Executive summary:

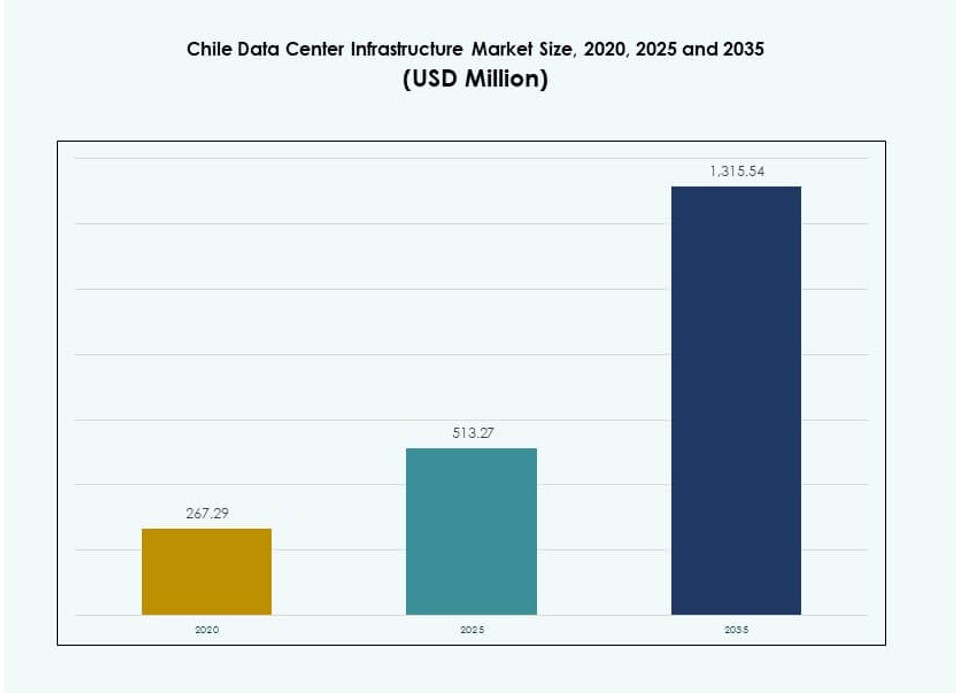

The Chile Data Center Infrastructure Market size was valued at USD 267.29 million in 2020 to USD 513.27 million in 2025 and is anticipated to reach USD 1,315.54 million by 2035, at a CAGR of 9.80% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2035 |

| Chile Data Center Infrastructure Market Size 2025 |

USD 513.27 Million |

| Chile Data Center Infrastructure Market, CAGR |

9.80% |

| Chile Data Center Infrastructure Market Size 2035 |

USD 1,315.54 Million |

The market is expanding due to rising cloud adoption, digital transformation, and demand for AI-ready infrastructure. Strategic partnerships and sustainable technologies are reshaping deployments, with a shift toward modular, energy-efficient, and high-density designs. Operators focus on liquid cooling, edge infrastructure, and green energy sourcing. Chile’s regulatory clarity, submarine cable connectivity, and renewable power supply make it attractive for hyperscale and colocation growth. This strengthens its value for investors targeting scalable and resilient digital infrastructure.

Santiago leads with most operational and planned facilities due to strong fiber infrastructure and enterprise presence. Northern regions are gaining momentum with renewable-powered edge deployments supporting mining and industrial sectors. Coastal zones like Valparaíso and Concepción are emerging as secondary hubs for redundancy, disaster recovery, and local interconnectivity. This regional diversification is building a distributed, low-latency infrastructure backbone across the country.

Market Dynamics:

Market Drivers

Expansion of Cloud Services and Digital Transformation Across Enterprise Workloads and Government Operations

The Chile Data Center Infrastructure Market is growing due to expanding digital services across public and private sectors. Enterprises are migrating legacy systems to cloud platforms, enhancing efficiency and cybersecurity. Government agencies are deploying e-governance tools, increasing the need for secure data hosting. Rising adoption of SaaS, IaaS, and hybrid cloud models is driving hyperscale developments. Domestic and regional firms are upgrading their IT capabilities to meet growing consumer expectations. Digital banking, telemedicine, and online education further raise data processing requirements. These shifts make Chile a critical market for investors targeting high-growth digital economies. It supports scalable infrastructure investments aligned with national digital agendas.

Surging Renewable Energy Integration with Data Center Power Architecture Across Grid-Connected Zones

Chile’s abundant renewable resources, especially solar and wind, have become a key market driver. Data center developers prefer green power sourcing to meet global ESG standards. Operators integrate photovoltaic panels, microgrids, and PPAs with local energy suppliers. Low carbon footprint attracts global hyperscale and colocation providers. Santiago and Northern Chile offer grid stability and renewable availability. Clean energy incentives lower operational costs and improve investor appeal. Chile Data Center Infrastructure Market supports long-term sustainability goals and positions itself as a future-ready hub. This energy shift also meets client demand for environmentally responsible data operations.

- For instance, Google’s Curie submarine cable became operational in 2020 with four fiber pairs and 72 Tbps capacity. It connects Los Angeles to Valparaíso, enhancing low-latency access to Google’s Quilicura data center in Chile.

Strategic Submarine Cable Connectivity Enhancing Regional Data Flows and Intercontinental Latency Performance

Chile’s access to international submarine cable networks strengthens its position as a digital gateway. Cables like the Curie system boost latency performance between South America and global internet hubs. Low-latency connectivity supports edge computing and high-frequency financial services. It enables global cloud providers to expand presence without regional performance compromises. The Chile Data Center Infrastructure Market benefits from reliable backhaul and peering points. Santiago becomes a magnet for low-latency content delivery and AI compute nodes. This strategic advantage improves data sovereignty, regulatory compliance, and cross-border digital trade. Investments flow into high-capacity fiber backbones and carrier-neutral facilities.

Increased Enterprise Demand for Edge, AI, and IoT Compute Power Across Urban and Industrial Corridors

Industrial automation and smart city programs drive demand for localized processing infrastructure. Enterprises need lower latency, reliable uptime, and secured connectivity. AI, video analytics, and sensor-based monitoring require robust compute resources near users. Data centers support latency-sensitive workloads across retail, energy, and logistics sectors. Chile Data Center Infrastructure Market aligns with national digital growth strategies and urban modernization plans. Santiago, Antofagasta, and Concepción see rising deployment of modular and edge data centers. This shift helps operators serve real-time applications without overloading hyperscale hubs. The market becomes essential for businesses adapting to intelligent infrastructure needs.

- For instance, AWS announced a $4 billion investment in Chile in 2025 for a hyperscale region operational by late 2026 supporting edge and AI workloads. AI, video analytics, and sensor-based monitoring require robust compute resources near users.

Market Trends

Growing Shift Toward Modular and Prefabricated Data Center Construction to Accelerate Deployment Timelines

Modular design is gaining traction for faster and scalable deployment across urban and remote locations. Vendors offer factory-built modules with integrated electrical and mechanical systems. It cuts construction time, ensures quality, and supports rapid rollout of edge capacity. Operators choose modular formats for pilot zones, emergency capacity, and temporary expansions. The Chile Data Center Infrastructure Market is witnessing higher demand for containerized and skid-based solutions. It suits earthquake-prone zones and reduces site risks. This trend helps meet demand surges from cloud, content, and enterprise sectors. Standardization and quick deployment are shaping future data infrastructure formats.

Rising Investments in Liquid Cooling Systems to Support AI and HPC Workloads Across Hyperscale Zones

High-performance computing workloads increase thermal load in data centers. Air-based cooling alone cannot meet the new thermal demands from AI and machine learning models. Liquid cooling systems offer better efficiency for dense server environments. Direct-to-chip and immersion technologies see strong pilot deployments. The Chile Data Center Infrastructure Market is evolving to support high-density workloads. Facilities targeting HPC and AI applications invest in scalable liquid cooling. It improves PUE and supports long-term energy savings. Operators deploy hybrid cooling to balance legacy integration and future readiness.

Increased Use of Software-Defined Power and Energy Management Platforms for Efficiency Optimization

Data center operators are integrating software-based tools to monitor and optimize energy usage. Platforms allow real-time power consumption tracking, capacity planning, and automated failover. AI-based tools help predict load trends and enhance uptime. The Chile Data Center Infrastructure Market embraces software-defined solutions for power and cooling optimization. It reduces energy waste and supports dynamic workload management. DCIM platforms gain traction among Tier III and Tier IV facilities. The trend improves visibility, sustainability, and cost control. Operators enhance operational efficiency without massive hardware overhauls.

Expansion of Multi-Tenant Data Center Ecosystems to Support Regional Cloud and Telecom Interconnectivity

Colocation and neutral-host models are growing in response to rising demand from telecom, fintech, and IT firms. Multi-tenant data centers enable shared access to power, network, and security. Tenants gain flexibility, scalability, and cost efficiency. The Chile Data Center Infrastructure Market supports regional data traffic consolidation. Interconnectivity hubs improve access to submarine cable landings and national backbones. Carrier-neutral designs allow clients to choose connectivity partners freely. Interconnection boosts value proposition of urban data centers in Santiago and Valparaíso. This trend supports ecosystem growth and service diversity.

Market Challenges

Infrastructure Vulnerability to Natural Disasters and Seismic Risks Across High-Intensity Earthquake Zones

Chile is located along the Pacific Ring of Fire, making it highly prone to seismic activity. Frequent earthquakes pose significant risks to structural stability and service uptime. Data centers require enhanced structural design and seismic isolation systems to maintain resilience. Cost of earthquake-proof construction raises initial investments for developers. Insurance premiums and compliance burdens add to financial constraints. Backup systems and redundancy layers must be designed for disaster scenarios. The Chile Data Center Infrastructure Market must overcome natural hazard risks to maintain investor confidence. Reliability and uptime become central concerns during site selection.

Limited Skilled Workforce Availability and High Training Costs for Data Center Operations

Managing high-density, mission-critical data centers requires skilled technicians and specialized certifications. Chile faces a talent shortage in fields such as cooling management, network configuration, and power systems. Lack of training institutions and local programs limits workforce availability. Operators invest in overseas training or import talent, raising HR costs. The Chile Data Center Infrastructure Market must close the skill gap to scale operations sustainably. Workforce limitations impact SLAs, uptime guarantees, and expansion timelines. High dependency on external consultants reduces operational autonomy.

Market Opportunities

Surging Foreign Direct Investment (FDI) from Cloud and Hyperscale Players Entering the Latin American Region

Global cloud leaders are investing in regional hubs to improve service availability and reduce latency. Chile attracts FDI due to renewable energy, submarine connectivity, and digital demand growth. Hyperscale firms seek land, power, and favorable regulation. The Chile Data Center Infrastructure Market enables entry into Andean and Pacific regions. Investor-friendly frameworks and government incentives support infrastructure localization.

Strong Potential for Edge Data Centers in Industrial Zones and Remote Mining Regions Across Northern Chile

Chile’s mining regions and industrial corridors generate high demand for localized data processing. Edge data centers enable real-time analytics, safety monitoring, and equipment automation. Regions like Antofagasta benefit from industrial digitization and IoT integration. The Chile Data Center Infrastructure Market supports compact edge builds with low-latency connectivity. Modular designs allow deployment in harsh and space-constrained environments.

Market Segmentation

By Infrastructure Type

The Chile Data Center Infrastructure Market is led by electrical infrastructure due to power-intensive workloads and hyperscale adoption. Mechanical and IT & network infrastructure segments follow closely, supported by rising cooling needs and server deployments. Civil and architectural components gain traction with seismic-resistant superstructures. Modular systems and prefabricated units improve scalability and reduce time to market. IT infrastructure remains crucial with growing demand for AI servers and enterprise storage.

By Electrical Infrastructure

Uninterruptible Power Supply (UPS) dominates this segment due to strict uptime needs across Tier III and Tier IV facilities. Power Distribution Units (PDUs) and grid connections are vital for stable delivery. Chile Data Center Infrastructure Market sees growth in Battery Energy Storage Systems (BESS) to support renewable integration. Transfer switches and switchgears offer fault tolerance and redundancy. Operators focus on smart power management to lower energy loss.

By Mechanical Infrastructure

Cooling units like CRAC/CRAH lead the mechanical segment due to their cost-effectiveness and reliability. Chillers, especially air-cooled ones, support high-density setups. Containment systems such as hot/cold aisles reduce energy use and increase efficiency. Chile Data Center Infrastructure Market prioritizes mechanical upgrades to meet thermal demands. Pumps and piping systems are customized for energy savings and water reuse.

By Civil / Structural & Architectural

Superstructures with steel frames dominate due to their flexibility and seismic resilience. Modular construction and raised floors are widely used to allow airflow and rapid deployment. The Chile Data Center Infrastructure Market includes architectural advancements in insulation and energy-efficient cladding. Site preparation remains critical for terrain-specific builds. Prefabricated solutions speed up delivery in urban zones.

By IT & Network Infrastructure

Servers and networking equipment represent the largest share due to workload expansion across cloud and enterprise. Storage and optical fiber upgrades follow, driven by high-throughput needs. Racks and enclosures adapt to liquid and high-density cooling setups. Chile Data Center Infrastructure Market aligns IT infrastructure with AI, analytics, and HPC trends. Cabling solutions ensure connectivity resilience and minimal signal loss.

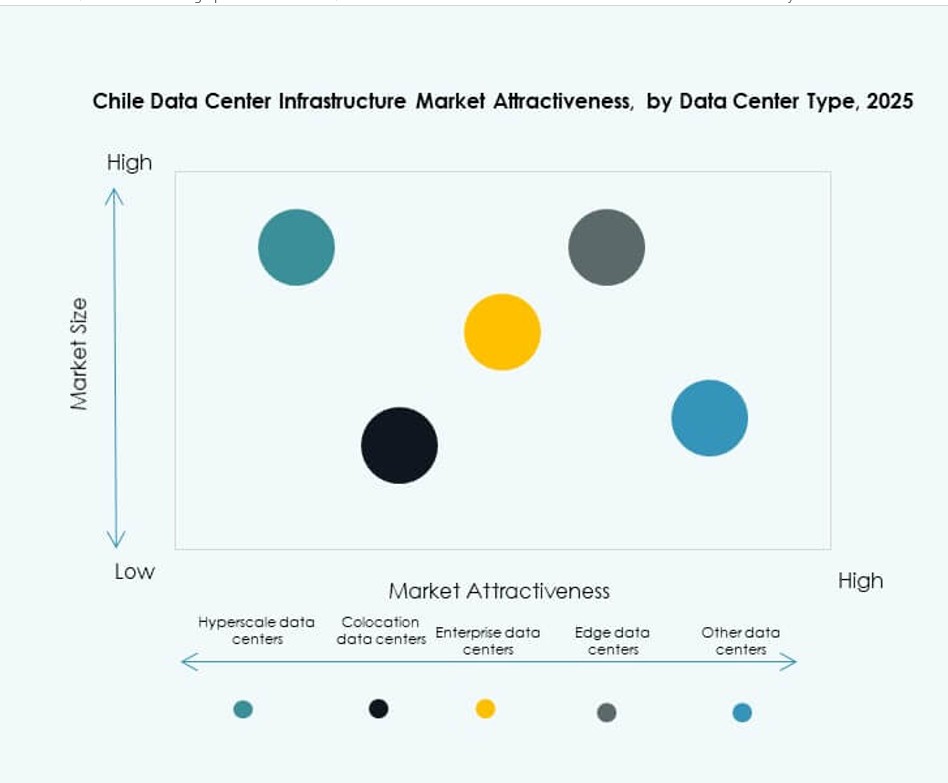

By Data Center Type

Colocation data centers dominate due to growing SME and telecom demand. Hyperscale centers are expanding with major global investments. Edge data centers emerge across mining and industrial areas. Chile Data Center Infrastructure Market supports enterprise and modular data centers as niche deployments. Operators mix models to suit urban and remote workloads.

By Delivery Model

Design-build/EPC and turnkey models lead due to their efficiency and reduced timeline. Modular factory-built units grow due to scalability. Retrofit/upgrade models support legacy site modernization. Chile Data Center Infrastructure Market includes custom construction and construction management services for specialized needs. Turnkey delivery ensures compliance and coordination.

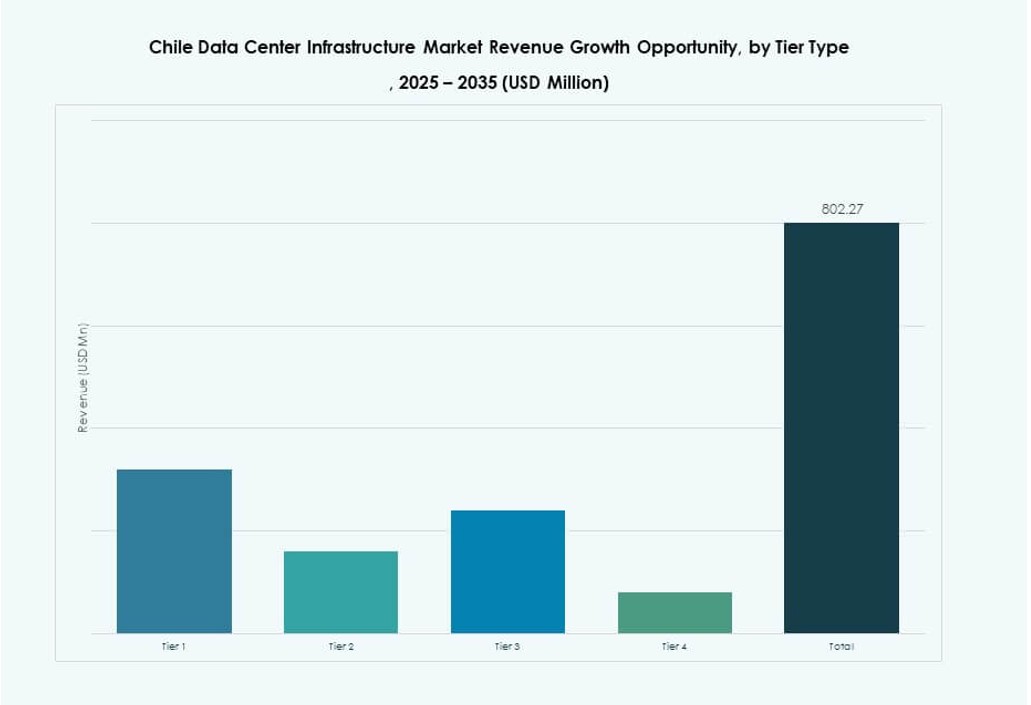

By Tier Type

Tier III holds the highest share for balancing uptime and cost. Tier IV gains share in mission-critical workloads like BFSI and healthcare. Chile Data Center Infrastructure Market sees Tier II for smaller enterprise setups. Tier I deployments are minimal due to limited redundancy. Tier III and IV growth align with regional cloud demand.

Regional Insights

Santiago Metropolitan Region Leads with Over 55% Market Share Due to Urban Demand and Infrastructure Readiness

Santiago dominates the Chile Data Center Infrastructure Market with its mature fiber network, energy availability, and strong enterprise base. The region hosts most colocation and cloud zones serving BFSI, government, and telecom clients. High urban data usage and digital transformation accelerate new builds. Global operators prefer Santiago for its workforce, land access, and grid reliability. Its leadership position continues with new hyperscale entries and carrier-neutral interconnects.

Northern Chile Holds Around 25% Market Share Driven by Industrial and Renewable Power Zones

Antofagasta and Atacama regions lead northern deployments due to mining industry digitization. Edge data centers support automation, safety, and real-time data handling. Renewable energy projects in these zones attract green data center builds. Chile Data Center Infrastructure Market sees modular, rugged facilities suited to remote industrial use. Submarine cable extension to the north improves regional connectivity.

- For instance, Acciona’s El Romero solar project in Atacama, at 247 MW-DC capacity, supplies 80 MW of power to Google’s Quilicura facility via Chile’s Central Grid since 2017.

Southern and Coastal Zones Account for 20% Market Share with Emerging Data Center Developments

Regions like Valparaíso, Concepción, and Biobío show rising data center interest. Valparaíso benefits from proximity to Santiago and port-based connectivity. Coastal zones support regional service redundancy and disaster recovery setups. Chile Data Center Infrastructure Market diversifies geographically to enhance service reach. Government digitalization and SME tech adoption spur regional demand.

- For instance, Ascenty operates a data center campus in Quilicura’s Santiago Metropolitan area with carrier-neutral connectivity supporting regional redundancy.

Competitive Insights:

- ABB

- Vertiv Group Corp.

- Schneider Electric

- Equinix, Inc.

- Scala Data Centers

- Ascenty

- MDC Data Centers

- Cisco Systems, Inc.

- Dell Inc.

- Oracle

The Chile Data Center Infrastructure Market features strong competition among global and regional players. It includes power and cooling system providers like ABB, Vertiv, and Schneider Electric, which lead due to their reliability and local service presence. Global colocation operators such as Equinix, Scala, and Ascenty continue expanding their footprint with hyperscale-ready facilities. Network and IT infrastructure vendors, including Cisco, Dell, and Oracle, maintain demand through strategic partnerships with data center developers. The market sees rising mergers and modular deployment initiatives, particularly in urban hubs like Santiago. It supports multi-tenant models and modular builds, attracting hyperscale and cloud service providers. Players differentiate by offering energy-efficient solutions, seismic-resilient designs, and rapid deployment models. Competition also intensifies in edge and regional zones as demand grows from industrial sectors.

Recent Developments:

- In October 2025, Vertiv Group Corp. established a strategic partnership with Grupo Datco to expand high-performance data center infrastructure across Chile and Argentina, focusing on AI and HPC demands.

- In June 2025, TECfusions partnered with Baeza Group to develop a 100MW AI-ready data center campus on 40 acres in Puente Alto, Chile. The project, announced on June 2, will launch with 10MW initial capacity and expand using zero-water cooling to address local scarcity issues.

- In June 2025, Microsoft launched its Chile Central sovereign data center region in the Santiago metropolitan area, featuring three independent sites for Azure, Microsoft 365, Dynamics 365, and Power Platform services.

- In December 10, 2024, Ascenty submitted an environmental review for a new data center in Chile, with construction set to begin in September 2025 and operations expected after 18 months.