Executive summary:

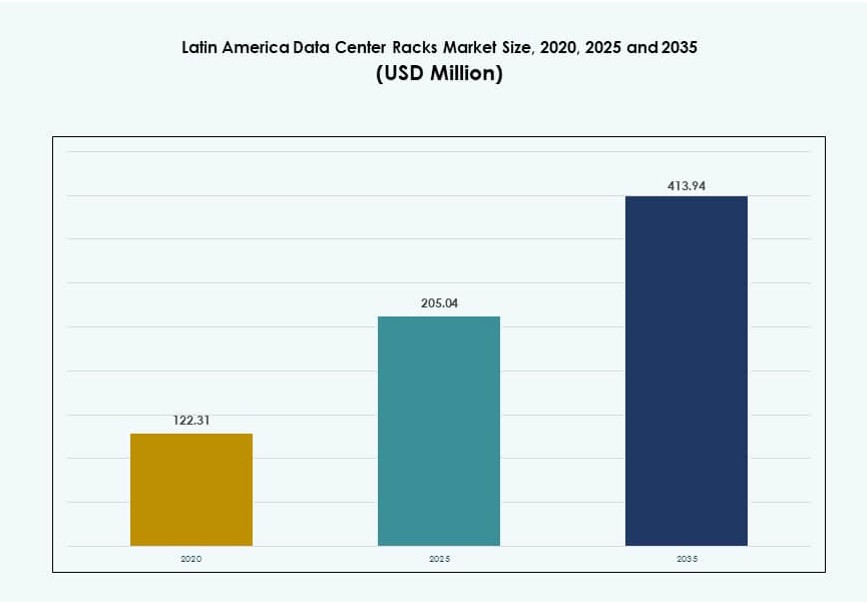

The Latin America Data Center Racks Market size was valued at USD 122.31 million in 2020 to USD 205.04 million in 2025 and is anticipated to reach USD 413.94 million by 2035, at a CAGR of 7.24% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2035 |

| Latin America Data Center Racks Market Size 2025 |

USD 205.04 Million |

| Latin America Data Center Racks Market, CAGR |

7.24% |

| Latin America Data Center Racks Market Size 2035 |

USD 413.94 Million |

The Latin America Data Center Racks Market is driven by cloud adoption, AI workloads, and enterprise digitization. Operators deploy higher-density racks to support compute-intensive applications. Modular and prefabricated rack systems gain preference for faster deployment. Liquid-cooling-ready racks support thermal efficiency needs. Telecom expansion and edge computing adoption raise rack demand in distributed locations. Innovation in smart racks improves monitoring and uptime. Businesses view the market as strategic for scaling digital services. Investors focus on infrastructure resilience and long-term capacity growth.

Brazil leads the region due to mature colocation ecosystems and strong hyperscale presence. Mexico follows with rapid expansion driven by cloud regions and proximity to North America. Chile and Colombia emerge as key markets supported by stable regulations and connectivity investments. Argentina and Peru show steady growth through enterprise and government demand. The Latin America Data Center Racks Market benefits from diversified regional growth patterns. Urban hubs attract large facilities, while tier-two cities drive edge deployments. Regional balance supports sustained market expansion.

Market Dynamics:

Market Drivers

Expansion of Hyperscale and Cloud Data Centers Across Major Latin American Countries

Hyperscale cloud providers are investing in new availability zones across Brazil, Chile, and Mexico. These deployments demand scalable, high-density rack infrastructure to support AI, analytics, and cloud workloads. The Latin America Data Center Racks Market is directly benefitting from this trend as operators expand and retrofit their facilities. Cloud demand from banks, fintech, and public institutions accelerates rack investments. High rack density and liquid-cooling compatibility are becoming essential. Brazil remains the largest hub, with other countries showing rising activity. The need to scale quickly in underserved cities pushes modular and pre-integrated rack designs. Enterprises and colocation operators prefer flexible rack architectures to manage growing power loads. Racks have become strategic assets in optimizing space, efficiency, and compute performance.

Rapid Adoption of Edge Computing Driving Smaller Rack Deployments Across Tier-2 Cities

Edge computing in Latin America is reshaping how data centers use and configure racks. Telcos and ISPs deploy localized micro data centers with compact rack footprints. The push for low-latency services fuels distributed infrastructure in healthcare, retail, and logistics. The Latin America Data Center Racks Market sees rising demand for shorter racks and smart enclosures. Energy-efficient edge rack formats support real-time analytics and IoT platforms. Rack infrastructure at the edge needs integrated cable management and airflow control. Customers demand reduced installation times and high serviceability. Smart city programs and 5G rollouts strengthen edge infrastructure needs. Rack vendors that support scalable edge formats gain a competitive edge.

- For instance, ODATA added its fourth hyperscale data center, QR04, near San Miguel de Allende, Mexico in 2025. The facility was designed with up to 24 MW of IT capacity and supports high rack power densities using advanced cooling systems.

Technology Convergence Pushing Demand for Intelligent and High-Density Rack Solutions

Artificial intelligence, big data, and HPC workloads require rack systems with advanced thermal handling. The Latin America Data Center Racks Market now favors racks that support 30–50 kW loads and beyond. Liquid-cooled racks, hot/cold aisle containment, and integrated monitoring sensors are now standard in high-growth facilities. Governments and businesses use digital twins to optimize rack performance before deployment. AI-driven workload orchestration increases rack utilization rates. Smart racks with onboard telemetry reduce downtime and improve service life. Infrastructure-as-code adoption improves rack provisioning efficiency across hybrid environments. Rack architecture plays a pivotal role in controlling operational costs and maximizing IT asset density. IT departments prioritize flexible rack systems that accommodate GPU clusters and storage nodes.

- For instance, Elea Data Centers announced its Rio AI City project in 2025, partnering with Oracle and the Rio de Janeiro city government. The site is planned to deliver up to 1.5 GW of IT load in its initial phase to support AI and cloud infrastructure.

Strategic Infrastructure Investments Supporting Regional Digitalization and Rack Capacity Growth

Digital transformation policies across Latin America stimulate public-private investment in digital infrastructure. Governments are establishing tech parks and sovereign cloud frameworks. The Latin America Data Center Racks Market is growing as rack procurement scales alongside greenfield and brownfield data center projects. Investors focus on Tier III+ and Tier IV readiness, increasing demand for high-availability rack configurations. National telecom operators modernize core and edge sites, boosting rack count. New submarine cables increase data traffic and require hyperscale nodes. Rack manufacturers partner with EPC firms to deliver pre-configured racks for faster integration. Racks are now viewed as a long-term strategic enabler of the region’s digital economy and data sovereignty efforts.

Market Trends

Widespread Use of Pre-Assembled, Modular, And Prefabricated Rack Systems to Speed Deployment

Operators across Latin America increasingly adopt prefabricated rack systems to reduce setup time. These plug-and-play units streamline deployments in both hyperscale and colocation environments. The Latin America Data Center Racks Market sees strong interest in factory-integrated racks with PDUs, containment, and cable management built in. Pre-assembled racks also reduce on-site labor costs. Rack modularity improves scalability, which suits operators expanding in phases. Smart monitoring tools embedded in prefabricated systems enhance asset visibility. These racks meet performance and compliance standards with minimal field adjustment. Telecom providers deploying regional edge nodes prefer this approach. The need for rapid time-to-market supports widespread adoption of prefabricated rack solutions.

Integration of DCIM Tools and Rack-Level Intelligence For Operational Optimization

Operators embed sensors, cameras, and telemetry modules into racks to enable granular monitoring. The Latin America Data Center Racks Market is shifting toward intelligent racks that feed real-time data into DCIM systems. Operators gain visibility into temperature, humidity, airflow, and energy metrics at the rack level. AI-based DCIM software helps optimize workload distribution and reduce energy waste. Predictive maintenance extends rack life and reduces downtime. Advanced racks offer digital twin compatibility for simulation and lifecycle planning. This data-centric approach enhances capacity planning and SLA management. Facility teams improve uptime and performance by managing racks through centralized dashboards. Rack intelligence supports better ROI for capital investments.

Growing Adoption of Liquid-Cooling Ready Racks for High-Performance Workloads

High-performance computing and AI workloads require more cooling than legacy rack designs can support. The Latin America Data Center Racks Market increasingly incorporates racks compatible with liquid-based cooling systems. These include direct-to-chip, immersion, and rear-door heat exchangers. Operators deploying 30–60 kW loads per rack favor these systems for thermal control. Liquid-ready racks reduce energy use and improve PUE. Cloud and government AI programs drive this requirement across hyperscale and research data centers. Cooling infrastructure aligns with rack-level architecture during design phases. Rack vendors now offer pre-engineered models that integrate with facility cooling plans. This trend supports sustainable and performance-focused growth in the region.

Surging Demand for Customizable Rack Designs to Accommodate Diverse Workloads

Latin American operators need rack solutions tailored to diverse application environments. The Latin America Data Center Racks Market sees demand for customized widths, heights, and power configurations. Workload diversity from BFSI, healthcare, and telecom drives this trend. Some facilities require shallow-depth racks for constrained spaces, while others need wide racks for high cable density. Custom rack offerings allow facilities to optimize airflow and weight distribution. Users prefer modularity to reconfigure racks across IT refresh cycles. Racks that adapt to GPUs, NVMe drives, and HPC gear are in high demand. Rack OEMs offer customization services to meet strict space, compliance, and cooling requirements. Flexibility in design gives operators long-term deployment value.

Market Challenges

Inconsistent Infrastructure and Regulatory Barriers Limit Rack Deployment Efficiency Across Regions

Infrastructure quality varies significantly across Latin America, slowing large-scale data center expansion. Power grid reliability and limited fiber access affect rack deployment in tier-2 and tier-3 markets. The Latin America Data Center Racks Market faces delays where permits, zoning laws, or customs clearance add friction. Operators struggle with regional code compliance and sourcing rack components across borders. In many countries, rack manufacturers depend on imports, exposing them to currency risks and longer lead times. Rack vendors must navigate fragmented procurement processes and public-sector delays. Standardizing rack specifications across multiple regions remains difficult. These barriers raise integration costs and delay modernization plans for regional operators.

Skilled Workforce Shortage and Low Awareness of Advanced Rack Systems Impact Market Maturity

Data center talent shortages across Latin America impact rack installation and support capabilities. Operators report difficulty in finding technicians skilled in high-density and liquid-cooling rack systems. The Latin America Data Center Racks Market struggles to scale rapidly in areas lacking technical training programs. Local integrators may not meet hyperscaler deployment standards. Knowledge gaps in airflow management and containment design lead to inefficiencies. Without skilled staff, facilities underutilize smart rack features. Vendor support teams often travel across borders, adding delays and cost. Workforce development is key to unlocking advanced rack infrastructure across the region.

Market Opportunities

Expansion of Edge and Modular Data Centers Unlocking New Rack Demand Across Underserved Areas

New edge deployments across tier-2 cities open growth areas for rack vendors. The Latin America Data Center Racks Market benefits from modular deployments needing pre-integrated racks. Sectors like retail, telecom, and smart cities create localized demand. These installations prioritize compact, intelligent, and scalable rack designs. Operators invest in secure racks with built-in monitoring. Rack OEMs with modular product lines can penetrate untapped markets. Shorter lead times and serviceability improve vendor success.

Cloud, AI, And HPC Investments Driving Demand for Specialized High-Capacity Rack Systems

Investments in AI infrastructure increase rack density requirements across major markets. The Latin America Data Center Racks Market supports AI labs and HPC nodes with advanced cooling needs. Liquid-cooling-compatible racks offer strong opportunity. Government digital initiatives and AI research funding support new installations. Rack OEMs offering customization and thermal optimization gain traction. Enterprises prefer integrated rack solutions to reduce deployment friction. Vendors can win through partnerships with cloud and academic sectors.

Market Segmentation

By Rack Type

Cabinet racks dominate the Latin America Data Center Racks Market due to their secure, enclosed structure and compatibility with containment systems. These are preferred in hyperscale and colocation deployments for airflow management and cable organization. Open frame racks hold a smaller share, mostly used in edge or non-critical facilities. Cabinet racks continue to grow with rising density and remote monitoring requirements. The “Others” category, including wall-mount and hybrid racks, sees limited use but gains interest in edge environments.

By Rack Height

42U racks lead the market, offering a balance between capacity, airflow, and serviceability. They serve as the industry standard in hyperscale and enterprise facilities across Latin America. Above 42U racks are gaining adoption for high-density AI and storage workloads. These tall racks maximize vertical space in facilities with high ceilings. Below 42U racks remain common in modular or edge data centers where space is constrained. The demand mix is shifting as compute loads increase, driving taller rack adoption.

By Width

19-inch racks hold the largest market share, serving as the default width for IT equipment across most facilities. They support a wide range of devices and align with global standards. 23-inch racks find adoption in specific telecom and industrial environments requiring more cable space. The “Others” category, including wider or custom-width racks, remains niche but is growing in use cases like HPC and dense GPU deployments. The Latin America Data Center Racks Market continues to standardize around 19-inch formats.

By Application

Server racks lead application-wise, driven by strong demand for compute infrastructure across industries. Enterprises and hyperscalers prioritize robust server rack configurations with power and cooling optimization. Network racks play a secondary but vital role, particularly in colocation and telco environments. Their design emphasizes structured cabling and airflow management. Server racks see higher refresh rates due to changing processor needs, which supports continued growth. Customization for mixed-use is increasing in newer deployments.

By End-user

Large data centers account for the dominant share, driven by hyperscale and colocation projects. These facilities require scalable, high-capacity racks for large IT loads. Small and mid-sized data centers also contribute, particularly through edge deployments and local enterprise needs. The Latin America Data Center Racks Market benefits from increased investments in both segments. Modular rack systems cater to SMBs requiring flexibility. Demand diversity across end-user tiers supports a balanced growth outlook.

By Vertical

IT and telecom is the leading vertical, accounting for the highest rack demand due to cloud, internet, and 5G infrastructure growth. BFSI follows, needing secure and compliant rack configurations for financial data. Healthcare racks must support high availability and privacy controls. Government and defense verticals deploy racks for national data programs. Energy, retail, and others contribute to market depth through regional edge use cases. The Latin America Data Center Racks Market reflects vertical diversity in rack requirements and growth.

Regional Insights

Brazil Leads with Over 38% Share Due to Hyperscale Expansion, Fiber Connectivity, And Regulatory Maturity

Brazil is the largest contributor to the Latin America Data Center Racks Market, accounting for over 38% of total revenue. Hyperscale cloud zones, submarine cable landings, and data localization policies drive rack deployments. São Paulo, Rio de Janeiro, and Campinas are key data center hubs. The country’s mature colocation market attracts international and regional players. Rack density and innovation adoption are highest in Brazil. Operators deploy liquid-cooling-ready racks for AI and enterprise workloads. Government support for digital transformation adds further strength to infrastructure growth.

- For instance, TIP Brasil launched its Tier III-certified DC3 facility in Campinas in November 2025, with capacity for up to 2,000 racks. The site supports colocation and cloud services, marking a major infrastructure expansion in Brazil.

Mexico, Chile, And Colombia Hold a Combined 34% Share Led by Cloud, Edge, And Energy Programs

Mexico accounts for around 15% of the market, driven by proximity to the U.S., growing hyperscale campuses, and telco-led edge rollouts. Querétaro and Monterrey emerge as high-growth zones. Chile contributes 11%, supported by green energy and data privacy regulations attracting hyperscale builds. Colombia represents roughly 8%, expanding with cloud adoption and smart city programs. These countries push for modular rack formats that support fast deployment. The Latin America Data Center Racks Market gains resilience from regional diversification and multi-country investments.

- For instance, KIO Networks expanded its presence in Querétaro with the launch of its QRO2 data center in 2025, reinforcing the region as a high-density digital hub. The new facility adds to an estimated 19 MW combined IT load capacity across the QRO campus.

Argentina, Peru, And Others Contribute 28% Through Local Enterprises, Modular Sites, And Public Sector Demand

Argentina, Peru, Ecuador, and Central American countries collectively contribute 28% of the market. Rack demand in these regions comes from national enterprise growth, public-sector digitalization, and retail-led edge infrastructure. Smaller colocation and modular facilities dominate deployments. Smart rack systems and short-height designs see increasing adoption. The Latin America Data Center Racks Market in these areas benefits from policy support and regional capacity gaps. Growth remains steady, with OEMs targeting underserved zones for new rack product penetration.

Competitive Insights:

- Vertiv Group

- Schneider Electric

- Rittal

- Eaton

- Legrand

- Furukawa Electric LatAm

- Panduit Corp.

- Belden Inc.

- Dell Inc.

- Cisco Systems, Inc.

The Latin America Data Center Racks Market features a mix of global infrastructure giants and regional manufacturers offering tailored solutions for hyperscale and edge facilities. Vertiv, Schneider Electric, and Rittal dominate due to their integrated rack ecosystems, advanced cooling compatibility, and strong service networks. Local providers like Furukawa Electric LatAm and Ecentrix Cabinets meet demand in country-specific projects, offering cost-efficient and customizable formats. Vendors compete on modularity, density support, and deployment speed. Liquid-cooling-ready racks and smart telemetry integration are key differentiators. Companies targeting telecom and government sectors gain ground through compliance-ready and prefabricated rack offerings. The market remains moderately consolidated, with alliances, M&A, and OEM expansions shaping vendor strategies. It favors players that offer pre-engineered, energy-efficient, and AI-compatible rack solutions.

Recent Developments:

- In October 2025, Vertiv partnered with Grupo Datco to broaden access to critical infrastructure solutions in Argentina and Chile. The collaboration aims to improve local support for high-density rack infrastructure and advanced data center applications. This alliance boosts Vertiv’s regional distribution and service capabilities, enabling faster deployment of rack systems for AI workloads and cloud expansion.

- In August 2025, Vertiv announced it would acquire Great Lakes Data Racks & Cabinets for roughly USD 200 million, strengthening its rack solutions portfolio across critical infrastructure. This move expands Vertiv’s capability in custom rack enclosures, seismic cabinets, and integrated cable management systems.

- In August 2025, ODATA launched its QR04 data center near San Miguel de Allende, Mexico, its fourth hyperscale facility in the country. The new site supports substantial cloud and AI demand, driving equipment and rack infrastructure uptake across the region.