, ASSA ABLOY acquired Kentix GmbH, a German company specializing in monitoring and access control products designed for data centers, enhancing their capabilities in physical security for this sector.

- In December 2024, Bosch Sicherheitssysteme GmbH sold its security and communications technology product business to the European investment firm Triton. The transaction included three business units Video, Access and Intrusion, and Communication as Bosch aims to focus more on systems integration business.