Executive summary:

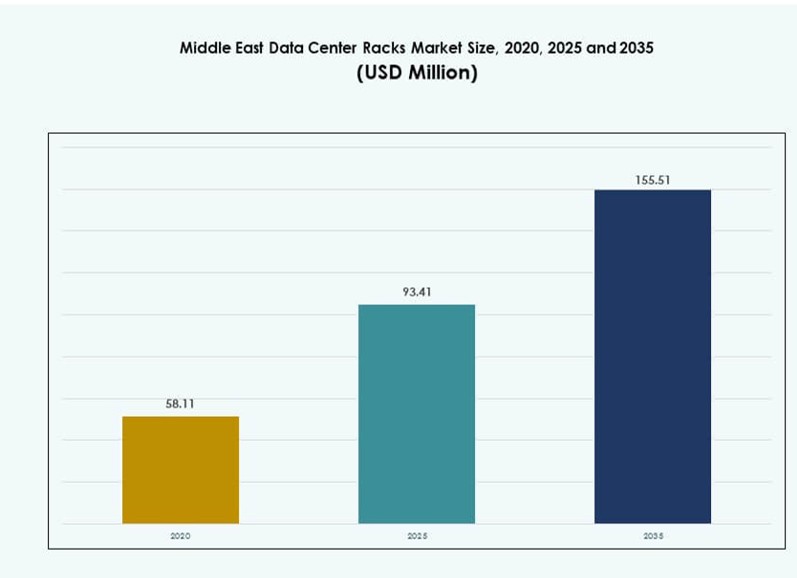

The Middle East Data Center Racks Market size was valued at USD 58.11 million in 2020 to USD 93.41 million in 2025 and is anticipated to reach USD 155.51 million by 2035, at a CAGR of 5.10% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2035 |

| Middle EastData Center Racks Market Size 2025 |

USD 93.41 Million |

| Middle EastData Center Racks Market, CAGR |

5.10% |

| Middle EastData Center Racks Market Size 2035 |

USD 155.51 Million |

Rising demand for AI infrastructure, data localization mandates, and growing hyperscale investments are accelerating rack deployments across the region. Operators are adopting modular, liquid-cooling-ready rack systems to support high-density workloads. Enterprises require scalable configurations to meet performance and sustainability targets. Smart rack solutions integrated with sensors and remote management tools are gaining traction. Strategic investments from global hyperscalers and local governments strengthen market stability. This market plays a vital role in enabling digital growth, secure cloud infrastructure, and long-term technology resilience. Investors benefit from growing demand across BFSI, telecom, and government verticals.

The UAE and Saudi Arabia lead the region due to aggressive cloud adoption, AI innovation, and national digital strategies. Israel shows strong growth driven by HPC and tech-driven enterprise demand. Countries like Qatar, Bahrain, and Kuwait are emerging markets investing in edge zones and sovereign infrastructure. These nations are focusing on localized data centers to meet compliance and latency goals. Regional rack demand is shaped by climate considerations, scalability, and power density needs. Strategic deployments in major cities strengthen the infrastructure backbone. The market is evolving with diverse rack configurations tailored for enterprise, government, and hyperscale facilities.

Market Dynamics:

Market Drivers

Rising Hyperscale Investments and National Digital Agendas Drive Rack Infrastructure Demand

The Middle East Data Center Racks Market benefits from large-scale digital transformation across the UAE, Saudi Arabia, and Israel. National programs like Saudi Vision 2030 and UAE Digital Government Strategy are accelerating the deployment of cloud zones and hyperscale campuses. These initiatives require robust infrastructure that supports high-density compute, driving rack demand. Government support for AI innovation has also pushed data center operators to upgrade rack configurations. The introduction of liquid-cooling-ready rack systems enables support for GPU-intensive workloads. Regulatory frameworks mandating data localization have increased colocation expansion across financial and healthcare verticals. Enterprises and public sector agencies seek customized rack layouts to meet security and uptime needs. The market plays a strategic role in enabling sovereign data infrastructure for digital economies. Investors gain stable returns from long-term rack and infrastructure deployments aligned with national priorities.

- For instance, AWS committed USD 5.3 billion in 2024 to launch its cloud region in Saudi Arabia, deploying hyperscale racks in Riyadh that comply with NCA cybersecurity and data residency regulations.

Adoption of AI, Edge, and High-Density Computing Catalyzes Rack Modernization Across Facilities

AI adoption across sectors such as fintech, logistics, and oil and gas has pushed demand for high-density rack configurations. Enterprises are shifting to 42U and above-42U rack heights to accommodate compute-intensive workloads. Modular rack systems with integrated power distribution and airflow containment are gaining preference in Tier III and Tier IV facilities. The Middle East Data Center Racks Market is evolving with demand for racks that support liquid-cooling components, direct-to-chip designs, and RDHx configurations. New rack standards are supporting both legacy and modern server architectures across cloud and enterprise domains. Operators deploy AI-specific racks with dedicated GPU trays and cable management enhancements. Rack solutions now include built-in monitoring and sensor-based temperature tracking to support real-time optimization. These shifts make the market essential for enabling innovation-led IT ecosystems in the region. Global vendors partner with local players to co-develop high-performance, locally compliant rack units.

- For instance, NVIDIA and Saudi Arabia’s HumaiN agreed in May 2025 to build 500 MW AI factories using 18,000 GB300 systems, requiring rack systems with over 50 kW densities and integrated direct-to-chip liquid cooling solutions.

Surging Enterprise Cloud Migration and Colocation Growth Elevate Rack Configuration Complexity

Enterprises are rapidly moving toward hybrid and multicloud environments, increasing complexity in rack planning and layout design. This has triggered demand for customizable cabinet racks and scalable open-frame systems. Colocation providers in Dubai, Riyadh, and Tel Aviv are expanding rack space to meet growing data workloads. The Middle East Data Center Racks Market supports IT infrastructure buildouts for high-performance compute clusters, storage nodes, and edge equipment. Operators focus on modular rack systems that enable easier upgrades and improved thermal efficiency. Rack height and width preferences vary by application, requiring flexible designs. Global cloud providers deploy hyperscale racks with advanced airflow designs and integrated cable trays. The market enables cost optimization and power usage efficiency improvements in large-scale deployments. It acts as a foundational layer for cloud-native enterprise operations across multiple sectors.

Data Sovereignty Regulations and Sustainability Goals Reshape Rack Procurement Strategies

Governments in the region enforce strict data residency requirements, which compel localized infrastructure investments. This has increased demand for regionally sourced and pre-certified rack units compatible with national data regulations. The Middle East Data Center Racks Market supports compliance by offering vendor-neutral designs that integrate with local hardware. Sustainability targets have driven innovation in rack energy efficiency, material use, and cooling support. Operators select rack systems with improved airflow management to support lower PUE metrics. Rack layouts are optimized for minimal floor space while maximizing compute capacity. Energy-conscious rack procurement is becoming a key part of green data center design. Local manufacturers are emerging to support rack customization aligned with regional use cases. These dynamics position the market as a strategic enabler of compliant and sustainable data infrastructure.

Market Trends

Integration of Liquid-Cooling and High-Power Racks Gains Ground in Next-Gen Facilities

Rack systems are increasingly optimized for liquid-cooling to handle high-thermal AI and HPC workloads. Operators adopt direct-to-chip and rear-door heat exchanger-supported racks to improve thermal performance. This trend is pronounced in hyperscale campuses deploying racks above 30 kW power density. The Middle East Data Center Racks Market reflects growing interest in prefabricated and customizable liquid-ready racks. Cloud providers target racks that support GPU-dense deployments for AI training models. Rack systems also include hot-swappable trays and reinforced structural designs for enhanced safety. Thermal simulation and CFD tools are used to plan rack integration across zones. Vendors compete by launching modular liquid-ready racks compatible with different form factors. The trend supports long-term scalability in dense compute environments.

Edge Rack Deployments Rise with Smart Cities and 5G Rollouts Across Tier-2 Markets

Growing smart city deployments and 5G infrastructure expansion in the Middle East are fueling demand for edge data centers. These facilities require compact, resilient, and prefabricated rack systems tailored for constrained environments. The Middle East Data Center Racks Market supports this with 19-inch and 23-inch rack formats optimized for edge compute. Governments in Bahrain, Oman, and Jordan are developing digital corridors that use localized edge nodes. Rack providers focus on mobility, integrated cooling modules, and high-speed cable management. Security integration with biometric and remote access modules is becoming standard. Small and mid-sized data centers deploy network racks for telco-grade performance in low-latency zones. Edge racks help offload hyperscale demand while bringing compute closer to users. These trends make edge racks a critical layer in regional IT transformation.

Standardization and Interoperability Become Priorities for Future-Proof Rack Procurement

Operators increasingly prioritize interoperable rack systems that support multi-vendor equipment and scalable deployment. Standards such as OCP (Open Compute Project) and ODCC influence rack designs in the region. The Middle East Data Center Racks Market benefits from this shift, with vendors offering rack solutions aligned with international guidelines. Interoperability reduces integration complexity across storage, compute, and networking components. Facilities in Riyadh and Dubai adopt standardized rack frames to enable plug-and-play module additions. Open rack designs also improve airflow and energy efficiency, reducing lifecycle costs. Large data centers procure standardized racks to reduce procurement lead time and downtime risk. Standardized racks help achieve rapid deployment timelines in dynamic infrastructure environments. This trend boosts modularity and flexibility across verticals.

AI-Driven Rack Monitoring and Digital Twin Integration Transform Infrastructure Management

Facility operators are adopting AI-powered rack monitoring systems to improve operational control. These systems offer real-time visibility into temperature, airflow, and power usage at the rack level. In the Middle East Data Center Racks Market, AI tools help optimize workload placement and thermal balancing across aisles. Digital twin platforms enable simulation of rack behavior before physical deployment. This enhances planning accuracy and reduces overprovisioning risks. Smart racks with integrated sensors support predictive maintenance and remote diagnostics. AI tools also help in identifying power anomalies and potential failure zones. Rack vendors integrate these technologies to deliver higher value in enterprise and hyperscale projects. These capabilities enhance lifecycle performance and support cost savings in operations.

Market Challenges

High Customization Needs and Complex Procurement Cycles Hinder Deployment Timelines

The Middle East Data Center Racks Market faces challenges in addressing diverse customization needs across industries and regions. Rack specifications differ by application, rack height, and cooling type, which complicates procurement. Operators often face delays in sourcing specialized cabinet racks with integrated containment or non-standard widths. Lack of regional manufacturing creates dependency on imports, which impacts lead times and costs. Facilities handling AI workloads require racks with specific airflow paths, cable trays, and liquid-cooling compatibility. Procurement teams must validate structural integrity, compliance, and interoperability, adding to deployment complexity. These factors extend the integration timeline and affect project milestones. Long lead times can delay hyperscale and enterprise go-lives, especially for build-to-suit facilities.

Supply Chain Disruptions and Lack of Local Manufacturing Capabilities Affect Rack Availability

The region depends heavily on imported rack systems and accessories, exposing it to global supply chain risks. Shipping delays, material shortages, and vendor backlogs have disrupted rack deliveries in recent years. The Middle East Data Center Racks Market needs stronger regional production to reduce reliance on international logistics. Lack of local fabrication also affects the ability to meet urgent or small-batch rack demands. Some vendors struggle with regional compliance or thermal design adaptation for harsh climates. Delays in obtaining rack accessories like PDUs, brackets, or containment doors further affect deployment timelines. Standardization efforts remain fragmented, limiting scalability across multi-site rollouts. Building resilient local manufacturing and logistics is critical to mitigate these structural challenges.

Market Opportunities

Expansion of Smart Infrastructure and AI Workloads Unlocks New High-Density Rack Use Cases

The rise of AI, IoT, and smart infrastructure creates fresh opportunities for deploying high-performance racks. These workloads demand compact, thermally optimized racks with integrated power and sensor features. The Middle East Data Center Racks Market offers growth potential in AI-specific rack models that support GPU trays and liquid-cooling. Government-backed digital projects and AI research hubs will drive long-term rack demand. Vendors can expand by launching region-specific designs aligned with sovereign infrastructure needs.

Localization, Green Standards, and Edge Infrastructure Development Enable Market Penetration

Regional players have an opportunity to serve demand for sustainable and compliant rack systems. Racks optimized for PUE targets, low-carbon materials, and efficient cooling gain traction. The Middle East Data Center Racks Market enables vendors to collaborate with governments for smart city edge projects. Expansion in secondary markets creates space for localized rack deployments. Custom solutions addressing desert climates, airflow challenges, and telecom edge needs offer strong growth outlook.

Market Segmentation

By Rack Type

Cabinet racks dominate the Middle East Data Center Racks Market due to their enclosed design, cable management, and security benefits. These racks are widely used in hyperscale and enterprise environments supporting high-density deployments. Open-frame racks are preferred in smaller setups and testing environments for ease of access. Cabinet racks offer better airflow control and are compatible with advanced cooling configurations. Growth is driven by cloud providers and colocation facilities requiring scalable and secure configurations.

By Rack Height

42U racks lead the segment due to their standardization and compatibility across diverse IT workloads. These racks balance density, cooling efficiency, and space optimization. Above 42U racks are gaining share due to hyperscale deployments requiring larger capacity per rack. Below 42U racks serve edge and SMB deployments with limited space. The Middle East Data Center Racks Market favors scalable rack heights aligned with power and cooling advancements.

By Width

The 19-inch width segment holds the highest share due to global compatibility and widespread use in network and server environments. It supports standardized IT equipment, PDUs, and cable systems. The 23-inch segment is growing in high-density scenarios needing additional airflow space and cable routing. Other width variants serve niche applications. The Middle East Data Center Racks Market supports width flexibility to match varied vertical demands.

By Application

Server racks dominate application share due to the growing compute density in hyperscale and enterprise data centers. These racks support mission-critical servers and offer strong structural integrity. Network racks are used extensively in telco and colocation environments for structured cabling and switch deployment. The Middle East Data Center Racks Market reflects growth in server rack demand driven by cloud computing and AI workloads.

By End-user

Large data centers are the primary end-user segment, driven by investments from hyperscale and government-backed digital projects. These facilities demand high-capacity racks with smart power and cooling integrations. Small and mid-sized data centers adopt open-frame or modular cabinets based on budget and floor space. The Middle East Data Center Racks Market supports flexible rack solutions across different operator profiles.

By Vertical

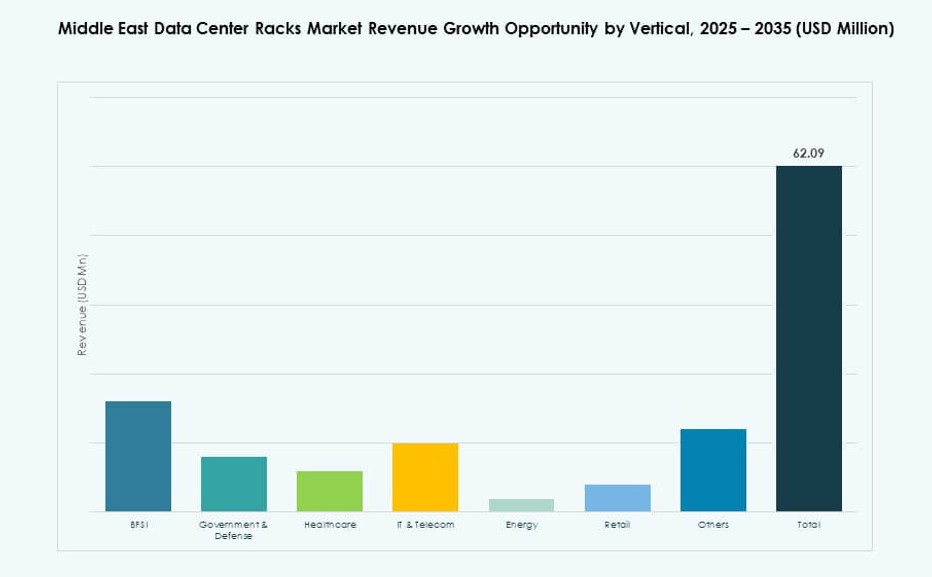

The IT & telecom sector leads due to ongoing digitization, 5G rollout, and cloud adoption. Government and defense follow closely, focusing on sovereign cloud and AI infrastructure. BFSI drives secure, redundant rack deployments for sensitive workloads. Healthcare requires high-availability systems for real-time data processing. Retail, energy, and others contribute to rising demand through e-commerce, grid monitoring, and smart logistics. The Middle East Data Center Racks Market serves all verticals with tailored rack configurations.

Regional Insights

GCC Subregion Dominates Market Share Due to Hyperscale Projects and Cloud Expansion

The GCC region accounts for over 68% of the Middle East Data Center Racks Market, led by the UAE and Saudi Arabia. These countries host hyperscale campuses, cloud availability zones, and sovereign data infrastructure programs. Their demand for high-density, liquid-ready, and AI-optimized rack systems continues to grow. Saudi Arabia’s NEOM and Riyadh hub developments support large-scale deployments. The UAE remains a regional hub for colocation and global cloud firms expanding rack footprints.

Levant Region Shows Steady Growth with Increasing Edge and Enterprise Rack Deployments

The Levant region, including Israel and Jordan, holds about 19% of the Middle East Data Center Racks Market. Israel leads in AI and HPC, requiring advanced racks supporting GPU clusters and direct cooling systems. Jordan’s telecom sector and enterprise cloud adoption drive steady growth in modular rack needs. Demand focuses on compact, secure racks for local facilities. The region benefits from strong tech innovation and government investment in digital infrastructure.

- For instance, Oracle Cloud’s Tel Aviv region supports AI and HPC workloads through GPU-accelerated instances deployed across its hyperscale infrastructure, aligned with national digital and cybersecurity priorities.

Emerging Middle East Markets Show Rising Potential for Edge-Optimized Rack Systems

Remaining Middle East countries, including Iraq, Oman, and Bahrain, contribute 13% share in the Middle East Data Center Racks Market. These regions focus on expanding digital infrastructure through smart city initiatives and localized compute nodes. Edge racks with 19-inch configurations and integrated power systems gain popularity. Operators deploy racks in constrained and high-temperature environments, pushing demand for resilient, space-efficient designs. Growth is expected to accelerate with increased telecom and government data programs.

- For instance, Gulf Data Hub has planned new data center capacity in Bahrain designed to support high-temperature operations and edge computing requirements, aligned with regional demand for modular rack deployments.

Competitive Insights:

- Schneider Electric

- Vertiv Group

- Rittal

- Eaton

- Cisco Systems, Inc.

- Hewlett Packard Enterprise (HPE)

- Dell Inc.

- Legrand

- Gulf Racks

- Powerware Enclosures

The Middle East Data Center Racks Market features a mix of global OEMs and regional rack specialists. Global vendors like Schneider Electric, Vertiv, and Rittal dominate large-scale deployments with modular, high-density cabinet solutions. Eaton, Cisco, and HPE lead in power-integrated and smart rack systems tailored for enterprise and hyperscale use. Regional players such as Gulf Racks and Powerware Enclosures offer locally manufactured, cost-effective alternatives aligned with regional climate and compliance needs. Competition is driven by design flexibility, cooling integration, and sustainability features. Companies focus on partnerships with hyperscalers and colocation providers to expand rack footprints. Product differentiation relies on thermal management, sensor integration, and rack-level efficiency. The market rewards players that offer quick deployment, compliance, and customization across government and private sector infrastructure builds.

Recent Developments:

- In August 2025, Vertiv completed its acquisition of Great Lakes Data Racks & Cabinets, a leading manufacturer of custom rack enclosures and integrated infrastructure solutions. This strategic move expands Vertiv’s portfolio of rack, cabinet, and white space products. It enhances Vertiv’s ability to deliver pre‑engineered solutions for high‑density, AI and edge computing environments.

- In May 2025, G42 and US hyperscalers confirmed plans for a 5 GW AI campus in the UAE, driving demand for record numbers of liquid-cooling-ready data center racks in the Middle East market.

- In May 2025, NVIDIA partnered with Saudi Arabia’s Humain to construct 500 MW AI factories using 18,000 GB300 systems, requiring extreme-density rack enclosures tailored for the region’s data center needs.

- In October 2024, Schneider Electric opened a new manufacturing facility in the UAE aimed at producing AI‑ready data center infrastructure, including modular and prefabricated rack solutions. The facility supports the UAE’s “Make it in the Emirates” strategy and the In‑Country Value program. It enables faster deployment of scalable, energy‑efficient digital infrastructure across the region.