Executive summary:

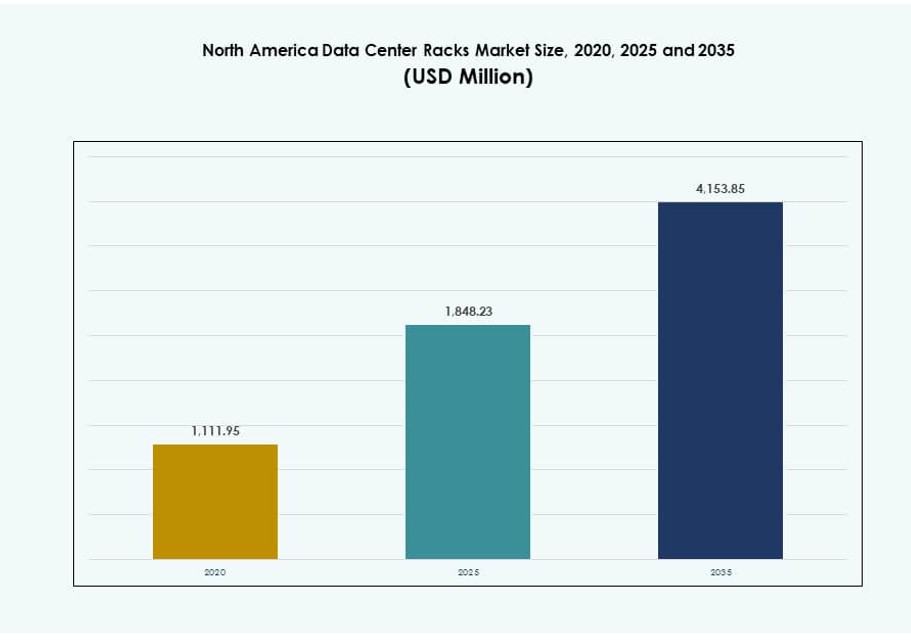

The North America Data Center Racks Market size was valued at USD 1,111.95 million in 2020 to USD 1,848.23 million in 2025 and is anticipated to reach USD 4,153.85 million by 2035, at a CAGR of 8.39% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2035 |

| North America Data Center Racks Market Size 2025 |

USD 1,848.23 Million |

| North America Data Center Racks Market, CAGR |

8.39% |

| North America Data Center Racks Market Size 2035 |

USD 4,153.85 Million |

Growth in the North America Data Center Racks Market is driven by AI-focused compute expansion, cloud service provider infrastructure upgrades, and edge data center rollouts. Enterprises and hyperscale operators are rapidly adopting high-density, liquid-ready rack systems to support power-hungry GPU clusters. Smart racks with built-in telemetry, modular integration, and compliance-friendly designs are in high demand. These infrastructure shifts align with energy efficiency mandates and the need for scalable operations. Strategic investments in standardized rack solutions reduce deployment timelines and lifecycle costs. Businesses benefit from unified infrastructure planning across facilities. Investors focus on long-term contracts and dense workloads that drive recurring rack procurement.

The United States leads the North America Data Center Racks Market with dominant hyperscale deployment volumes and strong enterprise modernization momentum. High regional demand stems from AI, cloud, and colocation investments. Canada follows as an emerging leader, with green data center initiatives and regional colocation growth across key metros like Toronto and Montreal. Mexico continues to expand its market position through manufacturing sector digitization and edge infrastructure development. While the U.S. drives volume and innovation, Canada and Mexico represent growth corridors with cost advantages and policy support. Regional dynamics favor vendors offering flexible, modular, and density-optimized rack formats.

Market Dynamics:

Market Drivers

Expansion Of Hyperscale And Colocation Data Center Footprints

The North America Data Center Racks Market benefits from rapid hyperscale campus expansion. Cloud operators deploy standardized racks at scale across new facilities. Rack density needs rise with AI and analytics workloads. Operators seek designs that support higher power loads. Thermal control needs push advanced rack layouts. Supply chain maturity supports faster rack delivery. Investors value predictable demand from long-term leases. Rack vendors gain from repeat procurement cycles. Strategic procurement frameworks increase rack deployment efficiency. Multi-region rollouts boost annualized rack volume.

Enterprise Shift Toward High-Density And AI-Ready Infrastructure

Enterprises modernize infrastructure to support AI training and inference. The North America Data Center Racks Market aligns with GPU-heavy deployments. High-density racks support accelerated computing platforms. Power distribution design becomes a core selection factor. Liquid-ready rack frames gain preference. Enterprises reduce floor space through vertical scale. This shift improves capital efficiency for operators. Investors view density gains as margin drivers. High-density adoption also drives custom rack configurations. Infrastructure teams adopt modular kits for faster scaling.

- For instance, hyperscalers re-architected rack designs to support densities between 10 and 50 kW per rack by late 2025, with companies like Meta, Google, and AWS deploying AI-specific infrastructure across U.S. sites such as Meta’s Prineville, Oregon campus for large-scale GPU workloads.

Standardization And Modular Design Adoption Across Facilities

Data center operators favor repeatable rack architectures. The North America Data Center Racks Market reflects strong modular adoption. Standard sizes simplify planning and deployment cycles. Operators reduce design complexity across regions. Modular racks support phased capacity rollout. Maintenance teams benefit from uniform components. This approach lowers operational risk. Vendors scale production with consistent specifications. Global design templates reduce engineering overhead. Interchangeable parts support fast break-fix operations.

- For instance, Google expanded its modular infrastructure in North American regions like Dallas in 2025, leveraging standardized, repeatable rack and power designs to accelerate deployment timelines for AI and cloud capacity, following a model similar to AWS’s availability zone architecture.

Focus On Operational Resilience And Compliance Requirements

Operators prioritize uptime and compliance mandates. The North America Data Center Racks Market supports resilience-focused designs. Seismic-rated racks address regional risk profiles. Security-ready cabinets protect critical workloads. Compliance standards shape material and locking choices. Enterprises demand audit-ready infrastructure. This focus increases average rack value. Long-term contracts attract institutional investors. Tier-specific rack formats meet evolving redundancy requirements. Infrastructure teams align racks with facility hardening standards.

Market Trends

Rising Preference For Liquid-Ready And Hybrid Cooling Rack Designs

The North America Data Center Racks Market shows strong interest in liquid-ready frames. Operators prepare facilities for future cooling shifts. Hybrid air and liquid compatibility gains traction. Rack vendors redesign airflow paths. Structural strength supports heavier heat exchangers. Early adoption reduces retrofit risk. Buyers favor future-proof designs. This trend reshapes product roadmaps. OEMs partner with liquid cooling firms for integrated offerings. Procurement criteria now include cooling compatibility.

Integration Of Smart Monitoring And Rack-Level Telemetry

Rack intelligence adoption expands across large facilities. The North America Data Center Racks Market integrates sensors at rack level. Operators track temperature and power in real time. Telemetry improves fault detection speed. Data feeds support automation platforms. Visibility reduces manual inspection needs. Smart racks align with software-defined operations. Vendors invest in embedded monitoring features. Predictive maintenance models use telemetry as baseline. Smart racks now influence long-term TCO models.

Growth Of Edge And Regional Data Center Deployments

Edge facilities gain importance near demand centers. The North America Data Center Racks Market adapts to smaller footprints. Compact racks suit regional and metro sites. Deployment speed becomes a purchase factor. Pre-configured racks support fast commissioning. Operators balance scale with proximity. This trend broadens customer profiles. Vendors target flexible product lines. Logistics-focused regions drive modular rack kits. Edge DCs adopt localized rack sourcing to reduce lead times.

Sustainability-Driven Rack Material And Design Choices

Sustainability goals influence infrastructure procurement. The North America Data Center Racks Market reflects low-impact material use. Lightweight alloys reduce transport emissions. Design efficiency lowers cooling demand. Operators align racks with green certifications. Procurement teams assess lifecycle impact. Sustainability improves brand perception. Investors favor assets with ESG alignment. Recyclable components improve end-of-life planning. ESG metrics now factor into vendor selection.

Market Challenges

Rising Power Density Creating Thermal And Structural Constraints

The North America Data Center Racks Market faces pressure from extreme power density. Traditional rack frames face load limitations. Heat concentration stresses airflow design. Structural upgrades increase capital needs. Operators must coordinate with facility teams. Retrofit complexity raises project timelines. Supply delays affect deployment schedules. This challenge tests engineering adaptability. Variable site power availability further constrains rack deployment. Advanced designs increase integration complexity at the facility level.

Supply Chain Volatility And Cost Pressure On Rack Components

Component sourcing remains uneven across regions. The North America Data Center Racks Market experiences material price swings. Steel and specialty parts face lead-time risk. Vendors manage inventory exposure carefully. Operators face budget planning challenges. Contract pricing becomes less predictable. Smaller buyers face procurement disadvantage. This pressure shapes vendor selection strategies. Fluctuating logistics costs increase landed rack prices. Currency fluctuations also disrupt sourcing plans.

Market Opportunities

Growth In AI-Specific And High-Performance Rack Solutions

AI workloads demand specialized infrastructure designs. The North America Data Center Racks Market supports tailored AI rack solutions. Vendors develop GPU-optimized frames. Power and cooling integration creates value. Operators seek turnkey rack systems. Early movers gain pricing leverage. This opportunity attracts strategic partnerships. Innovation cycles accelerate product differentiation. AI clusters require 50–100kW rack support. This drives niche high-margin product categories.

Expansion Of Managed And Pre-Integrated Rack Offerings

Operators prefer simplified deployment models. The North America Data Center Racks Market supports pre-integrated racks. Vendors bundle power, cooling, and monitoring. This approach shortens deployment time. Service providers reduce on-site labor. Enterprises favor predictable outcomes. Margins improve through value-added offerings. This model appeals to new entrants. Lifecycle service bundles gain traction across procurement cycles. Racks-as-a-service models are gaining early adopters.

Market Segmentation

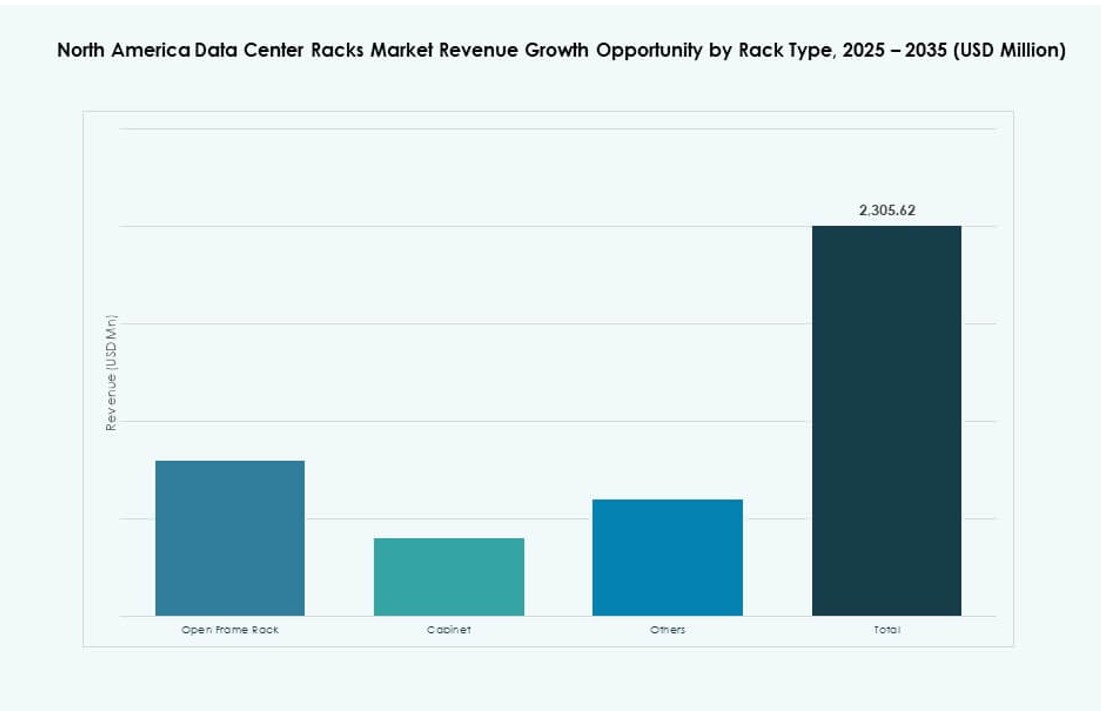

By Rack Type

The North America Data Center Racks Market shows strong dominance of cabinet racks. Cabinets lead due to security and airflow control. Hyperscale and enterprise sites favor enclosed designs. Open frame racks serve controlled environments. Others address niche industrial needs. Cabinet racks hold the largest share. Growth links to compliance and density needs. Vendors prioritize advanced cabinet features. Rack-based airflow optimization is more advanced in cabinets. Locking and cable management features also improve.

By Rack Height

Rack height selection reflects density strategies. The North America Data Center Racks Market sees strong demand for above 42U racks. Taller racks maximize vertical space use. Hyperscale facilities adopt higher profiles. Standard 42U remains common in legacy sites. Below 42U suits edge locations. Height choice links to cooling design. Operators seek flexibility across sites. High racks reduce real estate cost per server. Integration with hot-aisle containment improves cooling efficiency.

By Width

Width standards shape compatibility and scalability. The North America Data Center Racks Market favors 19-inch racks. This format supports most IT equipment. 23-inch racks serve telecom applications. Others address custom deployments. The 19-inch segment holds majority share. Growth follows server standardization. Vendors maintain broad accessory ecosystems. Width consistency simplifies procurement. Narrower racks allow for denser aisle configurations. Retrofit projects prefer industry-standard widths for minimal disruption.

By Application

Server racks dominate application demand. The North America Data Center Racks Market reflects server-heavy workloads. Compute expansion drives rack volume. Network racks support switching and routing layers. Server racks capture higher spending share. AI and cloud boost server density. Network racks grow with east-west traffic. Application mix mirrors workload evolution. Server racks often include power rails and blanking panels. Network racks prioritize cable airflow and side access.

By End-user

Large data centers lead rack consumption. The North America Data Center Racks Market aligns with hyperscale demand. Large sites deploy racks at scale. Small and mid-sized centers adopt modular units. Large operators hold dominant share. Growth ties to cloud expansion. Smaller users value flexibility. End-user needs influence design choices. Multi-tenant facilities deploy diverse rack formats. Customization remains limited for SMB-focused products.

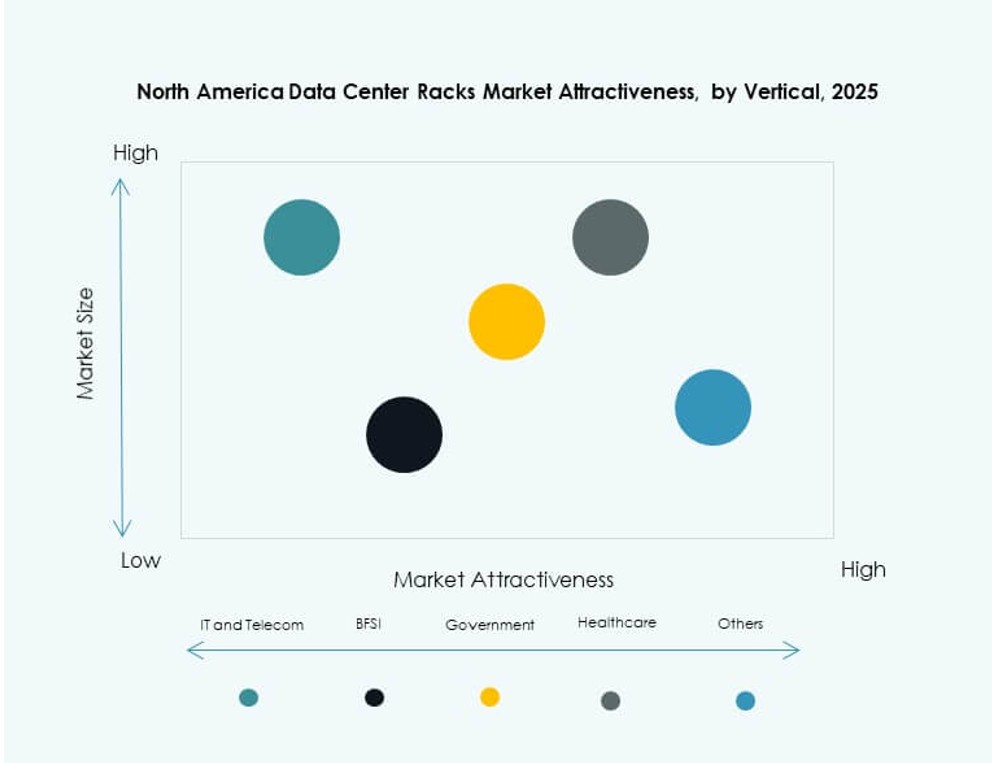

By Vertical

IT and telecom dominate vertical demand. The North America Data Center Racks Market serves digital service providers. BFSI follows with secure infrastructure needs. Government and defense require compliant designs. Healthcare demand rises with data growth. Energy and retail adopt digital platforms. IT and telecom hold the largest share. Vertical needs shape customization depth. Racks with EMI shielding serve defense applications. Healthcare racks focus on security and cooling.

Regional Insights

Regional Insights

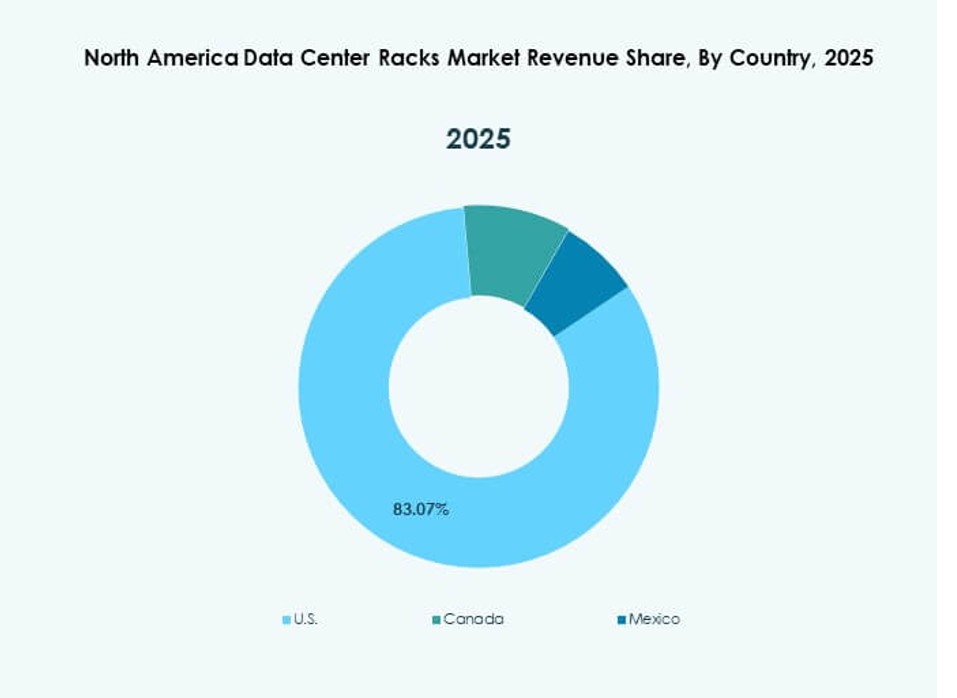

United States

The North America Data Center Racks Market sees the United States holding around 72% share. Hyperscale cloud investment drives demand. Enterprise IT modernization supports steady growth. AI clusters increase rack density needs. Colocation expansion fuels repeat orders. Strong vendor presence supports innovation. Regulatory clarity aids long-term planning. Racks are part of large-scale design-build contracts. U.S. buyers favor integrated rack-cooling bundles.

- For instance, Microsoft has deployed liquid-cooled racks in its U.S. Azure data centers to support large-scale GPU clusters for OpenAI workloads, with confirmed use of high-density infrastructure and advanced thermal solutions.

Canada

Canada accounts for nearly 18% market share. The North America Data Center Racks Market benefits from green data center growth. Cooler climates support efficient operations. Colocation investment rises in key metros. Enterprises adopt modern rack standards. Sustainability goals influence procurement. Stable policy supports infrastructure expansion. Canadian government incentives aid local deployment. Demand grows in Toronto, Montreal, and Vancouver corridors.

Mexico

Mexico holds close to 10% share and shows fast growth. The North America Data Center Racks Market expands with nearshoring trends. Manufacturing digitization boosts regional demand. Edge facilities support logistics networks. Cost advantages attract new deployments. Rack demand rises from regional data hubs. Growth outlook remains positive. Cloud services are expanding into industrial cities. National infrastructure policies support digital adoption.

- For instance, Equinix opened its first Mexico City data center (MX1) with 224 racks supporting up to 10 kW per rack, designed to host hybrid cloud and edge workloads in a high-availability environment.

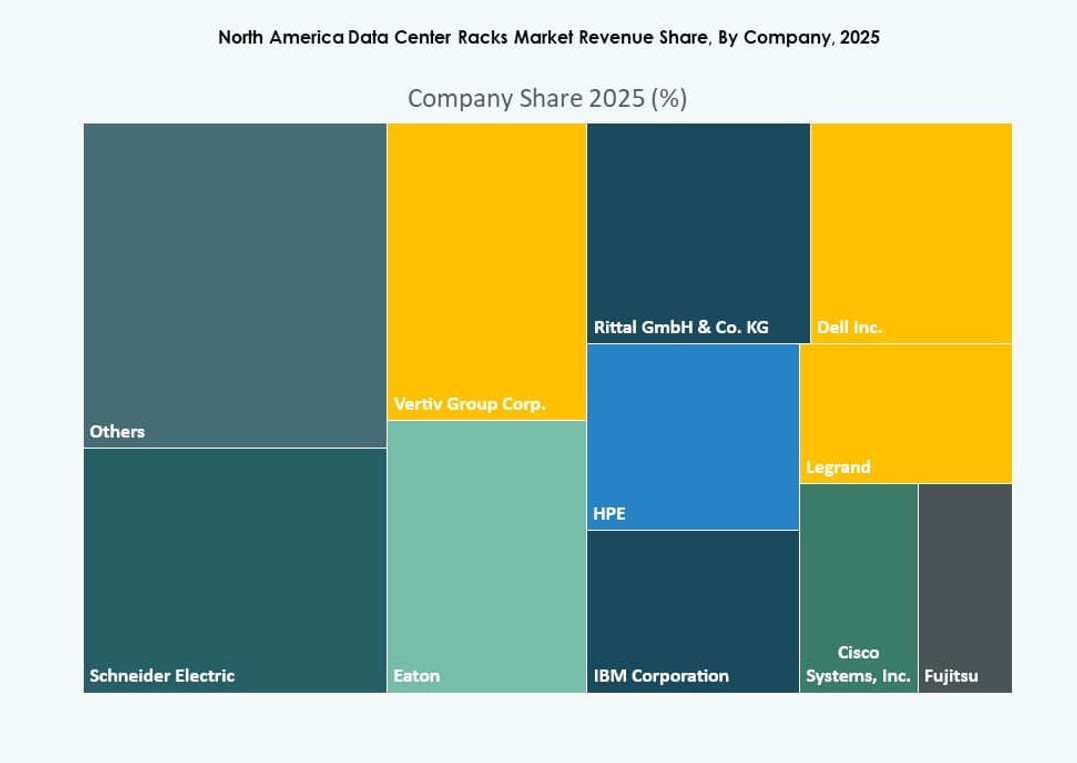

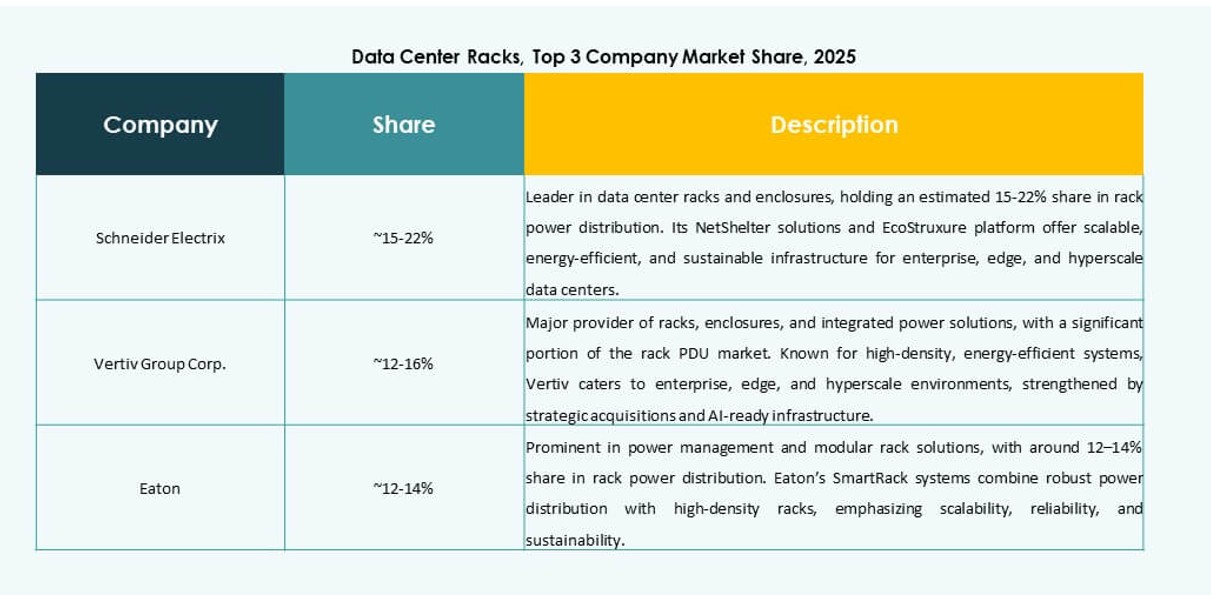

Competitive Insights:

- Schneider Electric

- Vertiv Group

- Rittal

- Eaton

- AMCO Enclosures

- Belden Inc.

- Chatsworth Products

- Cisco Systems, Inc.

- Dell Inc.

- Hewlett Packard Enterprise (HPE)

The North America Data Center Racks Market features strong competition driven by hyperscale and enterprise demand. It is led by established infrastructure providers offering cabinet, high-density, and integrated rack solutions. Vendors focus on pre-integrated offerings, liquid-cooling compatibility, and modular designs to win large-scale contracts. Companies such as Schneider Electric and Vertiv dominate with extensive regional presence and thermal management integration. Mid-sized players target edge deployments and niche customization. The market rewards players with flexible production and rapid deployment capabilities. Partnerships with hyperscalers and telecom firms influence regional volume share. Innovation in smart racks, sustainability, and high-density formats shapes differentiation across portfolios.

Recent Developments:

- In July 2025, Vertiv acquired Great Lakes Data Racks & Cabinets for approximately USD 200 million, expanding its portfolio of high-density, AI-ready rack solutions to meet surging demand in hyperscale data centers.

- In May 2025, Vertiv launched an 800 VDC power architecture designed for AI-focused data centers. The solution features centralized rectifiers with rack-level power conversion. While power-centric, the architecture directly supports high-density rack deployments by reducing copper usage and improving energy efficiency.

- In January 2024, Eaton introduced a new range of high-density rack enclosures designed to optimize cooling and space utilization in next-generation data centers.