Executive summary:

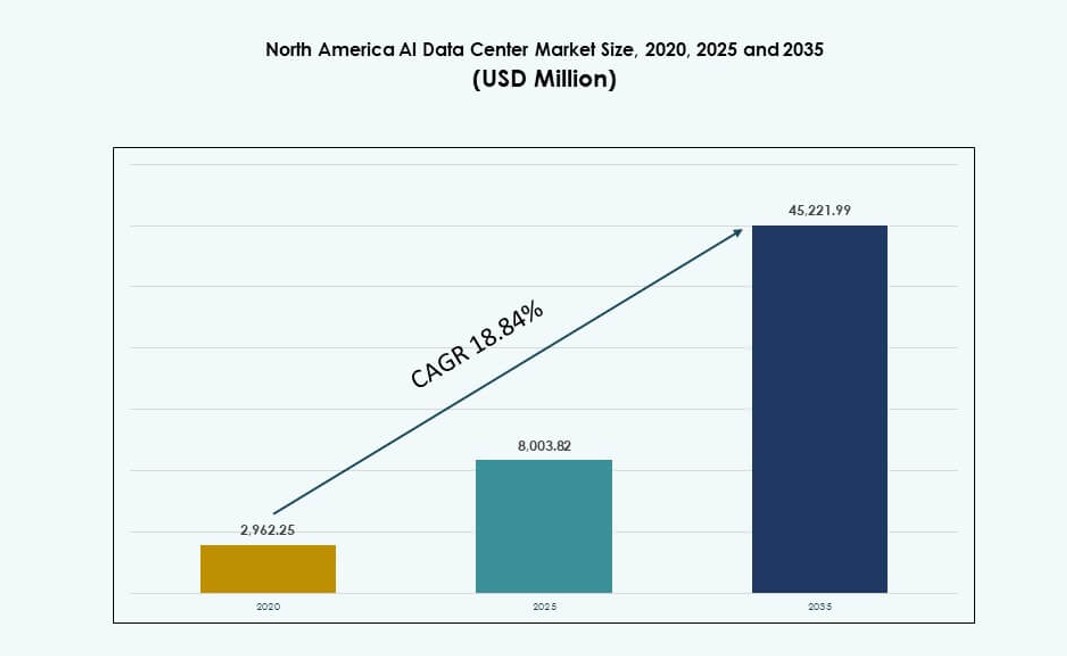

The North America AI Data Center Market size was valued at USD 2,962.25 million in 2020 to USD 8,003.82 million in 2025 and is anticipated to reach USD 45,221.99 million by 2035, at a CAGR of 18.84% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2035 |

| North America AI Data Center Market Size 2025 |

USD 8,003.82 Million |

| North America AI Data Center Market, CAGR |

18.84% |

| North America AI Data Center Market Size 2035 |

USD 45,221.99 Million |

Strong momentum in the North America AI Data Center Market comes from hyperscalers and enterprises deploying high-density racks for AI training. Demand for GPU-based systems and AI-specific silicon pushes power density thresholds. Operators integrate liquid cooling, modular design, and AIOps to boost operational efficiency. GenAI, NLP, and computer vision workloads increase space, power, and thermal requirements. AI infrastructure shifts from isolated clusters to regionally scaled facilities. Cloud providers build AI-optimized zones with localized data processing. It creates durable investment pathways and vendor ecosystem alignment. The market’s strategic role strengthens across verticals like healthcare, telecom, and BFSI.

The United States leads the North America AI Data Center Market with the largest market share, driven by hyperscale cloud concentration and AI infrastructure maturity. Canada follows with strong growth, supported by abundant renewable energy, cooler climates, and AI research initiatives. Mexico is emerging, powered by nearshoring trends, cross-border interconnection, and regional cloud infrastructure expansion. Geographic proximity to U.S. cloud nodes supports demand aggregation. It helps enable distributed AI computing and improves service availability across the region.Frequently Asked Questions:

Market Dynamics:

Market Drivers

Acceleration Of Large-Scale AI Model Training And Inference Workloads

The North America AI Data Center Market expands due to rapid growth in model training demand. Enterprises deploy large language models across search, healthcare, and finance. Training cycles require dense GPU clusters and low-latency fabrics. Data center operators redesign power and cooling layouts. Cloud platforms standardize AI-optimized server architectures. Chip vendors align roadmaps with hyperscale needs. Capital flows target scalable compute infrastructure. It strengthens long-term capacity planning confidence. Investors view this shift as structurally durable.

Rapid Adoption Of High-Density Compute And Advanced Cooling Architectures

The North America AI Data Center Market benefits from high-density rack adoption. AI servers push power levels beyond traditional limits. Operators deploy liquid and hybrid cooling systems. Facility designs shift toward modular and scalable formats. Equipment vendors deliver integrated rack solutions. Cooling innovation improves thermal stability and uptime. Energy efficiency gains support operating margins. It reduces performance bottlenecks under heavy loads. This driver supports premium colocation pricing.

- For instance, Equinix announced plans to expand liquid cooling to over 100 of its data centers across 45 metros to support high-density AI workloads, enabling more efficient thermal management across key U.S. markets like Ashburn and Silicon Valley. These deployments align with increasing rack power densities driven by GPU-based AI infrastructure.

Expansion Of Hyperscale Cloud And AI Platform Investments

The North America AI Data Center Market gains scale from hyperscale cloud expansion. Major platforms invest in AI-first regions. Custom silicon and GPU clusters anchor new campuses. Long-term power contracts secure predictable operations. Network upgrades improve east-west traffic flow. Platform ecosystems attract enterprise AI workloads. It raises entry barriers for smaller operators. Investors favor hyperscale-backed infrastructure assets. Strategic partnerships deepen market resilience.

Enterprise Digital Transformation And AI Integration Across Verticals

The North America AI Data Center Market grows with enterprise AI adoption. Healthcare uses AI for diagnostics and imaging. BFSI deploys fraud detection and risk models. Retail applies demand forecasting and personalization tools. Manufacturing adopts predictive maintenance platforms. These use cases require secure and compliant infrastructure. Data gravity favors regional data centers. It drives steady colocation demand. Businesses treat AI infrastructure as mission critical.

- For instance, GE HealthCare has used its Precision DL platform on AWS GPU instances to accelerate medical imaging workflows, demonstrating significant performance gains for AI model processing across large CT scan datasets. This deployment highlights practical use of cloud GPU compute for healthcare AI workloads.

Market Trends

Shift Toward Standardized AI-Ready Modular Data Center Designs

The North America AI Data Center Market shows a move toward modular builds. Operators prefer repeatable deployment models. Prefabricated power and cooling blocks reduce build time. Standard layouts ease capacity expansion planning. Vendors align product lines with modular needs. This trend improves deployment speed predictability. It lowers construction risk exposure. Financial models gain clarity for investors.

Rising Use Of AI-Driven Operations And Predictive Infrastructure Management

The North America AI Data Center Market adopts AI-led operations tools. Operators deploy predictive maintenance platforms. Sensor data guides thermal and power optimization. Fault detection improves service continuity. Automated workflows reduce manual intervention. It enhances uptime reliability. Operating teams scale efficiently. This trend supports margin stability.

Growing Preference For Hybrid And Multi-Cloud AI Architectures

The North America AI Data Center Market reflects hybrid deployment preference. Enterprises mix on-premise and cloud AI stacks. Sensitive workloads remain localized. Burst workloads shift to cloud regions. Interconnection demand rises across facilities. Colocation hubs gain strategic relevance. It reshapes capacity planning strategies. Vendors focus on connectivity services.

Increased Focus On Sustainability Metrics In AI Infrastructure Planning

The North America AI Data Center Market integrates sustainability benchmarks. Buyers assess carbon and energy metrics. Operators invest in efficient cooling systems. Renewable power sourcing gains priority. Reporting standards influence procurement decisions. It impacts site selection strategy. Sustainable assets attract long-term capital.

Market Challenges

Power Availability Constraints And Grid Infrastructure Limitations

The North America AI Data Center Market faces power access pressure. AI workloads demand high and stable energy supply. Grid upgrades lag rapid capacity buildouts. Permitting delays slow project timelines. Power pricing volatility affects cost forecasts. Operators compete for prime utility zones. It raises development complexity. Risk management becomes essential for investors.

Supply Chain Dependence On Advanced Hardware And Cooling Systems

The North America AI Data Center Market depends on specialized components. GPU availability fluctuates with global demand. Cooling equipment lead times remain extended. Logistics disruptions affect deployment schedules. Vendor concentration increases procurement risk. Cost escalation pressures margins. It challenges capacity forecasting accuracy. Operators diversify supplier strategies.

Market Opportunities

Expansion Of Edge And Regional AI Processing Facilities

The North America AI Data Center Market gains opportunity from edge AI growth. Latency-sensitive applications drive regional demand. Smart cities and autonomous systems require proximity compute. Smaller facilities complement hyperscale campuses. Operators target secondary metros. It opens new investment corridors. Edge assets diversify revenue streams. Long-term demand visibility improves.

Development Of AI-Optimized Colocation And Managed Services

The North America AI Data Center Market offers service-layer expansion. Enterprises seek managed AI infrastructure. Colocation providers bundle compute and orchestration tools. This model reduces client complexity. Premium services improve yield per rack. It strengthens customer stickiness. Investors favor service-led differentiation.

Market Segmentation

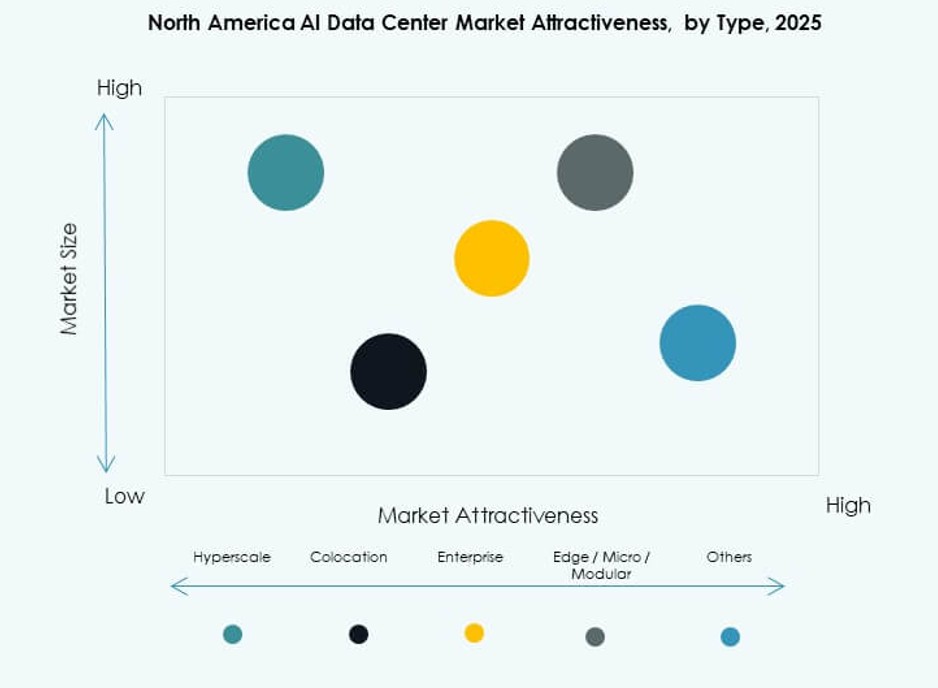

By Type

The North America AI Data Center Market sees hyperscale as the dominant type. Hyperscale facilities account for the largest market share. Cloud and AI platform operators drive demand. Colocation and enterprise data centers follow with strong growth. Enterprises seek flexible AI-ready capacity. Edge and micro data centers show rising adoption. These support low-latency workloads. Urban and regional use cases drive expansion.

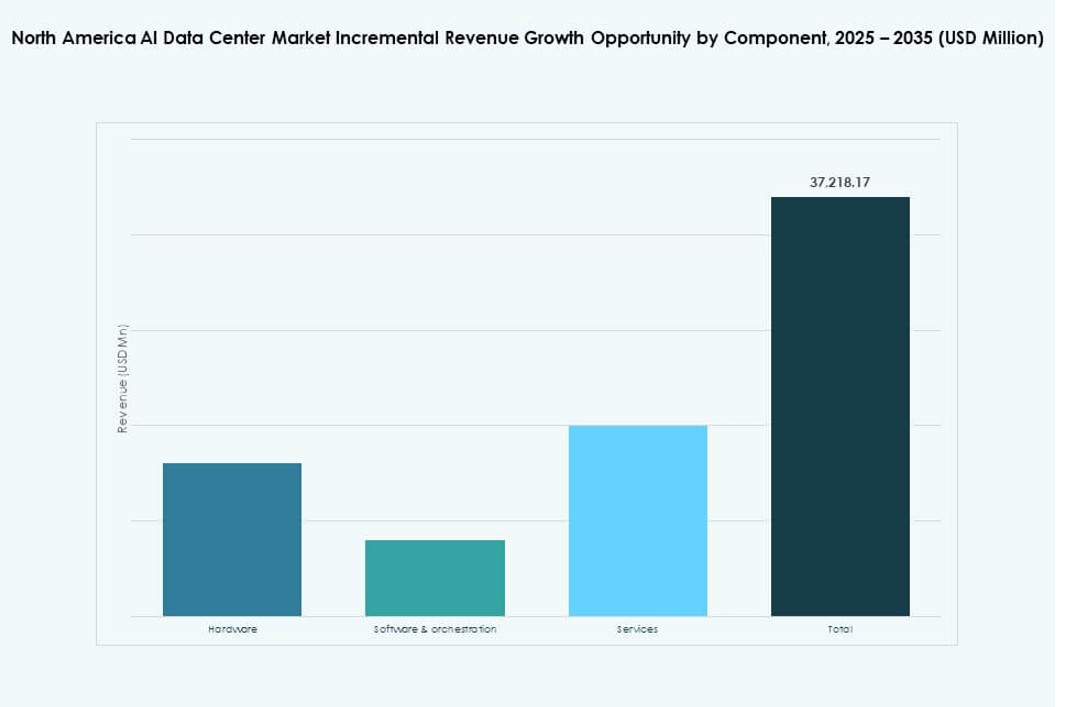

By Component

The North America AI Data Center Market remains hardware-led. Servers, accelerators, and networking dominate spend. GPUs and custom AI chips hold major share. Software and orchestration gain importance. Workload scheduling and monitoring tools expand. Services grow through managed offerings. Integration and lifecycle support gain relevance. Component balance shifts toward software value.

By Deployment

The North America AI Data Center Market favors cloud deployment. Cloud holds the largest share due to scalability. On-premise remains relevant for regulated sectors. Hybrid deployment shows the fastest growth. Enterprises balance control and flexibility. Data residency drives hybrid models. Operators design interoperable platforms. Deployment diversity shapes infrastructure planning.

By Application

The North America AI Data Center Market is led by generative AI. GenAI workloads consume the most compute capacity. Machine learning follows with broad enterprise use. NLP and computer vision expand across sectors. Media and retail drive inference demand. Other applications include robotics and analytics. Application mix increases infrastructure complexity. Growth favors high-density systems.

By Vertical

The North America AI Data Center Market sees IT and telecom lead usage. Cloud and network operators anchor demand. BFSI holds strong share due to compliance needs. Healthcare shows rapid adoption growth. Retail and media increase AI use. Manufacturing adopts predictive systems. Automotive supports autonomy research. Vertical diversity stabilizes demand cycles.

Regional Insights

United States

The North America AI Data Center Market is led by the United States with about 72% share. Hyperscale cloud concentration drives dominance. Strong AI startup and enterprise adoption support demand. Power and fiber availability favor large campuses. Federal and state incentives encourage investment. It remains the primary innovation hub. Capacity expansion continues across major metros.

- For instance, CoreSite launched its NY3 data center in Secaucus, New Jersey, adding more than 138,000 square feet of AI‑ready capacity adjacent to its existing NY2 facility, creating a highly connected campus on the Eastern Seaboard. The new site supports advanced workloads with cloud interconnection and liquid cooling for high‑density compute deployments.

Canada

The North America AI Data Center Market assigns Canada nearly 18% share. Abundant renewable energy supports sustainability goals. Cooler climates reduce cooling costs. AI research ecosystems attract infrastructure projects. Data sovereignty policies support local builds. It gains traction among global operators. Growth focuses on green facilities.

Mexico

The North America AI Data Center Market gives Mexico close to 10% share. Nearshore demand drives regional facilities. Connectivity to U.S. markets supports expansion. Edge and enterprise deployments lead growth. Cost advantages attract new entrants. It strengthens cross-border digital infrastructure. Regional importance continues to rise.

- For instance, KIO Data Centers launched its QRO2 facility in Querétaro, Mexico, expanding total regional capacity to nearly 19 MW with high-availability power and carrier-neutral connectivity. The site strengthens Querétaro’s role as a strategic digital infrastructure hub for cloud and AI workloads in North America.

Competitive Insights:

- Amazon Web Services (AWS)

- Microsoft (Azure)

- Google Cloud / Alphabet

- Meta Platforms

- NVIDIA

- Dell Technologies

- Hewlett Packard Enterprise (HPE)

- Equinix

- Digital Realty Trust

- Vantage Data Centers

The competitive landscape of the North America AI Data Center Market is defined by hyperscalers, equipment vendors, and colocation providers advancing AI infrastructure scale and capability. AWS, Microsoft, and Google dominate hyperscale cloud AI deployments with custom silicon and dedicated AI regions. Meta and NVIDIA invest heavily in GPU-powered data centers for model training. Dell, HPE, and Lenovo strengthen enterprise adoption with AI-ready server and storage systems. Equinix and Digital Realty lead in high-density colocation with strong interconnection assets. It shows intense capital flows, M&A activity, and partnerships centered on AI workloads, efficiency improvements, and regional expansion. Competitive differentiation focuses on cooling innovation, silicon acceleration, and service-layer integration. Market leaders shape long-term infrastructure strategy across the AI ecosystem.

Recent Developments:

- In September 2025, Nebius announced a $17.4 billion partnership with Microsoft to supply AI infrastructure over five years, including a new Nvidia-powered AI data center in Vineland, New Jersey.

- In July 2025, Equinix launched its largest AI-ready data hall in Ashburn, Virginia, offering 48 MW of capacity with direct cloud-exchange links tailored for North American AI infrastructure demands.

- In December 2024, NVIDIA Corporation completed its USD 700 million acquisition of Run:ai, integrating Kubernetes-native orchestration into its DGX platform suite to enhance AI workload management in data centers.

- In March 2024, Amazon Web Services earmarked USD 150 billion for new AI regions in Ohio, Oregon, and Virginia, featuring purpose-built liquid-cooling and 415 V power distribution to support high-density AI workloads.