Executive summary:

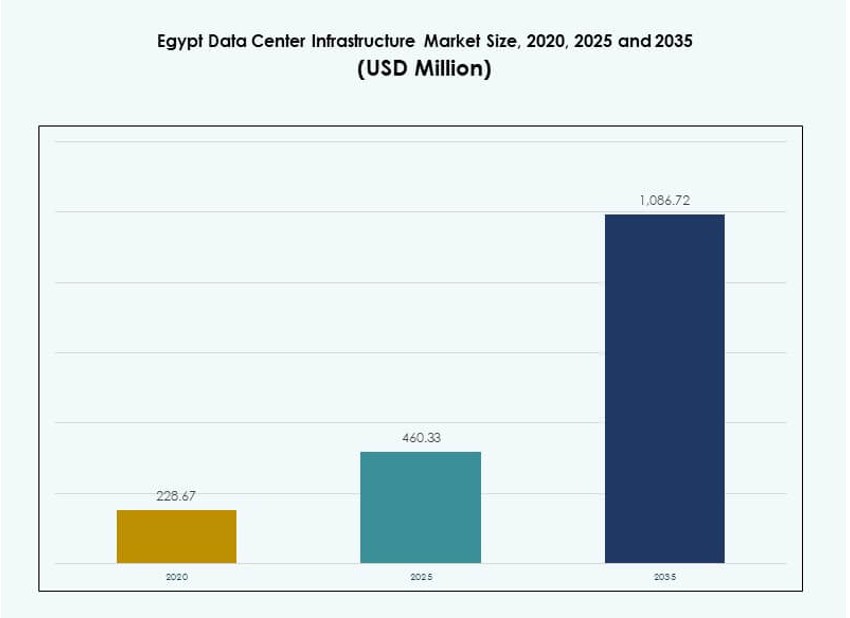

The Egypt Data Center Infrastructure Market size was valued at USD 228.67 million in 2020, grew to USD 460.33 million in 2025, and is anticipated to reach USD 1,086.72 million by 2035, at a CAGR of 8.85% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2035 |

| Egypt Data Center Infrastructure Market Size 2025 |

USD 460.33 Million |

| Egypt Data Center Infrastructure Market, CAGR |

8.85% |

| Egypt Data Center Infrastructure Market Size 2035 |

USD 1,086.72 Million |

Market growth is fueled by rising digital transformation, demand for data localization, and expansion of cloud computing. Enterprises and public institutions are investing in scalable infrastructure to support high-volume applications. Technology adoption spans modular data centers, energy-efficient cooling, and AI-driven management tools. Investors view Egypt as a strategic hub due to its location, robust submarine cable network, and regional digital growth. Innovation in edge deployment and prefabricated systems further improves project timelines and cost control.

Cairo leads the market due to strong enterprise demand, telecom presence, and superior interconnection access. Alexandria and Port Said are emerging as edge and colocation zones, benefiting from proximity to cable landing points and port-based logistics. Inland regions like Assiut and Suez are witnessing smaller deployments backed by education, government, and mobile connectivity expansion. Regional diversification supports wider digital access and infrastructure resilience across the country.

Market Dynamics:

Market Drivers

Growing Digital Transformation Across Enterprises and Public Sector Entities Drives Infrastructure Expansion

The Egypt Data Center Infrastructure Market is witnessing strong demand from enterprise digitization and public sector modernization. National strategies like Egypt Vision 2030 support IT infrastructure upgrades across government agencies, healthcare, and education. Organizations deploy private and hybrid clouds to manage increasing data workloads. Local enterprises aim to reduce latency and improve data sovereignty. Public cloud demand continues rising from e-commerce, telecom, and digital banking sectors. Infrastructure suppliers invest in scalable platforms to serve future workloads. Cairo leads adoption, but regional cities follow with smaller deployments. The market creates long-term value for investors targeting scalable digital infrastructure.

- For instance, Egypt launched its largest Data and Cloud Computing Center (P1) in April 2024 on 23,500 square meters, involving over 1,200 engineers and 5,000 working hours, with the Ministry of Health as a key beneficiary for improved data tracking.

Increased Connectivity Through Submarine Cables and Telecom Backbone Modernization

Submarine cable routes through Egypt connect Africa, Europe, and Asia, making it a strategic interconnection point. The country hosts over 10 active subsea cables with new routes planned in the Red Sea corridor. Telecom operators upgrade national backbone infrastructure to boost capacity and reduce latency. These improvements attract hyperscale cloud providers and global CDNs to localize services. Growing internet usage, especially mobile-first consumption, pushes demand for low-latency infrastructure. Egypt’s central geography supports its role in multi-region routing. Global players view Egypt as a digital corridor for regional expansion. It helps build strong foundation for edge deployments and data sovereignty compliance.

Rising Demand for Scalable and Modular Data Center Designs for Fast Deployment

Modular and prefabricated data center solutions gain traction in Egypt due to faster installation times and better cost control. Operators adopt containerized or modular designs to support demand surges and phased growth. These units integrate power, cooling, and IT infrastructure into standardized modules. Local and regional players prefer them to reduce construction time in areas with fewer skilled contractors. Modular deployments suit edge and colocation operators expanding to regional cities. The Egypt Data Center Infrastructure Market embraces this shift to improve time-to-market and reduce operational risks. Government incentives for industrial zones enable faster land allocation for these modular builds.

Government Initiatives, Investment Incentives, and Free Zones Attract Global Infrastructure Players

Government policies incentivize data center investment through tax exemptions, duty waivers, and land allocation in economic zones. The Information Technology Industry Development Agency (ITIDA) supports private investments in data hosting and digital services. Egypt’s free zones policy enables 100% foreign ownership and repatriation of profits. Local partnerships with utility providers simplify power access for data centers. Global firms collaborate with Egyptian partners to navigate regulatory and utility-related processes. The Egypt Data Center Infrastructure Market benefits from these reforms that de-risk investments and fast-track deployment. Multinational players see Egypt as a scalable base for pan-African and Middle Eastern operations.

- For instance, the Digital Egypt initiative launched 20 innovation centers by end-2023, one per governorate, to foster technological leadership.

Market Trends

Increased Adoption of Renewable Energy Integration and Energy-Efficient Cooling Systems

Operators in the Egypt Data Center Infrastructure Market integrate solar PV and hybrid systems to reduce grid dependency. Rising power costs and carbon goals encourage green energy use across new data center builds. Solar integration is feasible due to high irradiance in industrial and desert zones. Infrastructure suppliers focus on high-efficiency UPS systems, variable speed drives, and liquid cooling. Liquid-to-air and immersion systems support rack density beyond 30 kW. AI-driven energy management platforms optimize cooling and load balancing. Green energy compliance boosts ESG ratings and attracts climate-focused capital. Sustainability becomes central to long-term infrastructure competitiveness.

Edge Data Centers and Regional Hosting Facilities Gain Momentum Across Secondary Cities

Edge deployment accelerates across Suez, Alexandria, and Assiut to support latency-sensitive services. These micro facilities host CDNs, IoT platforms, and local content applications. Telecom players lead edge expansion with micro-modular units near mobile base stations. Financial services and e-learning platforms seek localized data processing to meet regulatory and speed needs. The Egypt Data Center Infrastructure Market supports this with modular prefabricated designs and containerized edge platforms. These formats reduce installation time and CAPEX. Low-cost land and growing data demand in regional zones sustain the shift toward distributed infrastructure.

Data Localization Push and Compliance Regulations Encourage Local Storage Growth

Egypt enforces strict compliance standards under the Personal Data Protection Law. Enterprises must process sensitive customer data locally, driving demand for compliant hosting facilities. Government agencies require Egyptian residency for cloud platforms storing public data. International firms partner with local data center operators to comply with rules while maintaining service levels. The Egypt Data Center Infrastructure Market aligns infrastructure design to meet data classification, encryption, and audit trail standards. Operators invest in physical and logical security upgrades to attract sensitive workload hosting. This trend supports colocation and hybrid cloud growth from banking, healthcare, and government verticals.

Interconnection and Carrier-Neutral Ecosystem Growth Drives Cloud On-Ramps

Carrier-neutral facilities emerge across Cairo and new digital parks, offering direct cloud on-ramps and cross-connects. These interconnection hubs enable low-latency access to Microsoft Azure, AWS, and Google Cloud platforms. Enterprises seek to reduce data transfer costs and optimize hybrid cloud performance. Cloud adoption accelerates as firms digitize ERP, CRM, and analytics stacks. Data center operators differentiate through dense network fabrics and neutral interconnection policies. The Egypt Data Center Infrastructure Market evolves to meet these demands by expanding cross-connect options and peering exchanges. This trend strengthens Egypt’s position as a cloud interconnect node for North and East Africa.

Market Challenges

High Power Costs and Grid Reliability Concerns Increase Operational Uncertainty for Investors

Power availability remains a key constraint in the Egypt Data Center Infrastructure Market, particularly in regional cities. Operators face high utility tariffs, limiting cost competitiveness in large-scale builds. Despite improvements, outages still affect grid reliability in certain areas. Backup systems like diesel generators and battery storage raise CAPEX and operational complexity. Infrastructure design must account for redundancy, power factor correction, and distribution losses. The need for high-voltage substations and dedicated feeders adds delays to construction. Regulatory clarity on renewable power wheeling is limited. These risks impact investor confidence and delay entry timelines for hyperscale players.

Limited Local Talent Pool for Data Center Design, Engineering, and Operation Roles

Skilled workforce shortages pose a structural bottleneck for data center growth in Egypt. Talent gaps exist in electrical engineering, HVAC system design, and network architecture. Operators face difficulties recruiting data center-certified personnel and experienced project managers. Training programs lag behind international standards in power systems, cybersecurity, and data center operations. This gap results in reliance on expatriates or outsourced specialists, increasing costs. Enterprises delay buildout due to contractor quality issues or supervision gaps. The Egypt Data Center Infrastructure Market requires long-term investment in education and certifications. Partnerships with universities and vocational institutes are essential to close this gap.

Market Opportunities

Rising Cloud Adoption and Digital Service Growth Unlock New Hosting and Colocation Demand

Public cloud expansion by AWS, Microsoft, and Huawei fuels hosting demand across finance, telecom, and education. Egyptian enterprises adopt SaaS and PaaS platforms to modernize core systems. Startups and e-commerce platforms require scalable colocation and disaster recovery. The Egypt Data Center Infrastructure Market enables this shift through tiered facilities with on-demand scaling. Flexible rack pricing and carrier-neutral interconnects attract SMEs and fintech firms.

Regional Integration with African and Middle Eastern Digital Corridors Strengthens Strategic Value

Egypt’s location and connectivity create opportunities to become a regional digital hub. Initiatives linking Egypt to East Africa and the Gulf via fiber corridors improve market relevance. Government support for digital economy zones near ports and borders boosts infrastructure demand. It positions Egypt as a preferred hub for transcontinental digital routing and cloud services.

Market Segmentation

By Infrastructure Type

The Egypt Data Center Infrastructure Market is dominated by electrical and mechanical infrastructure segments. Electrical infrastructure accounts for the largest share due to critical role in ensuring uptime. Mechanical systems, particularly cooling units, follow closely as thermal efficiency becomes vital in Egypt’s climate. IT and network infrastructure are growing steadily, driven by demand for edge and hyperscale deployments. Civil and architectural components play a role in modular and prefabricated designs, with faster deployment cycles gaining interest.

By Electrical Infrastructure

Uninterruptible power supply (UPS) systems lead the segment, supported by widespread demand for power redundancy. Battery energy storage systems (BESS) gain traction due to grid reliability issues and renewable integration. Transfer switches and switchgears are essential to power switchover efficiency. Power distribution units (PDUs) are standard across all facility sizes. Utility grid connectivity remains a core area of investment in both urban and secondary cities. Egypt’s growing digital infrastructure requires scalable, high-efficiency electrical systems to support long-term load growth.

By Mechanical Infrastructure

Cooling units such as CRAC and CRAH dominate due to high ambient temperatures. Containment systems improve thermal management and energy efficiency. Chillers, especially air-cooled types, see adoption in hyperscale and colocation builds. Pumps and piping systems form core support infrastructure for liquid-cooled systems. Operators increasingly prefer modular cooling setups to manage diverse rack densities. This segment reflects Egypt’s climatic needs and power optimization strategies.

By Civil / Structural & Architectural

Modular and prefabricated systems lead this segment, enabling rapid deployment and cost control. Superstructures using steel or concrete frames dominate hyperscale builds. Site preparation, building envelopes, and raised floors are essential in all facilities. Egypt’s zoning rules and industrial park layouts influence foundation and structure choices. The market increasingly integrates prefabrication to reduce construction timelines and improve scalability.

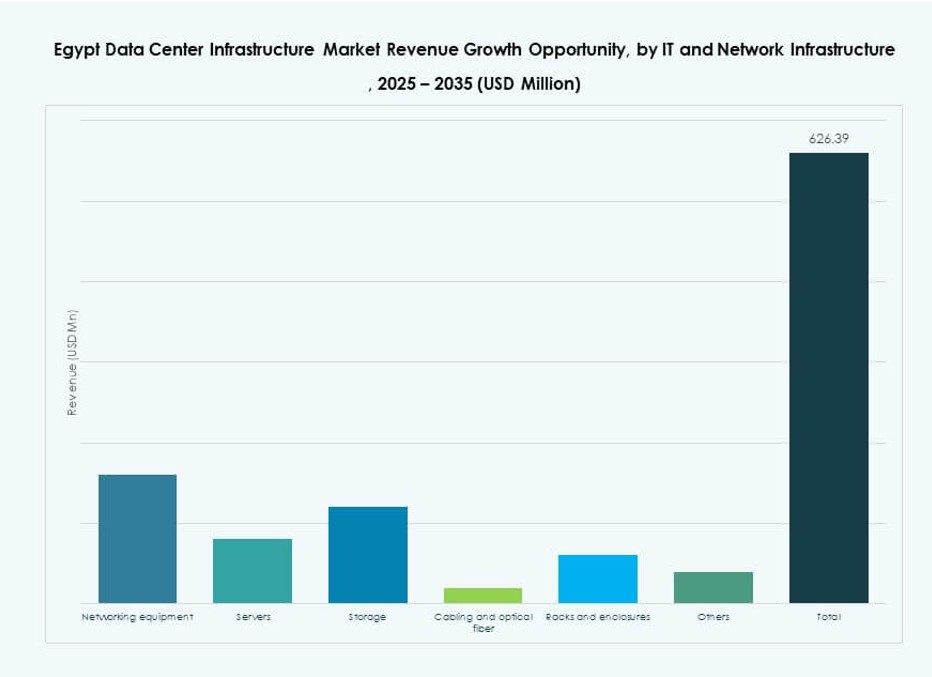

By IT & Network Infrastructure

Networking equipment and racks represent the largest share, followed by servers and storage. Optical fiber and structured cabling grow steadily due to cloud adoption and bandwidth needs. Enterprise and telecom players demand scalable, high-performance IT stacks. Equipment modularity and energy efficiency are key buying criteria. Egypt’s infrastructure builds align with global data center architecture trends.

By Data Center Type

Colocation data centers dominate in Egypt due to demand from SMEs, banks, and cloud platforms. Hyperscale builds are increasing, supported by global and regional players. Enterprise data centers are declining as firms shift to hosted or hybrid models. Edge data centers grow in secondary cities to serve local applications and content. The mix reflects Egypt’s maturing digital economy and cloud readiness.

By Delivery Model

Design-build/EPC leads, offering end-to-end solutions with speed and quality control. Turnkey and modular factory-built options gain popularity for edge and regional builds. Retrofit and upgrade models are used in older enterprise facilities. Construction management is common for large public-private partnerships. The market favors delivery models that reduce time to service.

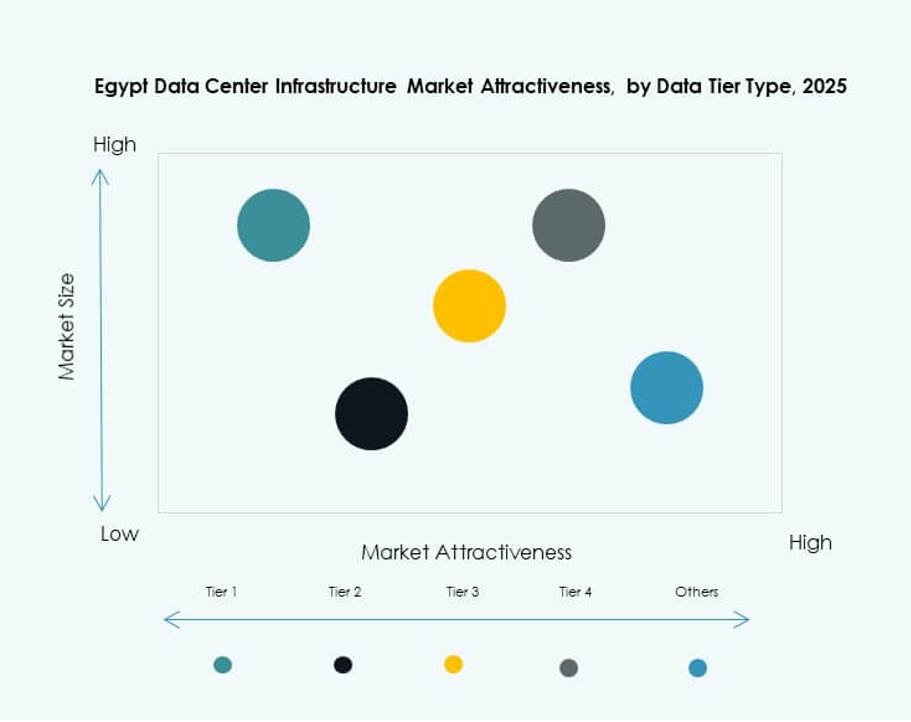

By Tier Type

Tier 3 data centers hold the largest market share, balancing cost and redundancy. Tier 4 is gaining adoption in financial and hyperscale segments requiring full fault tolerance. Tier 2 remains relevant for enterprise and regional edge setups. Tier 1 is used in limited applications with low uptime requirements. The tier mix aligns with Egypt’s evolving data sensitivity and availability expectations.

Regional Insights

Cairo Leads With 64% Share Due to Connectivity, Enterprise Demand, and Government Support

Cairo is the core hub in the Egypt Data Center Infrastructure Market, driven by dense population, enterprise presence, and superior connectivity. The city hosts most hyperscale, colocation, and government-backed data centers. Proximity to telecom backbones and subsea cables boosts capacity. Major universities, financial institutions, and ministries drive localized hosting. Cairo’s zoning regulations and infrastructure support large-scale facilities. It accounts for 64% of the total market due to its strategic significance.

- For instance, NEOIX’s hyperscale facility in the New Administrative Capital near Cairo offers 150MW initial capacity, expandable to 500MW, with desert cooling reducing energy use by 60%.

Alexandria and Port Said Hold 22% Market Share, Acting as Emerging Edge and Interconnection Zones

Alexandria and Port Said benefit from cable landing stations, proximity to Europe, and growing enterprise base. These cities see rising deployment of modular and edge data centers. Their ports also support industrial and logistics data requirements. Investors prefer these areas for regional distribution hubs and content delivery nodes. Port-based digital zones attract infrastructure investments with free zone benefits. Together, they represent 22% of Egypt’s infrastructure market.

- For instance, Telecom Egypt landed the SEA-ME-WE-6 subsea cable in Port Said, delivering 12.6 Tbps per fiber pair across 10 pairs for enhanced interconnection.

Other Regions Account for 14% Share, With Growth Driven by Education, Telecom, and Public Sector Demand

Assiut, Suez, and other inland cities are emerging locations for localized hosting. Telecom operators deploy containerized facilities for mobile services and IoT workloads. Government pushes for digitization in education, healthcare, and local governance drives regional demand. Power availability and land costs support future expansion in these zones. The Egypt Data Center Infrastructure Market sees steady growth outside major cities as digital services penetrate new demographics. These regions collectively hold a 14% share.

Competitive Insights:

- Telecom Egypt (TE Data)

- Elsewedy Data Centers

- Khazna Data Centers

- Gulf Data Hub

- G42 / Core42

- Huawei Technologies Co., Ltd.

- Schneider Electric

- Vertiv Group Corp.

- Cisco Systems, Inc.

- Hewlett Packard Enterprise

The Egypt Data Center Infrastructure Market features a competitive mix of local and global players. Telecom Egypt and Elsewedy Data Centers lead local infrastructure development with government support and national connectivity assets. Global firms like Schneider Electric, Huawei, and Vertiv offer power and cooling systems critical for Tier III and Tier IV builds. Gulf-based operators such as Khazna and G42 target Egypt for regional expansion due to its cable landing points and geographic reach. Technology vendors including Cisco, HPE, and Huawei supply networking, storage, and IT infrastructure. It supports growth through public-private partnerships, vendor alliances, and modular build strategies. Market competition focuses on energy efficiency, scalability, and interconnection density. Global players enter through joint ventures or local partnerships to meet compliance and deployment speed needs.

Recent Developments:

- In September 2025, Telecom Egypt (TE Data) received preliminary board approval for Helios Investment Partners to acquire a 75-80% stake in a subsidiary owning its Regional Data Hub (RDH) data center in Cairo, valued at around $177-260 million, with Telecom Egypt retaining 20-25%.

- In December 2024, Africa50 invested $15 million in Raya Data Center (RDC), a leading Egyptian provider, to support expansion of its Tier III data centers in Cairo amid growing demand in the digital economy.

- In September 2024, Orange Business completed the first phases of data center infrastructure for Grifols Egypt for Plasma Derivatives (GEPD) in Egypt’s New Administrative Capital, providing colocation services along with communications infrastructure.